HealthEquity PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain an edge with our PESTLE analysis of HealthEquity. It reveals political, economic, social, technological, legal, and environmental forces shaping strategy and risk. Buy the full, editable report for actionable insights and instant download.

Political factors

Tax policy and HSA favorability

HSAs depend on federal tax exemptions set by Congress/IRS; 2024 contribution limits are $4,150 individual/$8,300 family and there are over 33 million HSA accounts nationwide, highlighting scale. Any tax reform could change deductibility or eligible expenses, and election cycles periodically revive proposals to cap exclusions. Bipartisan support has been stable, so HealthEquity must monitor policy shifts and actively advocate to preserve HSA advantages.

Healthcare reform and HDHP incentives

Policy shifts to the ACA or employer-sponsored coverage directly affect HDHP adoption, the primary feeder for HSAs: IRS 2025 HSA limits are $4,300 individual/$8,650 family with HDHP minimum deductibles $1,650/$3,300. Incentives or mandates that reduce HDHP prevalence would slow HSA deposit and account growth, while policies promoting consumer-directed care (tax incentives, portability rules) can accelerate openings. Strategic alignment with benefit-design trends is critical for HealthEquity to capture flow of new HSAs.

Medicare and Medicaid coordination

Rules on HSA eligibility for those approaching Medicare constrain contribution windows and rollovers; 2025 IRS HSA limits are $4,150 individual/$8,300 family, shaping last-year contributions. Medicaid expansion in 40 states plus DC shifts employer coverage mixes and shrinks HSA addressable markets. Clarified dual-eligible rules (≈12.5M duals) reduce compliance friction and clear guidance cuts participant confusion and attrition.

Government procurement and public sector employers

Public sector adoption of HSAs varies with state budgets and political leadership, producing asymmetric uptake across states. RFP cycles and procurement rules typically set onboarding timelines of 6–18 months and materially shape pricing. Winning statewide mandates can deliver scale (hundreds of thousands to millions of members) and requires sustained policy fluency; HealthEquity advocacy can open attractive public pools.

- State budget & leadership: determines HSA adoption pace

- RFP cycles 6–18 months: affect onboarding & pricing

- Statewide mandates: potential for large-scale membership

- Advocacy: key to accessing public employer pools

Geopolitical and fiscal priorities

Federal deficit pressure—US net borrowing exceeded $1.6 trillion in FY2023 (Treasury)—raises scrutiny of tax expenditures, putting HSA tax advantages at greater risk during budget negotiations.

Shifts in Congressional leadership, notably the House change in Jan 2023, reshape committee agendas and can delay or reprioritize benefits policy and HSA reform.

Macroeconomic shocks divert political capital from benefits modernization, while a stable policy outlook enables HealthEquity to pursue multi-year product investments.

- Deficit: FY2023 > $1.6T (Treasury)

- Congress: House leadership shift Jan 2023

- Impact: funding scrutiny, delayed reforms

- Opportunity: stability = long-term investment

HSA demand steadies; ~33M accounts and federal limits face deficit risk

Federal tax treatment and IRS limits (2025 HSA limits $4,300 individual/$8,650 family) and ~33M HSA accounts sustain demand, but deficit pressure (FY2023 net borrowing >$1.6T) raises risk to exclusions. HDHP adoption drives flows—Medicaid expansion in 40 states+DC shrinks employer-addressable market; ~12.5M dual-eligibles constrain contributions. State procurement/RFPs (6–18 months) and targeted advocacy can unlock large public pools.

| Metric | Value |

|---|---|

| HSA accounts | ~33M |

| 2025 HSA limits | $4,300/$8,650 |

| FY2023 net borrowing | >$1.6T |

| Medicaid expansion | 40 states + DC |

| Dual-eligibles | ~12.5M |

| RFP/onboarding | 6–18 months |

What is included in the product

Explores how macro-environmental factors uniquely affect HealthEquity across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, forward-looking insights and detailed sub-points to help executives, investors, and strategists identify risks and opportunities.

Condenses HealthEquity's full PESTLE into a clean, visually segmented summary for quick reference, easy sharing, and drop‑in use in presentations, while allowing note additions to tailor insights to specific regions or business lines.

Economic factors

Interest rate environment and custodial yields

Net interest revenue on HSA cash balances tracks benchmark rates (federal funds 5.25–5.50% as of mid‑2025); rising rates expand custodial income while falling rates compress margins. Asset allocation between cash (cash yields ~4% in 2024) and invested HSA balances shifts the revenue mix and volatility exposure. Hedging and pricing levers can smooth short‑term swings in custodial yields.

Healthcare inflation and out-of-pocket costs

Rising medical costs increase demand for tax-advantaged saving and payment tools as consumers face higher out-of-pocket burdens; HSA contribution limits for 2024 were $4,150 individual and $8,300 family, which can shift more funds into HSAs. Higher deductibles commonly drive HSA contributions and utilization, but severe cost pressure can reduce capacity to save. HealthEquity’s education programs can optimize funding behavior and plan use.

Employment levels and wage growth

Employer-sponsored plans, covering roughly 155 million Americans, drive HSA eligibility so tight labor markets (U.S. unemployment ~3.8% mid‑2025) expand HealthEquity’s addressable base. Wage growth—average hourly earnings up ~4% YoY in 2024—increases contribution capacity and investment propensity, while layoffs or part‑time shifts reduce new accounts and contributions. Diversified employer channels help buffer cyclicality.

Market performance and investment revenue

HSA investment options generate fees linked to asset levels; industry HSA assets reached $117.7B at year-end 2023 (Devenir), so bull markets (S&P 500 +26.3% in 2023) can sharply boost AUM and trading, while downturns depress balances. Thoughtful product design and glidepaths help sustain participation through cycles, and low-cost ETFs (VTI expense 0.03%) plus advice can retain investors.

- Fees tied to AUM: higher in bull markets

- Market swings drive engagement and balances

- Glidepaths sustain long-term participation

- Low-cost ETFs and advice reduce attrition

Consolidation among benefits platforms

Consolidation among payroll, recordkeepers, and health plans is reshaping partnership economics, enabling scale players to demand lower fees while simultaneously broadening distribution for platforms like HealthEquity. Integration moats and high switching costs favor established administrators, making competitor displacements costly for employers and brokers. HealthEquity can defend margins by leveraging cross-sell of HSAs, COBRA, and FSA services across its client base.

- Scale pressure on pricing

- Broader distribution via large partners

- Integration moats protect incumbents

- Cross-sell as margin defense

HSA demand steadies; ~33M accounts and federal limits face deficit risk

Interest rates (fed funds 5.25–5.50% mid‑2025; cash yields ~4% in 2024) drive custodial income and margin volatility. Rising medical costs and 2024 HSA limits ($4,150 individual / $8,300 family) boost demand but cost pressure can curb savings. Employer coverage (~155M), unemployment ~3.8% mid‑2025 and wage growth (~4% YoY 2024) shape addressable base and contribution capacity.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| Cash yield | ~4% (2024) |

| HSA assets | $117.7B (2023) |

| Employer coverage | ~155M |

Preview Before You Purchase

HealthEquity PESTLE Analysis

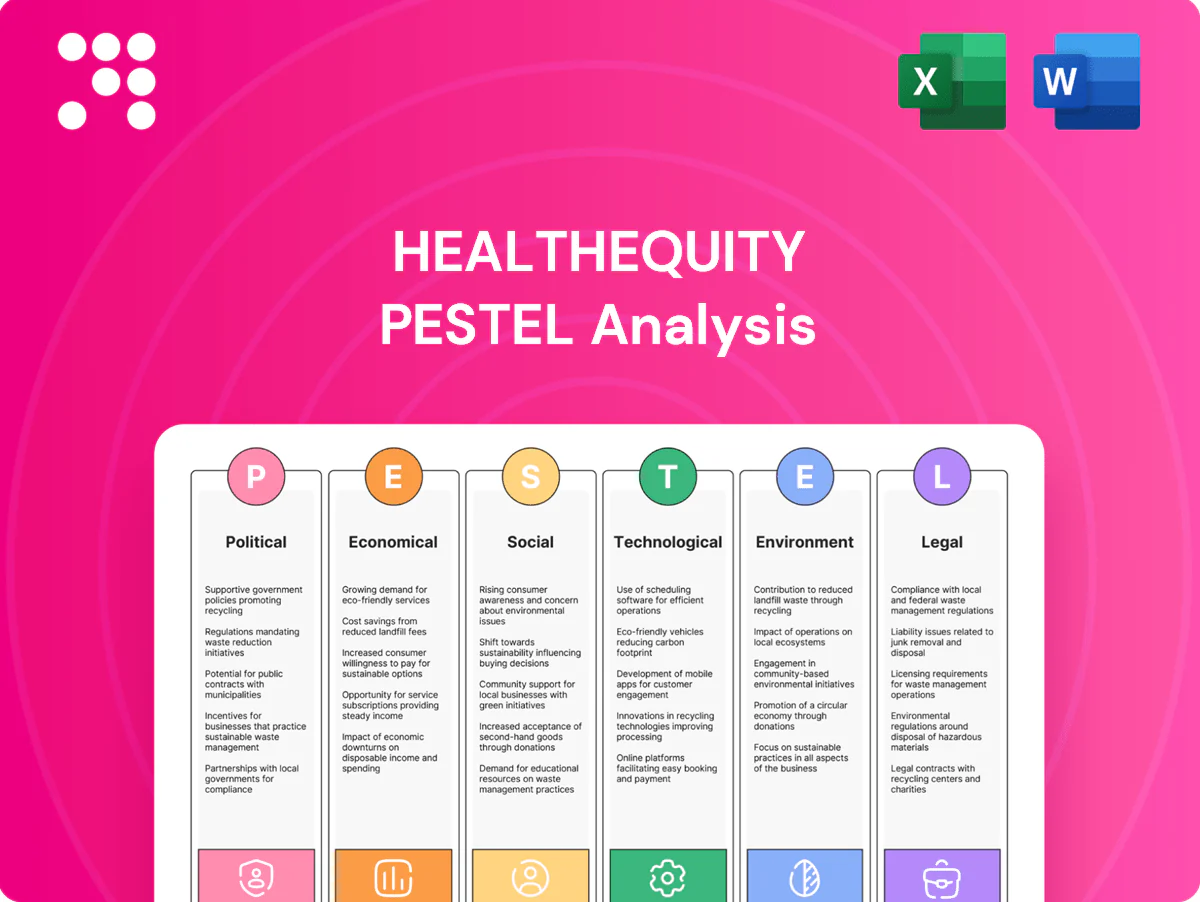

The preview shown here is the exact HealthEquity PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors relevant to HealthEquity. No placeholders or teasers—this is the final file available for immediate download.

Your Shortcut to Market Insight Starts Here

Gain an edge with our PESTLE analysis of HealthEquity. It reveals political, economic, social, technological, legal, and environmental forces shaping strategy and risk. Buy the full, editable report for actionable insights and instant download.

Political factors

Tax policy and HSA favorability

HSAs depend on federal tax exemptions set by Congress/IRS; 2024 contribution limits are $4,150 individual/$8,300 family and there are over 33 million HSA accounts nationwide, highlighting scale. Any tax reform could change deductibility or eligible expenses, and election cycles periodically revive proposals to cap exclusions. Bipartisan support has been stable, so HealthEquity must monitor policy shifts and actively advocate to preserve HSA advantages.

Healthcare reform and HDHP incentives

Policy shifts to the ACA or employer-sponsored coverage directly affect HDHP adoption, the primary feeder for HSAs: IRS 2025 HSA limits are $4,300 individual/$8,650 family with HDHP minimum deductibles $1,650/$3,300. Incentives or mandates that reduce HDHP prevalence would slow HSA deposit and account growth, while policies promoting consumer-directed care (tax incentives, portability rules) can accelerate openings. Strategic alignment with benefit-design trends is critical for HealthEquity to capture flow of new HSAs.

Medicare and Medicaid coordination

Rules on HSA eligibility for those approaching Medicare constrain contribution windows and rollovers; 2025 IRS HSA limits are $4,150 individual/$8,300 family, shaping last-year contributions. Medicaid expansion in 40 states plus DC shifts employer coverage mixes and shrinks HSA addressable markets. Clarified dual-eligible rules (≈12.5M duals) reduce compliance friction and clear guidance cuts participant confusion and attrition.

Government procurement and public sector employers

Public sector adoption of HSAs varies with state budgets and political leadership, producing asymmetric uptake across states. RFP cycles and procurement rules typically set onboarding timelines of 6–18 months and materially shape pricing. Winning statewide mandates can deliver scale (hundreds of thousands to millions of members) and requires sustained policy fluency; HealthEquity advocacy can open attractive public pools.

- State budget & leadership: determines HSA adoption pace

- RFP cycles 6–18 months: affect onboarding & pricing

- Statewide mandates: potential for large-scale membership

- Advocacy: key to accessing public employer pools

Geopolitical and fiscal priorities

Federal deficit pressure—US net borrowing exceeded $1.6 trillion in FY2023 (Treasury)—raises scrutiny of tax expenditures, putting HSA tax advantages at greater risk during budget negotiations.

Shifts in Congressional leadership, notably the House change in Jan 2023, reshape committee agendas and can delay or reprioritize benefits policy and HSA reform.

Macroeconomic shocks divert political capital from benefits modernization, while a stable policy outlook enables HealthEquity to pursue multi-year product investments.

- Deficit: FY2023 > $1.6T (Treasury)

- Congress: House leadership shift Jan 2023

- Impact: funding scrutiny, delayed reforms

- Opportunity: stability = long-term investment

HSA demand steadies; ~33M accounts and federal limits face deficit risk

Federal tax treatment and IRS limits (2025 HSA limits $4,300 individual/$8,650 family) and ~33M HSA accounts sustain demand, but deficit pressure (FY2023 net borrowing >$1.6T) raises risk to exclusions. HDHP adoption drives flows—Medicaid expansion in 40 states+DC shrinks employer-addressable market; ~12.5M dual-eligibles constrain contributions. State procurement/RFPs (6–18 months) and targeted advocacy can unlock large public pools.

| Metric | Value |

|---|---|

| HSA accounts | ~33M |

| 2025 HSA limits | $4,300/$8,650 |

| FY2023 net borrowing | >$1.6T |

| Medicaid expansion | 40 states + DC |

| Dual-eligibles | ~12.5M |

| RFP/onboarding | 6–18 months |

What is included in the product

Explores how macro-environmental factors uniquely affect HealthEquity across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, forward-looking insights and detailed sub-points to help executives, investors, and strategists identify risks and opportunities.

Condenses HealthEquity's full PESTLE into a clean, visually segmented summary for quick reference, easy sharing, and drop‑in use in presentations, while allowing note additions to tailor insights to specific regions or business lines.

Economic factors

Interest rate environment and custodial yields

Net interest revenue on HSA cash balances tracks benchmark rates (federal funds 5.25–5.50% as of mid‑2025); rising rates expand custodial income while falling rates compress margins. Asset allocation between cash (cash yields ~4% in 2024) and invested HSA balances shifts the revenue mix and volatility exposure. Hedging and pricing levers can smooth short‑term swings in custodial yields.

Healthcare inflation and out-of-pocket costs

Rising medical costs increase demand for tax-advantaged saving and payment tools as consumers face higher out-of-pocket burdens; HSA contribution limits for 2024 were $4,150 individual and $8,300 family, which can shift more funds into HSAs. Higher deductibles commonly drive HSA contributions and utilization, but severe cost pressure can reduce capacity to save. HealthEquity’s education programs can optimize funding behavior and plan use.

Employment levels and wage growth

Employer-sponsored plans, covering roughly 155 million Americans, drive HSA eligibility so tight labor markets (U.S. unemployment ~3.8% mid‑2025) expand HealthEquity’s addressable base. Wage growth—average hourly earnings up ~4% YoY in 2024—increases contribution capacity and investment propensity, while layoffs or part‑time shifts reduce new accounts and contributions. Diversified employer channels help buffer cyclicality.

Market performance and investment revenue

HSA investment options generate fees linked to asset levels; industry HSA assets reached $117.7B at year-end 2023 (Devenir), so bull markets (S&P 500 +26.3% in 2023) can sharply boost AUM and trading, while downturns depress balances. Thoughtful product design and glidepaths help sustain participation through cycles, and low-cost ETFs (VTI expense 0.03%) plus advice can retain investors.

- Fees tied to AUM: higher in bull markets

- Market swings drive engagement and balances

- Glidepaths sustain long-term participation

- Low-cost ETFs and advice reduce attrition

Consolidation among benefits platforms

Consolidation among payroll, recordkeepers, and health plans is reshaping partnership economics, enabling scale players to demand lower fees while simultaneously broadening distribution for platforms like HealthEquity. Integration moats and high switching costs favor established administrators, making competitor displacements costly for employers and brokers. HealthEquity can defend margins by leveraging cross-sell of HSAs, COBRA, and FSA services across its client base.

- Scale pressure on pricing

- Broader distribution via large partners

- Integration moats protect incumbents

- Cross-sell as margin defense

HSA demand steadies; ~33M accounts and federal limits face deficit risk

Interest rates (fed funds 5.25–5.50% mid‑2025; cash yields ~4% in 2024) drive custodial income and margin volatility. Rising medical costs and 2024 HSA limits ($4,150 individual / $8,300 family) boost demand but cost pressure can curb savings. Employer coverage (~155M), unemployment ~3.8% mid‑2025 and wage growth (~4% YoY 2024) shape addressable base and contribution capacity.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| Cash yield | ~4% (2024) |

| HSA assets | $117.7B (2023) |

| Employer coverage | ~155M |

Preview Before You Purchase

HealthEquity PESTLE Analysis

The preview shown here is the exact HealthEquity PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors relevant to HealthEquity. No placeholders or teasers—this is the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Gain an edge with our PESTLE analysis of HealthEquity. It reveals political, economic, social, technological, legal, and environmental forces shaping strategy and risk. Buy the full, editable report for actionable insights and instant download.

Political factors

Tax policy and HSA favorability

HSAs depend on federal tax exemptions set by Congress/IRS; 2024 contribution limits are $4,150 individual/$8,300 family and there are over 33 million HSA accounts nationwide, highlighting scale. Any tax reform could change deductibility or eligible expenses, and election cycles periodically revive proposals to cap exclusions. Bipartisan support has been stable, so HealthEquity must monitor policy shifts and actively advocate to preserve HSA advantages.

Healthcare reform and HDHP incentives

Policy shifts to the ACA or employer-sponsored coverage directly affect HDHP adoption, the primary feeder for HSAs: IRS 2025 HSA limits are $4,300 individual/$8,650 family with HDHP minimum deductibles $1,650/$3,300. Incentives or mandates that reduce HDHP prevalence would slow HSA deposit and account growth, while policies promoting consumer-directed care (tax incentives, portability rules) can accelerate openings. Strategic alignment with benefit-design trends is critical for HealthEquity to capture flow of new HSAs.

Medicare and Medicaid coordination

Rules on HSA eligibility for those approaching Medicare constrain contribution windows and rollovers; 2025 IRS HSA limits are $4,150 individual/$8,300 family, shaping last-year contributions. Medicaid expansion in 40 states plus DC shifts employer coverage mixes and shrinks HSA addressable markets. Clarified dual-eligible rules (≈12.5M duals) reduce compliance friction and clear guidance cuts participant confusion and attrition.

Government procurement and public sector employers

Public sector adoption of HSAs varies with state budgets and political leadership, producing asymmetric uptake across states. RFP cycles and procurement rules typically set onboarding timelines of 6–18 months and materially shape pricing. Winning statewide mandates can deliver scale (hundreds of thousands to millions of members) and requires sustained policy fluency; HealthEquity advocacy can open attractive public pools.

- State budget & leadership: determines HSA adoption pace

- RFP cycles 6–18 months: affect onboarding & pricing

- Statewide mandates: potential for large-scale membership

- Advocacy: key to accessing public employer pools

Geopolitical and fiscal priorities

Federal deficit pressure—US net borrowing exceeded $1.6 trillion in FY2023 (Treasury)—raises scrutiny of tax expenditures, putting HSA tax advantages at greater risk during budget negotiations.

Shifts in Congressional leadership, notably the House change in Jan 2023, reshape committee agendas and can delay or reprioritize benefits policy and HSA reform.

Macroeconomic shocks divert political capital from benefits modernization, while a stable policy outlook enables HealthEquity to pursue multi-year product investments.

- Deficit: FY2023 > $1.6T (Treasury)

- Congress: House leadership shift Jan 2023

- Impact: funding scrutiny, delayed reforms

- Opportunity: stability = long-term investment

HSA demand steadies; ~33M accounts and federal limits face deficit risk

Federal tax treatment and IRS limits (2025 HSA limits $4,300 individual/$8,650 family) and ~33M HSA accounts sustain demand, but deficit pressure (FY2023 net borrowing >$1.6T) raises risk to exclusions. HDHP adoption drives flows—Medicaid expansion in 40 states+DC shrinks employer-addressable market; ~12.5M dual-eligibles constrain contributions. State procurement/RFPs (6–18 months) and targeted advocacy can unlock large public pools.

| Metric | Value |

|---|---|

| HSA accounts | ~33M |

| 2025 HSA limits | $4,300/$8,650 |

| FY2023 net borrowing | >$1.6T |

| Medicaid expansion | 40 states + DC |

| Dual-eligibles | ~12.5M |

| RFP/onboarding | 6–18 months |

What is included in the product

Explores how macro-environmental factors uniquely affect HealthEquity across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed, forward-looking insights and detailed sub-points to help executives, investors, and strategists identify risks and opportunities.

Condenses HealthEquity's full PESTLE into a clean, visually segmented summary for quick reference, easy sharing, and drop‑in use in presentations, while allowing note additions to tailor insights to specific regions or business lines.

Economic factors

Interest rate environment and custodial yields

Net interest revenue on HSA cash balances tracks benchmark rates (federal funds 5.25–5.50% as of mid‑2025); rising rates expand custodial income while falling rates compress margins. Asset allocation between cash (cash yields ~4% in 2024) and invested HSA balances shifts the revenue mix and volatility exposure. Hedging and pricing levers can smooth short‑term swings in custodial yields.

Healthcare inflation and out-of-pocket costs

Rising medical costs increase demand for tax-advantaged saving and payment tools as consumers face higher out-of-pocket burdens; HSA contribution limits for 2024 were $4,150 individual and $8,300 family, which can shift more funds into HSAs. Higher deductibles commonly drive HSA contributions and utilization, but severe cost pressure can reduce capacity to save. HealthEquity’s education programs can optimize funding behavior and plan use.

Employment levels and wage growth

Employer-sponsored plans, covering roughly 155 million Americans, drive HSA eligibility so tight labor markets (U.S. unemployment ~3.8% mid‑2025) expand HealthEquity’s addressable base. Wage growth—average hourly earnings up ~4% YoY in 2024—increases contribution capacity and investment propensity, while layoffs or part‑time shifts reduce new accounts and contributions. Diversified employer channels help buffer cyclicality.

Market performance and investment revenue

HSA investment options generate fees linked to asset levels; industry HSA assets reached $117.7B at year-end 2023 (Devenir), so bull markets (S&P 500 +26.3% in 2023) can sharply boost AUM and trading, while downturns depress balances. Thoughtful product design and glidepaths help sustain participation through cycles, and low-cost ETFs (VTI expense 0.03%) plus advice can retain investors.

- Fees tied to AUM: higher in bull markets

- Market swings drive engagement and balances

- Glidepaths sustain long-term participation

- Low-cost ETFs and advice reduce attrition

Consolidation among benefits platforms

Consolidation among payroll, recordkeepers, and health plans is reshaping partnership economics, enabling scale players to demand lower fees while simultaneously broadening distribution for platforms like HealthEquity. Integration moats and high switching costs favor established administrators, making competitor displacements costly for employers and brokers. HealthEquity can defend margins by leveraging cross-sell of HSAs, COBRA, and FSA services across its client base.

- Scale pressure on pricing

- Broader distribution via large partners

- Integration moats protect incumbents

- Cross-sell as margin defense

HSA demand steadies; ~33M accounts and federal limits face deficit risk

Interest rates (fed funds 5.25–5.50% mid‑2025; cash yields ~4% in 2024) drive custodial income and margin volatility. Rising medical costs and 2024 HSA limits ($4,150 individual / $8,300 family) boost demand but cost pressure can curb savings. Employer coverage (~155M), unemployment ~3.8% mid‑2025 and wage growth (~4% YoY 2024) shape addressable base and contribution capacity.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (mid‑2025) |

| Cash yield | ~4% (2024) |

| HSA assets | $117.7B (2023) |

| Employer coverage | ~155M |

Preview Before You Purchase

HealthEquity PESTLE Analysis

The preview shown here is the exact HealthEquity PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It covers political, economic, social, technological, legal, and environmental factors relevant to HealthEquity. No placeholders or teasers—this is the final file available for immediate download.