Heidelberger Druckmaschinen PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Analyze how regulatory shifts, supply-chain pressures, and Industry 4.0 technologies are reshaping Heidelberger Druckmaschinen’s prospects with our concise PESTLE snapshot; buy the full, editable report now to access actionable risk assessments, growth levers, and strategic recommendations ready for immediate use.

Political factors

EU industrial policy and subsidies

Shifts in EU manufacturing incentives (eg IPCEI grants covering up to ~50% of project costs) shape Heidelberg’s capital and R&D location choices, while access to Digital Europe (€8.2bn 2021‑27) and the Innovation Fund (~€20bn 2020‑30) can cut green-tech/digitalization development costs materially; reduced funding or policy reversals would slow innovation and scale‑up, so monitoring eligibility criteria and local content rules (often >30% EU value‑add) is critical.

Trade tariffs and export controls

As a capital equipment exporter present in over 170 countries, Heidelberg faces tariff volatility on machinery and components, with MFN tariffs for electrical machinery ranging regionally up to about 14% (WTO/UNCTAD 2023 data).

Export controls on electronics and advanced drives tightened in 2023–24, disrupting procurement and shipments to sensitive markets and requiring license checks for certain drives and controls.

Strategic sourcing and multi-country assembly can shift value to lower-tariff jurisdictions and mitigate exposure, while proactive compliance and export licensing reduce delay and seizure risks in key markets.

Geopolitical supply chain risks

Regional tensions have pushed logistics costs up about 15% and extended lead times for precision parts by roughly 20% for European machinery makers, increasing working capital needs for Heidelberger Druckmaschinen. Diversifying suppliers across Europe, Asia and the Americas into three regional pools reduces single-point failures and mitigates >50% of supplier-concentration risk. Nearshoring critical assemblies can cut lead times by ~30% and lower transport spend; scenario planning that models 3–5 disruption scenarios helps balance inventory levels against service targets.

Public procurement and industrial alliances

Government-backed education and training centers routinely procure print equipment, and EU public procurement represents about 14% of GDP (Eurostat), creating steady demand. Participation in national industry alliances opens pilot and demonstration opportunities; transparent tenders favor compliant, energy-efficient models that can cut energy use by up to 40%. Stakeholder engagement enhances local acceptance and visibility.

- Procurement share: ~14% EU GDP

- Energy savings: up to 40%

- Alliances: pilot access

Energy policy and carbon pricing

European carbon pricing at roughly €85–100/tCO2 in 2024–25 raises factory energy costs and increases downstream TCO for Heidelberg Druckmaschinen customers, with German industrial electricity around €0.14–0.20/kWh in 2024; incentives for low-energy equipment and tightened CO2 rules are shifting demand towards energy-efficient presses and shortening replacement cycles, while long-term PPAs and efficiency upgrades act as hedges against price volatility.

- EU ETS price: €85–100/tCO2 (2024–25)

- German industrial power: ~€0.14–0.20/kWh (2024)

- Incentives ↑ demand for efficient presses

- PPAs/efficiency = hedge vs volatility

EU funding, carbon costs and tariffs drive energy-efficient production, compliance and nearshoring

EU grants (Digital Europe €8.2bn; Innovation Fund ~€20bn) and IPCEI support shape R&D/location; export controls (tightened 2023–24) and MFN tariffs up to ~14% raise compliance and tariff risk; EU ETS €85–100/tCO2 and German power €0.14–0.20/kWh (2024) shift demand to energy‑efficient presses and raise TCO; logistics +15% and lead times +20% pressure working capital and nearshoring decisions.

| Indicator | Value |

|---|---|

| Digital Europe | €8.2bn (2021‑27) |

| Innovation Fund | ~€20bn (2020‑30) |

| EU ETS | €85–100/tCO2 (2024–25) |

| German power | €0.14–0.20/kWh (2024) |

| MFN tariffs | up to ~14% |

| Procurement | ~14% EU GDP |

| Logistics impact | +15% costs; +20% lead times |

What is included in the product

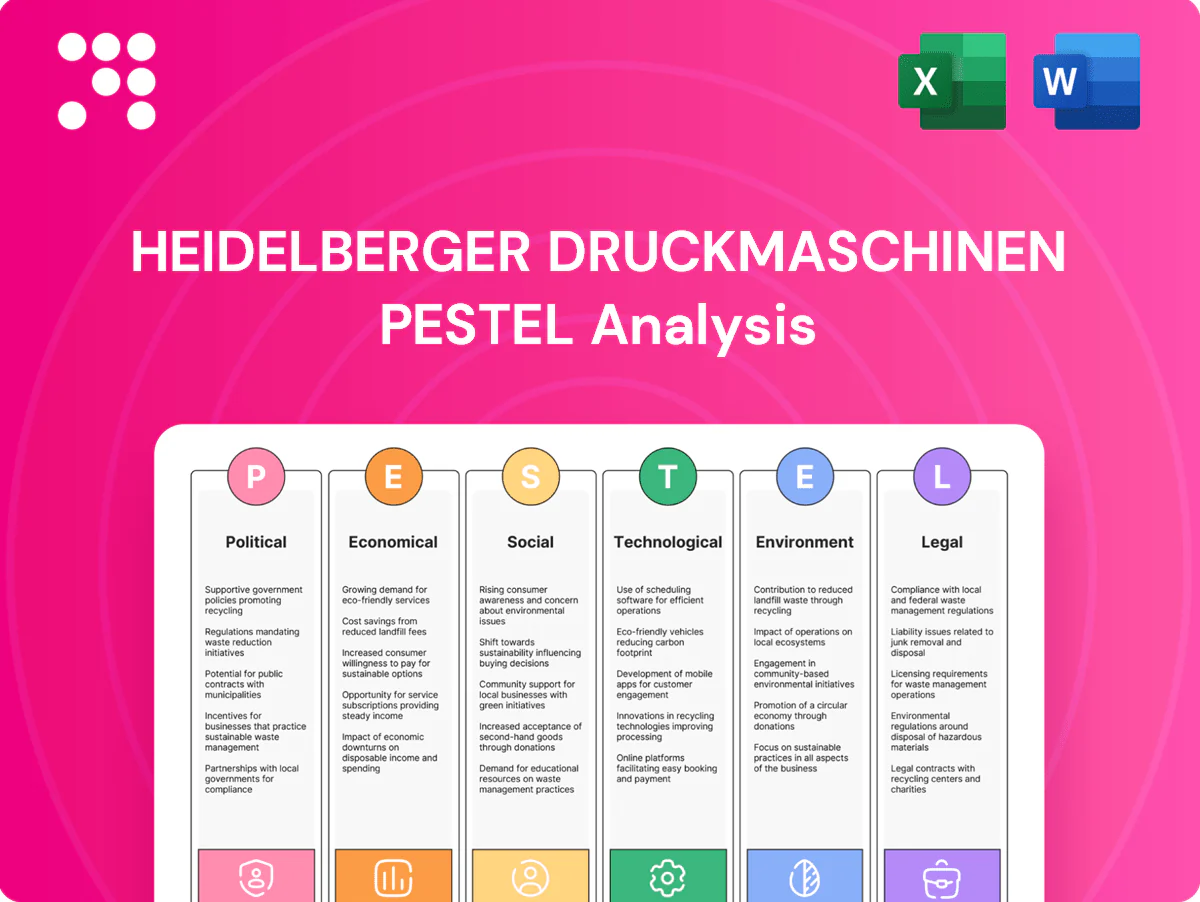

Explores how external macro-environmental factors uniquely affect Heidelberger Druckmaschinen across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and scenario responses.

A concise, visually segmented PESTLE summary for Heidelberger Druckmaschinen that can be dropped into presentations, edited with notes by region or business line, and easily shared across teams to streamline discussions on external risks and market positioning.

Economic factors

Capex cycles in print and packaging

Heidelberg’s order intake closely follows customers’ capex budgets, which track GDP and packaging demand; global packaging volumes rose about 3% in 2024, tempering new press orders and deferring service upgrades. Slowdowns push investment into maintenance, while counter-cyclical consumables and software subscriptions have helped stabilize recurring revenue. Flexible financing programs introduced in 2023–24 have begun unlocking latent demand by lowering upfront costs.

Interest rates and financing access

Higher interest rates have raised leasing and financing costs for printers, pressuring demand for capital-intensive Heidelberg equipment; vendor finance programs and lender partnerships have therefore been critical to sustaining order flow. Heidelberg's balance-sheet strength affects acceptance of long-term deals and warranty terms, while any rate declines in 2024–25 can accelerate conversion of the existing backlog into shipments.

Currency fluctuations

Euro strength or weakness alters Heidelberg Druckmaschinen export pricing and margin realization; EUR/USD averaged about 1.08 in 2024, amplifying FX impacts on export contracts. Natural hedging from multi-currency sourcing and global sales mix reduces volatility. Financial hedges (forwards/options) protect near-term cash flows but incur premium/transaction costs. Pricing clauses and indexation are used to manage long project lead times.

Input costs and component availability

Steel, electronics and precision components remain the main drivers of Heidelberger Druckmaschinen BOM costs and lead times; supply-chain bottlenecks eased in 2024 but component volatility persists. Inflationary pressure (EU annual inflation ~2.9% in 2024) forces dynamic pricing and systematic value engineering to protect margins. Supplier consolidation plus dual sourcing have strengthened continuity, while inventory optimization balances working capital against service levels.

- Steel, electronics, precision components

- Inflation-driven dynamic pricing & value engineering

- Supplier consolidation + dual sourcing

- Inventory optimization vs working capital

Shift from commercial to packaging growth

Packaging and labels are outpacing traditional commercial print; Smithers 2024 projects packaging-print CAGR about 3.6% to 2028, driving demand for flexo and hybrid digital lines that suit short runs and variants. Higher 24/7 packaging utilization raises service and consumables attach rates, improving recurring revenue and margin resilience as Heidelberg aligns portfolio to capture these segments.

- Growth: packaging CAGR ~3.6% (Smithers 2024)

- Tech: flexo & hybrid digital demand

- Revenue: higher attach rates in 24/7 ops

- Strategy: portfolio shift to higher-margin, resilient segments

EU funding, carbon costs and tariffs drive energy-efficient production, compliance and nearshoring

Heidelberg’s sales mirror customer capex and packaging demand; packaging CAGR ~3.6% (Smithers 2024) supports shift to flexo/hybrid. Higher rates raised leasing costs, pressuring big-ticket orders while finance programs eased uptake. EUR/USD ~1.08 (2024) and EU inflation ~2.9% (2024) drive pricing, hedging and value engineering.

| Metric | 2024 |

|---|---|

| Packaging CAGR | 3.6% |

| EUR/USD | 1.08 |

| EU inflation | 2.9% |

Preview Before You Purchase

Heidelberger Druckmaschinen PESTLE Analysis

The Heidelberger Druckmaschinen PESTLE analysis evaluates political, economic, social, technological, legal and environmental factors shaping the company’s strategic risks and opportunities, offering actionable insights for investors and managers. It highlights market drivers, regulatory pressures, and tech trends affecting operations and competitiveness. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.

Plan Smarter. Present Sharper. Compete Stronger.

Analyze how regulatory shifts, supply-chain pressures, and Industry 4.0 technologies are reshaping Heidelberger Druckmaschinen’s prospects with our concise PESTLE snapshot; buy the full, editable report now to access actionable risk assessments, growth levers, and strategic recommendations ready for immediate use.

Political factors

EU industrial policy and subsidies

Shifts in EU manufacturing incentives (eg IPCEI grants covering up to ~50% of project costs) shape Heidelberg’s capital and R&D location choices, while access to Digital Europe (€8.2bn 2021‑27) and the Innovation Fund (~€20bn 2020‑30) can cut green-tech/digitalization development costs materially; reduced funding or policy reversals would slow innovation and scale‑up, so monitoring eligibility criteria and local content rules (often >30% EU value‑add) is critical.

Trade tariffs and export controls

As a capital equipment exporter present in over 170 countries, Heidelberg faces tariff volatility on machinery and components, with MFN tariffs for electrical machinery ranging regionally up to about 14% (WTO/UNCTAD 2023 data).

Export controls on electronics and advanced drives tightened in 2023–24, disrupting procurement and shipments to sensitive markets and requiring license checks for certain drives and controls.

Strategic sourcing and multi-country assembly can shift value to lower-tariff jurisdictions and mitigate exposure, while proactive compliance and export licensing reduce delay and seizure risks in key markets.

Geopolitical supply chain risks

Regional tensions have pushed logistics costs up about 15% and extended lead times for precision parts by roughly 20% for European machinery makers, increasing working capital needs for Heidelberger Druckmaschinen. Diversifying suppliers across Europe, Asia and the Americas into three regional pools reduces single-point failures and mitigates >50% of supplier-concentration risk. Nearshoring critical assemblies can cut lead times by ~30% and lower transport spend; scenario planning that models 3–5 disruption scenarios helps balance inventory levels against service targets.

Public procurement and industrial alliances

Government-backed education and training centers routinely procure print equipment, and EU public procurement represents about 14% of GDP (Eurostat), creating steady demand. Participation in national industry alliances opens pilot and demonstration opportunities; transparent tenders favor compliant, energy-efficient models that can cut energy use by up to 40%. Stakeholder engagement enhances local acceptance and visibility.

- Procurement share: ~14% EU GDP

- Energy savings: up to 40%

- Alliances: pilot access

Energy policy and carbon pricing

European carbon pricing at roughly €85–100/tCO2 in 2024–25 raises factory energy costs and increases downstream TCO for Heidelberg Druckmaschinen customers, with German industrial electricity around €0.14–0.20/kWh in 2024; incentives for low-energy equipment and tightened CO2 rules are shifting demand towards energy-efficient presses and shortening replacement cycles, while long-term PPAs and efficiency upgrades act as hedges against price volatility.

- EU ETS price: €85–100/tCO2 (2024–25)

- German industrial power: ~€0.14–0.20/kWh (2024)

- Incentives ↑ demand for efficient presses

- PPAs/efficiency = hedge vs volatility

EU funding, carbon costs and tariffs drive energy-efficient production, compliance and nearshoring

EU grants (Digital Europe €8.2bn; Innovation Fund ~€20bn) and IPCEI support shape R&D/location; export controls (tightened 2023–24) and MFN tariffs up to ~14% raise compliance and tariff risk; EU ETS €85–100/tCO2 and German power €0.14–0.20/kWh (2024) shift demand to energy‑efficient presses and raise TCO; logistics +15% and lead times +20% pressure working capital and nearshoring decisions.

| Indicator | Value |

|---|---|

| Digital Europe | €8.2bn (2021‑27) |

| Innovation Fund | ~€20bn (2020‑30) |

| EU ETS | €85–100/tCO2 (2024–25) |

| German power | €0.14–0.20/kWh (2024) |

| MFN tariffs | up to ~14% |

| Procurement | ~14% EU GDP |

| Logistics impact | +15% costs; +20% lead times |

What is included in the product

Explores how external macro-environmental factors uniquely affect Heidelberger Druckmaschinen across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and scenario responses.

A concise, visually segmented PESTLE summary for Heidelberger Druckmaschinen that can be dropped into presentations, edited with notes by region or business line, and easily shared across teams to streamline discussions on external risks and market positioning.

Economic factors

Capex cycles in print and packaging

Heidelberg’s order intake closely follows customers’ capex budgets, which track GDP and packaging demand; global packaging volumes rose about 3% in 2024, tempering new press orders and deferring service upgrades. Slowdowns push investment into maintenance, while counter-cyclical consumables and software subscriptions have helped stabilize recurring revenue. Flexible financing programs introduced in 2023–24 have begun unlocking latent demand by lowering upfront costs.

Interest rates and financing access

Higher interest rates have raised leasing and financing costs for printers, pressuring demand for capital-intensive Heidelberg equipment; vendor finance programs and lender partnerships have therefore been critical to sustaining order flow. Heidelberg's balance-sheet strength affects acceptance of long-term deals and warranty terms, while any rate declines in 2024–25 can accelerate conversion of the existing backlog into shipments.

Currency fluctuations

Euro strength or weakness alters Heidelberg Druckmaschinen export pricing and margin realization; EUR/USD averaged about 1.08 in 2024, amplifying FX impacts on export contracts. Natural hedging from multi-currency sourcing and global sales mix reduces volatility. Financial hedges (forwards/options) protect near-term cash flows but incur premium/transaction costs. Pricing clauses and indexation are used to manage long project lead times.

Input costs and component availability

Steel, electronics and precision components remain the main drivers of Heidelberger Druckmaschinen BOM costs and lead times; supply-chain bottlenecks eased in 2024 but component volatility persists. Inflationary pressure (EU annual inflation ~2.9% in 2024) forces dynamic pricing and systematic value engineering to protect margins. Supplier consolidation plus dual sourcing have strengthened continuity, while inventory optimization balances working capital against service levels.

- Steel, electronics, precision components

- Inflation-driven dynamic pricing & value engineering

- Supplier consolidation + dual sourcing

- Inventory optimization vs working capital

Shift from commercial to packaging growth

Packaging and labels are outpacing traditional commercial print; Smithers 2024 projects packaging-print CAGR about 3.6% to 2028, driving demand for flexo and hybrid digital lines that suit short runs and variants. Higher 24/7 packaging utilization raises service and consumables attach rates, improving recurring revenue and margin resilience as Heidelberg aligns portfolio to capture these segments.

- Growth: packaging CAGR ~3.6% (Smithers 2024)

- Tech: flexo & hybrid digital demand

- Revenue: higher attach rates in 24/7 ops

- Strategy: portfolio shift to higher-margin, resilient segments

EU funding, carbon costs and tariffs drive energy-efficient production, compliance and nearshoring

Heidelberg’s sales mirror customer capex and packaging demand; packaging CAGR ~3.6% (Smithers 2024) supports shift to flexo/hybrid. Higher rates raised leasing costs, pressuring big-ticket orders while finance programs eased uptake. EUR/USD ~1.08 (2024) and EU inflation ~2.9% (2024) drive pricing, hedging and value engineering.

| Metric | 2024 |

|---|---|

| Packaging CAGR | 3.6% |

| EUR/USD | 1.08 |

| EU inflation | 2.9% |

Preview Before You Purchase

Heidelberger Druckmaschinen PESTLE Analysis

The Heidelberger Druckmaschinen PESTLE analysis evaluates political, economic, social, technological, legal and environmental factors shaping the company’s strategic risks and opportunities, offering actionable insights for investors and managers. It highlights market drivers, regulatory pressures, and tech trends affecting operations and competitiveness. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Analyze how regulatory shifts, supply-chain pressures, and Industry 4.0 technologies are reshaping Heidelberger Druckmaschinen’s prospects with our concise PESTLE snapshot; buy the full, editable report now to access actionable risk assessments, growth levers, and strategic recommendations ready for immediate use.

Political factors

EU industrial policy and subsidies

Shifts in EU manufacturing incentives (eg IPCEI grants covering up to ~50% of project costs) shape Heidelberg’s capital and R&D location choices, while access to Digital Europe (€8.2bn 2021‑27) and the Innovation Fund (~€20bn 2020‑30) can cut green-tech/digitalization development costs materially; reduced funding or policy reversals would slow innovation and scale‑up, so monitoring eligibility criteria and local content rules (often >30% EU value‑add) is critical.

Trade tariffs and export controls

As a capital equipment exporter present in over 170 countries, Heidelberg faces tariff volatility on machinery and components, with MFN tariffs for electrical machinery ranging regionally up to about 14% (WTO/UNCTAD 2023 data).

Export controls on electronics and advanced drives tightened in 2023–24, disrupting procurement and shipments to sensitive markets and requiring license checks for certain drives and controls.

Strategic sourcing and multi-country assembly can shift value to lower-tariff jurisdictions and mitigate exposure, while proactive compliance and export licensing reduce delay and seizure risks in key markets.

Geopolitical supply chain risks

Regional tensions have pushed logistics costs up about 15% and extended lead times for precision parts by roughly 20% for European machinery makers, increasing working capital needs for Heidelberger Druckmaschinen. Diversifying suppliers across Europe, Asia and the Americas into three regional pools reduces single-point failures and mitigates >50% of supplier-concentration risk. Nearshoring critical assemblies can cut lead times by ~30% and lower transport spend; scenario planning that models 3–5 disruption scenarios helps balance inventory levels against service targets.

Public procurement and industrial alliances

Government-backed education and training centers routinely procure print equipment, and EU public procurement represents about 14% of GDP (Eurostat), creating steady demand. Participation in national industry alliances opens pilot and demonstration opportunities; transparent tenders favor compliant, energy-efficient models that can cut energy use by up to 40%. Stakeholder engagement enhances local acceptance and visibility.

- Procurement share: ~14% EU GDP

- Energy savings: up to 40%

- Alliances: pilot access

Energy policy and carbon pricing

European carbon pricing at roughly €85–100/tCO2 in 2024–25 raises factory energy costs and increases downstream TCO for Heidelberg Druckmaschinen customers, with German industrial electricity around €0.14–0.20/kWh in 2024; incentives for low-energy equipment and tightened CO2 rules are shifting demand towards energy-efficient presses and shortening replacement cycles, while long-term PPAs and efficiency upgrades act as hedges against price volatility.

- EU ETS price: €85–100/tCO2 (2024–25)

- German industrial power: ~€0.14–0.20/kWh (2024)

- Incentives ↑ demand for efficient presses

- PPAs/efficiency = hedge vs volatility

EU funding, carbon costs and tariffs drive energy-efficient production, compliance and nearshoring

EU grants (Digital Europe €8.2bn; Innovation Fund ~€20bn) and IPCEI support shape R&D/location; export controls (tightened 2023–24) and MFN tariffs up to ~14% raise compliance and tariff risk; EU ETS €85–100/tCO2 and German power €0.14–0.20/kWh (2024) shift demand to energy‑efficient presses and raise TCO; logistics +15% and lead times +20% pressure working capital and nearshoring decisions.

| Indicator | Value |

|---|---|

| Digital Europe | €8.2bn (2021‑27) |

| Innovation Fund | ~€20bn (2020‑30) |

| EU ETS | €85–100/tCO2 (2024–25) |

| German power | €0.14–0.20/kWh (2024) |

| MFN tariffs | up to ~14% |

| Procurement | ~14% EU GDP |

| Logistics impact | +15% costs; +20% lead times |

What is included in the product

Explores how external macro-environmental factors uniquely affect Heidelberger Druckmaschinen across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and scenario responses.

A concise, visually segmented PESTLE summary for Heidelberger Druckmaschinen that can be dropped into presentations, edited with notes by region or business line, and easily shared across teams to streamline discussions on external risks and market positioning.

Economic factors

Capex cycles in print and packaging

Heidelberg’s order intake closely follows customers’ capex budgets, which track GDP and packaging demand; global packaging volumes rose about 3% in 2024, tempering new press orders and deferring service upgrades. Slowdowns push investment into maintenance, while counter-cyclical consumables and software subscriptions have helped stabilize recurring revenue. Flexible financing programs introduced in 2023–24 have begun unlocking latent demand by lowering upfront costs.

Interest rates and financing access

Higher interest rates have raised leasing and financing costs for printers, pressuring demand for capital-intensive Heidelberg equipment; vendor finance programs and lender partnerships have therefore been critical to sustaining order flow. Heidelberg's balance-sheet strength affects acceptance of long-term deals and warranty terms, while any rate declines in 2024–25 can accelerate conversion of the existing backlog into shipments.

Currency fluctuations

Euro strength or weakness alters Heidelberg Druckmaschinen export pricing and margin realization; EUR/USD averaged about 1.08 in 2024, amplifying FX impacts on export contracts. Natural hedging from multi-currency sourcing and global sales mix reduces volatility. Financial hedges (forwards/options) protect near-term cash flows but incur premium/transaction costs. Pricing clauses and indexation are used to manage long project lead times.

Input costs and component availability

Steel, electronics and precision components remain the main drivers of Heidelberger Druckmaschinen BOM costs and lead times; supply-chain bottlenecks eased in 2024 but component volatility persists. Inflationary pressure (EU annual inflation ~2.9% in 2024) forces dynamic pricing and systematic value engineering to protect margins. Supplier consolidation plus dual sourcing have strengthened continuity, while inventory optimization balances working capital against service levels.

- Steel, electronics, precision components

- Inflation-driven dynamic pricing & value engineering

- Supplier consolidation + dual sourcing

- Inventory optimization vs working capital

Shift from commercial to packaging growth

Packaging and labels are outpacing traditional commercial print; Smithers 2024 projects packaging-print CAGR about 3.6% to 2028, driving demand for flexo and hybrid digital lines that suit short runs and variants. Higher 24/7 packaging utilization raises service and consumables attach rates, improving recurring revenue and margin resilience as Heidelberg aligns portfolio to capture these segments.

- Growth: packaging CAGR ~3.6% (Smithers 2024)

- Tech: flexo & hybrid digital demand

- Revenue: higher attach rates in 24/7 ops

- Strategy: portfolio shift to higher-margin, resilient segments

EU funding, carbon costs and tariffs drive energy-efficient production, compliance and nearshoring

Heidelberg’s sales mirror customer capex and packaging demand; packaging CAGR ~3.6% (Smithers 2024) supports shift to flexo/hybrid. Higher rates raised leasing costs, pressuring big-ticket orders while finance programs eased uptake. EUR/USD ~1.08 (2024) and EU inflation ~2.9% (2024) drive pricing, hedging and value engineering.

| Metric | 2024 |

|---|---|

| Packaging CAGR | 3.6% |

| EUR/USD | 1.08 |

| EU inflation | 2.9% |

Preview Before You Purchase

Heidelberger Druckmaschinen PESTLE Analysis

The Heidelberger Druckmaschinen PESTLE analysis evaluates political, economic, social, technological, legal and environmental factors shaping the company’s strategic risks and opportunities, offering actionable insights for investors and managers. It highlights market drivers, regulatory pressures, and tech trends affecting operations and competitiveness. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use.