Heidelberg Materials Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Heidelberg Materials faces intense rivalry, strong supplier influence for raw materials, and moderate substitution threats as construction demand shifts—this snapshot highlights key competitive pressures and strategic vulnerabilities. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Raw material concentration

Heidelberg Materials sources limestone, aggregates and additives that are regionally concentrated, with operations across around 50 countries (2024), which localizes supplier risk. Quarry ownership and long-term leases reduce supplier leverage, though specialty additives sold by niche suppliers retain pricing power. Local scarcity or permitting constraints can tighten supply in key markets; strategic backward integration and multi-sourcing remain core mitigants.

Energy price volatility

Coal, petcoke, gas and electricity are critical kiln inputs, giving energy suppliers leverage as energy can represent c.20–30% of cement production costs; EU carbon prices averaged roughly €92/t in 2024, so spikes or rising carbon costs materially compress margins. Long-term fuel contracts and fuel switching reduce short-term exposure, while ongoing investments in alternative fuels and renewables steadily weaken supplier power.

Equipment and spare parts

Three major OEMs dominate supply of large kilns, mills and automation systems, creating notable switching costs; proprietary parts and tied maintenance contracts further raise supplier dependency. Adoption of predictive maintenance and standardized components reduces vendor lock-in and spare-parts spend. Implementation of digital twins and continuous condition monitoring strengthens Heidelberg Materials’ negotiating leverage by improving asset visibility and procurement timing.

Logistics and transport

Trucking and rail account for up to 30% of delivered cement and aggregates costs; tight truck/rail capacity and fuel surcharges in 2024 pushed spot logistics premiums by double digits, raising carrier bargaining power.

Owning terminals, optimizing routing and modal shifts to rail/lake reduce per-ton freight; long-term carrier contracts and modal flexibility stabilized logistics spend for Heidelberg Materials in 2024.

- Transport share: up to 30% of delivered cost

- 2024 spot logistics premiums: double-digit increases

- Mitigants: owned terminals, routing, modal mix

- Stabilizers: long-term carrier contracts, modal flexibility

Alternative fuels and SCMs

Suppliers of refuse-derived fuel, biomass and SCMs exert episodic bargaining power as availability fluctuates while Heidelberg Materials reported roughly 35% alternative fuel use in 2024, intensifying competition as decarbonization raises demand. Diversifying feedstocks and scaling calcined clay capacity reduces supplier dependence and price exposure. Strategic long-term offtake and JV partnerships secure volumes on more favorable terms.

- episodic supplier power

- 35% alternative fuel use (2024)

- calcined clay lowers reliance

- long-term partnerships secure volumes

Regional sourcing (~50 countries) limits supplier power; energy, carbon & transport drive costs

Heidelberg Materials sources regionally across ~50 countries (2024), limiting supplier power; quarry ownership and multi-sourcing reduce leverage, though niche additives keep pricing power. Energy (20–30% of costs) and EU carbon ~€92/t (2024) increase fuel supplier influence; 35% alternative fuel use (2024) and backward integration mitigate exposure; logistics can be up to 30% of delivered cost.

| Metric | 2024 |

|---|---|

| Countries | ~50 |

| Energy share of cost | 20–30% |

| EU carbon price | €92/t |

| Alternative fuel use | 35% |

| Transport share | up to 30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Heidelberg Materials, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and entry barriers shaping profitability. Offers strategic insights on disruptive threats, pricing leverage, and protective dynamics for use in investor reports or internal planning.

Concise, one-sheet Porter's Five Forces for Heidelberg Materials — instantly visualize competitive pressures with a radar chart, customize threat levels for regulation or new entrants, and drop into decks or Excel dashboards without macros for quick boardroom decisions.

Customers Bargaining Power

Large project buyers

Infrastructure agencies and major contractors buy cement and aggregates at scale and negotiate aggressively; Heidelberg Materials reported 2024 sales of about €20.2bn, intensifying pressure from large-volume buyers. Tender-based procurement and multi-year framework agreements compress margins, though superior reliability and technical support reduce price sensitivity. Value-added services and digital ordering platforms increase customer stickiness and recurring volumes.

Product commoditization

Standard cement and aggregates are highly price-transparent, giving buyers leverage as Heidelberg Materials sells commoditized products across more than 50 countries; 2024 group revenue was about €21 billion, amplifying buyer focus on price. Switching costs remain modest where logistics permit multiple suppliers, but performance cements and tailored mixes reduce head-to-head comparability. Certification and consistent quality (ISO, CE) create differentiation that softens buyer power.

Substitution and mix design

Buyers can alter concrete mix designs to lower clinker content or switch suppliers, increasing their bargaining power. Availability of SCMs enables buyer-level cost and CO2 optimization, especially with 2024 EU ETS carbon pricing near €100/t CO2. Heidelberg Materials' strong technical advisory helps influence specifications, while EPDs and low-carbon labels increasingly create non-price purchasing criteria.

Logistics proximity

Delivered price for Heidelberg Materials' cement and aggregates is heavily tied to distance; transport can account for up to 60% of delivered cost, so proximate buyers exert greater leverage than captive geographies. Expanding last-mile terminals and rail/river capacity narrows buyer alternatives, while real-time delivery tracking (2024 industry standard) improves service and retention.

- Proximity: distance drives up to 60% of delivered cost

- Leverage: buyers near multiple plants negotiate better terms

- Footprint: last-mile expansion reduces alternatives

- Retention: real-time tracking raises on-time performance and loyalty

Cyclic demand patterns

Construction cycles let buyers consolidate volumes and extract concessions during downturns, while tight capacity in strong markets erodes that leverage; Heidelberg Materials’ diversified footprint in over 50 countries helps dilute local buyer pressure. Balanced contract structures with indexation and minimum volumes share demand risk across cycles.

- Buyers leverage

- Capacity tightness

- Contract risk-sharing

- 50+ country diversification

Buyers gain leverage; sector 2024 sales €20.2bn, transport up to 60%

Large-volume buyers extract concessions as Heidelberg Materials reported 2024 sales of €20.2bn and operates in 50+ countries. Price transparency and low switching costs boost buyer leverage, though performance cements, certifications and technical support reduce it. Transport can be up to 60% of delivered cost and EU ETS pricing (~€100/t CO2) raises non-price criteria.

| Metric | Value |

|---|---|

| 2024 sales | €20.2bn |

| Countries | 50+ |

| Transport share | Up to 60% |

| EU ETS price | ~€100/t CO2 (2024) |

What You See Is What You Get

Heidelberg Materials Porter's Five Forces Analysis

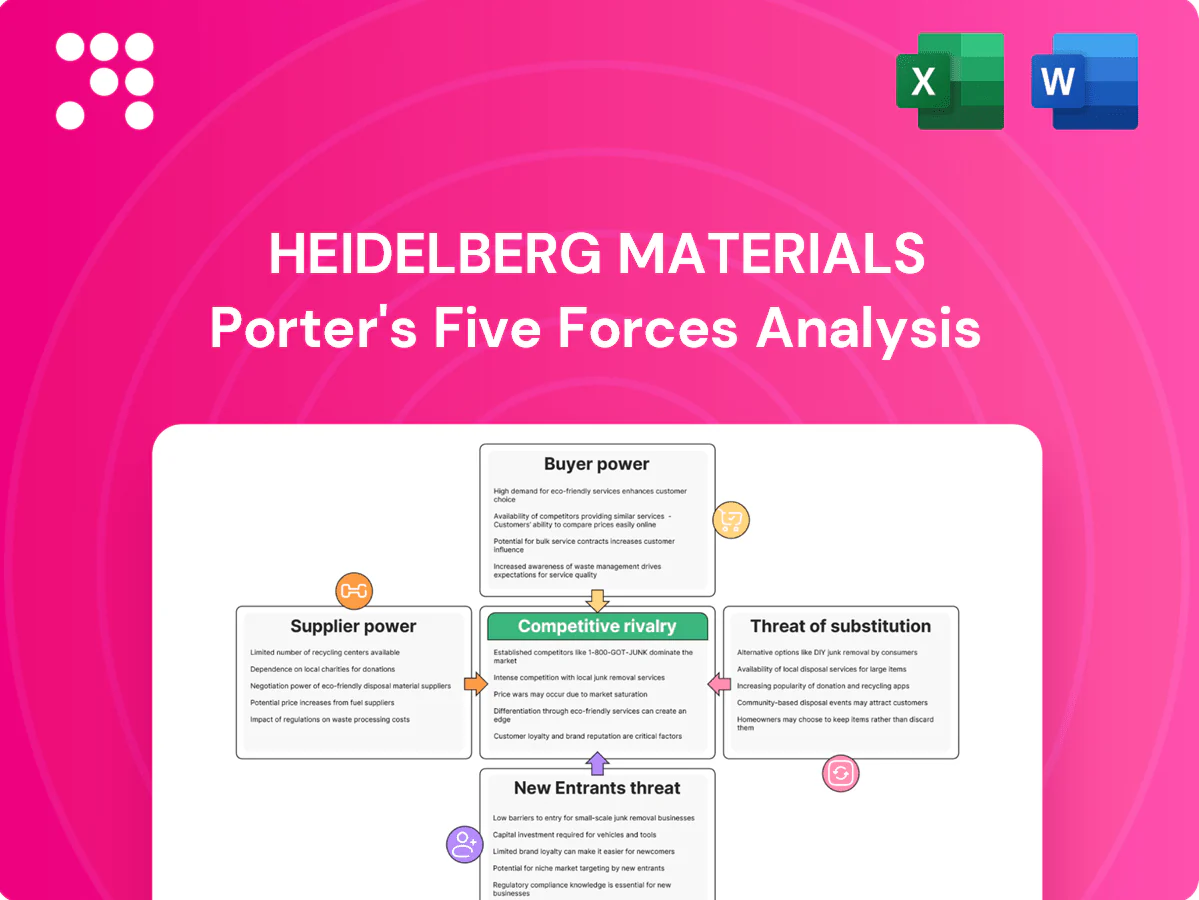

This Porter's Five Forces analysis of Heidelberg Materials is the actual, professionally written document you see in preview, covering supplier power, buyer power, competitive rivalry, threat of substitution and barriers to entry. Once you purchase, you’ll receive this exact file instantly—fully formatted and ready for use.

Don't Miss the Bigger Picture

Heidelberg Materials faces intense rivalry, strong supplier influence for raw materials, and moderate substitution threats as construction demand shifts—this snapshot highlights key competitive pressures and strategic vulnerabilities. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Raw material concentration

Heidelberg Materials sources limestone, aggregates and additives that are regionally concentrated, with operations across around 50 countries (2024), which localizes supplier risk. Quarry ownership and long-term leases reduce supplier leverage, though specialty additives sold by niche suppliers retain pricing power. Local scarcity or permitting constraints can tighten supply in key markets; strategic backward integration and multi-sourcing remain core mitigants.

Energy price volatility

Coal, petcoke, gas and electricity are critical kiln inputs, giving energy suppliers leverage as energy can represent c.20–30% of cement production costs; EU carbon prices averaged roughly €92/t in 2024, so spikes or rising carbon costs materially compress margins. Long-term fuel contracts and fuel switching reduce short-term exposure, while ongoing investments in alternative fuels and renewables steadily weaken supplier power.

Equipment and spare parts

Three major OEMs dominate supply of large kilns, mills and automation systems, creating notable switching costs; proprietary parts and tied maintenance contracts further raise supplier dependency. Adoption of predictive maintenance and standardized components reduces vendor lock-in and spare-parts spend. Implementation of digital twins and continuous condition monitoring strengthens Heidelberg Materials’ negotiating leverage by improving asset visibility and procurement timing.

Logistics and transport

Trucking and rail account for up to 30% of delivered cement and aggregates costs; tight truck/rail capacity and fuel surcharges in 2024 pushed spot logistics premiums by double digits, raising carrier bargaining power.

Owning terminals, optimizing routing and modal shifts to rail/lake reduce per-ton freight; long-term carrier contracts and modal flexibility stabilized logistics spend for Heidelberg Materials in 2024.

- Transport share: up to 30% of delivered cost

- 2024 spot logistics premiums: double-digit increases

- Mitigants: owned terminals, routing, modal mix

- Stabilizers: long-term carrier contracts, modal flexibility

Alternative fuels and SCMs

Suppliers of refuse-derived fuel, biomass and SCMs exert episodic bargaining power as availability fluctuates while Heidelberg Materials reported roughly 35% alternative fuel use in 2024, intensifying competition as decarbonization raises demand. Diversifying feedstocks and scaling calcined clay capacity reduces supplier dependence and price exposure. Strategic long-term offtake and JV partnerships secure volumes on more favorable terms.

- episodic supplier power

- 35% alternative fuel use (2024)

- calcined clay lowers reliance

- long-term partnerships secure volumes

Regional sourcing (~50 countries) limits supplier power; energy, carbon & transport drive costs

Heidelberg Materials sources regionally across ~50 countries (2024), limiting supplier power; quarry ownership and multi-sourcing reduce leverage, though niche additives keep pricing power. Energy (20–30% of costs) and EU carbon ~€92/t (2024) increase fuel supplier influence; 35% alternative fuel use (2024) and backward integration mitigate exposure; logistics can be up to 30% of delivered cost.

| Metric | 2024 |

|---|---|

| Countries | ~50 |

| Energy share of cost | 20–30% |

| EU carbon price | €92/t |

| Alternative fuel use | 35% |

| Transport share | up to 30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Heidelberg Materials, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and entry barriers shaping profitability. Offers strategic insights on disruptive threats, pricing leverage, and protective dynamics for use in investor reports or internal planning.

Concise, one-sheet Porter's Five Forces for Heidelberg Materials — instantly visualize competitive pressures with a radar chart, customize threat levels for regulation or new entrants, and drop into decks or Excel dashboards without macros for quick boardroom decisions.

Customers Bargaining Power

Large project buyers

Infrastructure agencies and major contractors buy cement and aggregates at scale and negotiate aggressively; Heidelberg Materials reported 2024 sales of about €20.2bn, intensifying pressure from large-volume buyers. Tender-based procurement and multi-year framework agreements compress margins, though superior reliability and technical support reduce price sensitivity. Value-added services and digital ordering platforms increase customer stickiness and recurring volumes.

Product commoditization

Standard cement and aggregates are highly price-transparent, giving buyers leverage as Heidelberg Materials sells commoditized products across more than 50 countries; 2024 group revenue was about €21 billion, amplifying buyer focus on price. Switching costs remain modest where logistics permit multiple suppliers, but performance cements and tailored mixes reduce head-to-head comparability. Certification and consistent quality (ISO, CE) create differentiation that softens buyer power.

Substitution and mix design

Buyers can alter concrete mix designs to lower clinker content or switch suppliers, increasing their bargaining power. Availability of SCMs enables buyer-level cost and CO2 optimization, especially with 2024 EU ETS carbon pricing near €100/t CO2. Heidelberg Materials' strong technical advisory helps influence specifications, while EPDs and low-carbon labels increasingly create non-price purchasing criteria.

Logistics proximity

Delivered price for Heidelberg Materials' cement and aggregates is heavily tied to distance; transport can account for up to 60% of delivered cost, so proximate buyers exert greater leverage than captive geographies. Expanding last-mile terminals and rail/river capacity narrows buyer alternatives, while real-time delivery tracking (2024 industry standard) improves service and retention.

- Proximity: distance drives up to 60% of delivered cost

- Leverage: buyers near multiple plants negotiate better terms

- Footprint: last-mile expansion reduces alternatives

- Retention: real-time tracking raises on-time performance and loyalty

Cyclic demand patterns

Construction cycles let buyers consolidate volumes and extract concessions during downturns, while tight capacity in strong markets erodes that leverage; Heidelberg Materials’ diversified footprint in over 50 countries helps dilute local buyer pressure. Balanced contract structures with indexation and minimum volumes share demand risk across cycles.

- Buyers leverage

- Capacity tightness

- Contract risk-sharing

- 50+ country diversification

Buyers gain leverage; sector 2024 sales €20.2bn, transport up to 60%

Large-volume buyers extract concessions as Heidelberg Materials reported 2024 sales of €20.2bn and operates in 50+ countries. Price transparency and low switching costs boost buyer leverage, though performance cements, certifications and technical support reduce it. Transport can be up to 60% of delivered cost and EU ETS pricing (~€100/t CO2) raises non-price criteria.

| Metric | Value |

|---|---|

| 2024 sales | €20.2bn |

| Countries | 50+ |

| Transport share | Up to 60% |

| EU ETS price | ~€100/t CO2 (2024) |

What You See Is What You Get

Heidelberg Materials Porter's Five Forces Analysis

This Porter's Five Forces analysis of Heidelberg Materials is the actual, professionally written document you see in preview, covering supplier power, buyer power, competitive rivalry, threat of substitution and barriers to entry. Once you purchase, you’ll receive this exact file instantly—fully formatted and ready for use.

Description

Don't Miss the Bigger Picture

Heidelberg Materials faces intense rivalry, strong supplier influence for raw materials, and moderate substitution threats as construction demand shifts—this snapshot highlights key competitive pressures and strategic vulnerabilities. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for investment or strategy.

Suppliers Bargaining Power

Raw material concentration

Heidelberg Materials sources limestone, aggregates and additives that are regionally concentrated, with operations across around 50 countries (2024), which localizes supplier risk. Quarry ownership and long-term leases reduce supplier leverage, though specialty additives sold by niche suppliers retain pricing power. Local scarcity or permitting constraints can tighten supply in key markets; strategic backward integration and multi-sourcing remain core mitigants.

Energy price volatility

Coal, petcoke, gas and electricity are critical kiln inputs, giving energy suppliers leverage as energy can represent c.20–30% of cement production costs; EU carbon prices averaged roughly €92/t in 2024, so spikes or rising carbon costs materially compress margins. Long-term fuel contracts and fuel switching reduce short-term exposure, while ongoing investments in alternative fuels and renewables steadily weaken supplier power.

Equipment and spare parts

Three major OEMs dominate supply of large kilns, mills and automation systems, creating notable switching costs; proprietary parts and tied maintenance contracts further raise supplier dependency. Adoption of predictive maintenance and standardized components reduces vendor lock-in and spare-parts spend. Implementation of digital twins and continuous condition monitoring strengthens Heidelberg Materials’ negotiating leverage by improving asset visibility and procurement timing.

Logistics and transport

Trucking and rail account for up to 30% of delivered cement and aggregates costs; tight truck/rail capacity and fuel surcharges in 2024 pushed spot logistics premiums by double digits, raising carrier bargaining power.

Owning terminals, optimizing routing and modal shifts to rail/lake reduce per-ton freight; long-term carrier contracts and modal flexibility stabilized logistics spend for Heidelberg Materials in 2024.

- Transport share: up to 30% of delivered cost

- 2024 spot logistics premiums: double-digit increases

- Mitigants: owned terminals, routing, modal mix

- Stabilizers: long-term carrier contracts, modal flexibility

Alternative fuels and SCMs

Suppliers of refuse-derived fuel, biomass and SCMs exert episodic bargaining power as availability fluctuates while Heidelberg Materials reported roughly 35% alternative fuel use in 2024, intensifying competition as decarbonization raises demand. Diversifying feedstocks and scaling calcined clay capacity reduces supplier dependence and price exposure. Strategic long-term offtake and JV partnerships secure volumes on more favorable terms.

- episodic supplier power

- 35% alternative fuel use (2024)

- calcined clay lowers reliance

- long-term partnerships secure volumes

Regional sourcing (~50 countries) limits supplier power; energy, carbon & transport drive costs

Heidelberg Materials sources regionally across ~50 countries (2024), limiting supplier power; quarry ownership and multi-sourcing reduce leverage, though niche additives keep pricing power. Energy (20–30% of costs) and EU carbon ~€92/t (2024) increase fuel supplier influence; 35% alternative fuel use (2024) and backward integration mitigate exposure; logistics can be up to 30% of delivered cost.

| Metric | 2024 |

|---|---|

| Countries | ~50 |

| Energy share of cost | 20–30% |

| EU carbon price | €92/t |

| Alternative fuel use | 35% |

| Transport share | up to 30% |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Heidelberg Materials, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and entry barriers shaping profitability. Offers strategic insights on disruptive threats, pricing leverage, and protective dynamics for use in investor reports or internal planning.

Concise, one-sheet Porter's Five Forces for Heidelberg Materials — instantly visualize competitive pressures with a radar chart, customize threat levels for regulation or new entrants, and drop into decks or Excel dashboards without macros for quick boardroom decisions.

Customers Bargaining Power

Large project buyers

Infrastructure agencies and major contractors buy cement and aggregates at scale and negotiate aggressively; Heidelberg Materials reported 2024 sales of about €20.2bn, intensifying pressure from large-volume buyers. Tender-based procurement and multi-year framework agreements compress margins, though superior reliability and technical support reduce price sensitivity. Value-added services and digital ordering platforms increase customer stickiness and recurring volumes.

Product commoditization

Standard cement and aggregates are highly price-transparent, giving buyers leverage as Heidelberg Materials sells commoditized products across more than 50 countries; 2024 group revenue was about €21 billion, amplifying buyer focus on price. Switching costs remain modest where logistics permit multiple suppliers, but performance cements and tailored mixes reduce head-to-head comparability. Certification and consistent quality (ISO, CE) create differentiation that softens buyer power.

Substitution and mix design

Buyers can alter concrete mix designs to lower clinker content or switch suppliers, increasing their bargaining power. Availability of SCMs enables buyer-level cost and CO2 optimization, especially with 2024 EU ETS carbon pricing near €100/t CO2. Heidelberg Materials' strong technical advisory helps influence specifications, while EPDs and low-carbon labels increasingly create non-price purchasing criteria.

Logistics proximity

Delivered price for Heidelberg Materials' cement and aggregates is heavily tied to distance; transport can account for up to 60% of delivered cost, so proximate buyers exert greater leverage than captive geographies. Expanding last-mile terminals and rail/river capacity narrows buyer alternatives, while real-time delivery tracking (2024 industry standard) improves service and retention.

- Proximity: distance drives up to 60% of delivered cost

- Leverage: buyers near multiple plants negotiate better terms

- Footprint: last-mile expansion reduces alternatives

- Retention: real-time tracking raises on-time performance and loyalty

Cyclic demand patterns

Construction cycles let buyers consolidate volumes and extract concessions during downturns, while tight capacity in strong markets erodes that leverage; Heidelberg Materials’ diversified footprint in over 50 countries helps dilute local buyer pressure. Balanced contract structures with indexation and minimum volumes share demand risk across cycles.

- Buyers leverage

- Capacity tightness

- Contract risk-sharing

- 50+ country diversification

Buyers gain leverage; sector 2024 sales €20.2bn, transport up to 60%

Large-volume buyers extract concessions as Heidelberg Materials reported 2024 sales of €20.2bn and operates in 50+ countries. Price transparency and low switching costs boost buyer leverage, though performance cements, certifications and technical support reduce it. Transport can be up to 60% of delivered cost and EU ETS pricing (~€100/t CO2) raises non-price criteria.

| Metric | Value |

|---|---|

| 2024 sales | €20.2bn |

| Countries | 50+ |

| Transport share | Up to 60% |

| EU ETS price | ~€100/t CO2 (2024) |

What You See Is What You Get

Heidelberg Materials Porter's Five Forces Analysis

This Porter's Five Forces analysis of Heidelberg Materials is the actual, professionally written document you see in preview, covering supplier power, buyer power, competitive rivalry, threat of substitution and barriers to entry. Once you purchase, you’ll receive this exact file instantly—fully formatted and ready for use.