Helios Technologies SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Helios Technologies shows strengths in diversified motion-control products and aftermarket revenue, with growth tied to marine and industrial recovery but faces margin pressure from competition and supply-chain risks; our full SWOT dives into financial implications, strategic levers, and scenario planning—purchase the complete, editable report to act with clarity.

Strengths

Integrated hydraulics-electronics platform

Helios Technologies (Nasdaq: HLIO) combines fluid power with electronic controls to deliver integrated motion solutions, creating strong OEM stickiness as customers prefer fewer suppliers and seamless system performance. This integration supports higher average selling prices and improved margins versus stand-alone components, and differentiates Helios from commodity hydraulic suppliers. Integrated offerings also position the company to capture systems-level revenue opportunities.

Diverse end-market exposure

Helios Technologies (NASDAQ: HLIO) serves agriculture, construction, material handling and recreational vehicles, spreading demand risk across cycles. When one sector slows, others can offset revenue swings, supporting resilience. This diversification expands application know-how and enables cross-industry innovation, enhancing product adaptability and aftermarket opportunities.

Global footprint and channels

Operations across Americas, EMEA and APAC enable Helios to provide close support for OEMs and distributors, improving response and service consistency. Localized engineering and manufacturing shorten lead times and allow region-specific customization for industrial and mobile markets. A broad channel mix supports both OEM and aftermarket revenue and reduces single-region macro risk.

Application engineering and custom solutions

Deep domain expertise in fluid power and controls drives tailored performance, supporting Helios's >$1 billion annual revenue (2024) by enabling higher-value system sales. Co-development with OEMs embeds Helios early in platform designs, increasing adoption and design wins. Extensive customization raises switching costs and boosts lifecycle revenue while field feedback from deployments accelerates continuous improvement.

- Deep domain expertise

- Early co-development

- Higher switching costs

- Lifecycle revenue growth

Innovation-driven portfolio

Helios Technologies (NYSE: HLIO) emphasizes efficiency, precision control, and reliability, directly matching customer value drivers and supporting premium pricing power. Electronics, software and IoT features deepen product differentiation and enabled new mobile and industrial platform wins in 2024. Continued R&D investment sustained competitive momentum and higher-margin product mix.

- Focus: efficiency, precision, reliability

- Differentiation: electronics, software, IoT

- R&D: drives platform wins (2024)

- Pricing: premium positioning, pricing power

Fluid-power + electronics drive OEM stickiness, higher ASPs, diversified markets, >$1B 2024

Helios Technologies (Nasdaq: HLIO) integrates fluid power and electronic controls, creating strong OEM stickiness and higher ASPs versus commodity suppliers. Diversified end-markets (agriculture, construction, material handling, RV) and operations across Americas, EMEA, APAC support resilience and service proximity. Deep domain expertise and R&D drove >$1 billion revenue in 2024, enabling premium pricing, lifecycle revenue and systems-level wins.

| Metric | 2024 / Fact |

|---|---|

| Revenue | >$1 billion (2024) |

| Regions | Americas, EMEA, APAC |

| Core markets | Agriculture, construction, material handling, RV |

| Differentiators | Electronics, software, IoT, integrated systems |

What is included in the product

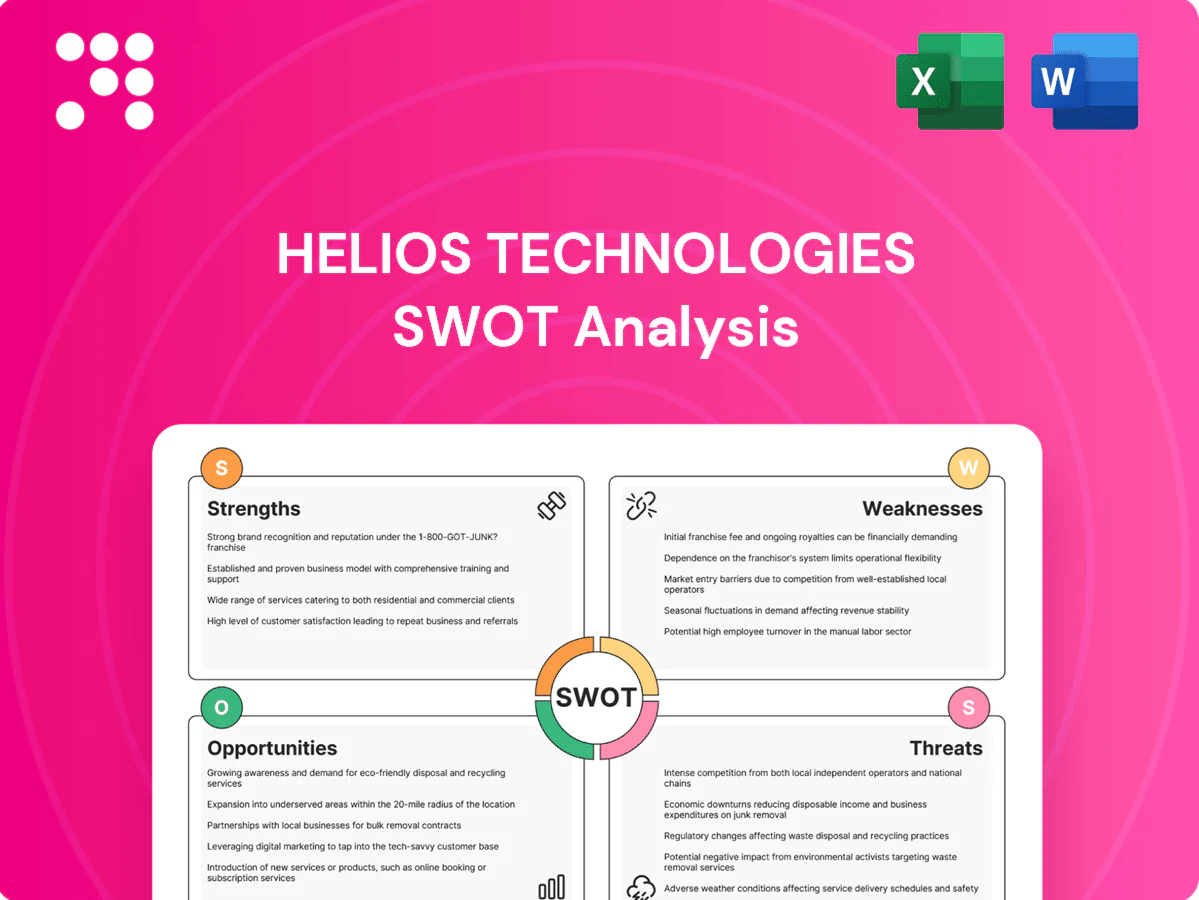

Provides a strategic overview of Helios Technologies’s internal strengths and weaknesses and external opportunities and threats, highlighting key growth drivers, operational gaps, competitive positioning, and market risks shaping its future.

Provides a concise SWOT matrix for Helios Technologies to quickly identify strengths, weaknesses, opportunities, and threats, enabling fast strategic alignment and decision-making.

Weaknesses

Exposure to cyclical capital goods

Core markets such as construction and agriculture, with IMF global growth at about 3.2% in 2024, are highly cyclical and can swing demand for capital goods. Cuts in OEM equipment production quickly transmit to component suppliers, compressing volumes and margins. Accurate forecasting is therefore critical to align inventory and capacity and limit rapid margin erosion.

Scale disadvantage vs mega-cap peers

Helios faces scale disadvantage vs mega-cap peers that typically report annual revenues exceeding $10 billion, while Helios remains in the low‑billion or sub‑billion range. Larger rivals leverage broader portfolios and procurement scale to pressure pricing and fulfillment. They also outspend Helios on R&D and global service networks, intensifying win‑rate pressure on key accounts.

Acquisition integration risk

Strategic M&A is a key growth lever for Helios but adds operational complexity, with systems, culture, and product-roadmap alignment often lagging. Industry experience shows planned synergies frequently slip from 12 months to 24+ months, delaying expected returns. Integration missteps can distract management and compress margins by several hundred basis points during the transition.

Commodity and supply chain sensitivity

Helios faces commodity and supply-chain sensitivity where steel, aluminum and electronic components materially drive COGS; volatility or component shortages can compress gross margins if costs are neither hedged nor passed to customers. Sudden lead-time spikes have previously disrupted delivery reliability, risking customer penalties and lost share. Tight supplier markets increase execution risk across its hydraulics and electronic controls businesses.

- Materials exposure: steel, aluminum, electronics affect COGS

- Margin risk: volatility/shortages squeeze gross margin

- Delivery risk: lead-time spikes disrupt reliability

- Commercial risk: penalties and lost market share

Product concentration in mobile hydraulics

Helios Technologies faces product concentration in mobile hydraulics, leaving performance tied to a narrow set of equipment applications and making revenue susceptible to platform design-outs that can produce lumpy quarters.

Limited diversification into adjacent high-growth niches restricts upside potential, while dependence on large OEM customers increases their negotiating leverage over pricing and terms.

- Exposure to narrow end-markets

- Revenue volatility from platform design-outs

- Low presence in faster-growing adjacent segments

- Higher OEM bargaining power

Cyclical demand, scale gap vs >$10B peers and 12→24+ month M&A drag

Helios is exposed to cyclical end markets (IMF global growth ~3.2% in 2024), causing volatile demand and margin pressure; scale disadvantage vs mega‑caps (> $10B revenue) limits pricing and R&D competitiveness. M&A integration often slips (12 → 24+ months), compressing margins; commodity and supplier volatility raise COGS and delivery risk.

| Metric | Detail |

|---|---|

| Global growth | IMF 2024 ~3.2% |

| Scale gap | Mega‑caps >$10B vs Helios low‑billion |

| Integration risk | Synergies 12 → 24+ months |

| Cost exposure | Steel, aluminum, electronics drive COGS |

Preview the Actual Deliverable

Helios Technologies SWOT Analysis

This is the actual Helios Technologies SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy now to unlock the complete, editable version.

Make Insightful Decisions Backed by Expert Research

Helios Technologies shows strengths in diversified motion-control products and aftermarket revenue, with growth tied to marine and industrial recovery but faces margin pressure from competition and supply-chain risks; our full SWOT dives into financial implications, strategic levers, and scenario planning—purchase the complete, editable report to act with clarity.

Strengths

Integrated hydraulics-electronics platform

Helios Technologies (Nasdaq: HLIO) combines fluid power with electronic controls to deliver integrated motion solutions, creating strong OEM stickiness as customers prefer fewer suppliers and seamless system performance. This integration supports higher average selling prices and improved margins versus stand-alone components, and differentiates Helios from commodity hydraulic suppliers. Integrated offerings also position the company to capture systems-level revenue opportunities.

Diverse end-market exposure

Helios Technologies (NASDAQ: HLIO) serves agriculture, construction, material handling and recreational vehicles, spreading demand risk across cycles. When one sector slows, others can offset revenue swings, supporting resilience. This diversification expands application know-how and enables cross-industry innovation, enhancing product adaptability and aftermarket opportunities.

Global footprint and channels

Operations across Americas, EMEA and APAC enable Helios to provide close support for OEMs and distributors, improving response and service consistency. Localized engineering and manufacturing shorten lead times and allow region-specific customization for industrial and mobile markets. A broad channel mix supports both OEM and aftermarket revenue and reduces single-region macro risk.

Application engineering and custom solutions

Deep domain expertise in fluid power and controls drives tailored performance, supporting Helios's >$1 billion annual revenue (2024) by enabling higher-value system sales. Co-development with OEMs embeds Helios early in platform designs, increasing adoption and design wins. Extensive customization raises switching costs and boosts lifecycle revenue while field feedback from deployments accelerates continuous improvement.

- Deep domain expertise

- Early co-development

- Higher switching costs

- Lifecycle revenue growth

Innovation-driven portfolio

Helios Technologies (NYSE: HLIO) emphasizes efficiency, precision control, and reliability, directly matching customer value drivers and supporting premium pricing power. Electronics, software and IoT features deepen product differentiation and enabled new mobile and industrial platform wins in 2024. Continued R&D investment sustained competitive momentum and higher-margin product mix.

- Focus: efficiency, precision, reliability

- Differentiation: electronics, software, IoT

- R&D: drives platform wins (2024)

- Pricing: premium positioning, pricing power

Fluid-power + electronics drive OEM stickiness, higher ASPs, diversified markets, >$1B 2024

Helios Technologies (Nasdaq: HLIO) integrates fluid power and electronic controls, creating strong OEM stickiness and higher ASPs versus commodity suppliers. Diversified end-markets (agriculture, construction, material handling, RV) and operations across Americas, EMEA, APAC support resilience and service proximity. Deep domain expertise and R&D drove >$1 billion revenue in 2024, enabling premium pricing, lifecycle revenue and systems-level wins.

| Metric | 2024 / Fact |

|---|---|

| Revenue | >$1 billion (2024) |

| Regions | Americas, EMEA, APAC |

| Core markets | Agriculture, construction, material handling, RV |

| Differentiators | Electronics, software, IoT, integrated systems |

What is included in the product

Provides a strategic overview of Helios Technologies’s internal strengths and weaknesses and external opportunities and threats, highlighting key growth drivers, operational gaps, competitive positioning, and market risks shaping its future.

Provides a concise SWOT matrix for Helios Technologies to quickly identify strengths, weaknesses, opportunities, and threats, enabling fast strategic alignment and decision-making.

Weaknesses

Exposure to cyclical capital goods

Core markets such as construction and agriculture, with IMF global growth at about 3.2% in 2024, are highly cyclical and can swing demand for capital goods. Cuts in OEM equipment production quickly transmit to component suppliers, compressing volumes and margins. Accurate forecasting is therefore critical to align inventory and capacity and limit rapid margin erosion.

Scale disadvantage vs mega-cap peers

Helios faces scale disadvantage vs mega-cap peers that typically report annual revenues exceeding $10 billion, while Helios remains in the low‑billion or sub‑billion range. Larger rivals leverage broader portfolios and procurement scale to pressure pricing and fulfillment. They also outspend Helios on R&D and global service networks, intensifying win‑rate pressure on key accounts.

Acquisition integration risk

Strategic M&A is a key growth lever for Helios but adds operational complexity, with systems, culture, and product-roadmap alignment often lagging. Industry experience shows planned synergies frequently slip from 12 months to 24+ months, delaying expected returns. Integration missteps can distract management and compress margins by several hundred basis points during the transition.

Commodity and supply chain sensitivity

Helios faces commodity and supply-chain sensitivity where steel, aluminum and electronic components materially drive COGS; volatility or component shortages can compress gross margins if costs are neither hedged nor passed to customers. Sudden lead-time spikes have previously disrupted delivery reliability, risking customer penalties and lost share. Tight supplier markets increase execution risk across its hydraulics and electronic controls businesses.

- Materials exposure: steel, aluminum, electronics affect COGS

- Margin risk: volatility/shortages squeeze gross margin

- Delivery risk: lead-time spikes disrupt reliability

- Commercial risk: penalties and lost market share

Product concentration in mobile hydraulics

Helios Technologies faces product concentration in mobile hydraulics, leaving performance tied to a narrow set of equipment applications and making revenue susceptible to platform design-outs that can produce lumpy quarters.

Limited diversification into adjacent high-growth niches restricts upside potential, while dependence on large OEM customers increases their negotiating leverage over pricing and terms.

- Exposure to narrow end-markets

- Revenue volatility from platform design-outs

- Low presence in faster-growing adjacent segments

- Higher OEM bargaining power

Cyclical demand, scale gap vs >$10B peers and 12→24+ month M&A drag

Helios is exposed to cyclical end markets (IMF global growth ~3.2% in 2024), causing volatile demand and margin pressure; scale disadvantage vs mega‑caps (> $10B revenue) limits pricing and R&D competitiveness. M&A integration often slips (12 → 24+ months), compressing margins; commodity and supplier volatility raise COGS and delivery risk.

| Metric | Detail |

|---|---|

| Global growth | IMF 2024 ~3.2% |

| Scale gap | Mega‑caps >$10B vs Helios low‑billion |

| Integration risk | Synergies 12 → 24+ months |

| Cost exposure | Steel, aluminum, electronics drive COGS |

Preview the Actual Deliverable

Helios Technologies SWOT Analysis

This is the actual Helios Technologies SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy now to unlock the complete, editable version.

Description

Make Insightful Decisions Backed by Expert Research

Helios Technologies shows strengths in diversified motion-control products and aftermarket revenue, with growth tied to marine and industrial recovery but faces margin pressure from competition and supply-chain risks; our full SWOT dives into financial implications, strategic levers, and scenario planning—purchase the complete, editable report to act with clarity.

Strengths

Integrated hydraulics-electronics platform

Helios Technologies (Nasdaq: HLIO) combines fluid power with electronic controls to deliver integrated motion solutions, creating strong OEM stickiness as customers prefer fewer suppliers and seamless system performance. This integration supports higher average selling prices and improved margins versus stand-alone components, and differentiates Helios from commodity hydraulic suppliers. Integrated offerings also position the company to capture systems-level revenue opportunities.

Diverse end-market exposure

Helios Technologies (NASDAQ: HLIO) serves agriculture, construction, material handling and recreational vehicles, spreading demand risk across cycles. When one sector slows, others can offset revenue swings, supporting resilience. This diversification expands application know-how and enables cross-industry innovation, enhancing product adaptability and aftermarket opportunities.

Global footprint and channels

Operations across Americas, EMEA and APAC enable Helios to provide close support for OEMs and distributors, improving response and service consistency. Localized engineering and manufacturing shorten lead times and allow region-specific customization for industrial and mobile markets. A broad channel mix supports both OEM and aftermarket revenue and reduces single-region macro risk.

Application engineering and custom solutions

Deep domain expertise in fluid power and controls drives tailored performance, supporting Helios's >$1 billion annual revenue (2024) by enabling higher-value system sales. Co-development with OEMs embeds Helios early in platform designs, increasing adoption and design wins. Extensive customization raises switching costs and boosts lifecycle revenue while field feedback from deployments accelerates continuous improvement.

- Deep domain expertise

- Early co-development

- Higher switching costs

- Lifecycle revenue growth

Innovation-driven portfolio

Helios Technologies (NYSE: HLIO) emphasizes efficiency, precision control, and reliability, directly matching customer value drivers and supporting premium pricing power. Electronics, software and IoT features deepen product differentiation and enabled new mobile and industrial platform wins in 2024. Continued R&D investment sustained competitive momentum and higher-margin product mix.

- Focus: efficiency, precision, reliability

- Differentiation: electronics, software, IoT

- R&D: drives platform wins (2024)

- Pricing: premium positioning, pricing power

Fluid-power + electronics drive OEM stickiness, higher ASPs, diversified markets, >$1B 2024

Helios Technologies (Nasdaq: HLIO) integrates fluid power and electronic controls, creating strong OEM stickiness and higher ASPs versus commodity suppliers. Diversified end-markets (agriculture, construction, material handling, RV) and operations across Americas, EMEA, APAC support resilience and service proximity. Deep domain expertise and R&D drove >$1 billion revenue in 2024, enabling premium pricing, lifecycle revenue and systems-level wins.

| Metric | 2024 / Fact |

|---|---|

| Revenue | >$1 billion (2024) |

| Regions | Americas, EMEA, APAC |

| Core markets | Agriculture, construction, material handling, RV |

| Differentiators | Electronics, software, IoT, integrated systems |

What is included in the product

Provides a strategic overview of Helios Technologies’s internal strengths and weaknesses and external opportunities and threats, highlighting key growth drivers, operational gaps, competitive positioning, and market risks shaping its future.

Provides a concise SWOT matrix for Helios Technologies to quickly identify strengths, weaknesses, opportunities, and threats, enabling fast strategic alignment and decision-making.

Weaknesses

Exposure to cyclical capital goods

Core markets such as construction and agriculture, with IMF global growth at about 3.2% in 2024, are highly cyclical and can swing demand for capital goods. Cuts in OEM equipment production quickly transmit to component suppliers, compressing volumes and margins. Accurate forecasting is therefore critical to align inventory and capacity and limit rapid margin erosion.

Scale disadvantage vs mega-cap peers

Helios faces scale disadvantage vs mega-cap peers that typically report annual revenues exceeding $10 billion, while Helios remains in the low‑billion or sub‑billion range. Larger rivals leverage broader portfolios and procurement scale to pressure pricing and fulfillment. They also outspend Helios on R&D and global service networks, intensifying win‑rate pressure on key accounts.

Acquisition integration risk

Strategic M&A is a key growth lever for Helios but adds operational complexity, with systems, culture, and product-roadmap alignment often lagging. Industry experience shows planned synergies frequently slip from 12 months to 24+ months, delaying expected returns. Integration missteps can distract management and compress margins by several hundred basis points during the transition.

Commodity and supply chain sensitivity

Helios faces commodity and supply-chain sensitivity where steel, aluminum and electronic components materially drive COGS; volatility or component shortages can compress gross margins if costs are neither hedged nor passed to customers. Sudden lead-time spikes have previously disrupted delivery reliability, risking customer penalties and lost share. Tight supplier markets increase execution risk across its hydraulics and electronic controls businesses.

- Materials exposure: steel, aluminum, electronics affect COGS

- Margin risk: volatility/shortages squeeze gross margin

- Delivery risk: lead-time spikes disrupt reliability

- Commercial risk: penalties and lost market share

Product concentration in mobile hydraulics

Helios Technologies faces product concentration in mobile hydraulics, leaving performance tied to a narrow set of equipment applications and making revenue susceptible to platform design-outs that can produce lumpy quarters.

Limited diversification into adjacent high-growth niches restricts upside potential, while dependence on large OEM customers increases their negotiating leverage over pricing and terms.

- Exposure to narrow end-markets

- Revenue volatility from platform design-outs

- Low presence in faster-growing adjacent segments

- Higher OEM bargaining power

Cyclical demand, scale gap vs >$10B peers and 12→24+ month M&A drag

Helios is exposed to cyclical end markets (IMF global growth ~3.2% in 2024), causing volatile demand and margin pressure; scale disadvantage vs mega‑caps (> $10B revenue) limits pricing and R&D competitiveness. M&A integration often slips (12 → 24+ months), compressing margins; commodity and supplier volatility raise COGS and delivery risk.

| Metric | Detail |

|---|---|

| Global growth | IMF 2024 ~3.2% |

| Scale gap | Mega‑caps >$10B vs Helios low‑billion |

| Integration risk | Synergies 12 → 24+ months |

| Cost exposure | Steel, aluminum, electronics drive COGS |

Preview the Actual Deliverable

Helios Technologies SWOT Analysis

This is the actual Helios Technologies SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy now to unlock the complete, editable version.