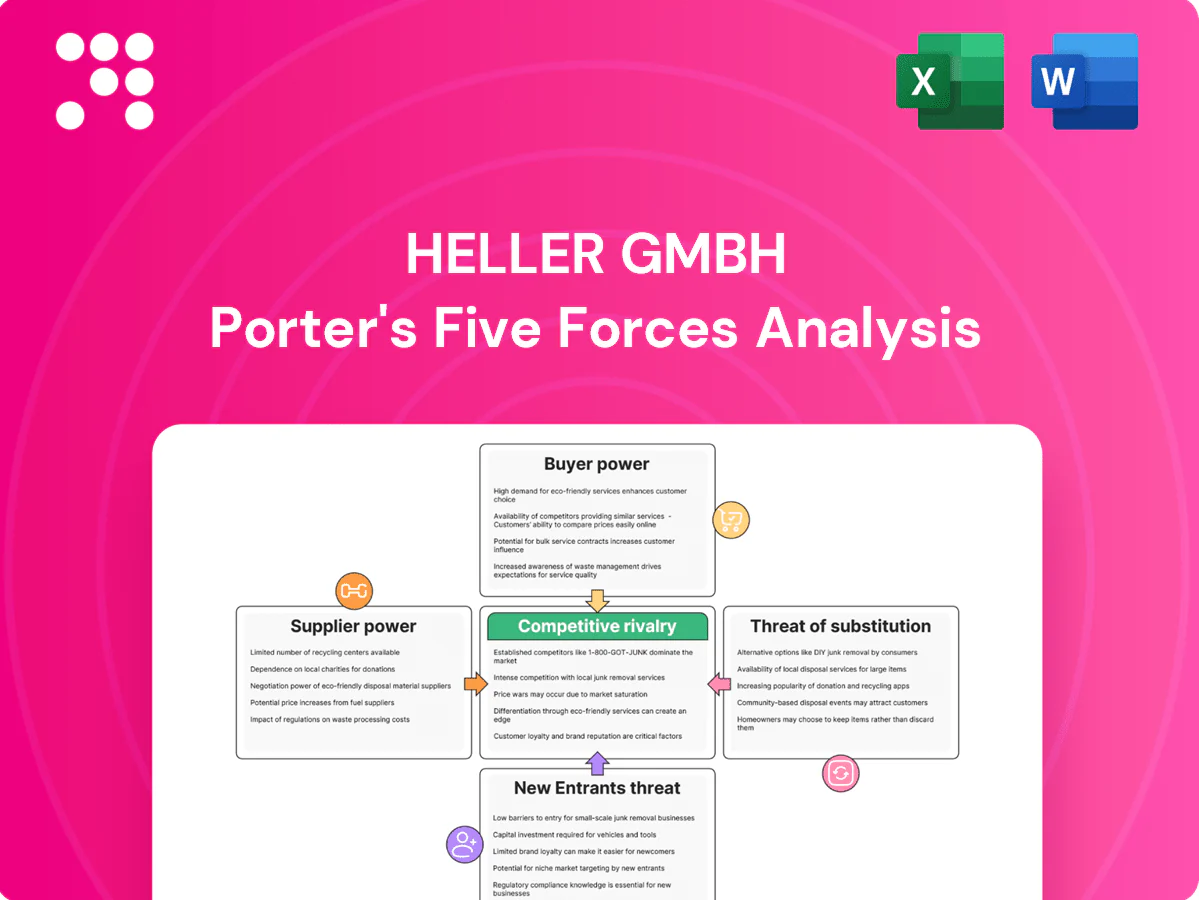

Heller GmbH Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Heller GmbH faces moderate supplier power, high buyer expectations, and niche competitive rivalry shaped by precision-engineering standards. Technological shifts and regulatory changes raise moderate threats of new entrants and substitutes. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Heller GmbH’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated precision component sources

High-spec spindles, linear guides and ball screws are dominated by global leaders such as NSK, SKF, Schaeffler, THK and Bosch Rexroth, and 2024 industry reports confirm these vendors retain the majority of supply. Alternatives exist but often require performance trade-offs and requalification, extending validation times. This concentration can tighten lead times and pricing power; Heller mitigates by maintaining multi-sourcing with 3+ approved suppliers and long-term agreements to stabilize supply.

Control systems dependency

Machine controls from Siemens, Fanuc and Heidenhain are critical components with limited substitutes, giving these suppliers notable bargaining power over Heller. Compatibility requirements and entrenched customer preferences raise switching costs and constrain Heller’s flexibility. Co-development roadmaps with control vendors can further lock in technical and commercial terms. Heller offsets this by differentiating software and offering dual-controller options to reduce dependence.

Materials and casting constraints

High-grade castings and specialty alloys depend on a small number of certified foundries with constrained capacity, making supplier leverage significant; qualification cycles of 6–18 months further raise switching costs. Energy and environmental costs—German industrial electricity ~€0.21/kWh in 2024 and EU ETS prices near €90/tCO2—drive price volatility. Strategic safety stock of 90–180 days and localized sourcing materially reduce disruption risk.

Automation and tooling ecosystem

Automation modules, probes and proprietary tooling interfaces often tie machines to specific vendors, giving suppliers pricing power on add-ons even as the global industrial automation market reached about $214.5B in 2024; OPC UA and IEC standards improve interoperability but integration engineering creates stickiness. Heller’s published open interfaces and expanding in-house integration teams reduce vendor lock-in and margin capture by suppliers.

- OPC UA adoption: 800+ members (2024)

- Market size: $214.5B (2024)

- Supplier add-on margins: elevated due to integration stickiness

- Heller: open interfaces + in-house integration = lower dependence

Geopolitical and logistics exposure

Global supply chains remain exposed to export controls, tariffs and shipping bottlenecks; WTO projected merchandise trade volume growth of just 1.4% in 2023, reflecting weak trade momentum into 2024. Sanctions and regionalization (eg, US CHIPS Act $52 billion) constrain key electronics and motion components, letting suppliers pass costs or prioritize larger customers. Heller’s regional hubs and buffer stocks mitigate immediate shocks and reduce supplier leverage.

- Export controls/tariffs: elevated supplier leverage

- Sanctions/regionalization: tighter electronic component access

- Supplier behavior: cost pass-through, prioritization

- Heller mitigation: regional hubs + buffer inventories

High supplier power; energy €0.21/kWh; EU ETS ~€90/tCO2

Supplier power is high: motion and control leaders (NSK, SKF, Siemens, Fanuc, Heidenhain) limit substitutes, raising prices and lead times. Energy (€0.21/kWh DE 2024) and EU ETS (~€90/tCO2) add cost volatility. Heller uses 3+ approved suppliers, 90–180d safety stock, regional hubs and open interfaces (OPC UA 800+).

| Metric | 2024 value |

|---|---|

| Automation market | $214.5B |

| OPC UA members | 800+ |

| German industrial electricity | €0.21/kWh |

| EU ETS price | ~€90/tCO2 |

What is included in the product

Tailored Porter's Five Forces analysis for Heller GmbH, uncovering competitive intensity, buyer and supplier power, substitute threats, and barriers to entry to clarify strategic risks and profitability drivers.

A one-sheet Porter's Five Forces for Heller GmbH—visual spider chart with customizable pressure levels, no macros, copy-ready layout for decks, easy data swaps and duplicate tabs for scenario testing, and seamless integration into Excel dashboards or reports to speed strategic decisions.

Customers Bargaining Power

Large OEMs and Tier-1s dominate demand

Large OEMs and Tier-1s in automotive, aerospace and machinery buy in large batches and press Heller on price and service through centralized procurement, reducing transaction margins.

Framework agreements, supplier audits and KPIs enforce strict delivery and quality terms, raising compliance costs for Heller.

To defend margin Heller must quantify and sell total cost of ownership improvements—maintenance, uptime and lifecycle savings—rather than price alone.

High switching costs but rational comparisons

Integration, training, and process validation make switching Heller systems costly and slow, often spanning multiple production cycles. In 2024 buyers still benchmark across DMG Mori, Makino, Okuma, Mazak, and Grob when evaluating investments. Demonstrated cycle-time, uptime, and quality advantages sway procurement decisions. Heller reinforces lock-in through application engineering and turnkey delivery.

Customization and acceptance tests

Engineered-to-order options give Heller buyers significant configuration power, with 2024 industry surveys showing about 70% of industrial buyers preferring configurable solutions. Strict FAT/SAT criteria can defer revenue recognition by weeks and force vendor-paid changes, increasing project costs. Tailored machines raise customer stickiness and after-sales services pull-through, boosting lifecycle value. Heller mitigates risk by combining customization with modular platforms.

Total cost of ownership focus

- Energy: 10–30% of operating costs

- Uptime: >98% expected

- Response: ≤4 hours

- Downtime cut: 20–40%

Global aftersales expectations

Multinational buyers demand worldwide parts, service and training, and gaps in local support cut willingness to pay and slow procurement cycles. Rapid service responsiveness drives repeat orders and fleet standardization, increasing lifetime value. Heller’s installed base and service network are primary defenses for maintaining price and margins.

- Worldwide parts & service coverage

- Local support gaps reduce willingness to pay

- Service responsiveness ↔ repeat orders & standardization

- Installed base & network defend price

Buyers demand >98% uptime, ≤4h response, 20–40% downtime cut

Large OEMs and Tier‑1s exert strong price/service pressure via centralized procurement and framework contracts, compressing margins.

Buyers focus on TCO—uptime, energy, tool life—with >98% uptime and ≤4h response expected; 70% prefer configurable solutions in 2024.

Heller cites 20–40% downtime reduction from digital services and leverages installed base and global service to defend pricing.

| Metric | Buyer Expectation | Heller 2024 |

|---|---|---|

| Uptime | >98% | ~98–99% |

| Response | ≤4h | ≤4h |

| Downtime cut | - | 20–40% |

Preview Before You Purchase

Heller GmbH Porter's Five Forces Analysis

This preview shows the exact Heller GmbH Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted report covering competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry. You’ll get instant access to this same ready-to-use document upon payment.

From Overview to Strategy Blueprint

Heller GmbH faces moderate supplier power, high buyer expectations, and niche competitive rivalry shaped by precision-engineering standards. Technological shifts and regulatory changes raise moderate threats of new entrants and substitutes. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Heller GmbH’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated precision component sources

High-spec spindles, linear guides and ball screws are dominated by global leaders such as NSK, SKF, Schaeffler, THK and Bosch Rexroth, and 2024 industry reports confirm these vendors retain the majority of supply. Alternatives exist but often require performance trade-offs and requalification, extending validation times. This concentration can tighten lead times and pricing power; Heller mitigates by maintaining multi-sourcing with 3+ approved suppliers and long-term agreements to stabilize supply.

Control systems dependency

Machine controls from Siemens, Fanuc and Heidenhain are critical components with limited substitutes, giving these suppliers notable bargaining power over Heller. Compatibility requirements and entrenched customer preferences raise switching costs and constrain Heller’s flexibility. Co-development roadmaps with control vendors can further lock in technical and commercial terms. Heller offsets this by differentiating software and offering dual-controller options to reduce dependence.

Materials and casting constraints

High-grade castings and specialty alloys depend on a small number of certified foundries with constrained capacity, making supplier leverage significant; qualification cycles of 6–18 months further raise switching costs. Energy and environmental costs—German industrial electricity ~€0.21/kWh in 2024 and EU ETS prices near €90/tCO2—drive price volatility. Strategic safety stock of 90–180 days and localized sourcing materially reduce disruption risk.

Automation and tooling ecosystem

Automation modules, probes and proprietary tooling interfaces often tie machines to specific vendors, giving suppliers pricing power on add-ons even as the global industrial automation market reached about $214.5B in 2024; OPC UA and IEC standards improve interoperability but integration engineering creates stickiness. Heller’s published open interfaces and expanding in-house integration teams reduce vendor lock-in and margin capture by suppliers.

- OPC UA adoption: 800+ members (2024)

- Market size: $214.5B (2024)

- Supplier add-on margins: elevated due to integration stickiness

- Heller: open interfaces + in-house integration = lower dependence

Geopolitical and logistics exposure

Global supply chains remain exposed to export controls, tariffs and shipping bottlenecks; WTO projected merchandise trade volume growth of just 1.4% in 2023, reflecting weak trade momentum into 2024. Sanctions and regionalization (eg, US CHIPS Act $52 billion) constrain key electronics and motion components, letting suppliers pass costs or prioritize larger customers. Heller’s regional hubs and buffer stocks mitigate immediate shocks and reduce supplier leverage.

- Export controls/tariffs: elevated supplier leverage

- Sanctions/regionalization: tighter electronic component access

- Supplier behavior: cost pass-through, prioritization

- Heller mitigation: regional hubs + buffer inventories

High supplier power; energy €0.21/kWh; EU ETS ~€90/tCO2

Supplier power is high: motion and control leaders (NSK, SKF, Siemens, Fanuc, Heidenhain) limit substitutes, raising prices and lead times. Energy (€0.21/kWh DE 2024) and EU ETS (~€90/tCO2) add cost volatility. Heller uses 3+ approved suppliers, 90–180d safety stock, regional hubs and open interfaces (OPC UA 800+).

| Metric | 2024 value |

|---|---|

| Automation market | $214.5B |

| OPC UA members | 800+ |

| German industrial electricity | €0.21/kWh |

| EU ETS price | ~€90/tCO2 |

What is included in the product

Tailored Porter's Five Forces analysis for Heller GmbH, uncovering competitive intensity, buyer and supplier power, substitute threats, and barriers to entry to clarify strategic risks and profitability drivers.

A one-sheet Porter's Five Forces for Heller GmbH—visual spider chart with customizable pressure levels, no macros, copy-ready layout for decks, easy data swaps and duplicate tabs for scenario testing, and seamless integration into Excel dashboards or reports to speed strategic decisions.

Customers Bargaining Power

Large OEMs and Tier-1s dominate demand

Large OEMs and Tier-1s in automotive, aerospace and machinery buy in large batches and press Heller on price and service through centralized procurement, reducing transaction margins.

Framework agreements, supplier audits and KPIs enforce strict delivery and quality terms, raising compliance costs for Heller.

To defend margin Heller must quantify and sell total cost of ownership improvements—maintenance, uptime and lifecycle savings—rather than price alone.

High switching costs but rational comparisons

Integration, training, and process validation make switching Heller systems costly and slow, often spanning multiple production cycles. In 2024 buyers still benchmark across DMG Mori, Makino, Okuma, Mazak, and Grob when evaluating investments. Demonstrated cycle-time, uptime, and quality advantages sway procurement decisions. Heller reinforces lock-in through application engineering and turnkey delivery.

Customization and acceptance tests

Engineered-to-order options give Heller buyers significant configuration power, with 2024 industry surveys showing about 70% of industrial buyers preferring configurable solutions. Strict FAT/SAT criteria can defer revenue recognition by weeks and force vendor-paid changes, increasing project costs. Tailored machines raise customer stickiness and after-sales services pull-through, boosting lifecycle value. Heller mitigates risk by combining customization with modular platforms.

Total cost of ownership focus

- Energy: 10–30% of operating costs

- Uptime: >98% expected

- Response: ≤4 hours

- Downtime cut: 20–40%

Global aftersales expectations

Multinational buyers demand worldwide parts, service and training, and gaps in local support cut willingness to pay and slow procurement cycles. Rapid service responsiveness drives repeat orders and fleet standardization, increasing lifetime value. Heller’s installed base and service network are primary defenses for maintaining price and margins.

- Worldwide parts & service coverage

- Local support gaps reduce willingness to pay

- Service responsiveness ↔ repeat orders & standardization

- Installed base & network defend price

Buyers demand >98% uptime, ≤4h response, 20–40% downtime cut

Large OEMs and Tier‑1s exert strong price/service pressure via centralized procurement and framework contracts, compressing margins.

Buyers focus on TCO—uptime, energy, tool life—with >98% uptime and ≤4h response expected; 70% prefer configurable solutions in 2024.

Heller cites 20–40% downtime reduction from digital services and leverages installed base and global service to defend pricing.

| Metric | Buyer Expectation | Heller 2024 |

|---|---|---|

| Uptime | >98% | ~98–99% |

| Response | ≤4h | ≤4h |

| Downtime cut | - | 20–40% |

Preview Before You Purchase

Heller GmbH Porter's Five Forces Analysis

This preview shows the exact Heller GmbH Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted report covering competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry. You’ll get instant access to this same ready-to-use document upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Heller GmbH faces moderate supplier power, high buyer expectations, and niche competitive rivalry shaped by precision-engineering standards. Technological shifts and regulatory changes raise moderate threats of new entrants and substitutes. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Heller GmbH’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated precision component sources

High-spec spindles, linear guides and ball screws are dominated by global leaders such as NSK, SKF, Schaeffler, THK and Bosch Rexroth, and 2024 industry reports confirm these vendors retain the majority of supply. Alternatives exist but often require performance trade-offs and requalification, extending validation times. This concentration can tighten lead times and pricing power; Heller mitigates by maintaining multi-sourcing with 3+ approved suppliers and long-term agreements to stabilize supply.

Control systems dependency

Machine controls from Siemens, Fanuc and Heidenhain are critical components with limited substitutes, giving these suppliers notable bargaining power over Heller. Compatibility requirements and entrenched customer preferences raise switching costs and constrain Heller’s flexibility. Co-development roadmaps with control vendors can further lock in technical and commercial terms. Heller offsets this by differentiating software and offering dual-controller options to reduce dependence.

Materials and casting constraints

High-grade castings and specialty alloys depend on a small number of certified foundries with constrained capacity, making supplier leverage significant; qualification cycles of 6–18 months further raise switching costs. Energy and environmental costs—German industrial electricity ~€0.21/kWh in 2024 and EU ETS prices near €90/tCO2—drive price volatility. Strategic safety stock of 90–180 days and localized sourcing materially reduce disruption risk.

Automation and tooling ecosystem

Automation modules, probes and proprietary tooling interfaces often tie machines to specific vendors, giving suppliers pricing power on add-ons even as the global industrial automation market reached about $214.5B in 2024; OPC UA and IEC standards improve interoperability but integration engineering creates stickiness. Heller’s published open interfaces and expanding in-house integration teams reduce vendor lock-in and margin capture by suppliers.

- OPC UA adoption: 800+ members (2024)

- Market size: $214.5B (2024)

- Supplier add-on margins: elevated due to integration stickiness

- Heller: open interfaces + in-house integration = lower dependence

Geopolitical and logistics exposure

Global supply chains remain exposed to export controls, tariffs and shipping bottlenecks; WTO projected merchandise trade volume growth of just 1.4% in 2023, reflecting weak trade momentum into 2024. Sanctions and regionalization (eg, US CHIPS Act $52 billion) constrain key electronics and motion components, letting suppliers pass costs or prioritize larger customers. Heller’s regional hubs and buffer stocks mitigate immediate shocks and reduce supplier leverage.

- Export controls/tariffs: elevated supplier leverage

- Sanctions/regionalization: tighter electronic component access

- Supplier behavior: cost pass-through, prioritization

- Heller mitigation: regional hubs + buffer inventories

High supplier power; energy €0.21/kWh; EU ETS ~€90/tCO2

Supplier power is high: motion and control leaders (NSK, SKF, Siemens, Fanuc, Heidenhain) limit substitutes, raising prices and lead times. Energy (€0.21/kWh DE 2024) and EU ETS (~€90/tCO2) add cost volatility. Heller uses 3+ approved suppliers, 90–180d safety stock, regional hubs and open interfaces (OPC UA 800+).

| Metric | 2024 value |

|---|---|

| Automation market | $214.5B |

| OPC UA members | 800+ |

| German industrial electricity | €0.21/kWh |

| EU ETS price | ~€90/tCO2 |

What is included in the product

Tailored Porter's Five Forces analysis for Heller GmbH, uncovering competitive intensity, buyer and supplier power, substitute threats, and barriers to entry to clarify strategic risks and profitability drivers.

A one-sheet Porter's Five Forces for Heller GmbH—visual spider chart with customizable pressure levels, no macros, copy-ready layout for decks, easy data swaps and duplicate tabs for scenario testing, and seamless integration into Excel dashboards or reports to speed strategic decisions.

Customers Bargaining Power

Large OEMs and Tier-1s dominate demand

Large OEMs and Tier-1s in automotive, aerospace and machinery buy in large batches and press Heller on price and service through centralized procurement, reducing transaction margins.

Framework agreements, supplier audits and KPIs enforce strict delivery and quality terms, raising compliance costs for Heller.

To defend margin Heller must quantify and sell total cost of ownership improvements—maintenance, uptime and lifecycle savings—rather than price alone.

High switching costs but rational comparisons

Integration, training, and process validation make switching Heller systems costly and slow, often spanning multiple production cycles. In 2024 buyers still benchmark across DMG Mori, Makino, Okuma, Mazak, and Grob when evaluating investments. Demonstrated cycle-time, uptime, and quality advantages sway procurement decisions. Heller reinforces lock-in through application engineering and turnkey delivery.

Customization and acceptance tests

Engineered-to-order options give Heller buyers significant configuration power, with 2024 industry surveys showing about 70% of industrial buyers preferring configurable solutions. Strict FAT/SAT criteria can defer revenue recognition by weeks and force vendor-paid changes, increasing project costs. Tailored machines raise customer stickiness and after-sales services pull-through, boosting lifecycle value. Heller mitigates risk by combining customization with modular platforms.

Total cost of ownership focus

- Energy: 10–30% of operating costs

- Uptime: >98% expected

- Response: ≤4 hours

- Downtime cut: 20–40%

Global aftersales expectations

Multinational buyers demand worldwide parts, service and training, and gaps in local support cut willingness to pay and slow procurement cycles. Rapid service responsiveness drives repeat orders and fleet standardization, increasing lifetime value. Heller’s installed base and service network are primary defenses for maintaining price and margins.

- Worldwide parts & service coverage

- Local support gaps reduce willingness to pay

- Service responsiveness ↔ repeat orders & standardization

- Installed base & network defend price

Buyers demand >98% uptime, ≤4h response, 20–40% downtime cut

Large OEMs and Tier‑1s exert strong price/service pressure via centralized procurement and framework contracts, compressing margins.

Buyers focus on TCO—uptime, energy, tool life—with >98% uptime and ≤4h response expected; 70% prefer configurable solutions in 2024.

Heller cites 20–40% downtime reduction from digital services and leverages installed base and global service to defend pricing.

| Metric | Buyer Expectation | Heller 2024 |

|---|---|---|

| Uptime | >98% | ~98–99% |

| Response | ≤4h | ≤4h |

| Downtime cut | - | 20–40% |

Preview Before You Purchase

Heller GmbH Porter's Five Forces Analysis

This preview shows the exact Heller GmbH Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The file is the full, professionally formatted report covering competitive rivalry, supplier power, buyer power, threat of substitutes, and barriers to entry. You’ll get instant access to this same ready-to-use document upon payment.