Hellenic Petroleum PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how political shifts, energy markets, regulation, and sustainability trends are reshaping Hellenic Petroleum’s strategy and risk profile—our PESTLE delivers actionable insights and clear implications for investors and managers. Purchase the full, ready-to-use analysis now to access the complete breakdown and practical recommendations.

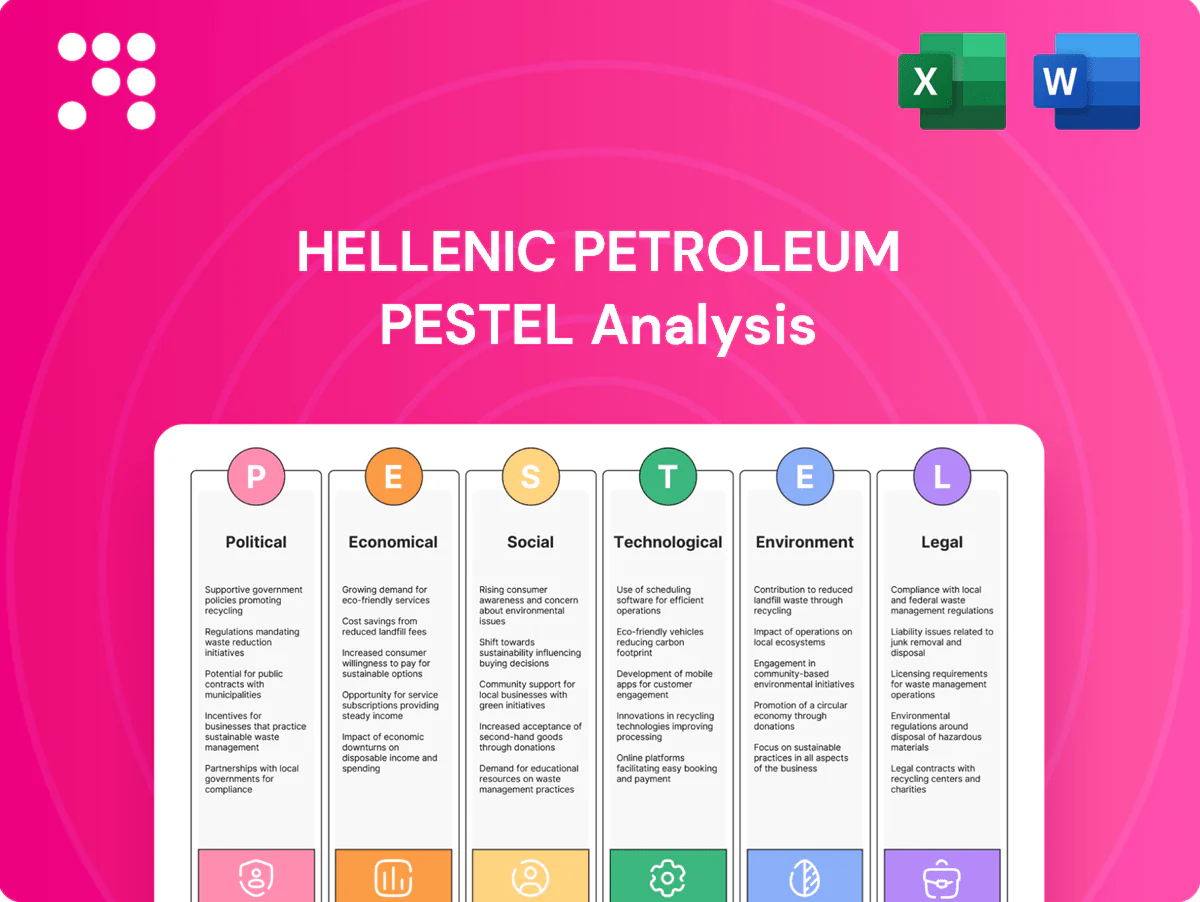

Political factors

EU energy and climate policy alignment

HELLENiQ ENERGY must align with Fit for 55 (EU target of -55% GHG by 2030) and REPowerEU plus Greece’s national decarbonization plans; these policy trajectories channel capital to renewables, efficiency and lower‑carbon fuels as EU 2030 renewables target is ~42.5%. Non‑compliance risks stranded assets and reduced access to EU funding (NextGenerationEU ~800bn) and incentives. Proactive engagement can secure permits and subsidies for transition projects.

Geopolitical supply security in SE Europe

Ukraine war, Eastern Mediterranean exploration and Balkan logistics reshape crude sourcing and gas flows, with Hellenic Petroleum operating ~320 kbpd refining capacity amid regional rerouting. Diversification into LNG (Revithoussa ~5 bcm/y), pipeline alternatives (TAP ~10 bcm/y) and storage — aligned with EU 90% storage targets — is politically encouraged. Supply shocks can squeeze refining margins or produce windfall margins depending on product balance. Diplomatic positioning dictates E&P access and offtake terms.

State influence and stakeholder expectations

Government stakes and national energy priorities steer Hellenic Petroleum’s governance and investment pacing, as policymakers balance energy security, consumer prices and climate goals—notably the EU -55% 2030 target and Greece’s net-zero by 2050 commitment. Public-private coordination funds large infrastructure like grids and interconnectors, while policy stability lowers financing costs; volatility raises risk premiums and delays long-cycle refinery and power projects.

Subsidies, taxes, and windfall measures

Excise taxes, carbon-related levies and occasional windfall taxes (applied across EU energy firms in 2022–23) directly squeeze Hellenic Petroleum margins; EU ETS carbon prices around €90/t in 2024–25 materially raise fuel costs. Subsidies for RES, hydrogen and efficiency programmes can partially offset these charges and lower project IRRs. Predictability of fiscal regimes determines investment returns and timing, while strong policy signals catalyze portfolio rebalancing toward low-carbon assets.

Regional integration and market liberalization

EU internal energy market rules promote cross-border competition and access; Single Day-Ahead Coupling now covers about 30 countries and ~96% of EU consumption, increasing price convergence. Power and gas liberalization expands trading and retail opportunities while compressing legacy refining and retail margins. Market coupling reshapes pricing and hedging strategies; participation in regional exchanges improves optimization of refining and generation assets.

- Cross-border access: SDAC ~30 countries, ~96% coverage

- Liberalization: more trading/retail, lower legacy margins

- Market coupling: tighter price correlation, new hedging needs

- Regional exchanges: better asset optimization

Align Greek energy with Fit for 55 and EU 42.5% 2030 renewables

HELLENiQ ENERGY must align with Fit for 55/REPowerEU and Greece net‑zero 2050; EU 2030 renewables target ≈42.5% channels capital and NextGenerationEU ≈€800bn funds.

Ukraine war and EMed/Balkan shifts affect crude sourcing for ~320 kbpd refining capacity and gas flows (Revithoussa ~5 bcm/y; TAP ~10 bcm/y), altering margins.

EU ETS ≈€90/t (2024–25) and prior windfall taxes squeeze margins; RES/hydrogen subsidies partly offset costs.

| Indicator | Value |

|---|---|

| Refining capacity | ~320 kbpd |

| EU ETS price | ≈€90/t (2024–25) |

| Storage/LNG | Revithoussa ~5 bcm/y |

| Pipeline | TAP ~10 bcm/y |

What is included in the product

Provides a concise PESTLE evaluation of Hellenic Petroleum, detailing political, economic, social, technological, environmental and legal drivers with data-backed trends and region-specific regulatory context to help executives and investors identify risks, opportunities and forward-looking scenarios for strategic planning.

A concise, visually segmented PESTLE summary for Hellenic Petroleum that relieves briefing pain points by enabling quick interpretation, easy sharing across teams, and drop‑in use in presentations or strategy sessions.

Economic factors

Refining margins and crude price volatility

Brent averaged about $86/bbl in 2024 as OPEC+ maintained roughly 3 mb/d of voluntary cuts, widening spreads and driving volatile product cracks (3-2-1 crack swings roughly $8–22/bbl in 2024), which creates pronounced earnings cyclicality for Hellenic Petroleum. The group’s complex EU refineries and crude flexibility mitigate shock exposure, while effective hedging and inventory management have smoothed cash flows. Margin cycles continue to dictate capex timing, with group capex guidance around €250–300m for the near term.

Gas and power market dynamics

Gas hub TTF averaging ~45 EUR/MWh in 2024 and rising power demand (+2% y/y in Greece 2024) directly tighten generation margins and retail competitiveness. Capacity mechanisms and RES penetration (~33% of Greek power in 2024) compress spark spreads, shifting economics toward flexible assets. High price volatility forces robust hedging, risk management and dynamic customer pricing. An integrated gas-power strategy smooths EBITDA swings and improves margin capture.

Interest rates, inflation, and capex intensity

Higher policy rates (ECB ~4.00% in mid-2025) lift WACC, making long-dated RES, hydrogen and CCS projects harder to finance and reducing net present value for HELPE’s transition pipeline.

Inflation (Eurozone ~2.5% in 2024) has pushed EPC and O&M costs higher, inflating project budgets and near-term operating expenses.

Prioritizing high-IRR, de-risked projects preserves balance-sheet resilience; tapping green finance (green bonds/EBRD/EIB) can materially lower funding costs and improve leverage metrics.

FX exposure and trade flows

Refining inputs like crude are dollar-priced while Hellenic Petroleum records sales in euros, exposing margins to EUR/USD moves; EUR/USD averaged about 1.09 in H1 2025, amplifying input cost volatility.

Regional exports/imports have shifted since 2022 due to sanctions and demand, with Mediterranean trade flows and freight rate swings altering route economics.

Active trade optimization and FX hedging programs, plus logistics flexibility (chartering and storage), help capture arbitrage and protect margins.

- EUR/USD ~1.09 (H1 2025)

- Sanctions-driven trade shifts since 2022

- Hedging + logistics = margin protection

Consumer demand and price elasticity

Fuel demand at Hellenic Petroleum remains tightly linked to macro growth and tourism seasonality—Greece recorded about 27.6 million tourist arrivals in 2023—while pump-price sensitivity drives short-term volume swings; gradual efficiency gains and EV uptake (global EV share of new passenger car sales ~14% in 2023 per IEA) trim volumes but support higher-margin premium products. Petrochemicals move with industrial and construction cycles, and expanded renewables and services reduce cyclical exposure.

- Demand sensitivity: macro growth + tourism

- Price elasticity: pump prices drive short-term volumes

- Structural trends: EVs (14% new car share 2023) and efficiency lower volumes

- Mix & resilience: premium products, petrochemicals track industry, renewables diversify

Align Greek energy with Fit for 55 and EU 42.5% 2030 renewables

Brent ~$86/bbl avg 2024; 3–2–1 crack swings $8–22/bbl drive earnings cyclicality. TTF ~45 EUR/MWh 2024; Greek power demand +2% y/y 2024; RES ~33%. ECB ~4.0% mid‑2025 raises WACC; Eurozone inflation ~2.5% 2024; EUR/USD ~1.09 H1 2025 impacts margins.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| TTF 2024 | €45/MWh |

| ECB rate | ~4.0% (mid‑2025) |

| EUR/USD H1 2025 | 1.09 |

Same Document Delivered

Hellenic Petroleum PESTLE Analysis

The preview shown here is the exact Hellenic Petroleum PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—what you see is the final, downloadable document.

Skip the Research. Get the Strategy.

Understand how political shifts, energy markets, regulation, and sustainability trends are reshaping Hellenic Petroleum’s strategy and risk profile—our PESTLE delivers actionable insights and clear implications for investors and managers. Purchase the full, ready-to-use analysis now to access the complete breakdown and practical recommendations.

Political factors

EU energy and climate policy alignment

HELLENiQ ENERGY must align with Fit for 55 (EU target of -55% GHG by 2030) and REPowerEU plus Greece’s national decarbonization plans; these policy trajectories channel capital to renewables, efficiency and lower‑carbon fuels as EU 2030 renewables target is ~42.5%. Non‑compliance risks stranded assets and reduced access to EU funding (NextGenerationEU ~800bn) and incentives. Proactive engagement can secure permits and subsidies for transition projects.

Geopolitical supply security in SE Europe

Ukraine war, Eastern Mediterranean exploration and Balkan logistics reshape crude sourcing and gas flows, with Hellenic Petroleum operating ~320 kbpd refining capacity amid regional rerouting. Diversification into LNG (Revithoussa ~5 bcm/y), pipeline alternatives (TAP ~10 bcm/y) and storage — aligned with EU 90% storage targets — is politically encouraged. Supply shocks can squeeze refining margins or produce windfall margins depending on product balance. Diplomatic positioning dictates E&P access and offtake terms.

State influence and stakeholder expectations

Government stakes and national energy priorities steer Hellenic Petroleum’s governance and investment pacing, as policymakers balance energy security, consumer prices and climate goals—notably the EU -55% 2030 target and Greece’s net-zero by 2050 commitment. Public-private coordination funds large infrastructure like grids and interconnectors, while policy stability lowers financing costs; volatility raises risk premiums and delays long-cycle refinery and power projects.

Subsidies, taxes, and windfall measures

Excise taxes, carbon-related levies and occasional windfall taxes (applied across EU energy firms in 2022–23) directly squeeze Hellenic Petroleum margins; EU ETS carbon prices around €90/t in 2024–25 materially raise fuel costs. Subsidies for RES, hydrogen and efficiency programmes can partially offset these charges and lower project IRRs. Predictability of fiscal regimes determines investment returns and timing, while strong policy signals catalyze portfolio rebalancing toward low-carbon assets.

Regional integration and market liberalization

EU internal energy market rules promote cross-border competition and access; Single Day-Ahead Coupling now covers about 30 countries and ~96% of EU consumption, increasing price convergence. Power and gas liberalization expands trading and retail opportunities while compressing legacy refining and retail margins. Market coupling reshapes pricing and hedging strategies; participation in regional exchanges improves optimization of refining and generation assets.

- Cross-border access: SDAC ~30 countries, ~96% coverage

- Liberalization: more trading/retail, lower legacy margins

- Market coupling: tighter price correlation, new hedging needs

- Regional exchanges: better asset optimization

Align Greek energy with Fit for 55 and EU 42.5% 2030 renewables

HELLENiQ ENERGY must align with Fit for 55/REPowerEU and Greece net‑zero 2050; EU 2030 renewables target ≈42.5% channels capital and NextGenerationEU ≈€800bn funds.

Ukraine war and EMed/Balkan shifts affect crude sourcing for ~320 kbpd refining capacity and gas flows (Revithoussa ~5 bcm/y; TAP ~10 bcm/y), altering margins.

EU ETS ≈€90/t (2024–25) and prior windfall taxes squeeze margins; RES/hydrogen subsidies partly offset costs.

| Indicator | Value |

|---|---|

| Refining capacity | ~320 kbpd |

| EU ETS price | ≈€90/t (2024–25) |

| Storage/LNG | Revithoussa ~5 bcm/y |

| Pipeline | TAP ~10 bcm/y |

What is included in the product

Provides a concise PESTLE evaluation of Hellenic Petroleum, detailing political, economic, social, technological, environmental and legal drivers with data-backed trends and region-specific regulatory context to help executives and investors identify risks, opportunities and forward-looking scenarios for strategic planning.

A concise, visually segmented PESTLE summary for Hellenic Petroleum that relieves briefing pain points by enabling quick interpretation, easy sharing across teams, and drop‑in use in presentations or strategy sessions.

Economic factors

Refining margins and crude price volatility

Brent averaged about $86/bbl in 2024 as OPEC+ maintained roughly 3 mb/d of voluntary cuts, widening spreads and driving volatile product cracks (3-2-1 crack swings roughly $8–22/bbl in 2024), which creates pronounced earnings cyclicality for Hellenic Petroleum. The group’s complex EU refineries and crude flexibility mitigate shock exposure, while effective hedging and inventory management have smoothed cash flows. Margin cycles continue to dictate capex timing, with group capex guidance around €250–300m for the near term.

Gas and power market dynamics

Gas hub TTF averaging ~45 EUR/MWh in 2024 and rising power demand (+2% y/y in Greece 2024) directly tighten generation margins and retail competitiveness. Capacity mechanisms and RES penetration (~33% of Greek power in 2024) compress spark spreads, shifting economics toward flexible assets. High price volatility forces robust hedging, risk management and dynamic customer pricing. An integrated gas-power strategy smooths EBITDA swings and improves margin capture.

Interest rates, inflation, and capex intensity

Higher policy rates (ECB ~4.00% in mid-2025) lift WACC, making long-dated RES, hydrogen and CCS projects harder to finance and reducing net present value for HELPE’s transition pipeline.

Inflation (Eurozone ~2.5% in 2024) has pushed EPC and O&M costs higher, inflating project budgets and near-term operating expenses.

Prioritizing high-IRR, de-risked projects preserves balance-sheet resilience; tapping green finance (green bonds/EBRD/EIB) can materially lower funding costs and improve leverage metrics.

FX exposure and trade flows

Refining inputs like crude are dollar-priced while Hellenic Petroleum records sales in euros, exposing margins to EUR/USD moves; EUR/USD averaged about 1.09 in H1 2025, amplifying input cost volatility.

Regional exports/imports have shifted since 2022 due to sanctions and demand, with Mediterranean trade flows and freight rate swings altering route economics.

Active trade optimization and FX hedging programs, plus logistics flexibility (chartering and storage), help capture arbitrage and protect margins.

- EUR/USD ~1.09 (H1 2025)

- Sanctions-driven trade shifts since 2022

- Hedging + logistics = margin protection

Consumer demand and price elasticity

Fuel demand at Hellenic Petroleum remains tightly linked to macro growth and tourism seasonality—Greece recorded about 27.6 million tourist arrivals in 2023—while pump-price sensitivity drives short-term volume swings; gradual efficiency gains and EV uptake (global EV share of new passenger car sales ~14% in 2023 per IEA) trim volumes but support higher-margin premium products. Petrochemicals move with industrial and construction cycles, and expanded renewables and services reduce cyclical exposure.

- Demand sensitivity: macro growth + tourism

- Price elasticity: pump prices drive short-term volumes

- Structural trends: EVs (14% new car share 2023) and efficiency lower volumes

- Mix & resilience: premium products, petrochemicals track industry, renewables diversify

Align Greek energy with Fit for 55 and EU 42.5% 2030 renewables

Brent ~$86/bbl avg 2024; 3–2–1 crack swings $8–22/bbl drive earnings cyclicality. TTF ~45 EUR/MWh 2024; Greek power demand +2% y/y 2024; RES ~33%. ECB ~4.0% mid‑2025 raises WACC; Eurozone inflation ~2.5% 2024; EUR/USD ~1.09 H1 2025 impacts margins.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| TTF 2024 | €45/MWh |

| ECB rate | ~4.0% (mid‑2025) |

| EUR/USD H1 2025 | 1.09 |

Same Document Delivered

Hellenic Petroleum PESTLE Analysis

The preview shown here is the exact Hellenic Petroleum PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—what you see is the final, downloadable document.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Understand how political shifts, energy markets, regulation, and sustainability trends are reshaping Hellenic Petroleum’s strategy and risk profile—our PESTLE delivers actionable insights and clear implications for investors and managers. Purchase the full, ready-to-use analysis now to access the complete breakdown and practical recommendations.

Political factors

EU energy and climate policy alignment

HELLENiQ ENERGY must align with Fit for 55 (EU target of -55% GHG by 2030) and REPowerEU plus Greece’s national decarbonization plans; these policy trajectories channel capital to renewables, efficiency and lower‑carbon fuels as EU 2030 renewables target is ~42.5%. Non‑compliance risks stranded assets and reduced access to EU funding (NextGenerationEU ~800bn) and incentives. Proactive engagement can secure permits and subsidies for transition projects.

Geopolitical supply security in SE Europe

Ukraine war, Eastern Mediterranean exploration and Balkan logistics reshape crude sourcing and gas flows, with Hellenic Petroleum operating ~320 kbpd refining capacity amid regional rerouting. Diversification into LNG (Revithoussa ~5 bcm/y), pipeline alternatives (TAP ~10 bcm/y) and storage — aligned with EU 90% storage targets — is politically encouraged. Supply shocks can squeeze refining margins or produce windfall margins depending on product balance. Diplomatic positioning dictates E&P access and offtake terms.

State influence and stakeholder expectations

Government stakes and national energy priorities steer Hellenic Petroleum’s governance and investment pacing, as policymakers balance energy security, consumer prices and climate goals—notably the EU -55% 2030 target and Greece’s net-zero by 2050 commitment. Public-private coordination funds large infrastructure like grids and interconnectors, while policy stability lowers financing costs; volatility raises risk premiums and delays long-cycle refinery and power projects.

Subsidies, taxes, and windfall measures

Excise taxes, carbon-related levies and occasional windfall taxes (applied across EU energy firms in 2022–23) directly squeeze Hellenic Petroleum margins; EU ETS carbon prices around €90/t in 2024–25 materially raise fuel costs. Subsidies for RES, hydrogen and efficiency programmes can partially offset these charges and lower project IRRs. Predictability of fiscal regimes determines investment returns and timing, while strong policy signals catalyze portfolio rebalancing toward low-carbon assets.

Regional integration and market liberalization

EU internal energy market rules promote cross-border competition and access; Single Day-Ahead Coupling now covers about 30 countries and ~96% of EU consumption, increasing price convergence. Power and gas liberalization expands trading and retail opportunities while compressing legacy refining and retail margins. Market coupling reshapes pricing and hedging strategies; participation in regional exchanges improves optimization of refining and generation assets.

- Cross-border access: SDAC ~30 countries, ~96% coverage

- Liberalization: more trading/retail, lower legacy margins

- Market coupling: tighter price correlation, new hedging needs

- Regional exchanges: better asset optimization

Align Greek energy with Fit for 55 and EU 42.5% 2030 renewables

HELLENiQ ENERGY must align with Fit for 55/REPowerEU and Greece net‑zero 2050; EU 2030 renewables target ≈42.5% channels capital and NextGenerationEU ≈€800bn funds.

Ukraine war and EMed/Balkan shifts affect crude sourcing for ~320 kbpd refining capacity and gas flows (Revithoussa ~5 bcm/y; TAP ~10 bcm/y), altering margins.

EU ETS ≈€90/t (2024–25) and prior windfall taxes squeeze margins; RES/hydrogen subsidies partly offset costs.

| Indicator | Value |

|---|---|

| Refining capacity | ~320 kbpd |

| EU ETS price | ≈€90/t (2024–25) |

| Storage/LNG | Revithoussa ~5 bcm/y |

| Pipeline | TAP ~10 bcm/y |

What is included in the product

Provides a concise PESTLE evaluation of Hellenic Petroleum, detailing political, economic, social, technological, environmental and legal drivers with data-backed trends and region-specific regulatory context to help executives and investors identify risks, opportunities and forward-looking scenarios for strategic planning.

A concise, visually segmented PESTLE summary for Hellenic Petroleum that relieves briefing pain points by enabling quick interpretation, easy sharing across teams, and drop‑in use in presentations or strategy sessions.

Economic factors

Refining margins and crude price volatility

Brent averaged about $86/bbl in 2024 as OPEC+ maintained roughly 3 mb/d of voluntary cuts, widening spreads and driving volatile product cracks (3-2-1 crack swings roughly $8–22/bbl in 2024), which creates pronounced earnings cyclicality for Hellenic Petroleum. The group’s complex EU refineries and crude flexibility mitigate shock exposure, while effective hedging and inventory management have smoothed cash flows. Margin cycles continue to dictate capex timing, with group capex guidance around €250–300m for the near term.

Gas and power market dynamics

Gas hub TTF averaging ~45 EUR/MWh in 2024 and rising power demand (+2% y/y in Greece 2024) directly tighten generation margins and retail competitiveness. Capacity mechanisms and RES penetration (~33% of Greek power in 2024) compress spark spreads, shifting economics toward flexible assets. High price volatility forces robust hedging, risk management and dynamic customer pricing. An integrated gas-power strategy smooths EBITDA swings and improves margin capture.

Interest rates, inflation, and capex intensity

Higher policy rates (ECB ~4.00% in mid-2025) lift WACC, making long-dated RES, hydrogen and CCS projects harder to finance and reducing net present value for HELPE’s transition pipeline.

Inflation (Eurozone ~2.5% in 2024) has pushed EPC and O&M costs higher, inflating project budgets and near-term operating expenses.

Prioritizing high-IRR, de-risked projects preserves balance-sheet resilience; tapping green finance (green bonds/EBRD/EIB) can materially lower funding costs and improve leverage metrics.

FX exposure and trade flows

Refining inputs like crude are dollar-priced while Hellenic Petroleum records sales in euros, exposing margins to EUR/USD moves; EUR/USD averaged about 1.09 in H1 2025, amplifying input cost volatility.

Regional exports/imports have shifted since 2022 due to sanctions and demand, with Mediterranean trade flows and freight rate swings altering route economics.

Active trade optimization and FX hedging programs, plus logistics flexibility (chartering and storage), help capture arbitrage and protect margins.

- EUR/USD ~1.09 (H1 2025)

- Sanctions-driven trade shifts since 2022

- Hedging + logistics = margin protection

Consumer demand and price elasticity

Fuel demand at Hellenic Petroleum remains tightly linked to macro growth and tourism seasonality—Greece recorded about 27.6 million tourist arrivals in 2023—while pump-price sensitivity drives short-term volume swings; gradual efficiency gains and EV uptake (global EV share of new passenger car sales ~14% in 2023 per IEA) trim volumes but support higher-margin premium products. Petrochemicals move with industrial and construction cycles, and expanded renewables and services reduce cyclical exposure.

- Demand sensitivity: macro growth + tourism

- Price elasticity: pump prices drive short-term volumes

- Structural trends: EVs (14% new car share 2023) and efficiency lower volumes

- Mix & resilience: premium products, petrochemicals track industry, renewables diversify

Align Greek energy with Fit for 55 and EU 42.5% 2030 renewables

Brent ~$86/bbl avg 2024; 3–2–1 crack swings $8–22/bbl drive earnings cyclicality. TTF ~45 EUR/MWh 2024; Greek power demand +2% y/y 2024; RES ~33%. ECB ~4.0% mid‑2025 raises WACC; Eurozone inflation ~2.5% 2024; EUR/USD ~1.09 H1 2025 impacts margins.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| TTF 2024 | €45/MWh |

| ECB rate | ~4.0% (mid‑2025) |

| EUR/USD H1 2025 | 1.09 |

Same Document Delivered

Hellenic Petroleum PESTLE Analysis

The preview shown here is the exact Hellenic Petroleum PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file contains the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—what you see is the final, downloadable document.