Hera PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

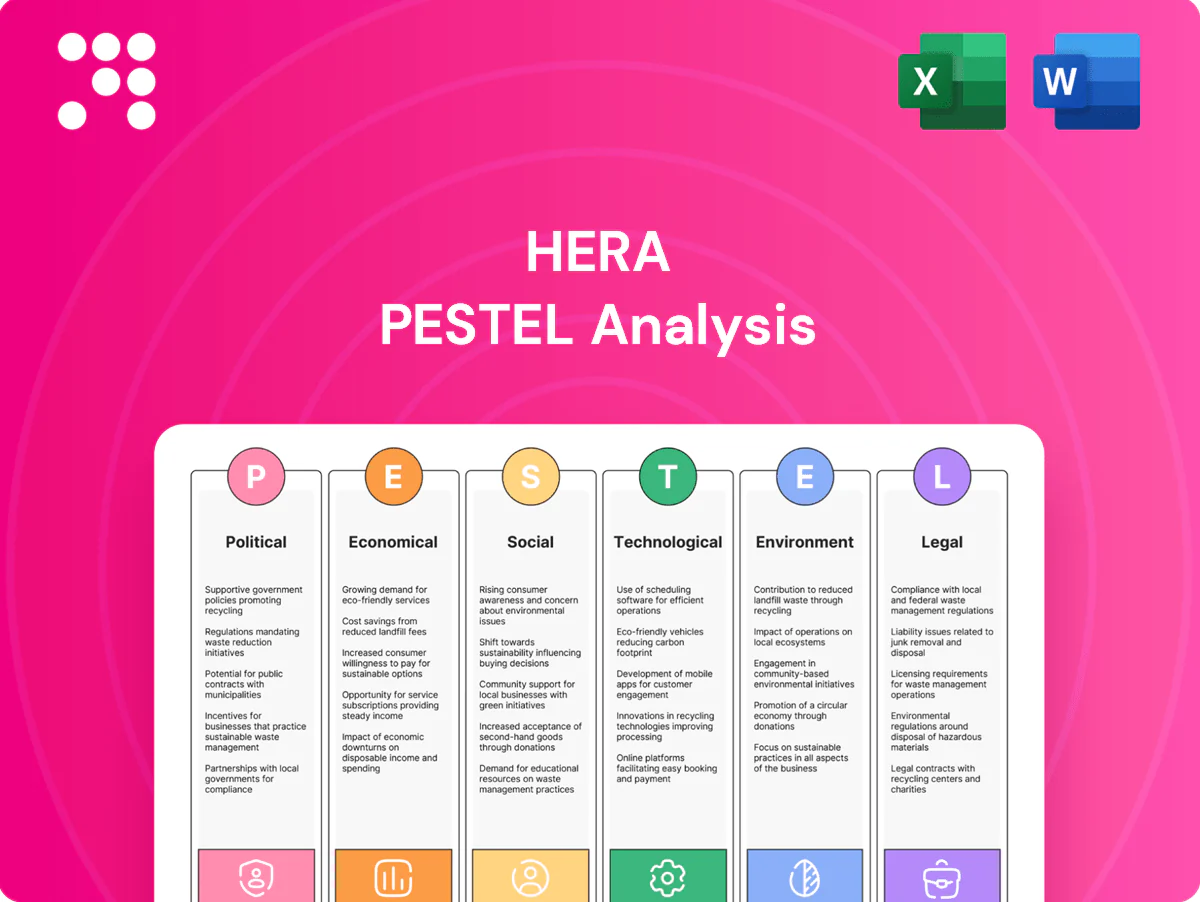

Unlock how political, economic, social, technological, legal and environmental forces are shaping Hera’s trajectory with our concise PESTLE snapshot—ideal for investors and strategists seeking actionable intelligence. Purchase the full PESTLE to access detailed, editable findings and immediate strategic recommendations.

Political factors

EU climate and energy policy

EU Fit for 55 (55% GHG cut by 2030) and REPowerEU (EU biomethane target 35 bcm by 2030) together with Italy’s PNIEC (2030 renewables ~30% target) push renewables, efficiency and grid upgrades that reshape Hera’s investment mix. Policy incentives prioritize biomethane, district heating decarbonization and electrification, while tighter targets and an EU ETS price around €90/tCO2 (2025) raise compliance costs but open subsidy windows. Policy stability is critical for Hera’s long‑lived utility assets.

National and local regulation

ARERA sets tariffs, service-quality standards and allowed returns across energy, water and waste, determining Hera’s revenue streams and pace of capex recovery; Hera serves c.4.5 million inhabitants, so tariff decisions scale materially. Municipal concessions for waste and water hinge on local politics and tender outcomes, affecting contract renewals and margins. Regional planning controls waste-to-energy siting and capacity; any ARERA or concession reset could rebase profitability.

Public procurement and concessions

Competitive tenders for distribution, collection and treatment define Hera’s operational territory and scale, with award criteria increasingly aligned to EU circular economy targets of 55% municipal waste recycling by 2025, 60% by 2030 and 65% by 2035. Long-term concessions, commonly 10–20 years, underpin predictable cash flows but embed strict performance obligations; renewal risk makes strong municipal and regulator relationships essential.

Energy security and diversification

Italy's post-2022 gas diversification toward LNG and pipeline volumes from Algeria and Azerbaijan reduces supply concentration for Hera's gas activities and can lower spot-driven price spikes; EU/Italy storage rules (90% target for winter fill implemented since 2023) increase system resilience but raise hedging and working-capital costs. Policy support for local renewable gas and WtE under the PNRR and regional incentives can cut import dependence, while tariff/subsidy shifts may quickly alter margin structures.

- Supply diversification: LNG, Algeria, Azerbaijan reduce concentration risk

- Storage mandate: 90% winter fill target increases hedging/flex costs

- Local supply: renewable gas and WtE supported by PNRR cut imports

- Policy risk: tariff/subsidy changes can materially change margins

Public acceptance and NIMBY

Waste-to-energy, anaerobic digestion and grid projects frequently face local NIMBY resistance that slows permitting; delays can jeopardize access to EU recovery and cohesion funds such as NextGenerationEU (€750bn) and the 2021–27 cohesion budget (€330bn).

- Community engagement reduces permit risk

- Benefit-sharing lowers opposition

- Delays threaten EU funding timelines

- Political capital required for strategic infrastructure

EU rules raise costs; biomethane 35 bcm, ETS ~€90/tCO2

EU Fit for 55/REPowerEU plus Italy PNIEC push renewables, biomethane 35 bcm by 2030 and tighter ETS (~€90/tCO2 in 2025), raising capex and compliance costs; ARERA tariffs and 10–20y municipal concessions drive revenue visibility for Hera (c.4.5m inhabitants); 90% storage mandate (from 2023) and LNG diversification lower supply risk but increase hedging/working-capital.

| Metric | Value |

|---|---|

| EU ETS (2025) | ~€90/tCO2 |

| Biomethane target | 35 bcm by 2030 |

| Hera served | 4.5m inhabitants |

| Storage rule | 90% winter fill (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Hera across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to reflect actual market and regulatory dynamics. Designed for executives and investors, it delivers forward-looking insights and clean, ready-to-use content for plans, decks, and scenario planning.

A concise, visually segmented PESTLE summary that highlights external risks and opportunities for quick reference in meetings or presentations. Editable notes per region or business line and an easily shareable format help align teams and support focused risk and market-positioning discussions.

Economic factors

Tariff frameworks and inflation

Indexation mechanisms in Hera’s regulated businesses partially shield revenues from inflation, as tariffs adjust with input price indices that tracked euro-area CPI moving from double digits in 2022 to about 2.7% in 2024 (Eurostat). Regulatory lag of several months can compress near-term margins before adjustments take effect. Rising rates — ECB policy around 4.25% in mid‑2025 — elevate WACC and capex hurdle rates, so operational efficiency gains are essential to sustain returns.

Energy price volatility

Wholesale electricity and gas swings have compressed Hera's supply margins and elevated customer churn during 2024-25, with European TTF gas monthly averages fluctuating between about 20–60 €/MWh in 2024, stressing merchant margins.

Capex intensity and funding

Grid digitalization, water resilience and circular-economy plants demand sustained capex for modernization and asset conversion, pressuring multi-utility spending plans. Access to EU programs such as NextGenerationEU (€806.9bn) and the green bond market helps lower financing costs and support projects. Capital allocation trade-offs between growth investment and dividends are pivotal, while execution discipline remains key to preserving credit metrics.

Macroeconomic growth and demand

Industrial activity is the main driver of commercial volumes for energy and waste; economic slowdowns cut industrial output and lower consumption and waste generation, directly reducing Hera’s variable revenues. Rising efficiency has flattened per‑capita energy use in many EU markets, while Italy’s population (~59.5 million) and ~69% urbanization shape service-density economics.

- Industrial output → commercial volumes

- Slowdowns reduce variable revenue

- Efficiency flattens per‑capita demand

- 59.5m population; ~69% urbanized → density effects

Input costs and supply chain

Equipment, chemical and construction cost inflation pressure Hera project budgets, with supply bottlenecks frequently delaying commissioning timelines and raising capex needs. Long-term procurement contracts and localization of key inputs have reduced exposure to spot-market volatility for utilities projects. Active vendor diversification and dual-sourcing strengthen resilience against regional disruptions.

- equipment cost exposure

- chemical input risk

- construction inflation

- long-term contracts

- localization

- vendor diversification

EU rules raise costs; biomethane 35 bcm, ETS ~€90/tCO2

Indexation cushions regulated revenues vs inflation (EU CPI ~2.7% in 2024) but regulatory lag compresses margins; ECB policy ~4.25% mid‑2025 raises WACC. Wholesale gas volatility (TTF 2024 ~20–60 €/MWh) and construction/chemical inflation pressure capex and margins, making EU funds and green financing (NextGenerationEU €806.9bn) key to lower financing costs.

| Metric | Value |

|---|---|

| Euro area CPI (2024) | ~2.7% |

| ECB policy rate (mid‑2025) | ~4.25% |

| TTF gas (2024 range) | €20–60/MWh |

| Italy population | 59.5m |

| NextGenerationEU | €806.9bn |

Full Version Awaits

Hera PESTLE Analysis

The preview shown here is the exact Hera PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with no placeholders. Download the final file immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political, economic, social, technological, legal and environmental forces are shaping Hera’s trajectory with our concise PESTLE snapshot—ideal for investors and strategists seeking actionable intelligence. Purchase the full PESTLE to access detailed, editable findings and immediate strategic recommendations.

Political factors

EU climate and energy policy

EU Fit for 55 (55% GHG cut by 2030) and REPowerEU (EU biomethane target 35 bcm by 2030) together with Italy’s PNIEC (2030 renewables ~30% target) push renewables, efficiency and grid upgrades that reshape Hera’s investment mix. Policy incentives prioritize biomethane, district heating decarbonization and electrification, while tighter targets and an EU ETS price around €90/tCO2 (2025) raise compliance costs but open subsidy windows. Policy stability is critical for Hera’s long‑lived utility assets.

National and local regulation

ARERA sets tariffs, service-quality standards and allowed returns across energy, water and waste, determining Hera’s revenue streams and pace of capex recovery; Hera serves c.4.5 million inhabitants, so tariff decisions scale materially. Municipal concessions for waste and water hinge on local politics and tender outcomes, affecting contract renewals and margins. Regional planning controls waste-to-energy siting and capacity; any ARERA or concession reset could rebase profitability.

Public procurement and concessions

Competitive tenders for distribution, collection and treatment define Hera’s operational territory and scale, with award criteria increasingly aligned to EU circular economy targets of 55% municipal waste recycling by 2025, 60% by 2030 and 65% by 2035. Long-term concessions, commonly 10–20 years, underpin predictable cash flows but embed strict performance obligations; renewal risk makes strong municipal and regulator relationships essential.

Energy security and diversification

Italy's post-2022 gas diversification toward LNG and pipeline volumes from Algeria and Azerbaijan reduces supply concentration for Hera's gas activities and can lower spot-driven price spikes; EU/Italy storage rules (90% target for winter fill implemented since 2023) increase system resilience but raise hedging and working-capital costs. Policy support for local renewable gas and WtE under the PNRR and regional incentives can cut import dependence, while tariff/subsidy shifts may quickly alter margin structures.

- Supply diversification: LNG, Algeria, Azerbaijan reduce concentration risk

- Storage mandate: 90% winter fill target increases hedging/flex costs

- Local supply: renewable gas and WtE supported by PNRR cut imports

- Policy risk: tariff/subsidy changes can materially change margins

Public acceptance and NIMBY

Waste-to-energy, anaerobic digestion and grid projects frequently face local NIMBY resistance that slows permitting; delays can jeopardize access to EU recovery and cohesion funds such as NextGenerationEU (€750bn) and the 2021–27 cohesion budget (€330bn).

- Community engagement reduces permit risk

- Benefit-sharing lowers opposition

- Delays threaten EU funding timelines

- Political capital required for strategic infrastructure

EU rules raise costs; biomethane 35 bcm, ETS ~€90/tCO2

EU Fit for 55/REPowerEU plus Italy PNIEC push renewables, biomethane 35 bcm by 2030 and tighter ETS (~€90/tCO2 in 2025), raising capex and compliance costs; ARERA tariffs and 10–20y municipal concessions drive revenue visibility for Hera (c.4.5m inhabitants); 90% storage mandate (from 2023) and LNG diversification lower supply risk but increase hedging/working-capital.

| Metric | Value |

|---|---|

| EU ETS (2025) | ~€90/tCO2 |

| Biomethane target | 35 bcm by 2030 |

| Hera served | 4.5m inhabitants |

| Storage rule | 90% winter fill (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Hera across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to reflect actual market and regulatory dynamics. Designed for executives and investors, it delivers forward-looking insights and clean, ready-to-use content for plans, decks, and scenario planning.

A concise, visually segmented PESTLE summary that highlights external risks and opportunities for quick reference in meetings or presentations. Editable notes per region or business line and an easily shareable format help align teams and support focused risk and market-positioning discussions.

Economic factors

Tariff frameworks and inflation

Indexation mechanisms in Hera’s regulated businesses partially shield revenues from inflation, as tariffs adjust with input price indices that tracked euro-area CPI moving from double digits in 2022 to about 2.7% in 2024 (Eurostat). Regulatory lag of several months can compress near-term margins before adjustments take effect. Rising rates — ECB policy around 4.25% in mid‑2025 — elevate WACC and capex hurdle rates, so operational efficiency gains are essential to sustain returns.

Energy price volatility

Wholesale electricity and gas swings have compressed Hera's supply margins and elevated customer churn during 2024-25, with European TTF gas monthly averages fluctuating between about 20–60 €/MWh in 2024, stressing merchant margins.

Capex intensity and funding

Grid digitalization, water resilience and circular-economy plants demand sustained capex for modernization and asset conversion, pressuring multi-utility spending plans. Access to EU programs such as NextGenerationEU (€806.9bn) and the green bond market helps lower financing costs and support projects. Capital allocation trade-offs between growth investment and dividends are pivotal, while execution discipline remains key to preserving credit metrics.

Macroeconomic growth and demand

Industrial activity is the main driver of commercial volumes for energy and waste; economic slowdowns cut industrial output and lower consumption and waste generation, directly reducing Hera’s variable revenues. Rising efficiency has flattened per‑capita energy use in many EU markets, while Italy’s population (~59.5 million) and ~69% urbanization shape service-density economics.

- Industrial output → commercial volumes

- Slowdowns reduce variable revenue

- Efficiency flattens per‑capita demand

- 59.5m population; ~69% urbanized → density effects

Input costs and supply chain

Equipment, chemical and construction cost inflation pressure Hera project budgets, with supply bottlenecks frequently delaying commissioning timelines and raising capex needs. Long-term procurement contracts and localization of key inputs have reduced exposure to spot-market volatility for utilities projects. Active vendor diversification and dual-sourcing strengthen resilience against regional disruptions.

- equipment cost exposure

- chemical input risk

- construction inflation

- long-term contracts

- localization

- vendor diversification

EU rules raise costs; biomethane 35 bcm, ETS ~€90/tCO2

Indexation cushions regulated revenues vs inflation (EU CPI ~2.7% in 2024) but regulatory lag compresses margins; ECB policy ~4.25% mid‑2025 raises WACC. Wholesale gas volatility (TTF 2024 ~20–60 €/MWh) and construction/chemical inflation pressure capex and margins, making EU funds and green financing (NextGenerationEU €806.9bn) key to lower financing costs.

| Metric | Value |

|---|---|

| Euro area CPI (2024) | ~2.7% |

| ECB policy rate (mid‑2025) | ~4.25% |

| TTF gas (2024 range) | €20–60/MWh |

| Italy population | 59.5m |

| NextGenerationEU | €806.9bn |

Full Version Awaits

Hera PESTLE Analysis

The preview shown here is the exact Hera PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with no placeholders. Download the final file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock how political, economic, social, technological, legal and environmental forces are shaping Hera’s trajectory with our concise PESTLE snapshot—ideal for investors and strategists seeking actionable intelligence. Purchase the full PESTLE to access detailed, editable findings and immediate strategic recommendations.

Political factors

EU climate and energy policy

EU Fit for 55 (55% GHG cut by 2030) and REPowerEU (EU biomethane target 35 bcm by 2030) together with Italy’s PNIEC (2030 renewables ~30% target) push renewables, efficiency and grid upgrades that reshape Hera’s investment mix. Policy incentives prioritize biomethane, district heating decarbonization and electrification, while tighter targets and an EU ETS price around €90/tCO2 (2025) raise compliance costs but open subsidy windows. Policy stability is critical for Hera’s long‑lived utility assets.

National and local regulation

ARERA sets tariffs, service-quality standards and allowed returns across energy, water and waste, determining Hera’s revenue streams and pace of capex recovery; Hera serves c.4.5 million inhabitants, so tariff decisions scale materially. Municipal concessions for waste and water hinge on local politics and tender outcomes, affecting contract renewals and margins. Regional planning controls waste-to-energy siting and capacity; any ARERA or concession reset could rebase profitability.

Public procurement and concessions

Competitive tenders for distribution, collection and treatment define Hera’s operational territory and scale, with award criteria increasingly aligned to EU circular economy targets of 55% municipal waste recycling by 2025, 60% by 2030 and 65% by 2035. Long-term concessions, commonly 10–20 years, underpin predictable cash flows but embed strict performance obligations; renewal risk makes strong municipal and regulator relationships essential.

Energy security and diversification

Italy's post-2022 gas diversification toward LNG and pipeline volumes from Algeria and Azerbaijan reduces supply concentration for Hera's gas activities and can lower spot-driven price spikes; EU/Italy storage rules (90% target for winter fill implemented since 2023) increase system resilience but raise hedging and working-capital costs. Policy support for local renewable gas and WtE under the PNRR and regional incentives can cut import dependence, while tariff/subsidy shifts may quickly alter margin structures.

- Supply diversification: LNG, Algeria, Azerbaijan reduce concentration risk

- Storage mandate: 90% winter fill target increases hedging/flex costs

- Local supply: renewable gas and WtE supported by PNRR cut imports

- Policy risk: tariff/subsidy changes can materially change margins

Public acceptance and NIMBY

Waste-to-energy, anaerobic digestion and grid projects frequently face local NIMBY resistance that slows permitting; delays can jeopardize access to EU recovery and cohesion funds such as NextGenerationEU (€750bn) and the 2021–27 cohesion budget (€330bn).

- Community engagement reduces permit risk

- Benefit-sharing lowers opposition

- Delays threaten EU funding timelines

- Political capital required for strategic infrastructure

EU rules raise costs; biomethane 35 bcm, ETS ~€90/tCO2

EU Fit for 55/REPowerEU plus Italy PNIEC push renewables, biomethane 35 bcm by 2030 and tighter ETS (~€90/tCO2 in 2025), raising capex and compliance costs; ARERA tariffs and 10–20y municipal concessions drive revenue visibility for Hera (c.4.5m inhabitants); 90% storage mandate (from 2023) and LNG diversification lower supply risk but increase hedging/working-capital.

| Metric | Value |

|---|---|

| EU ETS (2025) | ~€90/tCO2 |

| Biomethane target | 35 bcm by 2030 |

| Hera served | 4.5m inhabitants |

| Storage rule | 90% winter fill (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Hera across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to reflect actual market and regulatory dynamics. Designed for executives and investors, it delivers forward-looking insights and clean, ready-to-use content for plans, decks, and scenario planning.

A concise, visually segmented PESTLE summary that highlights external risks and opportunities for quick reference in meetings or presentations. Editable notes per region or business line and an easily shareable format help align teams and support focused risk and market-positioning discussions.

Economic factors

Tariff frameworks and inflation

Indexation mechanisms in Hera’s regulated businesses partially shield revenues from inflation, as tariffs adjust with input price indices that tracked euro-area CPI moving from double digits in 2022 to about 2.7% in 2024 (Eurostat). Regulatory lag of several months can compress near-term margins before adjustments take effect. Rising rates — ECB policy around 4.25% in mid‑2025 — elevate WACC and capex hurdle rates, so operational efficiency gains are essential to sustain returns.

Energy price volatility

Wholesale electricity and gas swings have compressed Hera's supply margins and elevated customer churn during 2024-25, with European TTF gas monthly averages fluctuating between about 20–60 €/MWh in 2024, stressing merchant margins.

Capex intensity and funding

Grid digitalization, water resilience and circular-economy plants demand sustained capex for modernization and asset conversion, pressuring multi-utility spending plans. Access to EU programs such as NextGenerationEU (€806.9bn) and the green bond market helps lower financing costs and support projects. Capital allocation trade-offs between growth investment and dividends are pivotal, while execution discipline remains key to preserving credit metrics.

Macroeconomic growth and demand

Industrial activity is the main driver of commercial volumes for energy and waste; economic slowdowns cut industrial output and lower consumption and waste generation, directly reducing Hera’s variable revenues. Rising efficiency has flattened per‑capita energy use in many EU markets, while Italy’s population (~59.5 million) and ~69% urbanization shape service-density economics.

- Industrial output → commercial volumes

- Slowdowns reduce variable revenue

- Efficiency flattens per‑capita demand

- 59.5m population; ~69% urbanized → density effects

Input costs and supply chain

Equipment, chemical and construction cost inflation pressure Hera project budgets, with supply bottlenecks frequently delaying commissioning timelines and raising capex needs. Long-term procurement contracts and localization of key inputs have reduced exposure to spot-market volatility for utilities projects. Active vendor diversification and dual-sourcing strengthen resilience against regional disruptions.

- equipment cost exposure

- chemical input risk

- construction inflation

- long-term contracts

- localization

- vendor diversification

EU rules raise costs; biomethane 35 bcm, ETS ~€90/tCO2

Indexation cushions regulated revenues vs inflation (EU CPI ~2.7% in 2024) but regulatory lag compresses margins; ECB policy ~4.25% mid‑2025 raises WACC. Wholesale gas volatility (TTF 2024 ~20–60 €/MWh) and construction/chemical inflation pressure capex and margins, making EU funds and green financing (NextGenerationEU €806.9bn) key to lower financing costs.

| Metric | Value |

|---|---|

| Euro area CPI (2024) | ~2.7% |

| ECB policy rate (mid‑2025) | ~4.25% |

| TTF gas (2024 range) | €20–60/MWh |

| Italy population | 59.5m |

| NextGenerationEU | €806.9bn |

Full Version Awaits

Hera PESTLE Analysis

The preview shown here is the exact Hera PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment with no placeholders. Download the final file immediately after checkout.