Hexagon Porter's Five Forces Analysis

From Overview to Strategy Blueprint

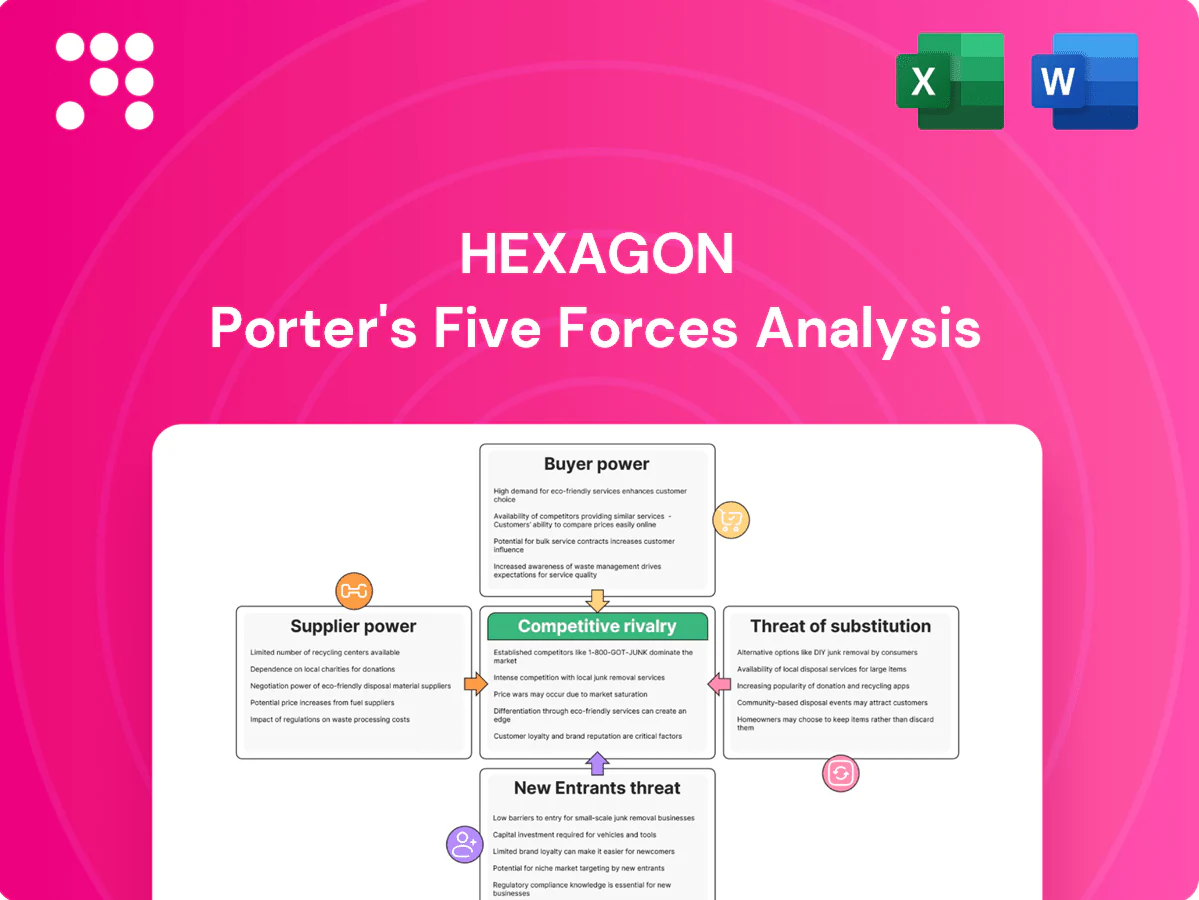

Hexagon’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of entrants, and substitutes shaping its tech-driven market position. This concise overview surfaces key pressures and strategic levers for Hexagon leadership and investors. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized sensor components

Hexagon depends on specialized optics, LiDAR, GNSS and edge compute chipsets from a concentrated supplier base, giving suppliers meaningful leverage; qualification cycles and component uniqueness raise switching costs and integration timeframes. In 2024 supply constraints pushed lead times for key sensors to multiple months, pressuring delivery schedules and margin management. Dual-sourcing and modular design partially mitigate supplier power.

Cloud and compute dependencies

Hyperscaler platforms provide hosting, AI/ML and data pipelines critical to digital twins. Market concentration (AWS ~32%, Azure ~23%, GCP ~11% in 2024) amplifies supplier power. Platform stickiness and egress fees (commonly $0.05–0.12/GB) mean pricing shifts or deprecations can hit margins and performance. Hybrid architectures reduce exposure but often increase ops complexity and costs by up to ~20%.

Geospatial and map data inputs

As of 2024 Maxar, Planet and Airbus dominate high-resolution satellite imagery and curated base-map supply, concentrating bargaining power. Restrictive licensing, usage caps and exclusivities shift leverage to these suppliers and can raise costs. Hexagon’s in-house capture via Leica Geosystems and sensors mitigates dependency but cannot replace all third-party inputs. Long-term supplier contracts and volume agreements help stabilize pricing and access.

Firmware, IP, and standards

Embedded firmware, codecs, and standards-compliant modules for Hexagon often carry royalty obligations and licensing terms that increase supplier leverage, while compliance with industry norms like OGC narrows alternative supplier options.

- IP-heavy components increase supplier bargaining power

- Standards compliance limits supplier choice

- Cross-licensing and in-house IP reduce dependence

Switching and qualification costs

Validating alternative parts for industrial reliability typically requires 6–12 months of testing and field trials in 2024, and the potential for even small field failure rates (industry targets often below 0.1%) deters rapid supplier changes, which strengthens supplier power in the short term. Strategic inventory, vendor take-apart agreements (VTAs), and co-development contracts help rebalance negotiating positions by shortening qualification lead times and sharing risk.

- Validation time: 6–12 months

- Field reliability benchmark: <0.1% failure target

- Mitigants: safety stock, VTAs, co-development agreements

Concentrated sensors, hyperscaler egress fees and 6–12 month validation force dual-sourcing

Hexagon relies on specialized optics, LiDAR, GNSS and edge chipsets from concentrated suppliers, creating leverage and multi-month lead times in 2024. Hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024) add platform power and egress costs ($0.05–0.12/GB). Validation for alternatives takes 6–12 months and field-failure targets <0.1%, so safety stock, dual-sourcing and co-dev mitigate risk.

| Metric | 2024 |

|---|---|

| AWS/Azure/GCP | 32%/23%/11% |

| Egress cost | $0.05–0.12/GB |

| Validation time | 6–12 months |

| Failure target | <0.1% |

What is included in the product

Concise Porter's Five Forces assessment of Hexagon, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive technologies and market dynamics that influence its pricing, margins, and strategic positioning.

A compact Hexagon Porter's Five Forces one-sheet that visualizes competitive pressure across all forces in an intuitive hexagon layout—ideal for rapid strategic decisions and slide-ready summaries.

Customers Bargaining Power

Enterprise and public-sector buyers

Large manufacturers, AEC firms and governments buy at scale via RFPs, with contracts commonly exceeding $1M and procurement cycles of 6–18 months. Volume and compliance needs drive price pressure and bespoke terms, often yielding double-digit discounts. Mission-critical use cases favor proven vendors, where referenceability and lifecycle support can command 10–20% pricing premium and lower churn.

Integration and switching costs

Hexagon solutions tightly integrate with PLM, CAD, ERP and OT systems, embedding data schemas, workflows and training that create high switching costs and materially temper buyer power once deployed. Open APIs in 2024 can modestly reduce lock-in by enabling selective data exchange, but they rarely eliminate migration complexity or retraining needs. Customers face substantive operational inertia despite API availability.

Outcome-based value focus

In 2024 customers evaluate Hexagon primarily on productivity, quality, and total cost of ownership rather than upfront price. Demonstrable ROI from pilot projects and case studies reduces price sensitivity and shortens procurement cycles. Bundled hardware-software-service offerings increase switching costs and stickiness. Value-based pricing lets Hexagon capture surplus in high-impact use cases where measured outcomes justify premium fees.

Vendor consolidation trends

Vendor consolidation in 2024 sees enterprises prioritizing fewer strategic platforms across sites and regions, with surveys indicating roughly 56% of large organizations actively reducing supplier counts to streamline procurement and compliance; consolidation strengthens buyers in master-agreement negotiations but raises the bar for vendors on global support and platform breadth; Hexagon’s broad portfolio and global footprint position it to capture platform mandates.

- Consolidation rate: ~56% (2024)

- Negotiation leverage: stronger for buyers

- Vendor win-criteria: global support, portfolio breadth

- Hexagon advantage: breadth and global presence

Interoperability expectations

Buyers increasingly demand open formats and standards compliance, raising comparability among vendors and strengthening customer leverage; certification and ecosystem connectors are now table stakes while Hexagon’s superior performance and domain expertise remain key differentiation; OGC membership exceeded 500 organizations in 2024, reflecting market-wide standards pressure.

- open-formats: increases buyer leverage

- certification/connectors: table stakes

- performance+domain expertise: sustain premium pricing

- OGC-membership-2024: >500

Procurement squeezes prices; mission-critical deals fetch 10-20% premiums

Large buyers (RFPs >$1M; procurement 6–18 months) exert price pressure securing double-digit discounts, yet mission-critical deals let Hexagon capture 10–20% premiums and reduce churn. Deep PLM/CAD/ERP integration raises switching costs despite 2024 open APIs and rising standards pressure (OGC >500). Supplier consolidation (56% cutting vendors) strengthens buyer leverage on terms.

| Metric | Value |

|---|---|

| Supplier consolidation | 56% |

| OGC membership (2024) | >500 |

| Procurement cycle | 6–18 months |

| Typical contract size | >$1M |

| Vendor price premium | 10–20% |

Same Document Delivered

Hexagon Porter's Five Forces Analysis

This preview shows the exact Hexagon Porter's Five Forces analysis you'll receive upon purchase—no placeholders or samples. The file is the complete, professionally formatted deliverable and will be available for immediate download after payment. Use it as-is for reporting or decision-making.

From Overview to Strategy Blueprint

Hexagon’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of entrants, and substitutes shaping its tech-driven market position. This concise overview surfaces key pressures and strategic levers for Hexagon leadership and investors. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized sensor components

Hexagon depends on specialized optics, LiDAR, GNSS and edge compute chipsets from a concentrated supplier base, giving suppliers meaningful leverage; qualification cycles and component uniqueness raise switching costs and integration timeframes. In 2024 supply constraints pushed lead times for key sensors to multiple months, pressuring delivery schedules and margin management. Dual-sourcing and modular design partially mitigate supplier power.

Cloud and compute dependencies

Hyperscaler platforms provide hosting, AI/ML and data pipelines critical to digital twins. Market concentration (AWS ~32%, Azure ~23%, GCP ~11% in 2024) amplifies supplier power. Platform stickiness and egress fees (commonly $0.05–0.12/GB) mean pricing shifts or deprecations can hit margins and performance. Hybrid architectures reduce exposure but often increase ops complexity and costs by up to ~20%.

Geospatial and map data inputs

As of 2024 Maxar, Planet and Airbus dominate high-resolution satellite imagery and curated base-map supply, concentrating bargaining power. Restrictive licensing, usage caps and exclusivities shift leverage to these suppliers and can raise costs. Hexagon’s in-house capture via Leica Geosystems and sensors mitigates dependency but cannot replace all third-party inputs. Long-term supplier contracts and volume agreements help stabilize pricing and access.

Firmware, IP, and standards

Embedded firmware, codecs, and standards-compliant modules for Hexagon often carry royalty obligations and licensing terms that increase supplier leverage, while compliance with industry norms like OGC narrows alternative supplier options.

- IP-heavy components increase supplier bargaining power

- Standards compliance limits supplier choice

- Cross-licensing and in-house IP reduce dependence

Switching and qualification costs

Validating alternative parts for industrial reliability typically requires 6–12 months of testing and field trials in 2024, and the potential for even small field failure rates (industry targets often below 0.1%) deters rapid supplier changes, which strengthens supplier power in the short term. Strategic inventory, vendor take-apart agreements (VTAs), and co-development contracts help rebalance negotiating positions by shortening qualification lead times and sharing risk.

- Validation time: 6–12 months

- Field reliability benchmark: <0.1% failure target

- Mitigants: safety stock, VTAs, co-development agreements

Concentrated sensors, hyperscaler egress fees and 6–12 month validation force dual-sourcing

Hexagon relies on specialized optics, LiDAR, GNSS and edge chipsets from concentrated suppliers, creating leverage and multi-month lead times in 2024. Hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024) add platform power and egress costs ($0.05–0.12/GB). Validation for alternatives takes 6–12 months and field-failure targets <0.1%, so safety stock, dual-sourcing and co-dev mitigate risk.

| Metric | 2024 |

|---|---|

| AWS/Azure/GCP | 32%/23%/11% |

| Egress cost | $0.05–0.12/GB |

| Validation time | 6–12 months |

| Failure target | <0.1% |

What is included in the product

Concise Porter's Five Forces assessment of Hexagon, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive technologies and market dynamics that influence its pricing, margins, and strategic positioning.

A compact Hexagon Porter's Five Forces one-sheet that visualizes competitive pressure across all forces in an intuitive hexagon layout—ideal for rapid strategic decisions and slide-ready summaries.

Customers Bargaining Power

Enterprise and public-sector buyers

Large manufacturers, AEC firms and governments buy at scale via RFPs, with contracts commonly exceeding $1M and procurement cycles of 6–18 months. Volume and compliance needs drive price pressure and bespoke terms, often yielding double-digit discounts. Mission-critical use cases favor proven vendors, where referenceability and lifecycle support can command 10–20% pricing premium and lower churn.

Integration and switching costs

Hexagon solutions tightly integrate with PLM, CAD, ERP and OT systems, embedding data schemas, workflows and training that create high switching costs and materially temper buyer power once deployed. Open APIs in 2024 can modestly reduce lock-in by enabling selective data exchange, but they rarely eliminate migration complexity or retraining needs. Customers face substantive operational inertia despite API availability.

Outcome-based value focus

In 2024 customers evaluate Hexagon primarily on productivity, quality, and total cost of ownership rather than upfront price. Demonstrable ROI from pilot projects and case studies reduces price sensitivity and shortens procurement cycles. Bundled hardware-software-service offerings increase switching costs and stickiness. Value-based pricing lets Hexagon capture surplus in high-impact use cases where measured outcomes justify premium fees.

Vendor consolidation trends

Vendor consolidation in 2024 sees enterprises prioritizing fewer strategic platforms across sites and regions, with surveys indicating roughly 56% of large organizations actively reducing supplier counts to streamline procurement and compliance; consolidation strengthens buyers in master-agreement negotiations but raises the bar for vendors on global support and platform breadth; Hexagon’s broad portfolio and global footprint position it to capture platform mandates.

- Consolidation rate: ~56% (2024)

- Negotiation leverage: stronger for buyers

- Vendor win-criteria: global support, portfolio breadth

- Hexagon advantage: breadth and global presence

Interoperability expectations

Buyers increasingly demand open formats and standards compliance, raising comparability among vendors and strengthening customer leverage; certification and ecosystem connectors are now table stakes while Hexagon’s superior performance and domain expertise remain key differentiation; OGC membership exceeded 500 organizations in 2024, reflecting market-wide standards pressure.

- open-formats: increases buyer leverage

- certification/connectors: table stakes

- performance+domain expertise: sustain premium pricing

- OGC-membership-2024: >500

Procurement squeezes prices; mission-critical deals fetch 10-20% premiums

Large buyers (RFPs >$1M; procurement 6–18 months) exert price pressure securing double-digit discounts, yet mission-critical deals let Hexagon capture 10–20% premiums and reduce churn. Deep PLM/CAD/ERP integration raises switching costs despite 2024 open APIs and rising standards pressure (OGC >500). Supplier consolidation (56% cutting vendors) strengthens buyer leverage on terms.

| Metric | Value |

|---|---|

| Supplier consolidation | 56% |

| OGC membership (2024) | >500 |

| Procurement cycle | 6–18 months |

| Typical contract size | >$1M |

| Vendor price premium | 10–20% |

Same Document Delivered

Hexagon Porter's Five Forces Analysis

This preview shows the exact Hexagon Porter's Five Forces analysis you'll receive upon purchase—no placeholders or samples. The file is the complete, professionally formatted deliverable and will be available for immediate download after payment. Use it as-is for reporting or decision-making.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Hexagon’s Porter's Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of entrants, and substitutes shaping its tech-driven market position. This concise overview surfaces key pressures and strategic levers for Hexagon leadership and investors. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Specialized sensor components

Hexagon depends on specialized optics, LiDAR, GNSS and edge compute chipsets from a concentrated supplier base, giving suppliers meaningful leverage; qualification cycles and component uniqueness raise switching costs and integration timeframes. In 2024 supply constraints pushed lead times for key sensors to multiple months, pressuring delivery schedules and margin management. Dual-sourcing and modular design partially mitigate supplier power.

Cloud and compute dependencies

Hyperscaler platforms provide hosting, AI/ML and data pipelines critical to digital twins. Market concentration (AWS ~32%, Azure ~23%, GCP ~11% in 2024) amplifies supplier power. Platform stickiness and egress fees (commonly $0.05–0.12/GB) mean pricing shifts or deprecations can hit margins and performance. Hybrid architectures reduce exposure but often increase ops complexity and costs by up to ~20%.

Geospatial and map data inputs

As of 2024 Maxar, Planet and Airbus dominate high-resolution satellite imagery and curated base-map supply, concentrating bargaining power. Restrictive licensing, usage caps and exclusivities shift leverage to these suppliers and can raise costs. Hexagon’s in-house capture via Leica Geosystems and sensors mitigates dependency but cannot replace all third-party inputs. Long-term supplier contracts and volume agreements help stabilize pricing and access.

Firmware, IP, and standards

Embedded firmware, codecs, and standards-compliant modules for Hexagon often carry royalty obligations and licensing terms that increase supplier leverage, while compliance with industry norms like OGC narrows alternative supplier options.

- IP-heavy components increase supplier bargaining power

- Standards compliance limits supplier choice

- Cross-licensing and in-house IP reduce dependence

Switching and qualification costs

Validating alternative parts for industrial reliability typically requires 6–12 months of testing and field trials in 2024, and the potential for even small field failure rates (industry targets often below 0.1%) deters rapid supplier changes, which strengthens supplier power in the short term. Strategic inventory, vendor take-apart agreements (VTAs), and co-development contracts help rebalance negotiating positions by shortening qualification lead times and sharing risk.

- Validation time: 6–12 months

- Field reliability benchmark: <0.1% failure target

- Mitigants: safety stock, VTAs, co-development agreements

Concentrated sensors, hyperscaler egress fees and 6–12 month validation force dual-sourcing

Hexagon relies on specialized optics, LiDAR, GNSS and edge chipsets from concentrated suppliers, creating leverage and multi-month lead times in 2024. Hyperscalers (AWS 32%, Azure 23%, GCP 11% in 2024) add platform power and egress costs ($0.05–0.12/GB). Validation for alternatives takes 6–12 months and field-failure targets <0.1%, so safety stock, dual-sourcing and co-dev mitigate risk.

| Metric | 2024 |

|---|---|

| AWS/Azure/GCP | 32%/23%/11% |

| Egress cost | $0.05–0.12/GB |

| Validation time | 6–12 months |

| Failure target | <0.1% |

What is included in the product

Concise Porter's Five Forces assessment of Hexagon, detailing competitive rivalry, buyer and supplier power, threat of substitutes and new entrants, and highlighting disruptive technologies and market dynamics that influence its pricing, margins, and strategic positioning.

A compact Hexagon Porter's Five Forces one-sheet that visualizes competitive pressure across all forces in an intuitive hexagon layout—ideal for rapid strategic decisions and slide-ready summaries.

Customers Bargaining Power

Enterprise and public-sector buyers

Large manufacturers, AEC firms and governments buy at scale via RFPs, with contracts commonly exceeding $1M and procurement cycles of 6–18 months. Volume and compliance needs drive price pressure and bespoke terms, often yielding double-digit discounts. Mission-critical use cases favor proven vendors, where referenceability and lifecycle support can command 10–20% pricing premium and lower churn.

Integration and switching costs

Hexagon solutions tightly integrate with PLM, CAD, ERP and OT systems, embedding data schemas, workflows and training that create high switching costs and materially temper buyer power once deployed. Open APIs in 2024 can modestly reduce lock-in by enabling selective data exchange, but they rarely eliminate migration complexity or retraining needs. Customers face substantive operational inertia despite API availability.

Outcome-based value focus

In 2024 customers evaluate Hexagon primarily on productivity, quality, and total cost of ownership rather than upfront price. Demonstrable ROI from pilot projects and case studies reduces price sensitivity and shortens procurement cycles. Bundled hardware-software-service offerings increase switching costs and stickiness. Value-based pricing lets Hexagon capture surplus in high-impact use cases where measured outcomes justify premium fees.

Vendor consolidation trends

Vendor consolidation in 2024 sees enterprises prioritizing fewer strategic platforms across sites and regions, with surveys indicating roughly 56% of large organizations actively reducing supplier counts to streamline procurement and compliance; consolidation strengthens buyers in master-agreement negotiations but raises the bar for vendors on global support and platform breadth; Hexagon’s broad portfolio and global footprint position it to capture platform mandates.

- Consolidation rate: ~56% (2024)

- Negotiation leverage: stronger for buyers

- Vendor win-criteria: global support, portfolio breadth

- Hexagon advantage: breadth and global presence

Interoperability expectations

Buyers increasingly demand open formats and standards compliance, raising comparability among vendors and strengthening customer leverage; certification and ecosystem connectors are now table stakes while Hexagon’s superior performance and domain expertise remain key differentiation; OGC membership exceeded 500 organizations in 2024, reflecting market-wide standards pressure.

- open-formats: increases buyer leverage

- certification/connectors: table stakes

- performance+domain expertise: sustain premium pricing

- OGC-membership-2024: >500

Procurement squeezes prices; mission-critical deals fetch 10-20% premiums

Large buyers (RFPs >$1M; procurement 6–18 months) exert price pressure securing double-digit discounts, yet mission-critical deals let Hexagon capture 10–20% premiums and reduce churn. Deep PLM/CAD/ERP integration raises switching costs despite 2024 open APIs and rising standards pressure (OGC >500). Supplier consolidation (56% cutting vendors) strengthens buyer leverage on terms.

| Metric | Value |

|---|---|

| Supplier consolidation | 56% |

| OGC membership (2024) | >500 |

| Procurement cycle | 6–18 months |

| Typical contract size | >$1M |

| Vendor price premium | 10–20% |

Same Document Delivered

Hexagon Porter's Five Forces Analysis

This preview shows the exact Hexagon Porter's Five Forces analysis you'll receive upon purchase—no placeholders or samples. The file is the complete, professionally formatted deliverable and will be available for immediate download after payment. Use it as-is for reporting or decision-making.