Hexcel Porter's Five Forces Analysis

From Overview to Strategy Blueprint

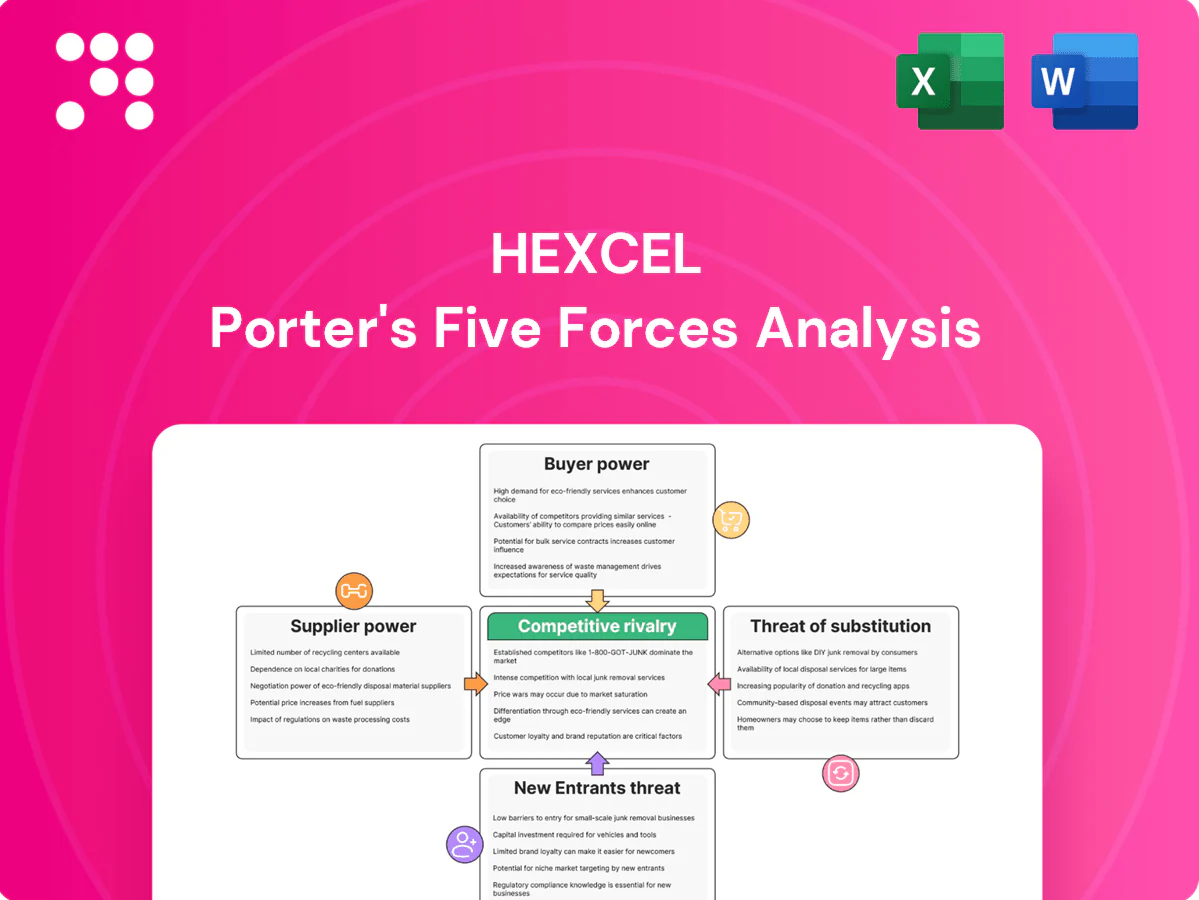

Hexcel faces moderate supplier power due to specialized composite materials, intense rivalry from aerospace composites peers, and a manageable threat of new entrants given high capital and tech barriers. Buyers wield bargaining power through large OEM contracts, while substitutes remain limited. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hexcel’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Hexcel depends on a limited set of suppliers for PAN precursor, specialty resins and aerospace-grade fibers, a point highlighted in its 2024 Form 10-K. Supplier concentration elevates switching costs and dependency risk; disruptions can delay production and compress margins. Long-term contracts mitigate but preserve supplier leverage.

Specialty chemicals and qualification

Resins, tougheners and aerospace adhesives must meet stringent program specs and are qualified per program, narrowing approved vendor lists to often 3–5 suppliers and limiting Hexcel’s ability to dual‑source quickly. Suppliers with unique chemistries command pricing and delivery leverage, and requalification timelines—commonly 12–24 months—further entrench supplier power, raising switching costs and lead‑time risk.

Capital-intensive equipment and utilities

Carbonization lines, autoclaves, and high-capacity energy systems are mission-critical and costly to modify, giving suppliers of specialized OEM equipment significant leverage over Hexcel’s timelines and contract terms. Limited global OEMs for these machines concentrate bargaining power and can extend multi-month lead times. Hexcel’s electricity- and gas-intensive processes leave it exposed to utility price swings, and while energy hedging reduces some risk, it only partially offsets supplier pricing power.

Geopolitical and trade exposure

Cross-border sourcing of acrylonitrile, fibers and specialty chemicals exposes Hexcel to tariffs, export controls and logistics bottlenecks; suppliers in tightly regulated regions commonly pass through compliance costs, and currency swings can strengthen supplier bargaining positions. Diversification of sources mitigates but does not eliminate this exposure.

- Tariffs and export controls

- Compliance cost pass-through

- Currency-driven supplier leverage

- Diversification reduces but not removes risk

Countervailing power via scale

Hexcel’s global scale and multi-year aerospace demand visibility give it leverage: the company reported approximately $2.6 billion in net sales in 2024 and sustained a multi-year commercial aircraft backlog, enabling volume commitments that blunt supplier pricing power. Joint development deals and vendor-managed inventory programs reduce stockouts and align incentives, but highly bespoke resin and prepreg formulations plus tight aerospace specifications limit standardization gains. Overall supplier power is moderate.

- Scale: Hexcel 2024 net sales ~ $2.6B

- Demand visibility: multi-year commercial backlog

- Supply mitigation: JVs and VMI reduce disruption

- Constraint: bespoke specs cap supplier substitutability

- Net: moderate supplier bargaining power

Supplier leverage: 12–24 month requal. vs $2.6B 2024 sales

Hexcel faces moderate supplier power: concentrated providers of PAN precursor, specialty resins and aerospace fibers (approved vendors often 3–5) and 12–24 month requalification timelines raise switching costs, while 2024 net sales ~$2.6B and multi-year aircraft backlog provide volume leverage; JVs/VMI mitigate but bespoke specs sustain supplier influence.

| Metric | Value |

|---|---|

| 2024 Net Sales | $2.6B |

| Approved suppliers | 3–5 |

| Requalification | 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis of Hexcel that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary on pricing, profitability and market dynamics to inform investor, executive, and academic use.

A concise one-sheet Porter's Five Forces for Hexcel that visualizes competitive pressure with an editable spider chart, lets you toggle scenarios (pre/post regulation, new entrant), and delivers a clean, copy-ready layout for decks—no macros, easy for non-finance users.

Customers Bargaining Power

Highly concentrated OEM base

Airbus, Boeing and major engine/defense primes drove the bulk of airframe and aero-structures demand in 2024, concentrating purchasing power and giving program-timing and delivery schedules outsized negotiating leverage.

Buyers’ dual-sourcing strategies and long lead contracts further compress pricing and tighten commercial terms across supply tiers.

Hexcel counters through demonstrated in-service performance, long qualification cycles and high switching costs that preserve margin and program stickiness.

Long qualification and switching costs

Once a composite material is on a program, change triggers lengthy requalification—industry requalification cycles typically run 6–18 months and can cost $1–5 million—creating embedded switching costs that moderate buyer power post-award. Pre-award buyers exploit competitive bids to extract concessions, but post-award leverage shifts to Hexcel due to continuity, certified supply chains and program risk.

Price-down expectations over program life

Aerospace OEMs in 2024 continued to insist on learning-curve price reductions and productivity give-backs built into multi-year agreements, pressuring Hexcel to meet embedded cost-down trajectories. Hexcel must deliver measurable yield and throughput gains to preserve margins as contracts expect progressive unit-cost declines. Failure to achieve these improvements risks losing future platform volumes to lower-cost rivals.

Demand cyclicality and inventory policies

Demand cyclicality—Boeing targeting ~38 737s/month in 2024 and US FY2024 defense discretionary spending near 858 billion USD—shifts Hexcel order momentum; buyers flex schedules, reducing capacity utilization and strengthening bargaining power. Vendor-managed inventory programs can smooth supply but shift holding costs to Hexcel. In downturns volatility amplifies buyer influence, compressing pricing and lead times.

- Buyers flex schedules → lower utilization

- 38/mo Boeing target (2024) → order volatility

- US defense budget ~858B (FY2024) → program shifts

- VMI transfers inventory burden to Hexcel

Specification control and design authority

Customers set material specs and performance envelopes, directing procurement choices and enabling trials of competitive alternates; co-development raises switching costs but transfers IP benefits. Buyer power stays high to moderate across program phases, strongest at qualification and pricing rounds and easing after qualification into production. In 2024 the global aerospace composites market exceeded 20 billion USD, reinforcing OEM leverage.

- Customer design authority → procurement control

- Co-development → partial lock-in + shared IP

- Program phase-sensitive buyer power

- 2024 market size >20 billion USD

Concentrated OEM demand and dual-sourcing squeeze pre-award pricing; switching costs protect margins

Buyers concentrated (Airbus/Boeing/primes) and dual-sourcing compress pricing pre-award, while Hexcel's in-service performance, long requalification (6–18 months, $1–5M) and switching costs protect post-award margins. OEMs demand learning-curve cost reductions; Boeing 38/mo (2024) and US defense ~$858B (FY2024) drive order volatility. 2024 aerospace composites market >$20B; VMI shifts inventory risk to Hexcel.

| Metric | 2024 value |

|---|---|

| Boeing production target | ~38/mo |

| US defense budget | ~$858B (FY2024) |

| Composites market | >$20B |

| Requalification | 6–18 months; $1–5M |

Preview the Actual Deliverable

Hexcel Porter's Five Forces Analysis

This preview shows the exact Hexcel Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The full, professionally formatted document is ready for download and use the moment you buy. You're viewing the final deliverable in its entirety.

From Overview to Strategy Blueprint

Hexcel faces moderate supplier power due to specialized composite materials, intense rivalry from aerospace composites peers, and a manageable threat of new entrants given high capital and tech barriers. Buyers wield bargaining power through large OEM contracts, while substitutes remain limited. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hexcel’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Hexcel depends on a limited set of suppliers for PAN precursor, specialty resins and aerospace-grade fibers, a point highlighted in its 2024 Form 10-K. Supplier concentration elevates switching costs and dependency risk; disruptions can delay production and compress margins. Long-term contracts mitigate but preserve supplier leverage.

Specialty chemicals and qualification

Resins, tougheners and aerospace adhesives must meet stringent program specs and are qualified per program, narrowing approved vendor lists to often 3–5 suppliers and limiting Hexcel’s ability to dual‑source quickly. Suppliers with unique chemistries command pricing and delivery leverage, and requalification timelines—commonly 12–24 months—further entrench supplier power, raising switching costs and lead‑time risk.

Capital-intensive equipment and utilities

Carbonization lines, autoclaves, and high-capacity energy systems are mission-critical and costly to modify, giving suppliers of specialized OEM equipment significant leverage over Hexcel’s timelines and contract terms. Limited global OEMs for these machines concentrate bargaining power and can extend multi-month lead times. Hexcel’s electricity- and gas-intensive processes leave it exposed to utility price swings, and while energy hedging reduces some risk, it only partially offsets supplier pricing power.

Geopolitical and trade exposure

Cross-border sourcing of acrylonitrile, fibers and specialty chemicals exposes Hexcel to tariffs, export controls and logistics bottlenecks; suppliers in tightly regulated regions commonly pass through compliance costs, and currency swings can strengthen supplier bargaining positions. Diversification of sources mitigates but does not eliminate this exposure.

- Tariffs and export controls

- Compliance cost pass-through

- Currency-driven supplier leverage

- Diversification reduces but not removes risk

Countervailing power via scale

Hexcel’s global scale and multi-year aerospace demand visibility give it leverage: the company reported approximately $2.6 billion in net sales in 2024 and sustained a multi-year commercial aircraft backlog, enabling volume commitments that blunt supplier pricing power. Joint development deals and vendor-managed inventory programs reduce stockouts and align incentives, but highly bespoke resin and prepreg formulations plus tight aerospace specifications limit standardization gains. Overall supplier power is moderate.

- Scale: Hexcel 2024 net sales ~ $2.6B

- Demand visibility: multi-year commercial backlog

- Supply mitigation: JVs and VMI reduce disruption

- Constraint: bespoke specs cap supplier substitutability

- Net: moderate supplier bargaining power

Supplier leverage: 12–24 month requal. vs $2.6B 2024 sales

Hexcel faces moderate supplier power: concentrated providers of PAN precursor, specialty resins and aerospace fibers (approved vendors often 3–5) and 12–24 month requalification timelines raise switching costs, while 2024 net sales ~$2.6B and multi-year aircraft backlog provide volume leverage; JVs/VMI mitigate but bespoke specs sustain supplier influence.

| Metric | Value |

|---|---|

| 2024 Net Sales | $2.6B |

| Approved suppliers | 3–5 |

| Requalification | 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis of Hexcel that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary on pricing, profitability and market dynamics to inform investor, executive, and academic use.

A concise one-sheet Porter's Five Forces for Hexcel that visualizes competitive pressure with an editable spider chart, lets you toggle scenarios (pre/post regulation, new entrant), and delivers a clean, copy-ready layout for decks—no macros, easy for non-finance users.

Customers Bargaining Power

Highly concentrated OEM base

Airbus, Boeing and major engine/defense primes drove the bulk of airframe and aero-structures demand in 2024, concentrating purchasing power and giving program-timing and delivery schedules outsized negotiating leverage.

Buyers’ dual-sourcing strategies and long lead contracts further compress pricing and tighten commercial terms across supply tiers.

Hexcel counters through demonstrated in-service performance, long qualification cycles and high switching costs that preserve margin and program stickiness.

Long qualification and switching costs

Once a composite material is on a program, change triggers lengthy requalification—industry requalification cycles typically run 6–18 months and can cost $1–5 million—creating embedded switching costs that moderate buyer power post-award. Pre-award buyers exploit competitive bids to extract concessions, but post-award leverage shifts to Hexcel due to continuity, certified supply chains and program risk.

Price-down expectations over program life

Aerospace OEMs in 2024 continued to insist on learning-curve price reductions and productivity give-backs built into multi-year agreements, pressuring Hexcel to meet embedded cost-down trajectories. Hexcel must deliver measurable yield and throughput gains to preserve margins as contracts expect progressive unit-cost declines. Failure to achieve these improvements risks losing future platform volumes to lower-cost rivals.

Demand cyclicality and inventory policies

Demand cyclicality—Boeing targeting ~38 737s/month in 2024 and US FY2024 defense discretionary spending near 858 billion USD—shifts Hexcel order momentum; buyers flex schedules, reducing capacity utilization and strengthening bargaining power. Vendor-managed inventory programs can smooth supply but shift holding costs to Hexcel. In downturns volatility amplifies buyer influence, compressing pricing and lead times.

- Buyers flex schedules → lower utilization

- 38/mo Boeing target (2024) → order volatility

- US defense budget ~858B (FY2024) → program shifts

- VMI transfers inventory burden to Hexcel

Specification control and design authority

Customers set material specs and performance envelopes, directing procurement choices and enabling trials of competitive alternates; co-development raises switching costs but transfers IP benefits. Buyer power stays high to moderate across program phases, strongest at qualification and pricing rounds and easing after qualification into production. In 2024 the global aerospace composites market exceeded 20 billion USD, reinforcing OEM leverage.

- Customer design authority → procurement control

- Co-development → partial lock-in + shared IP

- Program phase-sensitive buyer power

- 2024 market size >20 billion USD

Concentrated OEM demand and dual-sourcing squeeze pre-award pricing; switching costs protect margins

Buyers concentrated (Airbus/Boeing/primes) and dual-sourcing compress pricing pre-award, while Hexcel's in-service performance, long requalification (6–18 months, $1–5M) and switching costs protect post-award margins. OEMs demand learning-curve cost reductions; Boeing 38/mo (2024) and US defense ~$858B (FY2024) drive order volatility. 2024 aerospace composites market >$20B; VMI shifts inventory risk to Hexcel.

| Metric | 2024 value |

|---|---|

| Boeing production target | ~38/mo |

| US defense budget | ~$858B (FY2024) |

| Composites market | >$20B |

| Requalification | 6–18 months; $1–5M |

Preview the Actual Deliverable

Hexcel Porter's Five Forces Analysis

This preview shows the exact Hexcel Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The full, professionally formatted document is ready for download and use the moment you buy. You're viewing the final deliverable in its entirety.

Description

From Overview to Strategy Blueprint

Hexcel faces moderate supplier power due to specialized composite materials, intense rivalry from aerospace composites peers, and a manageable threat of new entrants given high capital and tech barriers. Buyers wield bargaining power through large OEM contracts, while substitutes remain limited. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hexcel’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated critical inputs

Hexcel depends on a limited set of suppliers for PAN precursor, specialty resins and aerospace-grade fibers, a point highlighted in its 2024 Form 10-K. Supplier concentration elevates switching costs and dependency risk; disruptions can delay production and compress margins. Long-term contracts mitigate but preserve supplier leverage.

Specialty chemicals and qualification

Resins, tougheners and aerospace adhesives must meet stringent program specs and are qualified per program, narrowing approved vendor lists to often 3–5 suppliers and limiting Hexcel’s ability to dual‑source quickly. Suppliers with unique chemistries command pricing and delivery leverage, and requalification timelines—commonly 12–24 months—further entrench supplier power, raising switching costs and lead‑time risk.

Capital-intensive equipment and utilities

Carbonization lines, autoclaves, and high-capacity energy systems are mission-critical and costly to modify, giving suppliers of specialized OEM equipment significant leverage over Hexcel’s timelines and contract terms. Limited global OEMs for these machines concentrate bargaining power and can extend multi-month lead times. Hexcel’s electricity- and gas-intensive processes leave it exposed to utility price swings, and while energy hedging reduces some risk, it only partially offsets supplier pricing power.

Geopolitical and trade exposure

Cross-border sourcing of acrylonitrile, fibers and specialty chemicals exposes Hexcel to tariffs, export controls and logistics bottlenecks; suppliers in tightly regulated regions commonly pass through compliance costs, and currency swings can strengthen supplier bargaining positions. Diversification of sources mitigates but does not eliminate this exposure.

- Tariffs and export controls

- Compliance cost pass-through

- Currency-driven supplier leverage

- Diversification reduces but not removes risk

Countervailing power via scale

Hexcel’s global scale and multi-year aerospace demand visibility give it leverage: the company reported approximately $2.6 billion in net sales in 2024 and sustained a multi-year commercial aircraft backlog, enabling volume commitments that blunt supplier pricing power. Joint development deals and vendor-managed inventory programs reduce stockouts and align incentives, but highly bespoke resin and prepreg formulations plus tight aerospace specifications limit standardization gains. Overall supplier power is moderate.

- Scale: Hexcel 2024 net sales ~ $2.6B

- Demand visibility: multi-year commercial backlog

- Supply mitigation: JVs and VMI reduce disruption

- Constraint: bespoke specs cap supplier substitutability

- Net: moderate supplier bargaining power

Supplier leverage: 12–24 month requal. vs $2.6B 2024 sales

Hexcel faces moderate supplier power: concentrated providers of PAN precursor, specialty resins and aerospace fibers (approved vendors often 3–5) and 12–24 month requalification timelines raise switching costs, while 2024 net sales ~$2.6B and multi-year aircraft backlog provide volume leverage; JVs/VMI mitigate but bespoke specs sustain supplier influence.

| Metric | Value |

|---|---|

| 2024 Net Sales | $2.6B |

| Approved suppliers | 3–5 |

| Requalification | 12–24 months |

What is included in the product

Tailored Porter's Five Forces analysis of Hexcel that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic commentary on pricing, profitability and market dynamics to inform investor, executive, and academic use.

A concise one-sheet Porter's Five Forces for Hexcel that visualizes competitive pressure with an editable spider chart, lets you toggle scenarios (pre/post regulation, new entrant), and delivers a clean, copy-ready layout for decks—no macros, easy for non-finance users.

Customers Bargaining Power

Highly concentrated OEM base

Airbus, Boeing and major engine/defense primes drove the bulk of airframe and aero-structures demand in 2024, concentrating purchasing power and giving program-timing and delivery schedules outsized negotiating leverage.

Buyers’ dual-sourcing strategies and long lead contracts further compress pricing and tighten commercial terms across supply tiers.

Hexcel counters through demonstrated in-service performance, long qualification cycles and high switching costs that preserve margin and program stickiness.

Long qualification and switching costs

Once a composite material is on a program, change triggers lengthy requalification—industry requalification cycles typically run 6–18 months and can cost $1–5 million—creating embedded switching costs that moderate buyer power post-award. Pre-award buyers exploit competitive bids to extract concessions, but post-award leverage shifts to Hexcel due to continuity, certified supply chains and program risk.

Price-down expectations over program life

Aerospace OEMs in 2024 continued to insist on learning-curve price reductions and productivity give-backs built into multi-year agreements, pressuring Hexcel to meet embedded cost-down trajectories. Hexcel must deliver measurable yield and throughput gains to preserve margins as contracts expect progressive unit-cost declines. Failure to achieve these improvements risks losing future platform volumes to lower-cost rivals.

Demand cyclicality and inventory policies

Demand cyclicality—Boeing targeting ~38 737s/month in 2024 and US FY2024 defense discretionary spending near 858 billion USD—shifts Hexcel order momentum; buyers flex schedules, reducing capacity utilization and strengthening bargaining power. Vendor-managed inventory programs can smooth supply but shift holding costs to Hexcel. In downturns volatility amplifies buyer influence, compressing pricing and lead times.

- Buyers flex schedules → lower utilization

- 38/mo Boeing target (2024) → order volatility

- US defense budget ~858B (FY2024) → program shifts

- VMI transfers inventory burden to Hexcel

Specification control and design authority

Customers set material specs and performance envelopes, directing procurement choices and enabling trials of competitive alternates; co-development raises switching costs but transfers IP benefits. Buyer power stays high to moderate across program phases, strongest at qualification and pricing rounds and easing after qualification into production. In 2024 the global aerospace composites market exceeded 20 billion USD, reinforcing OEM leverage.

- Customer design authority → procurement control

- Co-development → partial lock-in + shared IP

- Program phase-sensitive buyer power

- 2024 market size >20 billion USD

Concentrated OEM demand and dual-sourcing squeeze pre-award pricing; switching costs protect margins

Buyers concentrated (Airbus/Boeing/primes) and dual-sourcing compress pricing pre-award, while Hexcel's in-service performance, long requalification (6–18 months, $1–5M) and switching costs protect post-award margins. OEMs demand learning-curve cost reductions; Boeing 38/mo (2024) and US defense ~$858B (FY2024) drive order volatility. 2024 aerospace composites market >$20B; VMI shifts inventory risk to Hexcel.

| Metric | 2024 value |

|---|---|

| Boeing production target | ~38/mo |

| US defense budget | ~$858B (FY2024) |

| Composites market | >$20B |

| Requalification | 6–18 months; $1–5M |

Preview the Actual Deliverable

Hexcel Porter's Five Forces Analysis

This preview shows the exact Hexcel Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The full, professionally formatted document is ready for download and use the moment you buy. You're viewing the final deliverable in its entirety.