HF Sinclair Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

Curious where HF Sinclair’s products sit—Stars, Cash Cows, Dogs or Question Marks? This preview gives a taste, but the full BCG Matrix maps every offering into its quadrant with data-backed rationale and clear strategic moves. Buy the complete report for a Word write-up and an Excel summary you can use immediately to reallocate capital and sharpen priorities.

Stars

Renewable diesel platform

High-growth demand and 2024 policy tailwinds such as sustained tax incentives under the Inflation Reduction Act position HF Sinclair’s renewable diesel platform in leader territory; existing refinery footprints and conversion experience lower execution risk. The unit still consumes significant capex and working capital for feedstock sourcing and pretreatment and upgrades. Keep share and scale pretreatment and it can flip into a powerhouse cash engine; invest while the market’s hot.

Low-carbon fuel credits and integration

Owning both low-carbon fuel production and downstream placement lets HF Sinclair capture full credit value and retail margins, leveraging its refinery footprint and trading desks to monetize LCFS/low-carbon fuel credits often priced around $160/MTCO2e in 2024. That vertical integration accelerates share gains in a compliance market growing roughly 15% CAGR through 2030. Maintaining compliance systems and trading sophistication requires sustained spend; HF Sinclair’s reinvestment keeps the commercialization flywheel spinning.

Export diesel channels

Latin America demand growth continues to pull U.S. Gulf and inland diesel barrels, and HF Sinclair’s logistics network places molecules into higher-margin export lanes, lifting its share in this expanding channel.

Success depends on sustained marketing muscle and resilient supply chains to convert access into contracted flows.

Keep pushing long-term contracts and waterborne optionality to secure price capture and operational flexibility.

Specialty performance products adjacencies

Specialty performance product adjacencies—niche, higher-spec formulations that ride industrial and mobility transitions—can outgrow base fuels and position HF Sinclair as a Star in the BCG matrix; the company’s refining and marketing scale and legacy brands give it permission to lead select niches. These lines require technical selling, sustained promotion, and channel investments to convert R&D into margin lift. Worth the push while categories expand.

- focus: selective high-margin formulations

- capability: existing refining & brand reach

- need: technical sales + marketing

- timing: leverage mobility/industrial shifts

Operational excellence data stack

Operational excellence data stack is a Star for HF Sinclair in the BCG matrix: digital optimization across refineries and midstream can lift throughput 3–5% and yield 0.5–1.5%, while early movers cut downtime 20–30% and operating costs 5–10%; building and sustaining these systems is cash-intensive (typical complex-level investments $50–150M), so doubling down widens the operating gap during a steep adoption curve.

- Throughput uplift 3–5%

- Yield gain 0.5–1.5%

- Downtime reduction 20–30%

- Capex $50–150M per complex

Renewable diesel boom: LCFS tailwinds, 15% market CAGR, 3–5% ops upside

High-growth renewable diesel and specialty formulations are Stars given 2024 tailwinds: LCFS credits ≈ $160/MTCO2e and a compliance market ~15% CAGR to 2030; existing refinery conversion experience reduces execution risk. Operational digital upgrades can raise throughput 3–5% and yield 0.5–1.5% but need $50–150M per complex. Vertical integration captures retail margins and credits; prioritize contracts and pretreatment scale.

| Metric | 2024 value |

|---|---|

| LCFS price | $160/MTCO2e |

| Compliance market CAGR | ~15% to 2030 |

| Throughput uplift | 3–5% |

| Yield gain | 0.5–1.5% |

| Capex per complex | $50–150M |

What is included in the product

Concise BCG review of HF Sinclair’s units, showing Stars, Cash Cows, Question Marks, Dogs with strategic investment recommendations.

One-page HF Sinclair BCG Matrix placing business units in quadrants to simplify portfolio decisions for executives.

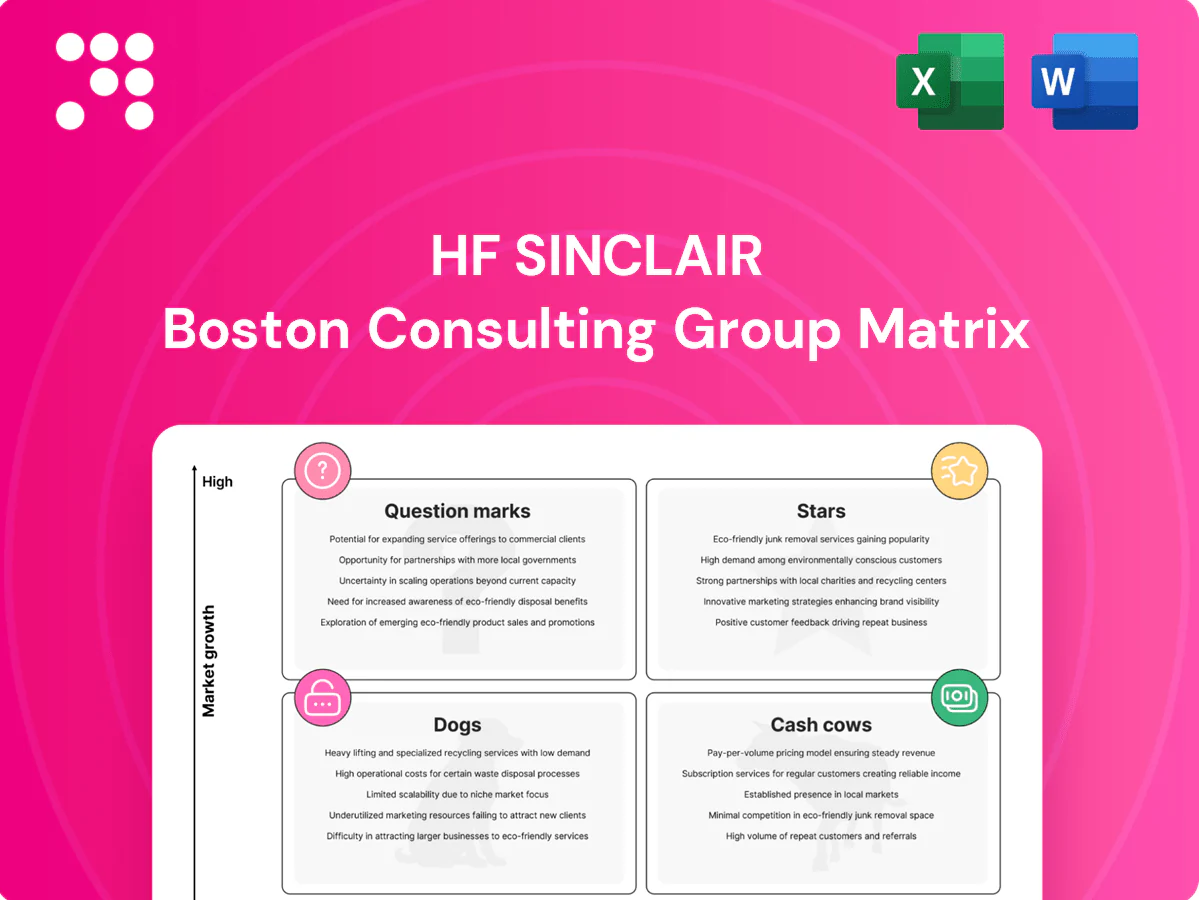

Cash Cows

Core gasoline and diesel refining

Core gasoline and diesel refining sits in mature markets with large share and dependable cash flow; U.S. gasoline demand ran about 8.9 million b/d in 2024, keeping steady throughput. When cracks normalized in 2024 (roughly mid-single-digit to low-teens $/bbl), the network still threw off reliable dollars. Capex is maintenance-heavy, not growth-heavy—milk it, keep reliability top-tier, and defend costs.

Jet fuel into stable hubs

Aviation demand largely recovered in 2024, with U.S. jet fuel consumption averaging about 1.8 million barrels per day (EIA), placing the market in a mature demand lane. HF Sinclair’s slate and hub placement deliver durable volumes into major airport-centered terminals, supporting steady refining throughput. Marketing spend remains modest versus returns, keeping SG&A leverage favorable. Maintain contracts, optimize yields and bank the cash to fund returns.

Pipelines and terminals

Pipelines and terminals are fee-based, mature, and sticky within HF Sinclair (NYSE DINO), delivering through-cycle cash with relatively low growth; incremental investments in connections and pumps lift efficiency and capacity. Maintain high uptime and competitive tariffs to sustain the annuity; prioritize maintenance capex and commercial contracts in 2024 to protect cash generation. Tariff discipline and utilization drive predictability.

Base oils and lubricants core lines

Base oils and lubricants core lines are HF Sinclair cash cows: established brands and loyal industrial accounts drove predictable reorder cycles in 2024, delivering steady operating cash flow and margins that held up better than commodity fuels.

Limited promotion is needed once channels are set; focus on protecting quality and service while squeezing more throughput improves utilization and incremental margin.

- Established brands

- Loyal industrial customers

- Predictable reorder

- Margins > commodity fuels

- Low promo, protect quality

Asphalt and other heavy ends

Asphalt and other heavy ends deliver steady, seasonal cash flow for HF Sinclair, with peak offtake concentrated in the April–September paving season (roughly 60% of annual volumes), serving mature municipal and contractor buyers with predictable pricing patterns and low incremental marketing costs.

Optimize refinery blending and logistics to maximize margin capture; these operations are capital-efficient and can fund higher-growth, higher-risk downstream and low‑carbon bets.

- Seasonal offtake: ~60% Apr–Sep

- Mature buyers: stable contract pricing

- Low marketing: high margin tailwind

- Strategic role: fund riskier growth initiatives

Refining cash engines: gas, jet, fee pipelines, lube margins and seasonal asphalt

Core gasoline/diesel refining, fee-based pipelines/terminals, base oils/lubricants and asphalt are HF Sinclair cash cows: 2024 U.S. gasoline demand ~8.9 million b/d, jet fuel ~1.8 million b/d; cracks normalized mid-single-digit to low-teens $/bbl, delivering steady FCF; asphalt ~60% Apr–Sep offtake. Prioritize reliability, tariff discipline, yield optimization and maintenance capex to preserve cash flow.

| Asset | 2024 metric | Role |

|---|---|---|

| Refining (gas/diesel) | Gasoline ~8.9m b/d; cracks mid-single to low-teens $/bbl | High cash generation |

| Aviation | Jet ~1.8m b/d | Durable volumes |

| Pipelines/terminals | Fee-based, sticky | Annuity cash |

| Base oils/lubes | Stable reorder; margins > commodity fuels | Predictable FCF |

| Asphalt | ~60% Apr–Sep seasonality | Seasonal cash |

Preview = Final Product

HF Sinclair BCG Matrix

The file you're previewing is the exact HF Sinclair BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic clarity. After payment the same document downloads immediately to your inbox, editable and presentation-ready. Use it in planning, investor decks, or client meetings with zero surprises.

Visual. Strategic. Downloadable.

Curious where HF Sinclair’s products sit—Stars, Cash Cows, Dogs or Question Marks? This preview gives a taste, but the full BCG Matrix maps every offering into its quadrant with data-backed rationale and clear strategic moves. Buy the complete report for a Word write-up and an Excel summary you can use immediately to reallocate capital and sharpen priorities.

Stars

Renewable diesel platform

High-growth demand and 2024 policy tailwinds such as sustained tax incentives under the Inflation Reduction Act position HF Sinclair’s renewable diesel platform in leader territory; existing refinery footprints and conversion experience lower execution risk. The unit still consumes significant capex and working capital for feedstock sourcing and pretreatment and upgrades. Keep share and scale pretreatment and it can flip into a powerhouse cash engine; invest while the market’s hot.

Low-carbon fuel credits and integration

Owning both low-carbon fuel production and downstream placement lets HF Sinclair capture full credit value and retail margins, leveraging its refinery footprint and trading desks to monetize LCFS/low-carbon fuel credits often priced around $160/MTCO2e in 2024. That vertical integration accelerates share gains in a compliance market growing roughly 15% CAGR through 2030. Maintaining compliance systems and trading sophistication requires sustained spend; HF Sinclair’s reinvestment keeps the commercialization flywheel spinning.

Export diesel channels

Latin America demand growth continues to pull U.S. Gulf and inland diesel barrels, and HF Sinclair’s logistics network places molecules into higher-margin export lanes, lifting its share in this expanding channel.

Success depends on sustained marketing muscle and resilient supply chains to convert access into contracted flows.

Keep pushing long-term contracts and waterborne optionality to secure price capture and operational flexibility.

Specialty performance products adjacencies

Specialty performance product adjacencies—niche, higher-spec formulations that ride industrial and mobility transitions—can outgrow base fuels and position HF Sinclair as a Star in the BCG matrix; the company’s refining and marketing scale and legacy brands give it permission to lead select niches. These lines require technical selling, sustained promotion, and channel investments to convert R&D into margin lift. Worth the push while categories expand.

- focus: selective high-margin formulations

- capability: existing refining & brand reach

- need: technical sales + marketing

- timing: leverage mobility/industrial shifts

Operational excellence data stack

Operational excellence data stack is a Star for HF Sinclair in the BCG matrix: digital optimization across refineries and midstream can lift throughput 3–5% and yield 0.5–1.5%, while early movers cut downtime 20–30% and operating costs 5–10%; building and sustaining these systems is cash-intensive (typical complex-level investments $50–150M), so doubling down widens the operating gap during a steep adoption curve.

- Throughput uplift 3–5%

- Yield gain 0.5–1.5%

- Downtime reduction 20–30%

- Capex $50–150M per complex

Renewable diesel boom: LCFS tailwinds, 15% market CAGR, 3–5% ops upside

High-growth renewable diesel and specialty formulations are Stars given 2024 tailwinds: LCFS credits ≈ $160/MTCO2e and a compliance market ~15% CAGR to 2030; existing refinery conversion experience reduces execution risk. Operational digital upgrades can raise throughput 3–5% and yield 0.5–1.5% but need $50–150M per complex. Vertical integration captures retail margins and credits; prioritize contracts and pretreatment scale.

| Metric | 2024 value |

|---|---|

| LCFS price | $160/MTCO2e |

| Compliance market CAGR | ~15% to 2030 |

| Throughput uplift | 3–5% |

| Yield gain | 0.5–1.5% |

| Capex per complex | $50–150M |

What is included in the product

Concise BCG review of HF Sinclair’s units, showing Stars, Cash Cows, Question Marks, Dogs with strategic investment recommendations.

One-page HF Sinclair BCG Matrix placing business units in quadrants to simplify portfolio decisions for executives.

Cash Cows

Core gasoline and diesel refining

Core gasoline and diesel refining sits in mature markets with large share and dependable cash flow; U.S. gasoline demand ran about 8.9 million b/d in 2024, keeping steady throughput. When cracks normalized in 2024 (roughly mid-single-digit to low-teens $/bbl), the network still threw off reliable dollars. Capex is maintenance-heavy, not growth-heavy—milk it, keep reliability top-tier, and defend costs.

Jet fuel into stable hubs

Aviation demand largely recovered in 2024, with U.S. jet fuel consumption averaging about 1.8 million barrels per day (EIA), placing the market in a mature demand lane. HF Sinclair’s slate and hub placement deliver durable volumes into major airport-centered terminals, supporting steady refining throughput. Marketing spend remains modest versus returns, keeping SG&A leverage favorable. Maintain contracts, optimize yields and bank the cash to fund returns.

Pipelines and terminals

Pipelines and terminals are fee-based, mature, and sticky within HF Sinclair (NYSE DINO), delivering through-cycle cash with relatively low growth; incremental investments in connections and pumps lift efficiency and capacity. Maintain high uptime and competitive tariffs to sustain the annuity; prioritize maintenance capex and commercial contracts in 2024 to protect cash generation. Tariff discipline and utilization drive predictability.

Base oils and lubricants core lines

Base oils and lubricants core lines are HF Sinclair cash cows: established brands and loyal industrial accounts drove predictable reorder cycles in 2024, delivering steady operating cash flow and margins that held up better than commodity fuels.

Limited promotion is needed once channels are set; focus on protecting quality and service while squeezing more throughput improves utilization and incremental margin.

- Established brands

- Loyal industrial customers

- Predictable reorder

- Margins > commodity fuels

- Low promo, protect quality

Asphalt and other heavy ends

Asphalt and other heavy ends deliver steady, seasonal cash flow for HF Sinclair, with peak offtake concentrated in the April–September paving season (roughly 60% of annual volumes), serving mature municipal and contractor buyers with predictable pricing patterns and low incremental marketing costs.

Optimize refinery blending and logistics to maximize margin capture; these operations are capital-efficient and can fund higher-growth, higher-risk downstream and low‑carbon bets.

- Seasonal offtake: ~60% Apr–Sep

- Mature buyers: stable contract pricing

- Low marketing: high margin tailwind

- Strategic role: fund riskier growth initiatives

Refining cash engines: gas, jet, fee pipelines, lube margins and seasonal asphalt

Core gasoline/diesel refining, fee-based pipelines/terminals, base oils/lubricants and asphalt are HF Sinclair cash cows: 2024 U.S. gasoline demand ~8.9 million b/d, jet fuel ~1.8 million b/d; cracks normalized mid-single-digit to low-teens $/bbl, delivering steady FCF; asphalt ~60% Apr–Sep offtake. Prioritize reliability, tariff discipline, yield optimization and maintenance capex to preserve cash flow.

| Asset | 2024 metric | Role |

|---|---|---|

| Refining (gas/diesel) | Gasoline ~8.9m b/d; cracks mid-single to low-teens $/bbl | High cash generation |

| Aviation | Jet ~1.8m b/d | Durable volumes |

| Pipelines/terminals | Fee-based, sticky | Annuity cash |

| Base oils/lubes | Stable reorder; margins > commodity fuels | Predictable FCF |

| Asphalt | ~60% Apr–Sep seasonality | Seasonal cash |

Preview = Final Product

HF Sinclair BCG Matrix

The file you're previewing is the exact HF Sinclair BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic clarity. After payment the same document downloads immediately to your inbox, editable and presentation-ready. Use it in planning, investor decks, or client meetings with zero surprises.

Original: $10.00

-65%$10.00

$3.50Description

Visual. Strategic. Downloadable.

Curious where HF Sinclair’s products sit—Stars, Cash Cows, Dogs or Question Marks? This preview gives a taste, but the full BCG Matrix maps every offering into its quadrant with data-backed rationale and clear strategic moves. Buy the complete report for a Word write-up and an Excel summary you can use immediately to reallocate capital and sharpen priorities.

Stars

Renewable diesel platform

High-growth demand and 2024 policy tailwinds such as sustained tax incentives under the Inflation Reduction Act position HF Sinclair’s renewable diesel platform in leader territory; existing refinery footprints and conversion experience lower execution risk. The unit still consumes significant capex and working capital for feedstock sourcing and pretreatment and upgrades. Keep share and scale pretreatment and it can flip into a powerhouse cash engine; invest while the market’s hot.

Low-carbon fuel credits and integration

Owning both low-carbon fuel production and downstream placement lets HF Sinclair capture full credit value and retail margins, leveraging its refinery footprint and trading desks to monetize LCFS/low-carbon fuel credits often priced around $160/MTCO2e in 2024. That vertical integration accelerates share gains in a compliance market growing roughly 15% CAGR through 2030. Maintaining compliance systems and trading sophistication requires sustained spend; HF Sinclair’s reinvestment keeps the commercialization flywheel spinning.

Export diesel channels

Latin America demand growth continues to pull U.S. Gulf and inland diesel barrels, and HF Sinclair’s logistics network places molecules into higher-margin export lanes, lifting its share in this expanding channel.

Success depends on sustained marketing muscle and resilient supply chains to convert access into contracted flows.

Keep pushing long-term contracts and waterborne optionality to secure price capture and operational flexibility.

Specialty performance products adjacencies

Specialty performance product adjacencies—niche, higher-spec formulations that ride industrial and mobility transitions—can outgrow base fuels and position HF Sinclair as a Star in the BCG matrix; the company’s refining and marketing scale and legacy brands give it permission to lead select niches. These lines require technical selling, sustained promotion, and channel investments to convert R&D into margin lift. Worth the push while categories expand.

- focus: selective high-margin formulations

- capability: existing refining & brand reach

- need: technical sales + marketing

- timing: leverage mobility/industrial shifts

Operational excellence data stack

Operational excellence data stack is a Star for HF Sinclair in the BCG matrix: digital optimization across refineries and midstream can lift throughput 3–5% and yield 0.5–1.5%, while early movers cut downtime 20–30% and operating costs 5–10%; building and sustaining these systems is cash-intensive (typical complex-level investments $50–150M), so doubling down widens the operating gap during a steep adoption curve.

- Throughput uplift 3–5%

- Yield gain 0.5–1.5%

- Downtime reduction 20–30%

- Capex $50–150M per complex

Renewable diesel boom: LCFS tailwinds, 15% market CAGR, 3–5% ops upside

High-growth renewable diesel and specialty formulations are Stars given 2024 tailwinds: LCFS credits ≈ $160/MTCO2e and a compliance market ~15% CAGR to 2030; existing refinery conversion experience reduces execution risk. Operational digital upgrades can raise throughput 3–5% and yield 0.5–1.5% but need $50–150M per complex. Vertical integration captures retail margins and credits; prioritize contracts and pretreatment scale.

| Metric | 2024 value |

|---|---|

| LCFS price | $160/MTCO2e |

| Compliance market CAGR | ~15% to 2030 |

| Throughput uplift | 3–5% |

| Yield gain | 0.5–1.5% |

| Capex per complex | $50–150M |

What is included in the product

Concise BCG review of HF Sinclair’s units, showing Stars, Cash Cows, Question Marks, Dogs with strategic investment recommendations.

One-page HF Sinclair BCG Matrix placing business units in quadrants to simplify portfolio decisions for executives.

Cash Cows

Core gasoline and diesel refining

Core gasoline and diesel refining sits in mature markets with large share and dependable cash flow; U.S. gasoline demand ran about 8.9 million b/d in 2024, keeping steady throughput. When cracks normalized in 2024 (roughly mid-single-digit to low-teens $/bbl), the network still threw off reliable dollars. Capex is maintenance-heavy, not growth-heavy—milk it, keep reliability top-tier, and defend costs.

Jet fuel into stable hubs

Aviation demand largely recovered in 2024, with U.S. jet fuel consumption averaging about 1.8 million barrels per day (EIA), placing the market in a mature demand lane. HF Sinclair’s slate and hub placement deliver durable volumes into major airport-centered terminals, supporting steady refining throughput. Marketing spend remains modest versus returns, keeping SG&A leverage favorable. Maintain contracts, optimize yields and bank the cash to fund returns.

Pipelines and terminals

Pipelines and terminals are fee-based, mature, and sticky within HF Sinclair (NYSE DINO), delivering through-cycle cash with relatively low growth; incremental investments in connections and pumps lift efficiency and capacity. Maintain high uptime and competitive tariffs to sustain the annuity; prioritize maintenance capex and commercial contracts in 2024 to protect cash generation. Tariff discipline and utilization drive predictability.

Base oils and lubricants core lines

Base oils and lubricants core lines are HF Sinclair cash cows: established brands and loyal industrial accounts drove predictable reorder cycles in 2024, delivering steady operating cash flow and margins that held up better than commodity fuels.

Limited promotion is needed once channels are set; focus on protecting quality and service while squeezing more throughput improves utilization and incremental margin.

- Established brands

- Loyal industrial customers

- Predictable reorder

- Margins > commodity fuels

- Low promo, protect quality

Asphalt and other heavy ends

Asphalt and other heavy ends deliver steady, seasonal cash flow for HF Sinclair, with peak offtake concentrated in the April–September paving season (roughly 60% of annual volumes), serving mature municipal and contractor buyers with predictable pricing patterns and low incremental marketing costs.

Optimize refinery blending and logistics to maximize margin capture; these operations are capital-efficient and can fund higher-growth, higher-risk downstream and low‑carbon bets.

- Seasonal offtake: ~60% Apr–Sep

- Mature buyers: stable contract pricing

- Low marketing: high margin tailwind

- Strategic role: fund riskier growth initiatives

Refining cash engines: gas, jet, fee pipelines, lube margins and seasonal asphalt

Core gasoline/diesel refining, fee-based pipelines/terminals, base oils/lubricants and asphalt are HF Sinclair cash cows: 2024 U.S. gasoline demand ~8.9 million b/d, jet fuel ~1.8 million b/d; cracks normalized mid-single-digit to low-teens $/bbl, delivering steady FCF; asphalt ~60% Apr–Sep offtake. Prioritize reliability, tariff discipline, yield optimization and maintenance capex to preserve cash flow.

| Asset | 2024 metric | Role |

|---|---|---|

| Refining (gas/diesel) | Gasoline ~8.9m b/d; cracks mid-single to low-teens $/bbl | High cash generation |

| Aviation | Jet ~1.8m b/d | Durable volumes |

| Pipelines/terminals | Fee-based, sticky | Annuity cash |

| Base oils/lubes | Stable reorder; margins > commodity fuels | Predictable FCF |

| Asphalt | ~60% Apr–Sep seasonality | Seasonal cash |

Preview = Final Product

HF Sinclair BCG Matrix

The file you're previewing is the exact HF Sinclair BCG Matrix you'll receive after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready report tailored for strategic clarity. After payment the same document downloads immediately to your inbox, editable and presentation-ready. Use it in planning, investor decks, or client meetings with zero surprises.