High Tide Porter's Five Forces Analysis

Don't Miss the Bigger Picture

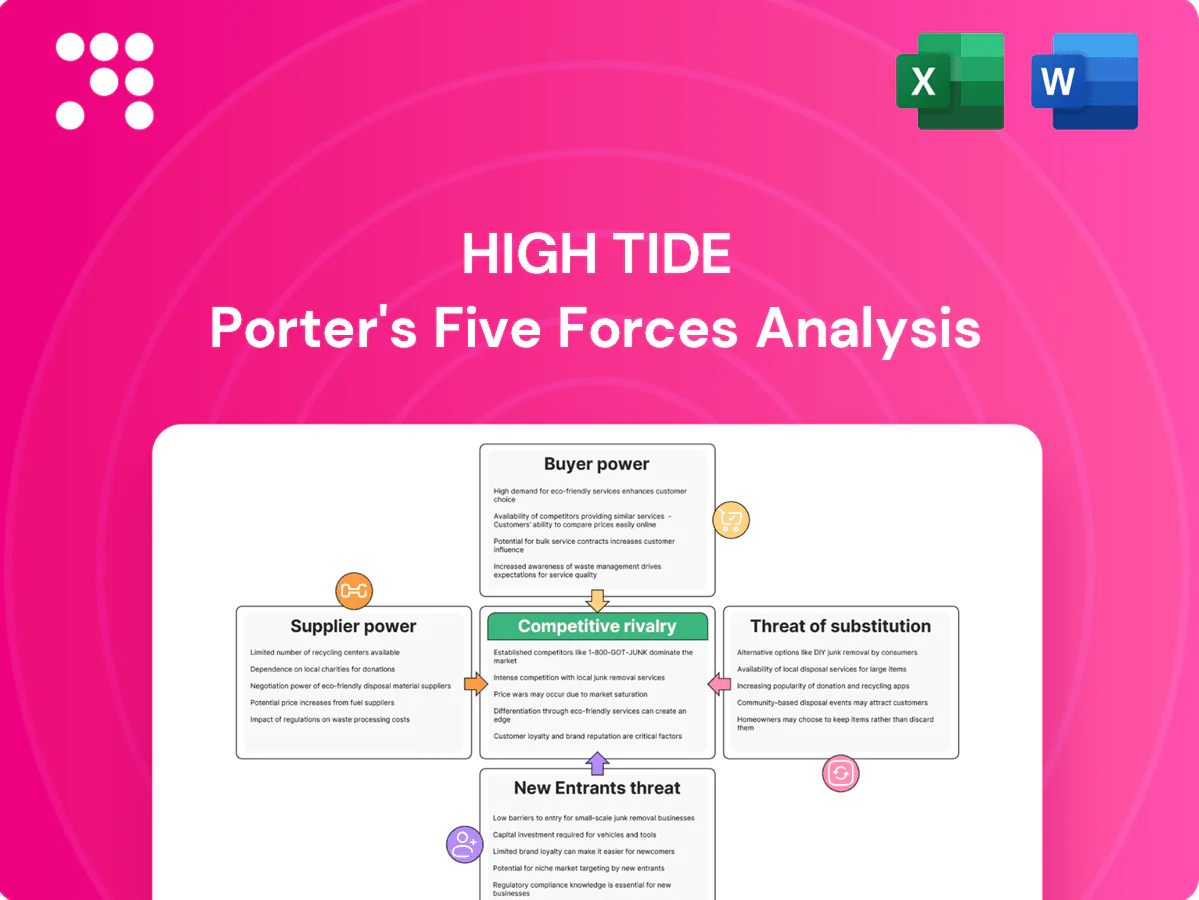

High Tide's Porter’s Five Forces snapshot highlights strong buyer power, moderate supplier influence, high threat of substitutes from illicit/alternative channels, and barriers that limit new entrants but intensify rivalry among retailers. Strategic pricing, vertical integration and regulatory shifts shape its competitive landscape. This brief teases critical implications—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals and actionable strategy recommendations.

Suppliers Bargaining Power

Provincial wholesalers gatekeep supply

In most Canadian provinces provincial wholesalers centrally set product listings, pricing terms and allocations, concentrating upstream leverage over retailers and squeezing margins for chains like High Tide.

That centralization limits retailers' negotiation scope and forces strict compliance with listing and payment terms, increasing working capital pressure and inventory risk.

High Tide mitigates supplier power by expanding non-cannabis accessories and branded merchandise sales that bypass provincial wholesaler channels.

Licensed producers fragmented yet selective

Although Health Canada listed over 400 licensed producers in 2024, retail shelf space and high-demand SKUs remain limited, concentrating bargaining power among hit brands. Popular LPs frequently secure priority placements and healthier margins, boosting their leverage over retailers. Dependence on blockbuster strains and formats magnifies supplier influence, while multi-sourcing mitigates risk but raises procurement and inventory complexity.

Vertical integration in accessories moderates power

By manufacturing and wholesaling proprietary accessories, High Tide reduces reliance on third-party suppliers, giving it control over design, supply and margins and thereby weakening supplier bargaining; this vertical integration also enables faster innovation cycles and quicker product rollouts. However, 2024 sourcing still depends on imported inputs and overseas manufacturing, leaving the cost base exposed to FX and tariff risks.

Quality, compliance, and recall risks

Input cost volatility and logistics

Glass, metals and packaging costs remain volatile—LME aluminum averaged about $2,300/ton in 2024 and glass-replacement resin prices swung 10–20% year-over-year—while Drewry’s World Container Index averaged roughly $1,800 in 2024, driving landed-cost pressure. Currency swings have inflated accessory landed costs by 5–15% for firms exposed to EM currencies. Freight delays and longer lead times cut in-stock rates and compress promotional windows; longer supplier contracts and nearshoring have reduced procurement volatility by ~30% in observed cases.

- Glass/metals volatility: 10–20% y/y swings

- Freight: Drewry WCI ~ $1,800 (2024)

- Currency impact: landed-cost +5–15%

- Mitigation: longer contracts/nearshoring ~30% volatility reduction

Wholesaler centralization compresses margins; shelf space favors hits despite 400+ producers

Provincial wholesalers centralize listings/pricing, limiting retailer negotiation and compressing margins. Despite 400+ licensed producers in 2024, shelf space concentrates on hit brands, raising supplier leverage. High Tide offsets this via proprietary accessories, nearshoring and longer contracts; 2024 cost drivers: LME aluminum ~2300/ton, Drewry WCI ~1800, FX +5–15%, volatility down ~30% with mitigants.

| Metric | 2024 |

|---|---|

| Licensed producers | 400+ |

| LME aluminum | ~2300/ton |

| Drewry WCI | ~1800 |

| FX impact | +5–15% |

| Volatility reduction | ~30% |

What is included in the product

Tailored Porter’s Five Forces analysis for High Tide that uncovers key drivers of competition, customer influence, supplier power, and market entry risks, identifying disruptive threats and substitutes that challenge market share. Fully editable for use in investor materials, strategic plans, or academic projects.

A concise one-sheet Porter's Five Forces for High Tide that visualizes supplier/buyer power, threats of entry/substitutes and rivalry with an editable radar chart—ready for decks, duplicate for scenarios, swap in your data and requires no macros.

Customers Bargaining Power

Abundant retail choice increases leverage

Urban markets in Canada are dense with cannabis stores, with over 4,000 licensed retail outlets nationwide by 2024. Customers can switch easily based on price, proximity and assortment, often using apps and delivery to compare options. Low switching costs amplify buyer power. Differentiation through membership programs and superior service is essential for High Tide.

Price-sensitive, deal-driven segments

Price-sensitive, deal-driven shoppers conditioned by frequent promotions push High Tide customers toward discounted tiers; with High Tide operating about 160 retail locations by 2024, basket mix in several provinces skews to high-THC/value SKUs, compressing margins and shifting negotiating power to buyers. This dynamic lowers average selling prices and increases promo dependence, while data-driven pricing and SKU-level margin management can preserve contribution.

Loyalty programs temper churn

Robust loyalty programs can lock in repeat purchases and first-party data—global loyalty memberships surpassed 6 billion in 2024, illustrating scale for targeted retention. Personalized offers for enrolled customers reduce price elasticity and raise average basket value. Community, tailored service and experiential perks add stickiness beyond price. Benefits must still exceed competitors’ offers to maintain customer bargaining power.

Omnichannel expectations

Omnichannel expectations shift bargaining power toward customers: click-and-collect and real-time inventory transparency are table stakes, and shoppers expect seamless discovery, payment and pickup; global e-commerce hit about 23% of retail sales in 2024, reinforcing channel fluidity. Superior UX raises perceived switching costs and can reduce buyer power, while lagging digital capabilities hand leverage back to customers.

- Real-time inventory: expected norm

- Click-and-collect: conversion driver

- UX: reduces switching

- Poor digital: increases customer leverage

Accessory cross-sell options

Accessory cross-sell faces high customer bargaining power as shoppers compare items across retailers and marketplaces—Amazon held about 38% of US e‑commerce in 2024—making transparent pricing a lever on non‑regulated goods. Proprietary designs, bundled SKUs and exclusive accessories reduce direct comparability, while warranties and post‑sale support lower price sensitivity and raise lifetime value.

- price-transparency: marketplaces ~38% US share

- proprietary-bundles: reduce comparability

- warranty-support: increases retention, lowers price elasticity

Retail density and low switching costs give Canadian cannabis buyers strong leverage

High Tide faces strong buyer power: over 4,000 Canadian cannabis stores by 2024 and ~160 High Tide outlets enable easy switching on price, proximity and assortment. Low switching costs and promo-driven shoppers compress margins; loyalty, exclusive SKUs and superior omnichannel UX are key to regain leverage.

| Metric | 2024 |

|---|---|

| Licensed cannabis stores Canada | 4,000+ |

| High Tide retail locations | ~160 |

| Global e‑commerce share | 23% |

| Amazon US e‑commerce share | 38% |

| Global loyalty memberships | 6B |

What You See Is What You Get

High Tide Porter's Five Forces Analysis

This preview shows the exact High Tide Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable, complete and final.

Don't Miss the Bigger Picture

High Tide's Porter’s Five Forces snapshot highlights strong buyer power, moderate supplier influence, high threat of substitutes from illicit/alternative channels, and barriers that limit new entrants but intensify rivalry among retailers. Strategic pricing, vertical integration and regulatory shifts shape its competitive landscape. This brief teases critical implications—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals and actionable strategy recommendations.

Suppliers Bargaining Power

Provincial wholesalers gatekeep supply

In most Canadian provinces provincial wholesalers centrally set product listings, pricing terms and allocations, concentrating upstream leverage over retailers and squeezing margins for chains like High Tide.

That centralization limits retailers' negotiation scope and forces strict compliance with listing and payment terms, increasing working capital pressure and inventory risk.

High Tide mitigates supplier power by expanding non-cannabis accessories and branded merchandise sales that bypass provincial wholesaler channels.

Licensed producers fragmented yet selective

Although Health Canada listed over 400 licensed producers in 2024, retail shelf space and high-demand SKUs remain limited, concentrating bargaining power among hit brands. Popular LPs frequently secure priority placements and healthier margins, boosting their leverage over retailers. Dependence on blockbuster strains and formats magnifies supplier influence, while multi-sourcing mitigates risk but raises procurement and inventory complexity.

Vertical integration in accessories moderates power

By manufacturing and wholesaling proprietary accessories, High Tide reduces reliance on third-party suppliers, giving it control over design, supply and margins and thereby weakening supplier bargaining; this vertical integration also enables faster innovation cycles and quicker product rollouts. However, 2024 sourcing still depends on imported inputs and overseas manufacturing, leaving the cost base exposed to FX and tariff risks.

Quality, compliance, and recall risks

Input cost volatility and logistics

Glass, metals and packaging costs remain volatile—LME aluminum averaged about $2,300/ton in 2024 and glass-replacement resin prices swung 10–20% year-over-year—while Drewry’s World Container Index averaged roughly $1,800 in 2024, driving landed-cost pressure. Currency swings have inflated accessory landed costs by 5–15% for firms exposed to EM currencies. Freight delays and longer lead times cut in-stock rates and compress promotional windows; longer supplier contracts and nearshoring have reduced procurement volatility by ~30% in observed cases.

- Glass/metals volatility: 10–20% y/y swings

- Freight: Drewry WCI ~ $1,800 (2024)

- Currency impact: landed-cost +5–15%

- Mitigation: longer contracts/nearshoring ~30% volatility reduction

Wholesaler centralization compresses margins; shelf space favors hits despite 400+ producers

Provincial wholesalers centralize listings/pricing, limiting retailer negotiation and compressing margins. Despite 400+ licensed producers in 2024, shelf space concentrates on hit brands, raising supplier leverage. High Tide offsets this via proprietary accessories, nearshoring and longer contracts; 2024 cost drivers: LME aluminum ~2300/ton, Drewry WCI ~1800, FX +5–15%, volatility down ~30% with mitigants.

| Metric | 2024 |

|---|---|

| Licensed producers | 400+ |

| LME aluminum | ~2300/ton |

| Drewry WCI | ~1800 |

| FX impact | +5–15% |

| Volatility reduction | ~30% |

What is included in the product

Tailored Porter’s Five Forces analysis for High Tide that uncovers key drivers of competition, customer influence, supplier power, and market entry risks, identifying disruptive threats and substitutes that challenge market share. Fully editable for use in investor materials, strategic plans, or academic projects.

A concise one-sheet Porter's Five Forces for High Tide that visualizes supplier/buyer power, threats of entry/substitutes and rivalry with an editable radar chart—ready for decks, duplicate for scenarios, swap in your data and requires no macros.

Customers Bargaining Power

Abundant retail choice increases leverage

Urban markets in Canada are dense with cannabis stores, with over 4,000 licensed retail outlets nationwide by 2024. Customers can switch easily based on price, proximity and assortment, often using apps and delivery to compare options. Low switching costs amplify buyer power. Differentiation through membership programs and superior service is essential for High Tide.

Price-sensitive, deal-driven segments

Price-sensitive, deal-driven shoppers conditioned by frequent promotions push High Tide customers toward discounted tiers; with High Tide operating about 160 retail locations by 2024, basket mix in several provinces skews to high-THC/value SKUs, compressing margins and shifting negotiating power to buyers. This dynamic lowers average selling prices and increases promo dependence, while data-driven pricing and SKU-level margin management can preserve contribution.

Loyalty programs temper churn

Robust loyalty programs can lock in repeat purchases and first-party data—global loyalty memberships surpassed 6 billion in 2024, illustrating scale for targeted retention. Personalized offers for enrolled customers reduce price elasticity and raise average basket value. Community, tailored service and experiential perks add stickiness beyond price. Benefits must still exceed competitors’ offers to maintain customer bargaining power.

Omnichannel expectations

Omnichannel expectations shift bargaining power toward customers: click-and-collect and real-time inventory transparency are table stakes, and shoppers expect seamless discovery, payment and pickup; global e-commerce hit about 23% of retail sales in 2024, reinforcing channel fluidity. Superior UX raises perceived switching costs and can reduce buyer power, while lagging digital capabilities hand leverage back to customers.

- Real-time inventory: expected norm

- Click-and-collect: conversion driver

- UX: reduces switching

- Poor digital: increases customer leverage

Accessory cross-sell options

Accessory cross-sell faces high customer bargaining power as shoppers compare items across retailers and marketplaces—Amazon held about 38% of US e‑commerce in 2024—making transparent pricing a lever on non‑regulated goods. Proprietary designs, bundled SKUs and exclusive accessories reduce direct comparability, while warranties and post‑sale support lower price sensitivity and raise lifetime value.

- price-transparency: marketplaces ~38% US share

- proprietary-bundles: reduce comparability

- warranty-support: increases retention, lowers price elasticity

Retail density and low switching costs give Canadian cannabis buyers strong leverage

High Tide faces strong buyer power: over 4,000 Canadian cannabis stores by 2024 and ~160 High Tide outlets enable easy switching on price, proximity and assortment. Low switching costs and promo-driven shoppers compress margins; loyalty, exclusive SKUs and superior omnichannel UX are key to regain leverage.

| Metric | 2024 |

|---|---|

| Licensed cannabis stores Canada | 4,000+ |

| High Tide retail locations | ~160 |

| Global e‑commerce share | 23% |

| Amazon US e‑commerce share | 38% |

| Global loyalty memberships | 6B |

What You See Is What You Get

High Tide Porter's Five Forces Analysis

This preview shows the exact High Tide Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable, complete and final.

Description

Don't Miss the Bigger Picture

High Tide's Porter’s Five Forces snapshot highlights strong buyer power, moderate supplier influence, high threat of substitutes from illicit/alternative channels, and barriers that limit new entrants but intensify rivalry among retailers. Strategic pricing, vertical integration and regulatory shifts shape its competitive landscape. This brief teases critical implications—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals and actionable strategy recommendations.

Suppliers Bargaining Power

Provincial wholesalers gatekeep supply

In most Canadian provinces provincial wholesalers centrally set product listings, pricing terms and allocations, concentrating upstream leverage over retailers and squeezing margins for chains like High Tide.

That centralization limits retailers' negotiation scope and forces strict compliance with listing and payment terms, increasing working capital pressure and inventory risk.

High Tide mitigates supplier power by expanding non-cannabis accessories and branded merchandise sales that bypass provincial wholesaler channels.

Licensed producers fragmented yet selective

Although Health Canada listed over 400 licensed producers in 2024, retail shelf space and high-demand SKUs remain limited, concentrating bargaining power among hit brands. Popular LPs frequently secure priority placements and healthier margins, boosting their leverage over retailers. Dependence on blockbuster strains and formats magnifies supplier influence, while multi-sourcing mitigates risk but raises procurement and inventory complexity.

Vertical integration in accessories moderates power

By manufacturing and wholesaling proprietary accessories, High Tide reduces reliance on third-party suppliers, giving it control over design, supply and margins and thereby weakening supplier bargaining; this vertical integration also enables faster innovation cycles and quicker product rollouts. However, 2024 sourcing still depends on imported inputs and overseas manufacturing, leaving the cost base exposed to FX and tariff risks.

Quality, compliance, and recall risks

Input cost volatility and logistics

Glass, metals and packaging costs remain volatile—LME aluminum averaged about $2,300/ton in 2024 and glass-replacement resin prices swung 10–20% year-over-year—while Drewry’s World Container Index averaged roughly $1,800 in 2024, driving landed-cost pressure. Currency swings have inflated accessory landed costs by 5–15% for firms exposed to EM currencies. Freight delays and longer lead times cut in-stock rates and compress promotional windows; longer supplier contracts and nearshoring have reduced procurement volatility by ~30% in observed cases.

- Glass/metals volatility: 10–20% y/y swings

- Freight: Drewry WCI ~ $1,800 (2024)

- Currency impact: landed-cost +5–15%

- Mitigation: longer contracts/nearshoring ~30% volatility reduction

Wholesaler centralization compresses margins; shelf space favors hits despite 400+ producers

Provincial wholesalers centralize listings/pricing, limiting retailer negotiation and compressing margins. Despite 400+ licensed producers in 2024, shelf space concentrates on hit brands, raising supplier leverage. High Tide offsets this via proprietary accessories, nearshoring and longer contracts; 2024 cost drivers: LME aluminum ~2300/ton, Drewry WCI ~1800, FX +5–15%, volatility down ~30% with mitigants.

| Metric | 2024 |

|---|---|

| Licensed producers | 400+ |

| LME aluminum | ~2300/ton |

| Drewry WCI | ~1800 |

| FX impact | +5–15% |

| Volatility reduction | ~30% |

What is included in the product

Tailored Porter’s Five Forces analysis for High Tide that uncovers key drivers of competition, customer influence, supplier power, and market entry risks, identifying disruptive threats and substitutes that challenge market share. Fully editable for use in investor materials, strategic plans, or academic projects.

A concise one-sheet Porter's Five Forces for High Tide that visualizes supplier/buyer power, threats of entry/substitutes and rivalry with an editable radar chart—ready for decks, duplicate for scenarios, swap in your data and requires no macros.

Customers Bargaining Power

Abundant retail choice increases leverage

Urban markets in Canada are dense with cannabis stores, with over 4,000 licensed retail outlets nationwide by 2024. Customers can switch easily based on price, proximity and assortment, often using apps and delivery to compare options. Low switching costs amplify buyer power. Differentiation through membership programs and superior service is essential for High Tide.

Price-sensitive, deal-driven segments

Price-sensitive, deal-driven shoppers conditioned by frequent promotions push High Tide customers toward discounted tiers; with High Tide operating about 160 retail locations by 2024, basket mix in several provinces skews to high-THC/value SKUs, compressing margins and shifting negotiating power to buyers. This dynamic lowers average selling prices and increases promo dependence, while data-driven pricing and SKU-level margin management can preserve contribution.

Loyalty programs temper churn

Robust loyalty programs can lock in repeat purchases and first-party data—global loyalty memberships surpassed 6 billion in 2024, illustrating scale for targeted retention. Personalized offers for enrolled customers reduce price elasticity and raise average basket value. Community, tailored service and experiential perks add stickiness beyond price. Benefits must still exceed competitors’ offers to maintain customer bargaining power.

Omnichannel expectations

Omnichannel expectations shift bargaining power toward customers: click-and-collect and real-time inventory transparency are table stakes, and shoppers expect seamless discovery, payment and pickup; global e-commerce hit about 23% of retail sales in 2024, reinforcing channel fluidity. Superior UX raises perceived switching costs and can reduce buyer power, while lagging digital capabilities hand leverage back to customers.

- Real-time inventory: expected norm

- Click-and-collect: conversion driver

- UX: reduces switching

- Poor digital: increases customer leverage

Accessory cross-sell options

Accessory cross-sell faces high customer bargaining power as shoppers compare items across retailers and marketplaces—Amazon held about 38% of US e‑commerce in 2024—making transparent pricing a lever on non‑regulated goods. Proprietary designs, bundled SKUs and exclusive accessories reduce direct comparability, while warranties and post‑sale support lower price sensitivity and raise lifetime value.

- price-transparency: marketplaces ~38% US share

- proprietary-bundles: reduce comparability

- warranty-support: increases retention, lowers price elasticity

Retail density and low switching costs give Canadian cannabis buyers strong leverage

High Tide faces strong buyer power: over 4,000 Canadian cannabis stores by 2024 and ~160 High Tide outlets enable easy switching on price, proximity and assortment. Low switching costs and promo-driven shoppers compress margins; loyalty, exclusive SKUs and superior omnichannel UX are key to regain leverage.

| Metric | 2024 |

|---|---|

| Licensed cannabis stores Canada | 4,000+ |

| High Tide retail locations | ~160 |

| Global e‑commerce share | 23% |

| Amazon US e‑commerce share | 38% |

| Global loyalty memberships | 6B |

What You See Is What You Get

High Tide Porter's Five Forces Analysis

This preview shows the exact High Tide Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see is the deliverable, complete and final.