Hillenbrand Porter's Five Forces Analysis

From Overview to Strategy Blueprint

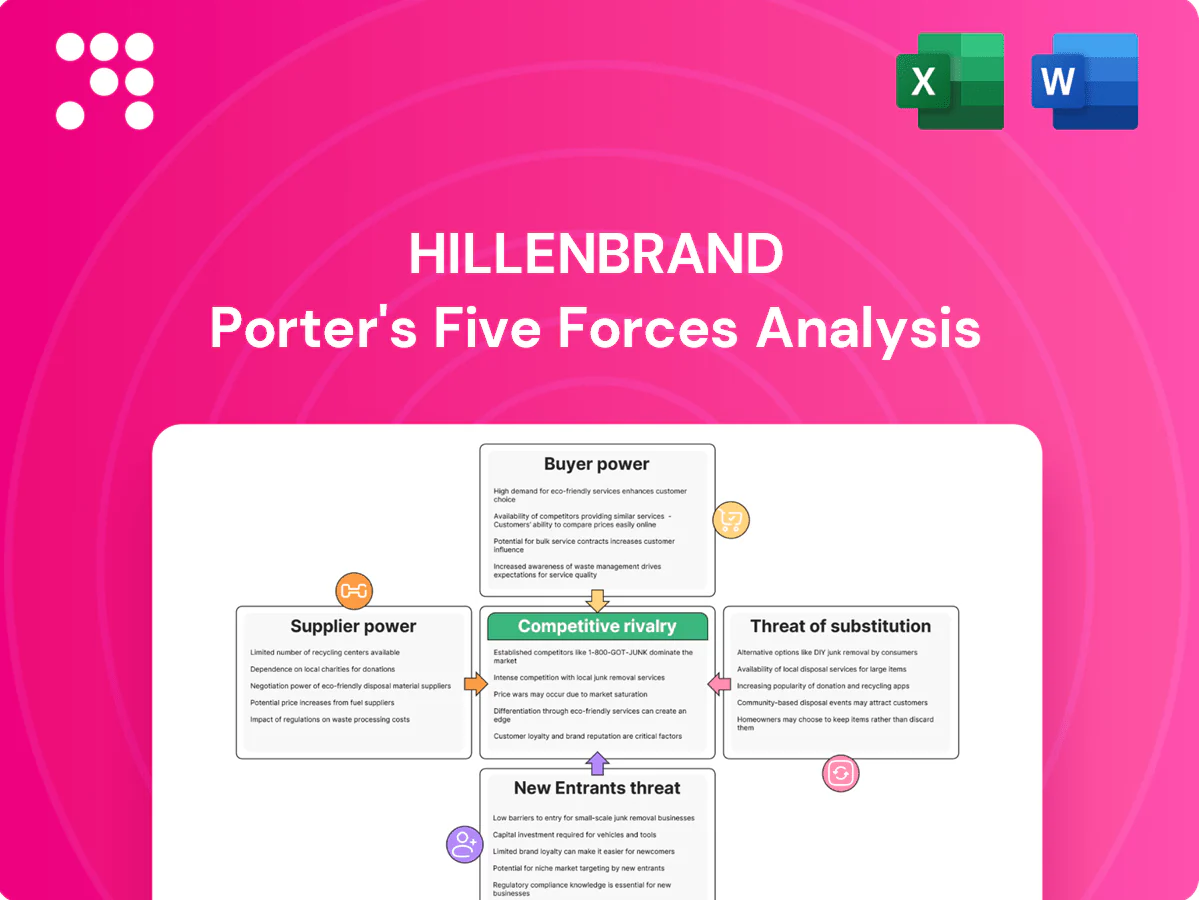

Hillenbrand faces moderate supplier power, differentiated products that limit substitutes, and steady barriers deterring rapid new entrants. Buyer negotiation and industry rivalry shape margins, while regulatory and technological shifts create evolving strategic challenges. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hillenbrand’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components concentration

APS and MTS depend on precision components, controls, high-grade steel and resins with few qualified sources. Concentrated suppliers can impose pricing and lead-time pressure; 2022–24 disruptions pushed specialty control lead times beyond 20 weeks. Dual-sourcing is possible but qualification cycles commonly run 12–24 months, yielding moderate to high supplier leverage in critical categories.

Switching costs and qualification

Engineering specs, regulatory standards, and performance testing raise switching costs for Hillenbrand: supplier requalification typically requires 6–12 months and full documentation. Requalifying a new supplier risks production delays and warranty exposure; safety-critical audits commonly add 3–6 months. These factors compress short-term negotiating flexibility and can increase procurement costs materially.

Long-term and VMI agreements

Framework contracts, VMI and hedging stabilize costs and supply—VMI adoption and contractual hedges helped many manufacturers offset 2024 inflationary pressure (US CPI ~3.4%) and lower logistics cost volatility (global freight rates down ~25% vs 2022). Such arrangements dilute supplier power by smoothing price swings. They can, however, lock in volumes or pricing floors, limiting flexibility. Net effect: balanced supplier power for core inputs.

Global supply chain risk

Hillenbrand exposure across Europe, Asia and the Americas creates currency, logistics and geopolitical risk, with 2024 remaining marked by elevated transport volatility and selective export controls that tighten supply in key segments. Freight spikes and sanctions have periodically increased supplier leverage in tight markets, and diversification/regionalization lower but do not remove systemic risk. Suppliers gain episodic bargaining power during disruptions, forcing premium sourcing and inventory costs.

- 2024: elevated transport volatility and selective export controls

- Regional exposure: currency and geopolitical sensitivity

- Diversification reduces but does not eliminate supplier risk

- Disruptions create episodic supplier pricing power

Technology and IP from suppliers

Controls, drives and automation vendors embed proprietary technology that raises switching costs; in 2024 the global industrial automation market topped about $200 billion, amplifying vendor leverage. When system performance hinges on specific platforms, Hillenbrand’s dependence and supplier bargaining power increase. Co-development deepens integration and creates path lock-in, boosting supplier influence over lifecycle economics and margins.

- Proprietary platforms raise switching costs

- 2024 industrial automation market ~ $200B

- Co-development creates path lock-in

- Supplier influence on lifecycle economics grows

Precision supply tight with >20-week lead times; automation gives episodic leverage

Hillenbrand faces moderate–high supplier power for precision components: critical lead times >20 weeks in 2022–24 and requalification 6–12 months. Framework contracts, VMI and hedges reduced price volatility (US CPI 2024 ~3.4%, freight -25% vs 2022) but can lock volumes. Proprietary automation (global market ~ $200B in 2024) and regional exposure create episodic leverage during disruptions.

| Metric | 2024 Value |

|---|---|

| Control lead times | >20 weeks |

| Requalification | 6–12 months |

| US CPI | ~3.4% |

| Freight vs 2022 | -25% |

| Automation market | ~$200B |

What is included in the product

Concise Porter’s Five Forces assessment of Hillenbrand, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal pricing pressure, margin risks, and strategic levers for sustaining market position.

A tailored Hillenbrand Porter's Five Forces one-sheet that isolates key competitive pressures—relieving decision paralysis by highlighting priority risks and actionable levers (pricing, suppliers, M&A) for fast, board-ready strategy.

Customers Bargaining Power

Large, sophisticated customers

Plastics processors, food producers and industrial OEMs run professional procurement that benchmarks total cost of ownership, uptime (often targeting 95%+ availability) and energy use to the decimal point.

Their scale supports multi-year competitive tenders, commonly 3–5 year contracts, and portfolio-level sourcing that aggregates spend into $M+ bids.

These practices routinely extract 5–15% price and stricter commercial terms, giving large customers pronounced leverage over Hillenbrand suppliers.

Project-based competitive bidding

Project-based RFPs dominate Hillenbrand capital equipment procurement, with comparable specs across rivals driving head-to-head price competition; industry bid data in 2024 showed average tender discounts of roughly 5–12%. Buyers extract concessions through discounting and value-added sweeteners (service contracts, financing, spare parts bundles). During 2024 peak capex pockets, customer leverage increased noticeably, compressing gross margins on awarded projects.

Switching and integration costs

Once installed, Hillenbrand equipment locks into tooling, software and workflows, making replacements costly in downtime, training and revalidation; industry studies (2024) estimate aftermarket services can represent 20–40% of lifecycle revenue, reinforcing ties. Recurring demand for parts and service creates steady annuity streams and raises effective switching costs. This structural stickiness cushions Hillenbrand from pure price pressure.

Customization and performance differentiation

Engineered-to-order systems meet unique throughput, material, or quality needs, turning procurement toward tailored outcomes; performance guarantees therefore shift buyer focus from upfront price to measurable results, narrowing comparable alternatives. Buyer power moderates when specifications are proprietary or IP-encumbered, making switching costly and reducing price sensitivity.

- Customization reduces comparable vendors

- Performance guarantees favor outcome-based buying

- Proprietary specs lower buyer leverage

Aftermarket and lifecycle services

Aftermarket parts, retrofits, and digital monitoring create strong customer stickiness for Hillenbrand, shifting value toward lifecycle services and reducing buyers’ negotiating leverage. Predictive maintenance—McKinsey finds it can cut unplanned downtime roughly 40% and lower maintenance costs—raises perceived value and willingness to accept higher service pricing. Bundled service contracts materially lower churn, turning one-off buyers into recurring-revenue customers and shrinking buyer bargaining over time.

- stickiness: parts, retrofits, digital monitoring

- value: predictive maintenance ~40% less downtime (McKinsey)

- retention: bundled contracts reduce churn, raise recurring revenue

Processors win 3-5 year tenders, gain 5-12% discounts and aftermarket leverage

Large processors run professional procurement, securing 3–5 year tenders and extracting 5–12% average discounts in 2024, giving pronounced price leverage. Aftermarket services (20–40% lifecycle revenue) and high switching costs from tooling/software reduce buyer power. Performance guarantees and proprietary specs further moderate price sensitivity.

| Metric | 2024 Value |

|---|---|

| Average tender discount | 5–12% |

| Contract length | 3–5 years |

| Aftermarket share | 20–40% |

| Downtime cut (predictive maintenance) | ~40% |

Preview the Actual Deliverable

Hillenbrand Porter's Five Forces Analysis

This preview shows the exact Hillenbrand Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final deliverable as displayed here, available instantly upon payment.

From Overview to Strategy Blueprint

Hillenbrand faces moderate supplier power, differentiated products that limit substitutes, and steady barriers deterring rapid new entrants. Buyer negotiation and industry rivalry shape margins, while regulatory and technological shifts create evolving strategic challenges. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hillenbrand’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components concentration

APS and MTS depend on precision components, controls, high-grade steel and resins with few qualified sources. Concentrated suppliers can impose pricing and lead-time pressure; 2022–24 disruptions pushed specialty control lead times beyond 20 weeks. Dual-sourcing is possible but qualification cycles commonly run 12–24 months, yielding moderate to high supplier leverage in critical categories.

Switching costs and qualification

Engineering specs, regulatory standards, and performance testing raise switching costs for Hillenbrand: supplier requalification typically requires 6–12 months and full documentation. Requalifying a new supplier risks production delays and warranty exposure; safety-critical audits commonly add 3–6 months. These factors compress short-term negotiating flexibility and can increase procurement costs materially.

Long-term and VMI agreements

Framework contracts, VMI and hedging stabilize costs and supply—VMI adoption and contractual hedges helped many manufacturers offset 2024 inflationary pressure (US CPI ~3.4%) and lower logistics cost volatility (global freight rates down ~25% vs 2022). Such arrangements dilute supplier power by smoothing price swings. They can, however, lock in volumes or pricing floors, limiting flexibility. Net effect: balanced supplier power for core inputs.

Global supply chain risk

Hillenbrand exposure across Europe, Asia and the Americas creates currency, logistics and geopolitical risk, with 2024 remaining marked by elevated transport volatility and selective export controls that tighten supply in key segments. Freight spikes and sanctions have periodically increased supplier leverage in tight markets, and diversification/regionalization lower but do not remove systemic risk. Suppliers gain episodic bargaining power during disruptions, forcing premium sourcing and inventory costs.

- 2024: elevated transport volatility and selective export controls

- Regional exposure: currency and geopolitical sensitivity

- Diversification reduces but does not eliminate supplier risk

- Disruptions create episodic supplier pricing power

Technology and IP from suppliers

Controls, drives and automation vendors embed proprietary technology that raises switching costs; in 2024 the global industrial automation market topped about $200 billion, amplifying vendor leverage. When system performance hinges on specific platforms, Hillenbrand’s dependence and supplier bargaining power increase. Co-development deepens integration and creates path lock-in, boosting supplier influence over lifecycle economics and margins.

- Proprietary platforms raise switching costs

- 2024 industrial automation market ~ $200B

- Co-development creates path lock-in

- Supplier influence on lifecycle economics grows

Precision supply tight with >20-week lead times; automation gives episodic leverage

Hillenbrand faces moderate–high supplier power for precision components: critical lead times >20 weeks in 2022–24 and requalification 6–12 months. Framework contracts, VMI and hedges reduced price volatility (US CPI 2024 ~3.4%, freight -25% vs 2022) but can lock volumes. Proprietary automation (global market ~ $200B in 2024) and regional exposure create episodic leverage during disruptions.

| Metric | 2024 Value |

|---|---|

| Control lead times | >20 weeks |

| Requalification | 6–12 months |

| US CPI | ~3.4% |

| Freight vs 2022 | -25% |

| Automation market | ~$200B |

What is included in the product

Concise Porter’s Five Forces assessment of Hillenbrand, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal pricing pressure, margin risks, and strategic levers for sustaining market position.

A tailored Hillenbrand Porter's Five Forces one-sheet that isolates key competitive pressures—relieving decision paralysis by highlighting priority risks and actionable levers (pricing, suppliers, M&A) for fast, board-ready strategy.

Customers Bargaining Power

Large, sophisticated customers

Plastics processors, food producers and industrial OEMs run professional procurement that benchmarks total cost of ownership, uptime (often targeting 95%+ availability) and energy use to the decimal point.

Their scale supports multi-year competitive tenders, commonly 3–5 year contracts, and portfolio-level sourcing that aggregates spend into $M+ bids.

These practices routinely extract 5–15% price and stricter commercial terms, giving large customers pronounced leverage over Hillenbrand suppliers.

Project-based competitive bidding

Project-based RFPs dominate Hillenbrand capital equipment procurement, with comparable specs across rivals driving head-to-head price competition; industry bid data in 2024 showed average tender discounts of roughly 5–12%. Buyers extract concessions through discounting and value-added sweeteners (service contracts, financing, spare parts bundles). During 2024 peak capex pockets, customer leverage increased noticeably, compressing gross margins on awarded projects.

Switching and integration costs

Once installed, Hillenbrand equipment locks into tooling, software and workflows, making replacements costly in downtime, training and revalidation; industry studies (2024) estimate aftermarket services can represent 20–40% of lifecycle revenue, reinforcing ties. Recurring demand for parts and service creates steady annuity streams and raises effective switching costs. This structural stickiness cushions Hillenbrand from pure price pressure.

Customization and performance differentiation

Engineered-to-order systems meet unique throughput, material, or quality needs, turning procurement toward tailored outcomes; performance guarantees therefore shift buyer focus from upfront price to measurable results, narrowing comparable alternatives. Buyer power moderates when specifications are proprietary or IP-encumbered, making switching costly and reducing price sensitivity.

- Customization reduces comparable vendors

- Performance guarantees favor outcome-based buying

- Proprietary specs lower buyer leverage

Aftermarket and lifecycle services

Aftermarket parts, retrofits, and digital monitoring create strong customer stickiness for Hillenbrand, shifting value toward lifecycle services and reducing buyers’ negotiating leverage. Predictive maintenance—McKinsey finds it can cut unplanned downtime roughly 40% and lower maintenance costs—raises perceived value and willingness to accept higher service pricing. Bundled service contracts materially lower churn, turning one-off buyers into recurring-revenue customers and shrinking buyer bargaining over time.

- stickiness: parts, retrofits, digital monitoring

- value: predictive maintenance ~40% less downtime (McKinsey)

- retention: bundled contracts reduce churn, raise recurring revenue

Processors win 3-5 year tenders, gain 5-12% discounts and aftermarket leverage

Large processors run professional procurement, securing 3–5 year tenders and extracting 5–12% average discounts in 2024, giving pronounced price leverage. Aftermarket services (20–40% lifecycle revenue) and high switching costs from tooling/software reduce buyer power. Performance guarantees and proprietary specs further moderate price sensitivity.

| Metric | 2024 Value |

|---|---|

| Average tender discount | 5–12% |

| Contract length | 3–5 years |

| Aftermarket share | 20–40% |

| Downtime cut (predictive maintenance) | ~40% |

Preview the Actual Deliverable

Hillenbrand Porter's Five Forces Analysis

This preview shows the exact Hillenbrand Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final deliverable as displayed here, available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Hillenbrand faces moderate supplier power, differentiated products that limit substitutes, and steady barriers deterring rapid new entrants. Buyer negotiation and industry rivalry shape margins, while regulatory and technological shifts create evolving strategic challenges. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hillenbrand’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components concentration

APS and MTS depend on precision components, controls, high-grade steel and resins with few qualified sources. Concentrated suppliers can impose pricing and lead-time pressure; 2022–24 disruptions pushed specialty control lead times beyond 20 weeks. Dual-sourcing is possible but qualification cycles commonly run 12–24 months, yielding moderate to high supplier leverage in critical categories.

Switching costs and qualification

Engineering specs, regulatory standards, and performance testing raise switching costs for Hillenbrand: supplier requalification typically requires 6–12 months and full documentation. Requalifying a new supplier risks production delays and warranty exposure; safety-critical audits commonly add 3–6 months. These factors compress short-term negotiating flexibility and can increase procurement costs materially.

Long-term and VMI agreements

Framework contracts, VMI and hedging stabilize costs and supply—VMI adoption and contractual hedges helped many manufacturers offset 2024 inflationary pressure (US CPI ~3.4%) and lower logistics cost volatility (global freight rates down ~25% vs 2022). Such arrangements dilute supplier power by smoothing price swings. They can, however, lock in volumes or pricing floors, limiting flexibility. Net effect: balanced supplier power for core inputs.

Global supply chain risk

Hillenbrand exposure across Europe, Asia and the Americas creates currency, logistics and geopolitical risk, with 2024 remaining marked by elevated transport volatility and selective export controls that tighten supply in key segments. Freight spikes and sanctions have periodically increased supplier leverage in tight markets, and diversification/regionalization lower but do not remove systemic risk. Suppliers gain episodic bargaining power during disruptions, forcing premium sourcing and inventory costs.

- 2024: elevated transport volatility and selective export controls

- Regional exposure: currency and geopolitical sensitivity

- Diversification reduces but does not eliminate supplier risk

- Disruptions create episodic supplier pricing power

Technology and IP from suppliers

Controls, drives and automation vendors embed proprietary technology that raises switching costs; in 2024 the global industrial automation market topped about $200 billion, amplifying vendor leverage. When system performance hinges on specific platforms, Hillenbrand’s dependence and supplier bargaining power increase. Co-development deepens integration and creates path lock-in, boosting supplier influence over lifecycle economics and margins.

- Proprietary platforms raise switching costs

- 2024 industrial automation market ~ $200B

- Co-development creates path lock-in

- Supplier influence on lifecycle economics grows

Precision supply tight with >20-week lead times; automation gives episodic leverage

Hillenbrand faces moderate–high supplier power for precision components: critical lead times >20 weeks in 2022–24 and requalification 6–12 months. Framework contracts, VMI and hedges reduced price volatility (US CPI 2024 ~3.4%, freight -25% vs 2022) but can lock volumes. Proprietary automation (global market ~ $200B in 2024) and regional exposure create episodic leverage during disruptions.

| Metric | 2024 Value |

|---|---|

| Control lead times | >20 weeks |

| Requalification | 6–12 months |

| US CPI | ~3.4% |

| Freight vs 2022 | -25% |

| Automation market | ~$200B |

What is included in the product

Concise Porter’s Five Forces assessment of Hillenbrand, examining competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers to reveal pricing pressure, margin risks, and strategic levers for sustaining market position.

A tailored Hillenbrand Porter's Five Forces one-sheet that isolates key competitive pressures—relieving decision paralysis by highlighting priority risks and actionable levers (pricing, suppliers, M&A) for fast, board-ready strategy.

Customers Bargaining Power

Large, sophisticated customers

Plastics processors, food producers and industrial OEMs run professional procurement that benchmarks total cost of ownership, uptime (often targeting 95%+ availability) and energy use to the decimal point.

Their scale supports multi-year competitive tenders, commonly 3–5 year contracts, and portfolio-level sourcing that aggregates spend into $M+ bids.

These practices routinely extract 5–15% price and stricter commercial terms, giving large customers pronounced leverage over Hillenbrand suppliers.

Project-based competitive bidding

Project-based RFPs dominate Hillenbrand capital equipment procurement, with comparable specs across rivals driving head-to-head price competition; industry bid data in 2024 showed average tender discounts of roughly 5–12%. Buyers extract concessions through discounting and value-added sweeteners (service contracts, financing, spare parts bundles). During 2024 peak capex pockets, customer leverage increased noticeably, compressing gross margins on awarded projects.

Switching and integration costs

Once installed, Hillenbrand equipment locks into tooling, software and workflows, making replacements costly in downtime, training and revalidation; industry studies (2024) estimate aftermarket services can represent 20–40% of lifecycle revenue, reinforcing ties. Recurring demand for parts and service creates steady annuity streams and raises effective switching costs. This structural stickiness cushions Hillenbrand from pure price pressure.

Customization and performance differentiation

Engineered-to-order systems meet unique throughput, material, or quality needs, turning procurement toward tailored outcomes; performance guarantees therefore shift buyer focus from upfront price to measurable results, narrowing comparable alternatives. Buyer power moderates when specifications are proprietary or IP-encumbered, making switching costly and reducing price sensitivity.

- Customization reduces comparable vendors

- Performance guarantees favor outcome-based buying

- Proprietary specs lower buyer leverage

Aftermarket and lifecycle services

Aftermarket parts, retrofits, and digital monitoring create strong customer stickiness for Hillenbrand, shifting value toward lifecycle services and reducing buyers’ negotiating leverage. Predictive maintenance—McKinsey finds it can cut unplanned downtime roughly 40% and lower maintenance costs—raises perceived value and willingness to accept higher service pricing. Bundled service contracts materially lower churn, turning one-off buyers into recurring-revenue customers and shrinking buyer bargaining over time.

- stickiness: parts, retrofits, digital monitoring

- value: predictive maintenance ~40% less downtime (McKinsey)

- retention: bundled contracts reduce churn, raise recurring revenue

Processors win 3-5 year tenders, gain 5-12% discounts and aftermarket leverage

Large processors run professional procurement, securing 3–5 year tenders and extracting 5–12% average discounts in 2024, giving pronounced price leverage. Aftermarket services (20–40% lifecycle revenue) and high switching costs from tooling/software reduce buyer power. Performance guarantees and proprietary specs further moderate price sensitivity.

| Metric | 2024 Value |

|---|---|

| Average tender discount | 5–12% |

| Contract length | 3–5 years |

| Aftermarket share | 20–40% |

| Downtime cut (predictive maintenance) | ~40% |

Preview the Actual Deliverable

Hillenbrand Porter's Five Forces Analysis

This preview shows the exact Hillenbrand Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're getting the final deliverable as displayed here, available instantly upon payment.