Hillenbrand SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Hillenbrand’s SWOT highlights a resilient industrial platform with diversified end markets, cost-efficiency drivers, and acquisition-fueled growth, alongside exposure to cyclical demand and integration risks. Want the full picture—purchase the complete SWOT to access a research-backed, editable Word and Excel package with strategic recommendations and financial context.

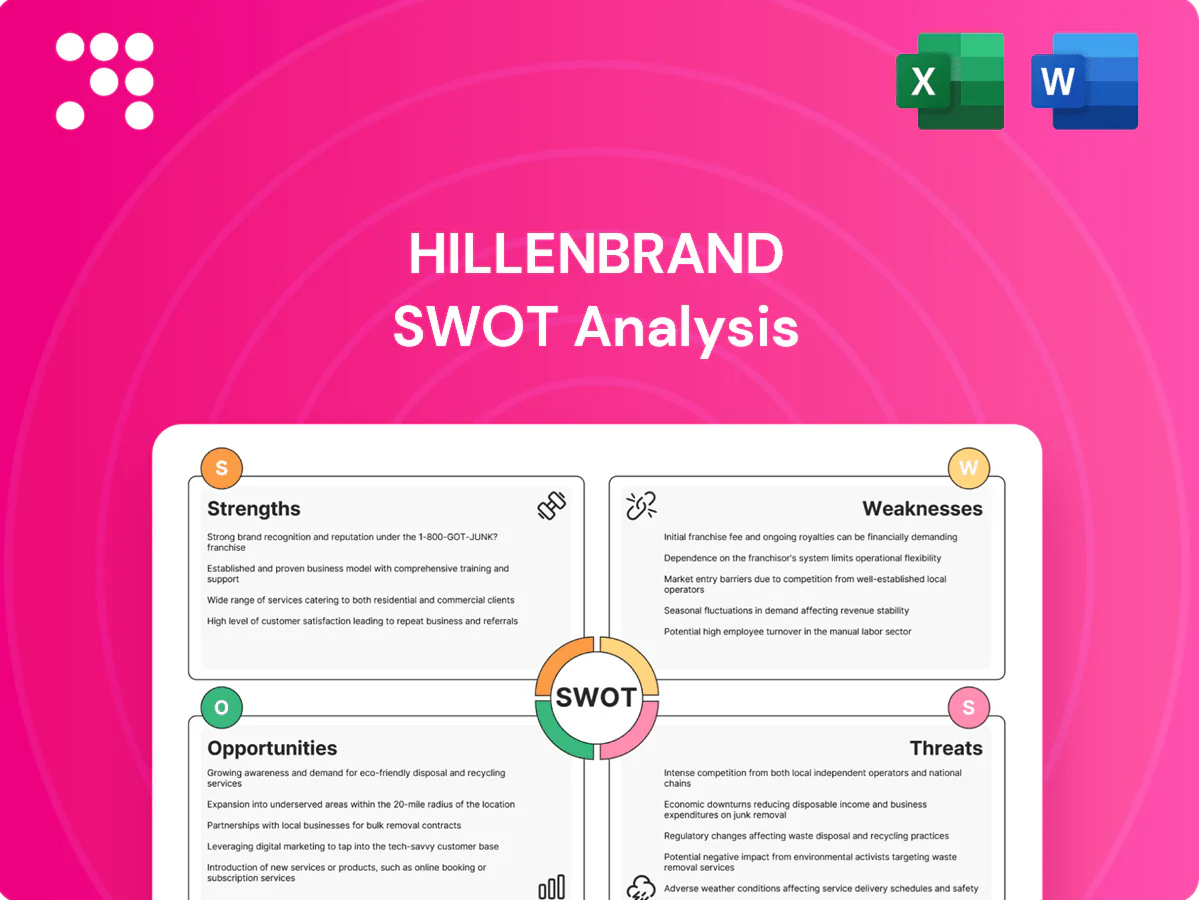

Strengths

Diversified industrial portfolio

Operating through APS and MTS balances exposure across plastics processing, food and broader industrial end-markets, with Hillenbrand reporting $2.8B revenue in FY2024. This mix smooths revenue volatility when one sector slows and enables cross-selling of solutions and best-practice transfer between segments. Diversification enhances resilience and strengthens bargaining power with suppliers and customers.

Deep engineered solutions expertise

Deep engineered-solutions expertise at Hillenbrand (NYSE: HI) — founded 1906 — creates high switching costs through design, integration, and service of complex process equipment. Customers prioritize performance, uptime, and regulatory compliance, favoring proven engineering partners. This know-how enables premium pricing and differentiation and drives lifecycle value via upgrades and optimization.

Large installed base and aftermarket

Hillenbrand’s large installed base generates recurring parts, service and retrofit revenue that stabilizes cash flow—FY2024 sales totaled approximately $2.3 billion, with aftermarket contributing a meaningful, higher-margin mix.

Close aftermarket intimacy strengthens customer relationships and feeds product roadmaps via service feedback and usage data.

Regular service touchpoints enable upsell of upgrades and digital monitoring, while high-margin aftermarket cash supports reinvestment and M&A.

Global footprint and customer proximity

Hillenbrand's presence across key industrial regions enables faster delivery and localized support, reducing lead times and enabling application-specific engineering, supporting its participation in multinational capex programs; Hillenbrand reported roughly $2.1 billion revenue in fiscal 2024, reflecting broad geographic diversification that helps mitigate geopolitical and currency risks.

- Faster delivery/local support

- Shorter lead times, tailored engineering

- Geographic diversification of risks

- Access to multinational capex

Innovation focused on productivity

Hillenbrand's innovation focus—R&D geared to throughput, energy efficiency and precision—directly boosts customer ROI and supported company revenue of about $2.6B in FY2024, helping drive higher-margin aftermarket sales.

Advanced controls and automation differentiate offerings, continuous product upgrades align with tightening sustainability and regulatory standards, and this tech moat shields share from low-cost competitors.

- R&D: throughput, energy, precision

- Differentiator: controls & automation

- Compliance: sustainability/regulatory readiness

- Defensive: protects vs low-cost rivals

Engineered solutions and installed base drive recurring high-margin aftermarket revenue

Hillenbrand (FY2024) reported $2.8B revenue, with APS and MTS diversifying exposure across plastics, food and industrial markets and enabling cross-selling. Deep engineered-solutions expertise creates high switching costs and supports premium pricing and lifecycle upgrades. A large installed base generates recurring, higher-margin aftermarket revenue and stable cash flow, funding R&D and M&A.

| Metric | Value/Note |

|---|---|

| Total revenue (FY2024) | $2.8B |

| Aftermarket sales (FY2024) | ~$2.3B (company disclosure) |

| Competitive edge | Engineered solutions, installed base, R&D |

What is included in the product

Provides a concise SWOT analysis of Hillenbrand, highlighting internal strengths and weaknesses alongside external opportunities and threats to evaluate its strategic position, growth drivers, and potential risks.

Provides a focused Hillenbrand SWOT matrix for rapid identification and resolution of strategic pain points, enabling teams to align actions to strengths, address weaknesses, and prioritize opportunities for faster decision-making.

Weaknesses

End-market cyclicality

End-market cyclicality: capital equipment demand in Hillenbrand's plastics and industrial end-markets tracks macro cycles, and FY2024 revenue of about $1.8 billion highlighted sensitivity to order timing. Order timing and backlog visibility can be uneven, with quarter-to-quarter swings in bookings. Downturns pressure utilization and approvals, compressing margins and delaying cash conversion.

High capital intensity

Hillenbrand’s custom engineering and complex manufacturing drive high capital intensity, tying up working capital and stretching lead times against $2.1B revenue in fiscal 2024 and approximately $80M capex in 2024.

Cost overruns or delays can quickly erode its ~23% gross margin, while swings in capacity utilization worsen fixed-cost absorption.

Large, ongoing investment needs may constrain flexibility during prolonged downturns.

Exposure to plastics scrutiny

Public and regulatory pressure on plastics can depress demand for certain Hillenbrand applications, with customers delaying projects pending material transitions; Hillenbrand reported approximately $2.7 billion in revenue in FY2024, exposing a material share to plastics markets. Compliance and extended producer responsibility rules raise costs and operational complexity. Portfolio repositioning may be required to meet circularity targets and customer timelines.

Integration and focus risks from M&A

Acquisitions drive Hillenbrand's growth but introduce integration, cultural and synergy risks that can erode expected returns and operational focus.

Deal execution can distract R&D and customer responsiveness, while overpaying or misjudging market fit risks value destruction.

Systems and supply-chain harmonization often take longer than planned, increasing short-term costs and complexity.

- Integration risk

- R&D distraction

- Overpayment risk

- Supply-chain delays

Customer concentration in key niches

Hillenbrand's specialized equipment often targets a limited set of large strategic accounts, and the company's 2024 Form 10-K explicitly cites customer concentration risk. Loss or delay of a few major projects can materially impact quarterly results, while sophisticated buyers drive intense pricing negotiations and margin pressure. Dependence on key verticals increases exposure to sector-specific downturns and project timing volatility.

- Customer concentration risk (10-K disclosure)

- High project timing sensitivity

- Pressure from sophisticated buyers

- Exposure to vertical-specific cycles

Cyclic revenue, concentrated customers and high capex amplify quarter-to-quarter margin risk

Hillenbrand's revenue cyclicality and customer concentration create quarter-to-quarter volatility; FY2024 revenue was about $2.7B with ~23% gross margin and ~$80M capex, exposing sensitivity to order timing, utilization and plastics end-market shifts. High capital intensity and frequent acquisitions raise integration, capex and working-capital strain, increasing execution and margin risk.

| Metric | FY2024 |

|---|---|

| Revenue | $2.7B |

| Gross margin | ~23% |

| Capex | $80M |

| Customer concentration | 10-K disclosed |

What You See Is What You Get

Hillenbrand SWOT Analysis

This Hillenbrand SWOT analysis provides concise, actionable insights into strengths, weaknesses, opportunities and threats to support strategic decision-making. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable document with full sourcing and recommendations.

Make Insightful Decisions Backed by Expert Research

Hillenbrand’s SWOT highlights a resilient industrial platform with diversified end markets, cost-efficiency drivers, and acquisition-fueled growth, alongside exposure to cyclical demand and integration risks. Want the full picture—purchase the complete SWOT to access a research-backed, editable Word and Excel package with strategic recommendations and financial context.

Strengths

Diversified industrial portfolio

Operating through APS and MTS balances exposure across plastics processing, food and broader industrial end-markets, with Hillenbrand reporting $2.8B revenue in FY2024. This mix smooths revenue volatility when one sector slows and enables cross-selling of solutions and best-practice transfer between segments. Diversification enhances resilience and strengthens bargaining power with suppliers and customers.

Deep engineered solutions expertise

Deep engineered-solutions expertise at Hillenbrand (NYSE: HI) — founded 1906 — creates high switching costs through design, integration, and service of complex process equipment. Customers prioritize performance, uptime, and regulatory compliance, favoring proven engineering partners. This know-how enables premium pricing and differentiation and drives lifecycle value via upgrades and optimization.

Large installed base and aftermarket

Hillenbrand’s large installed base generates recurring parts, service and retrofit revenue that stabilizes cash flow—FY2024 sales totaled approximately $2.3 billion, with aftermarket contributing a meaningful, higher-margin mix.

Close aftermarket intimacy strengthens customer relationships and feeds product roadmaps via service feedback and usage data.

Regular service touchpoints enable upsell of upgrades and digital monitoring, while high-margin aftermarket cash supports reinvestment and M&A.

Global footprint and customer proximity

Hillenbrand's presence across key industrial regions enables faster delivery and localized support, reducing lead times and enabling application-specific engineering, supporting its participation in multinational capex programs; Hillenbrand reported roughly $2.1 billion revenue in fiscal 2024, reflecting broad geographic diversification that helps mitigate geopolitical and currency risks.

- Faster delivery/local support

- Shorter lead times, tailored engineering

- Geographic diversification of risks

- Access to multinational capex

Innovation focused on productivity

Hillenbrand's innovation focus—R&D geared to throughput, energy efficiency and precision—directly boosts customer ROI and supported company revenue of about $2.6B in FY2024, helping drive higher-margin aftermarket sales.

Advanced controls and automation differentiate offerings, continuous product upgrades align with tightening sustainability and regulatory standards, and this tech moat shields share from low-cost competitors.

- R&D: throughput, energy, precision

- Differentiator: controls & automation

- Compliance: sustainability/regulatory readiness

- Defensive: protects vs low-cost rivals

Engineered solutions and installed base drive recurring high-margin aftermarket revenue

Hillenbrand (FY2024) reported $2.8B revenue, with APS and MTS diversifying exposure across plastics, food and industrial markets and enabling cross-selling. Deep engineered-solutions expertise creates high switching costs and supports premium pricing and lifecycle upgrades. A large installed base generates recurring, higher-margin aftermarket revenue and stable cash flow, funding R&D and M&A.

| Metric | Value/Note |

|---|---|

| Total revenue (FY2024) | $2.8B |

| Aftermarket sales (FY2024) | ~$2.3B (company disclosure) |

| Competitive edge | Engineered solutions, installed base, R&D |

What is included in the product

Provides a concise SWOT analysis of Hillenbrand, highlighting internal strengths and weaknesses alongside external opportunities and threats to evaluate its strategic position, growth drivers, and potential risks.

Provides a focused Hillenbrand SWOT matrix for rapid identification and resolution of strategic pain points, enabling teams to align actions to strengths, address weaknesses, and prioritize opportunities for faster decision-making.

Weaknesses

End-market cyclicality

End-market cyclicality: capital equipment demand in Hillenbrand's plastics and industrial end-markets tracks macro cycles, and FY2024 revenue of about $1.8 billion highlighted sensitivity to order timing. Order timing and backlog visibility can be uneven, with quarter-to-quarter swings in bookings. Downturns pressure utilization and approvals, compressing margins and delaying cash conversion.

High capital intensity

Hillenbrand’s custom engineering and complex manufacturing drive high capital intensity, tying up working capital and stretching lead times against $2.1B revenue in fiscal 2024 and approximately $80M capex in 2024.

Cost overruns or delays can quickly erode its ~23% gross margin, while swings in capacity utilization worsen fixed-cost absorption.

Large, ongoing investment needs may constrain flexibility during prolonged downturns.

Exposure to plastics scrutiny

Public and regulatory pressure on plastics can depress demand for certain Hillenbrand applications, with customers delaying projects pending material transitions; Hillenbrand reported approximately $2.7 billion in revenue in FY2024, exposing a material share to plastics markets. Compliance and extended producer responsibility rules raise costs and operational complexity. Portfolio repositioning may be required to meet circularity targets and customer timelines.

Integration and focus risks from M&A

Acquisitions drive Hillenbrand's growth but introduce integration, cultural and synergy risks that can erode expected returns and operational focus.

Deal execution can distract R&D and customer responsiveness, while overpaying or misjudging market fit risks value destruction.

Systems and supply-chain harmonization often take longer than planned, increasing short-term costs and complexity.

- Integration risk

- R&D distraction

- Overpayment risk

- Supply-chain delays

Customer concentration in key niches

Hillenbrand's specialized equipment often targets a limited set of large strategic accounts, and the company's 2024 Form 10-K explicitly cites customer concentration risk. Loss or delay of a few major projects can materially impact quarterly results, while sophisticated buyers drive intense pricing negotiations and margin pressure. Dependence on key verticals increases exposure to sector-specific downturns and project timing volatility.

- Customer concentration risk (10-K disclosure)

- High project timing sensitivity

- Pressure from sophisticated buyers

- Exposure to vertical-specific cycles

Cyclic revenue, concentrated customers and high capex amplify quarter-to-quarter margin risk

Hillenbrand's revenue cyclicality and customer concentration create quarter-to-quarter volatility; FY2024 revenue was about $2.7B with ~23% gross margin and ~$80M capex, exposing sensitivity to order timing, utilization and plastics end-market shifts. High capital intensity and frequent acquisitions raise integration, capex and working-capital strain, increasing execution and margin risk.

| Metric | FY2024 |

|---|---|

| Revenue | $2.7B |

| Gross margin | ~23% |

| Capex | $80M |

| Customer concentration | 10-K disclosed |

What You See Is What You Get

Hillenbrand SWOT Analysis

This Hillenbrand SWOT analysis provides concise, actionable insights into strengths, weaknesses, opportunities and threats to support strategic decision-making. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable document with full sourcing and recommendations.

Description

Make Insightful Decisions Backed by Expert Research

Hillenbrand’s SWOT highlights a resilient industrial platform with diversified end markets, cost-efficiency drivers, and acquisition-fueled growth, alongside exposure to cyclical demand and integration risks. Want the full picture—purchase the complete SWOT to access a research-backed, editable Word and Excel package with strategic recommendations and financial context.

Strengths

Diversified industrial portfolio

Operating through APS and MTS balances exposure across plastics processing, food and broader industrial end-markets, with Hillenbrand reporting $2.8B revenue in FY2024. This mix smooths revenue volatility when one sector slows and enables cross-selling of solutions and best-practice transfer between segments. Diversification enhances resilience and strengthens bargaining power with suppliers and customers.

Deep engineered solutions expertise

Deep engineered-solutions expertise at Hillenbrand (NYSE: HI) — founded 1906 — creates high switching costs through design, integration, and service of complex process equipment. Customers prioritize performance, uptime, and regulatory compliance, favoring proven engineering partners. This know-how enables premium pricing and differentiation and drives lifecycle value via upgrades and optimization.

Large installed base and aftermarket

Hillenbrand’s large installed base generates recurring parts, service and retrofit revenue that stabilizes cash flow—FY2024 sales totaled approximately $2.3 billion, with aftermarket contributing a meaningful, higher-margin mix.

Close aftermarket intimacy strengthens customer relationships and feeds product roadmaps via service feedback and usage data.

Regular service touchpoints enable upsell of upgrades and digital monitoring, while high-margin aftermarket cash supports reinvestment and M&A.

Global footprint and customer proximity

Hillenbrand's presence across key industrial regions enables faster delivery and localized support, reducing lead times and enabling application-specific engineering, supporting its participation in multinational capex programs; Hillenbrand reported roughly $2.1 billion revenue in fiscal 2024, reflecting broad geographic diversification that helps mitigate geopolitical and currency risks.

- Faster delivery/local support

- Shorter lead times, tailored engineering

- Geographic diversification of risks

- Access to multinational capex

Innovation focused on productivity

Hillenbrand's innovation focus—R&D geared to throughput, energy efficiency and precision—directly boosts customer ROI and supported company revenue of about $2.6B in FY2024, helping drive higher-margin aftermarket sales.

Advanced controls and automation differentiate offerings, continuous product upgrades align with tightening sustainability and regulatory standards, and this tech moat shields share from low-cost competitors.

- R&D: throughput, energy, precision

- Differentiator: controls & automation

- Compliance: sustainability/regulatory readiness

- Defensive: protects vs low-cost rivals

Engineered solutions and installed base drive recurring high-margin aftermarket revenue

Hillenbrand (FY2024) reported $2.8B revenue, with APS and MTS diversifying exposure across plastics, food and industrial markets and enabling cross-selling. Deep engineered-solutions expertise creates high switching costs and supports premium pricing and lifecycle upgrades. A large installed base generates recurring, higher-margin aftermarket revenue and stable cash flow, funding R&D and M&A.

| Metric | Value/Note |

|---|---|

| Total revenue (FY2024) | $2.8B |

| Aftermarket sales (FY2024) | ~$2.3B (company disclosure) |

| Competitive edge | Engineered solutions, installed base, R&D |

What is included in the product

Provides a concise SWOT analysis of Hillenbrand, highlighting internal strengths and weaknesses alongside external opportunities and threats to evaluate its strategic position, growth drivers, and potential risks.

Provides a focused Hillenbrand SWOT matrix for rapid identification and resolution of strategic pain points, enabling teams to align actions to strengths, address weaknesses, and prioritize opportunities for faster decision-making.

Weaknesses

End-market cyclicality

End-market cyclicality: capital equipment demand in Hillenbrand's plastics and industrial end-markets tracks macro cycles, and FY2024 revenue of about $1.8 billion highlighted sensitivity to order timing. Order timing and backlog visibility can be uneven, with quarter-to-quarter swings in bookings. Downturns pressure utilization and approvals, compressing margins and delaying cash conversion.

High capital intensity

Hillenbrand’s custom engineering and complex manufacturing drive high capital intensity, tying up working capital and stretching lead times against $2.1B revenue in fiscal 2024 and approximately $80M capex in 2024.

Cost overruns or delays can quickly erode its ~23% gross margin, while swings in capacity utilization worsen fixed-cost absorption.

Large, ongoing investment needs may constrain flexibility during prolonged downturns.

Exposure to plastics scrutiny

Public and regulatory pressure on plastics can depress demand for certain Hillenbrand applications, with customers delaying projects pending material transitions; Hillenbrand reported approximately $2.7 billion in revenue in FY2024, exposing a material share to plastics markets. Compliance and extended producer responsibility rules raise costs and operational complexity. Portfolio repositioning may be required to meet circularity targets and customer timelines.

Integration and focus risks from M&A

Acquisitions drive Hillenbrand's growth but introduce integration, cultural and synergy risks that can erode expected returns and operational focus.

Deal execution can distract R&D and customer responsiveness, while overpaying or misjudging market fit risks value destruction.

Systems and supply-chain harmonization often take longer than planned, increasing short-term costs and complexity.

- Integration risk

- R&D distraction

- Overpayment risk

- Supply-chain delays

Customer concentration in key niches

Hillenbrand's specialized equipment often targets a limited set of large strategic accounts, and the company's 2024 Form 10-K explicitly cites customer concentration risk. Loss or delay of a few major projects can materially impact quarterly results, while sophisticated buyers drive intense pricing negotiations and margin pressure. Dependence on key verticals increases exposure to sector-specific downturns and project timing volatility.

- Customer concentration risk (10-K disclosure)

- High project timing sensitivity

- Pressure from sophisticated buyers

- Exposure to vertical-specific cycles

Cyclic revenue, concentrated customers and high capex amplify quarter-to-quarter margin risk

Hillenbrand's revenue cyclicality and customer concentration create quarter-to-quarter volatility; FY2024 revenue was about $2.7B with ~23% gross margin and ~$80M capex, exposing sensitivity to order timing, utilization and plastics end-market shifts. High capital intensity and frequent acquisitions raise integration, capex and working-capital strain, increasing execution and margin risk.

| Metric | FY2024 |

|---|---|

| Revenue | $2.7B |

| Gross margin | ~23% |

| Capex | $80M |

| Customer concentration | 10-K disclosed |

What You See Is What You Get

Hillenbrand SWOT Analysis

This Hillenbrand SWOT analysis provides concise, actionable insights into strengths, weaknesses, opportunities and threats to support strategic decision-making. The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the complete, editable document with full sourcing and recommendations.