Hillman Solutions Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

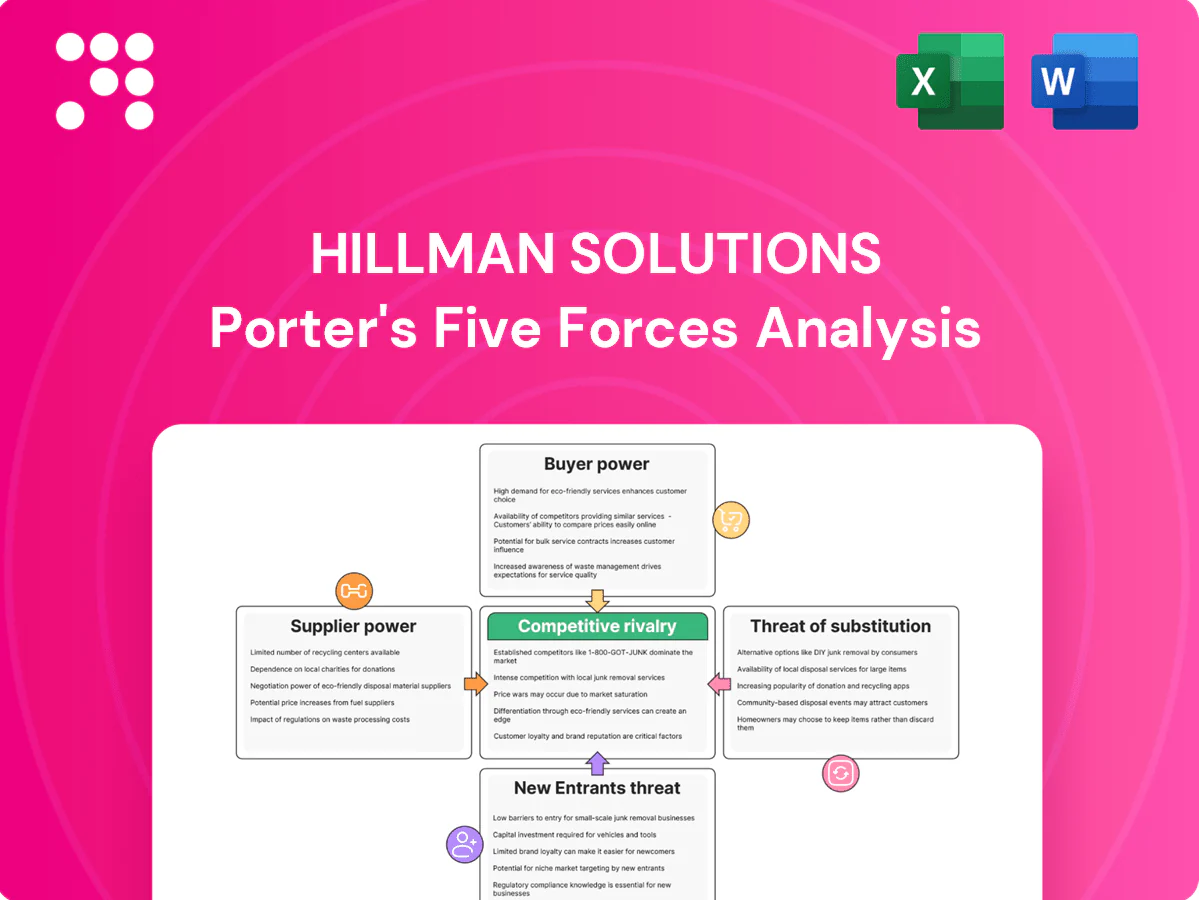

Hillman Solutions faces moderate buyer power, evolving supplier dynamics, and steady threat from substitutes as it navigates a fragmented hardware market; competitive rivalry and potential new entrants shape margin pressure and strategic choices. This snapshot highlights key pressures but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a consultant-grade, actionable breakdown to inform investment or strategy decisions.

Suppliers Bargaining Power

Commodity Inputs Volatility

Fasteners depend on steel, zinc, aluminum and resins, which experienced double-digit percentage swings in 2024, allowing suppliers to pass cost spikes through and compress margins when Hillman’s retail pricing lags. Hedging and multi-sourcing moderate volatility but cannot fully remove exposure, especially for resins tied to petrochemical cycles. Hillman’s scale improves negotiating leverage and enabled procurement savings in 2024, yet material-cost exposure remains a persistent margin risk.

Specialized Equipment & Key Systems

Key duplication kiosks and cutting machines come from a limited vendor pool, with three OEMs estimated to supply roughly 70% of advanced self-service units in 2024. Fewer qualified OEMs raise switching costs and create lead-time risk, often 12–20 weeks for replacements. Dependence on service and spare parts increases supplier leverage and cost volatility. Long-term agreements and growing in-house repair capabilities partially offset this power.

Global Sourcing & Logistics Dependencies

Imports from Asia and Mexico, which account for over 65% of Hillman’s sourced volume, expose the company to port bottlenecks, freight volatility and geopolitical risk; Drewry reported container rates volatility of +/-40% in 2024. Carriers and freight brokers seized leverage during tight capacity cycles, pushing spot premiums as high as 25–35%. Nearshoring and diversified lanes reduced single-point failures, while inventory buffers and VMI improved service at the cost of 10–20% higher working capital requirements.

Specification & Quality Requirements

Retail customers demand consistent, certified quality across Hillman Solutions’ broad portfolio of roughly 100,000 SKUs, constraining rapid supplier switching and favoring established mills and finishers. Mandatory compliance with ROHS, ASTM and retailer packaging specs narrows the qualified supplier pool and increases onboarding time and cost. Approved vendor lists give upstream partners measurable negotiating leverage on pricing and lead times.

- SKU breadth: ~100,000

- Compliance: ROHS, ASTM, retailer packaging

- Switching friction: favors established mills/finishers

- Approved vendor lists: increases supplier negotiating room

Countervailing Buyer Scale

- Aggregated volume lowers per-unit cost

- Private-labels and dual-sourcing reduce supplier sway

- Niche parts/rush orders preserve supplier leverage

Supplier pressure, OEM concentration and freight volatility compress margins and raise supply risk

Suppliers hold moderate-to-high power: material-price swings in 2024 (steel/zinc/resins double-digit) and resins tied to petrochem cycles compressed margins despite Hillman scale. Key OEMs (3 firms ~70% of advanced kiosks) and certified mills for ~100,000 SKUs increase switching cost and lead times (12–20 weeks). Imports >65% expose Hillman to freight volatility (container rates ±40%, spot premiums 25–35%) though nearshoring, dual-sourcing and long-term contracts mitigate risk.

| Metric | 2024 Value |

|---|---|

| SKU breadth | ~100,000 |

| Imported volume | >65% |

| OEM concentration (kiosks) | 3 firms ≈70% |

| Container rate volatility | ±40% |

| Spot freight premiums | 25–35% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Hillman Solutions, identifying disruptive forces, substitutes, and supplier/buyer power that affect pricing and profitability.

Hillman Solutions’ Porter's Five Forces one-sheet quickly highlights competitive pressures with customizable ratings and a spider chart, removing analysis bottlenecks and delivering presentation-ready visuals and notes without complex tools.

Customers Bargaining Power

Retail Consolidation

Major chains dominate Hillman distribution: Home Depot (US sales $157.4B in 2023) and Lowe's ($96.3B) together exceed $253.7B, giving them scale to pressure pricing, payment terms and slotting. Losing a top account would be material and elevate buyer power. Hillman's category captaincy can balance influence but only if it delivers measurable sales uplift and cost efficiencies.

Switching Costs & Service Integration

VMI, planogramming and in-aisle service embed Hillman in retailer operations, creating data, fixture and process lock‑ins that materially raise switching costs; industry studies in 2024 show VMI programs can cut inventory carrying by ~20–25% and reduce out‑of‑stock events. Buyers still use RFPs to benchmark pricing and service levels, so retention ultimately depends on Hillman maintaining high fill rates, on‑shelf availability and measurable labor relief.

Private Label & Assortment Control

Retailers now steer brand architecture toward private label, with private-label penetration rising to about 18% in the US in 2024, shifting margin capture upstream and increasing cost transparency. Hillman benefits as a private-label enabler, gaining volume but facing tighter cost and gross-margin targets from retail partners. Rapid assortment resets—often executed within weeks—allow retailers to reallocate space quickly, amplifying short-term demand volatility for Hillman.

Price Sensitivity vs Availability

- Price premium tolerated: 2–5%

- Typical OOS rate: 7–8%

- Target turns: 8–12

- Category growth leverage: 5–10% YoY

- Dispute/shrink reduction via data: ~10–15%

Omnichannel Fulfillment Demands

Buyers now demand D2C, BOPIS, and e-commerce-ready packaging, with McKinsey 2024 noting roughly 70% of shoppers use multiple channels; Deloitte 2024 reports BOPIS orders rose about 22% YoY. Compliance with varied channel SLAs adds operational complexity and can increase per-unit fulfillment costs by 5–12%, squeezing supplier margins. Suppliers meeting omnichannel SLAs gain stickiness and pricing influence, while failures boost buyer negotiating power and churn risk.

- Omnichannel adoption: 70% multichannel shoppers (McKinsey 2024)

- BOPIS growth: +22% YoY (Deloitte 2024)

- Fulfillment cost impact: +5–12% per unit

- Consequence: higher buyer leverage and churn if SLAs missed

Pricing power vs private label: reliability key to retaining big retail accounts

Large retailers (Home Depot $157.4B 2023; Lowe's $96.3B) have strong pricing leverage; losing a top account is material. VMI/planogram lock‑ins raise switching costs, but private‑label rise (~18% US 2024) and omnichannel SLAs (+22% BOPIS 2024) increase buyer pressure. Reliability (fill rates, turns 8–12) determines retention.

| Metric | Value |

|---|---|

| HD sales 2023 | $157.4B |

| Lowe's 2023 | $96.3B |

| Private label 2024 | ~18% |

| BOPIS growth 2024 | +22% |

What You See Is What You Get

Hillman Solutions Porter's Five Forces Analysis

This preview shows the exact Hillman Solutions Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted, comprehensive, and ready for immediate download and use. Purchase grants instant access to this exact document.

A Must-Have Tool for Decision-Makers

Hillman Solutions faces moderate buyer power, evolving supplier dynamics, and steady threat from substitutes as it navigates a fragmented hardware market; competitive rivalry and potential new entrants shape margin pressure and strategic choices. This snapshot highlights key pressures but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a consultant-grade, actionable breakdown to inform investment or strategy decisions.

Suppliers Bargaining Power

Commodity Inputs Volatility

Fasteners depend on steel, zinc, aluminum and resins, which experienced double-digit percentage swings in 2024, allowing suppliers to pass cost spikes through and compress margins when Hillman’s retail pricing lags. Hedging and multi-sourcing moderate volatility but cannot fully remove exposure, especially for resins tied to petrochemical cycles. Hillman’s scale improves negotiating leverage and enabled procurement savings in 2024, yet material-cost exposure remains a persistent margin risk.

Specialized Equipment & Key Systems

Key duplication kiosks and cutting machines come from a limited vendor pool, with three OEMs estimated to supply roughly 70% of advanced self-service units in 2024. Fewer qualified OEMs raise switching costs and create lead-time risk, often 12–20 weeks for replacements. Dependence on service and spare parts increases supplier leverage and cost volatility. Long-term agreements and growing in-house repair capabilities partially offset this power.

Global Sourcing & Logistics Dependencies

Imports from Asia and Mexico, which account for over 65% of Hillman’s sourced volume, expose the company to port bottlenecks, freight volatility and geopolitical risk; Drewry reported container rates volatility of +/-40% in 2024. Carriers and freight brokers seized leverage during tight capacity cycles, pushing spot premiums as high as 25–35%. Nearshoring and diversified lanes reduced single-point failures, while inventory buffers and VMI improved service at the cost of 10–20% higher working capital requirements.

Specification & Quality Requirements

Retail customers demand consistent, certified quality across Hillman Solutions’ broad portfolio of roughly 100,000 SKUs, constraining rapid supplier switching and favoring established mills and finishers. Mandatory compliance with ROHS, ASTM and retailer packaging specs narrows the qualified supplier pool and increases onboarding time and cost. Approved vendor lists give upstream partners measurable negotiating leverage on pricing and lead times.

- SKU breadth: ~100,000

- Compliance: ROHS, ASTM, retailer packaging

- Switching friction: favors established mills/finishers

- Approved vendor lists: increases supplier negotiating room

Countervailing Buyer Scale

- Aggregated volume lowers per-unit cost

- Private-labels and dual-sourcing reduce supplier sway

- Niche parts/rush orders preserve supplier leverage

Supplier pressure, OEM concentration and freight volatility compress margins and raise supply risk

Suppliers hold moderate-to-high power: material-price swings in 2024 (steel/zinc/resins double-digit) and resins tied to petrochem cycles compressed margins despite Hillman scale. Key OEMs (3 firms ~70% of advanced kiosks) and certified mills for ~100,000 SKUs increase switching cost and lead times (12–20 weeks). Imports >65% expose Hillman to freight volatility (container rates ±40%, spot premiums 25–35%) though nearshoring, dual-sourcing and long-term contracts mitigate risk.

| Metric | 2024 Value |

|---|---|

| SKU breadth | ~100,000 |

| Imported volume | >65% |

| OEM concentration (kiosks) | 3 firms ≈70% |

| Container rate volatility | ±40% |

| Spot freight premiums | 25–35% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Hillman Solutions, identifying disruptive forces, substitutes, and supplier/buyer power that affect pricing and profitability.

Hillman Solutions’ Porter's Five Forces one-sheet quickly highlights competitive pressures with customizable ratings and a spider chart, removing analysis bottlenecks and delivering presentation-ready visuals and notes without complex tools.

Customers Bargaining Power

Retail Consolidation

Major chains dominate Hillman distribution: Home Depot (US sales $157.4B in 2023) and Lowe's ($96.3B) together exceed $253.7B, giving them scale to pressure pricing, payment terms and slotting. Losing a top account would be material and elevate buyer power. Hillman's category captaincy can balance influence but only if it delivers measurable sales uplift and cost efficiencies.

Switching Costs & Service Integration

VMI, planogramming and in-aisle service embed Hillman in retailer operations, creating data, fixture and process lock‑ins that materially raise switching costs; industry studies in 2024 show VMI programs can cut inventory carrying by ~20–25% and reduce out‑of‑stock events. Buyers still use RFPs to benchmark pricing and service levels, so retention ultimately depends on Hillman maintaining high fill rates, on‑shelf availability and measurable labor relief.

Private Label & Assortment Control

Retailers now steer brand architecture toward private label, with private-label penetration rising to about 18% in the US in 2024, shifting margin capture upstream and increasing cost transparency. Hillman benefits as a private-label enabler, gaining volume but facing tighter cost and gross-margin targets from retail partners. Rapid assortment resets—often executed within weeks—allow retailers to reallocate space quickly, amplifying short-term demand volatility for Hillman.

Price Sensitivity vs Availability

- Price premium tolerated: 2–5%

- Typical OOS rate: 7–8%

- Target turns: 8–12

- Category growth leverage: 5–10% YoY

- Dispute/shrink reduction via data: ~10–15%

Omnichannel Fulfillment Demands

Buyers now demand D2C, BOPIS, and e-commerce-ready packaging, with McKinsey 2024 noting roughly 70% of shoppers use multiple channels; Deloitte 2024 reports BOPIS orders rose about 22% YoY. Compliance with varied channel SLAs adds operational complexity and can increase per-unit fulfillment costs by 5–12%, squeezing supplier margins. Suppliers meeting omnichannel SLAs gain stickiness and pricing influence, while failures boost buyer negotiating power and churn risk.

- Omnichannel adoption: 70% multichannel shoppers (McKinsey 2024)

- BOPIS growth: +22% YoY (Deloitte 2024)

- Fulfillment cost impact: +5–12% per unit

- Consequence: higher buyer leverage and churn if SLAs missed

Pricing power vs private label: reliability key to retaining big retail accounts

Large retailers (Home Depot $157.4B 2023; Lowe's $96.3B) have strong pricing leverage; losing a top account is material. VMI/planogram lock‑ins raise switching costs, but private‑label rise (~18% US 2024) and omnichannel SLAs (+22% BOPIS 2024) increase buyer pressure. Reliability (fill rates, turns 8–12) determines retention.

| Metric | Value |

|---|---|

| HD sales 2023 | $157.4B |

| Lowe's 2023 | $96.3B |

| Private label 2024 | ~18% |

| BOPIS growth 2024 | +22% |

What You See Is What You Get

Hillman Solutions Porter's Five Forces Analysis

This preview shows the exact Hillman Solutions Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted, comprehensive, and ready for immediate download and use. Purchase grants instant access to this exact document.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Hillman Solutions faces moderate buyer power, evolving supplier dynamics, and steady threat from substitutes as it navigates a fragmented hardware market; competitive rivalry and potential new entrants shape margin pressure and strategic choices. This snapshot highlights key pressures but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis for a consultant-grade, actionable breakdown to inform investment or strategy decisions.

Suppliers Bargaining Power

Commodity Inputs Volatility

Fasteners depend on steel, zinc, aluminum and resins, which experienced double-digit percentage swings in 2024, allowing suppliers to pass cost spikes through and compress margins when Hillman’s retail pricing lags. Hedging and multi-sourcing moderate volatility but cannot fully remove exposure, especially for resins tied to petrochemical cycles. Hillman’s scale improves negotiating leverage and enabled procurement savings in 2024, yet material-cost exposure remains a persistent margin risk.

Specialized Equipment & Key Systems

Key duplication kiosks and cutting machines come from a limited vendor pool, with three OEMs estimated to supply roughly 70% of advanced self-service units in 2024. Fewer qualified OEMs raise switching costs and create lead-time risk, often 12–20 weeks for replacements. Dependence on service and spare parts increases supplier leverage and cost volatility. Long-term agreements and growing in-house repair capabilities partially offset this power.

Global Sourcing & Logistics Dependencies

Imports from Asia and Mexico, which account for over 65% of Hillman’s sourced volume, expose the company to port bottlenecks, freight volatility and geopolitical risk; Drewry reported container rates volatility of +/-40% in 2024. Carriers and freight brokers seized leverage during tight capacity cycles, pushing spot premiums as high as 25–35%. Nearshoring and diversified lanes reduced single-point failures, while inventory buffers and VMI improved service at the cost of 10–20% higher working capital requirements.

Specification & Quality Requirements

Retail customers demand consistent, certified quality across Hillman Solutions’ broad portfolio of roughly 100,000 SKUs, constraining rapid supplier switching and favoring established mills and finishers. Mandatory compliance with ROHS, ASTM and retailer packaging specs narrows the qualified supplier pool and increases onboarding time and cost. Approved vendor lists give upstream partners measurable negotiating leverage on pricing and lead times.

- SKU breadth: ~100,000

- Compliance: ROHS, ASTM, retailer packaging

- Switching friction: favors established mills/finishers

- Approved vendor lists: increases supplier negotiating room

Countervailing Buyer Scale

- Aggregated volume lowers per-unit cost

- Private-labels and dual-sourcing reduce supplier sway

- Niche parts/rush orders preserve supplier leverage

Supplier pressure, OEM concentration and freight volatility compress margins and raise supply risk

Suppliers hold moderate-to-high power: material-price swings in 2024 (steel/zinc/resins double-digit) and resins tied to petrochem cycles compressed margins despite Hillman scale. Key OEMs (3 firms ~70% of advanced kiosks) and certified mills for ~100,000 SKUs increase switching cost and lead times (12–20 weeks). Imports >65% expose Hillman to freight volatility (container rates ±40%, spot premiums 25–35%) though nearshoring, dual-sourcing and long-term contracts mitigate risk.

| Metric | 2024 Value |

|---|---|

| SKU breadth | ~100,000 |

| Imported volume | >65% |

| OEM concentration (kiosks) | 3 firms ≈70% |

| Container rate volatility | ±40% |

| Spot freight premiums | 25–35% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for Hillman Solutions, identifying disruptive forces, substitutes, and supplier/buyer power that affect pricing and profitability.

Hillman Solutions’ Porter's Five Forces one-sheet quickly highlights competitive pressures with customizable ratings and a spider chart, removing analysis bottlenecks and delivering presentation-ready visuals and notes without complex tools.

Customers Bargaining Power

Retail Consolidation

Major chains dominate Hillman distribution: Home Depot (US sales $157.4B in 2023) and Lowe's ($96.3B) together exceed $253.7B, giving them scale to pressure pricing, payment terms and slotting. Losing a top account would be material and elevate buyer power. Hillman's category captaincy can balance influence but only if it delivers measurable sales uplift and cost efficiencies.

Switching Costs & Service Integration

VMI, planogramming and in-aisle service embed Hillman in retailer operations, creating data, fixture and process lock‑ins that materially raise switching costs; industry studies in 2024 show VMI programs can cut inventory carrying by ~20–25% and reduce out‑of‑stock events. Buyers still use RFPs to benchmark pricing and service levels, so retention ultimately depends on Hillman maintaining high fill rates, on‑shelf availability and measurable labor relief.

Private Label & Assortment Control

Retailers now steer brand architecture toward private label, with private-label penetration rising to about 18% in the US in 2024, shifting margin capture upstream and increasing cost transparency. Hillman benefits as a private-label enabler, gaining volume but facing tighter cost and gross-margin targets from retail partners. Rapid assortment resets—often executed within weeks—allow retailers to reallocate space quickly, amplifying short-term demand volatility for Hillman.

Price Sensitivity vs Availability

- Price premium tolerated: 2–5%

- Typical OOS rate: 7–8%

- Target turns: 8–12

- Category growth leverage: 5–10% YoY

- Dispute/shrink reduction via data: ~10–15%

Omnichannel Fulfillment Demands

Buyers now demand D2C, BOPIS, and e-commerce-ready packaging, with McKinsey 2024 noting roughly 70% of shoppers use multiple channels; Deloitte 2024 reports BOPIS orders rose about 22% YoY. Compliance with varied channel SLAs adds operational complexity and can increase per-unit fulfillment costs by 5–12%, squeezing supplier margins. Suppliers meeting omnichannel SLAs gain stickiness and pricing influence, while failures boost buyer negotiating power and churn risk.

- Omnichannel adoption: 70% multichannel shoppers (McKinsey 2024)

- BOPIS growth: +22% YoY (Deloitte 2024)

- Fulfillment cost impact: +5–12% per unit

- Consequence: higher buyer leverage and churn if SLAs missed

Pricing power vs private label: reliability key to retaining big retail accounts

Large retailers (Home Depot $157.4B 2023; Lowe's $96.3B) have strong pricing leverage; losing a top account is material. VMI/planogram lock‑ins raise switching costs, but private‑label rise (~18% US 2024) and omnichannel SLAs (+22% BOPIS 2024) increase buyer pressure. Reliability (fill rates, turns 8–12) determines retention.

| Metric | Value |

|---|---|

| HD sales 2023 | $157.4B |

| Lowe's 2023 | $96.3B |

| Private label 2024 | ~18% |

| BOPIS growth 2024 | +22% |

What You See Is What You Get

Hillman Solutions Porter's Five Forces Analysis

This preview shows the exact Hillman Solutions Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file is fully formatted, comprehensive, and ready for immediate download and use. Purchase grants instant access to this exact document.