China Oil And Gas Group Business Model Canvas

Oil & Gas Business Model Canvas: Value Streams, Partnerships, and Risks

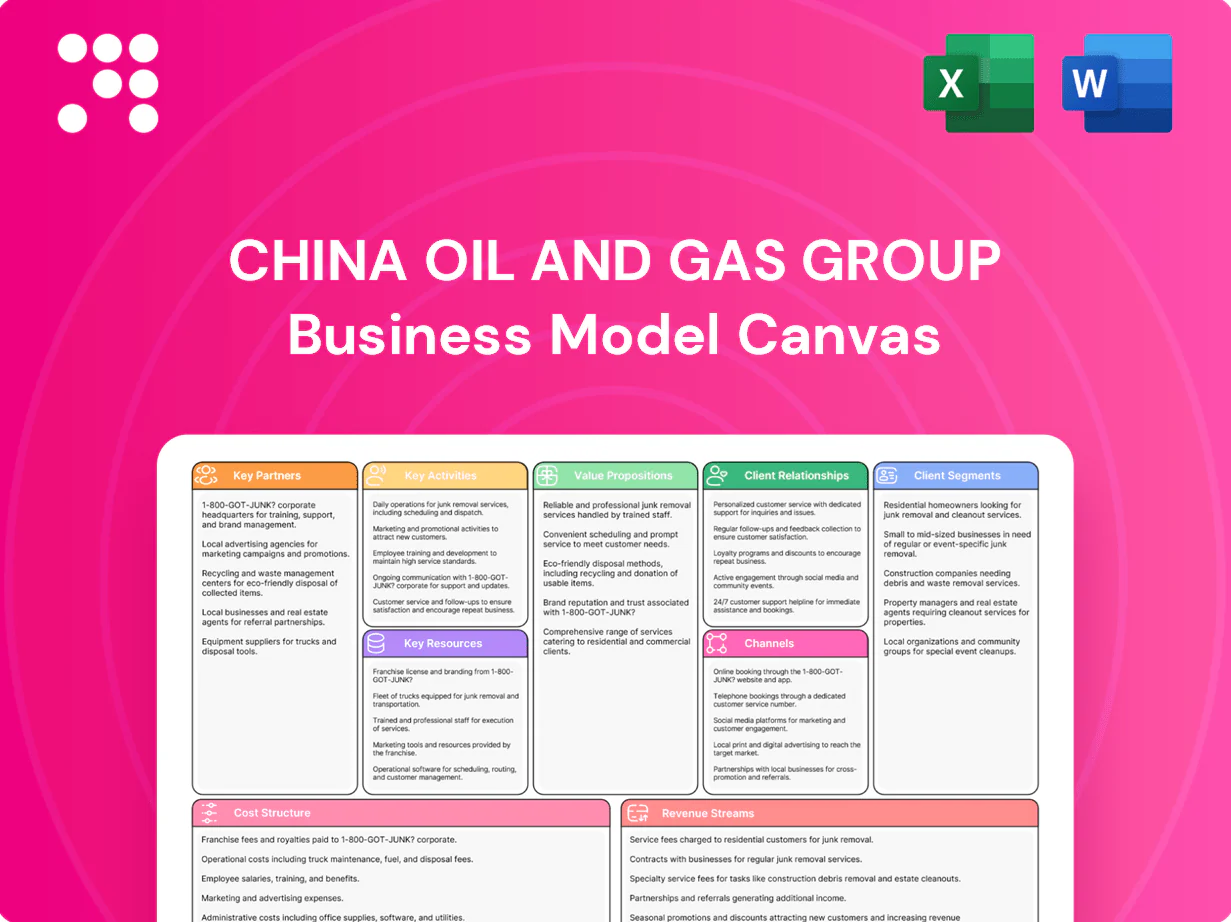

Dive into China Oil And Gas Group’s Business Model Canvas to see how it creates value across upstream and downstream operations, partnerships, and revenue streams. This concise, actionable snapshot reveals growth levers and risks—purchase the full Canvas in Word/Excel for a section-by-section strategic playbook.

Partnerships

Government and SOE alliances

Partner with central and provincial energy authorities and the three major NOCs—CNPC, Sinopec and CNOOC—to secure acreage access and align policy; these SOE alliances are essential given CNPC/Sinopec/CNOOC dominance of upstream assets. They accelerate approvals for CBM and shale pilots and pipeline rights-of-way, and strengthen compliance with safety and environmental standards. Preferential offtake and grid interconnection can be negotiated through SOE offtake agreements.

E&P joint ventures

Collaborate with domestic and international oilfield operators to share risk and technology, supporting China’s crude base (≈3.7 mb/d in 2023) and frontier unconventional targets. JV structures can optimize capex, often lowering initial spend by up to 40% through shared wells and services. Partners supply completion know-how, drilling and enhanced recovery techniques; equity and production-sharing models improve project bankability and lender appetite.

Oilfield service providers

Work with drilling, fracturing, logging and seismic contractors to standardize workflows; 2024 joint projects shortened spud-to-first-gas cycles by about 20%, accelerating cash flow. Performance-based contracts—now ~35% of new service agreements—align costs with measured well productivity. Local suppliers reduced logistics lead times roughly 18% across major basins, boosting operational resilience.

Midstream and utility partners

Tie-ups with pipeline owners, LNG/CNG plant operators and city-gas distributors secure capacity reservations and last-mile access; China was the world’s largest LNG importer in 2024, underscoring midstream leverage. Joint planning with these partners reduces bottlenecks and line-pack risk, while co-investments help stabilize tariffs and throughput.

- Capacity reservations

- Last-mile access

- Joint planning

- Co-investments

Financiers and technology vendors

Engage banks, leasing firms, and OEMs to finance capex and accelerate tech adoption, using structured finance for gathering systems and processing units to optimize cash flow and off-balance solutions.

Digital vendors supply SCADA, AI-driven subsurface models, and continuous emissions monitoring to improve production efficiency and regulatory compliance.

Long-term vendor agreements lock pricing and service levels, lowering lifecycle costs and mitigating supply-chain risk.

- Financiers: banks, leasing firms, OEMs

- Structured finance: gathering & processing

- Tech vendors: SCADA, AI subsurface, emissions

- Agreements: long-term for lower lifecycle costs

Partner SOEs & provinces for acreage/offtake; JVs cut capex 40%

Partner with CNPC, Sinopec, CNOOC and provincial authorities for acreage, offtake and approvals; 2023 China crude ~3.7 mb/d and 2024 largest LNG importer status increase midstream leverage. JVs with operators can cut initial capex ~40%; service contracts (≈35% new) and tech vendors shortened spud-to-first-gas ~20% and cut supplier lead times ~18%.

| Partner | Key metric |

|---|---|

| SOEs | acreage/offtake |

| JVs | capex -40% |

| Services/tech | spud→gas -20% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to China Oil And Gas Group’s upstream, midstream and downstream operations, covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks; investor-ready with competitive-advantage analysis, linked SWOT insights and actionable strategic recommendations for funding, partnerships and operational scaling.

High-level view of China Oil And Gas Group’s business model with editable cells, relieving the pain of scattered strategy and complex asset portfolios. Great for quickly aligning stakeholders, speeding decision-making, and standardizing analysis across projects.

Activities

Unconventional resource development

Prospect, appraise and develop CBM and shale gas blocks, targeting resource-rich basins with 2024 pilot projects showing 18% uplift in EUR per well and 12% higher initial production; execute drilling and multi-stage fracturing programs with pad drilling scaled to cut per-well costs by ~20% in pilots. Optimize completions using geosteering and microseismic feedback to boost EUR and reduce decline rates.

Integrated midstream operations

Build and operate gathering, processing, compression and transmission assets to connect upstream fields to markets, ensuring gas quality control, dehydration and NGL recovery at scale. In 2024 China remains the world’s second-largest natural gas consumer, so balancing flows via storage and line-pack management is critical to meet seasonal demand. Secure third-party throughput to maximize utilization and capture fee-based revenues.

Downstream gas distribution

Sell to industrial users, power plants, city-gas companies and transport (CNG/LNG), targeting segments that drove China’s downstream demand as natural gas consumption surpassed 400 bcm in 2024. Structure indexed contracts and balancing services to manage price volatility and pipeline/backhaul constraints. Provide metering, billing and 24/7 customer support while scaling small-scale LNG hubs for off-grid demand growth.

Portfolio and capital management

Portfolio and capital management allocates capital across basins and lifecycle stages, hedges commodity exposure to optimize realized pricing, pursues M&A and farm-ins to refresh inventory, and enforces HSSE compliance with ESG reporting; China remained the world’s largest crude importer in 2024.

- Allocate capital: basins + lifecycle

- Hedge & price optimization

- M&A / farm-ins to refresh inventory

- HSSE compliance & ESG reporting

Technology and emissions management

Deploy integrated digital subsurface models, predictive maintenance and SCADA to optimize wells and reduce downtime, while using satellite and continuous sensors for methane detection and flare minimization; methane is ~80 times more potent than CO2 over 20 years.

Electrify compressors where grid or battery power is feasible and implement CO2/NGL capture from separation units to retain value and cut emissions, with continuous benchmarking for performance improvement.

- Digital subsurface modeling

- Predictive maintenance & SCADA

- Methane detection & flare reduction

- Compressor electrification & CO2/NGL capture

- Benchmarking for continuous improvement

Prospect CBM/shale: 18% EUR, 12% IP, 20% lower cost; tap >400 bcm market

Prospect, appraise and develop CBM/shale with 2024 pilots showing 18% EUR uplift, 12% higher IP and ~20% lower per-well costs; drill, frac and optimize completions to cut declines. Build gathering, processing and transmission to serve China’s >400 bcm 2024 market, capture throughput fees and balance via storage. Deploy digital subsurface, SCADA, methane sensing and compressor electrification to cut emissions.

| Activity | 2024 metric | Impact |

|---|---|---|

| Upstream | +18% EUR, +12% IP, -20% cost | Higher ROIC |

| Midstream | >400 bcm market | Fee revenue, security |

| Decarbonization | CH4 ~80x CO2 (20y) | Emissions reduction |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the authentic China Oil And Gas Group Business Model Canvas, not a mockup, and displays the same structure and content you'll receive after purchase. When you complete your order you'll download this exact file—fully formatted and ready to edit in Word and Excel. No placeholders, no surprises—what you see is what you will own.

Oil & Gas Business Model Canvas: Value Streams, Partnerships, and Risks

Dive into China Oil And Gas Group’s Business Model Canvas to see how it creates value across upstream and downstream operations, partnerships, and revenue streams. This concise, actionable snapshot reveals growth levers and risks—purchase the full Canvas in Word/Excel for a section-by-section strategic playbook.

Partnerships

Government and SOE alliances

Partner with central and provincial energy authorities and the three major NOCs—CNPC, Sinopec and CNOOC—to secure acreage access and align policy; these SOE alliances are essential given CNPC/Sinopec/CNOOC dominance of upstream assets. They accelerate approvals for CBM and shale pilots and pipeline rights-of-way, and strengthen compliance with safety and environmental standards. Preferential offtake and grid interconnection can be negotiated through SOE offtake agreements.

E&P joint ventures

Collaborate with domestic and international oilfield operators to share risk and technology, supporting China’s crude base (≈3.7 mb/d in 2023) and frontier unconventional targets. JV structures can optimize capex, often lowering initial spend by up to 40% through shared wells and services. Partners supply completion know-how, drilling and enhanced recovery techniques; equity and production-sharing models improve project bankability and lender appetite.

Oilfield service providers

Work with drilling, fracturing, logging and seismic contractors to standardize workflows; 2024 joint projects shortened spud-to-first-gas cycles by about 20%, accelerating cash flow. Performance-based contracts—now ~35% of new service agreements—align costs with measured well productivity. Local suppliers reduced logistics lead times roughly 18% across major basins, boosting operational resilience.

Midstream and utility partners

Tie-ups with pipeline owners, LNG/CNG plant operators and city-gas distributors secure capacity reservations and last-mile access; China was the world’s largest LNG importer in 2024, underscoring midstream leverage. Joint planning with these partners reduces bottlenecks and line-pack risk, while co-investments help stabilize tariffs and throughput.

- Capacity reservations

- Last-mile access

- Joint planning

- Co-investments

Financiers and technology vendors

Engage banks, leasing firms, and OEMs to finance capex and accelerate tech adoption, using structured finance for gathering systems and processing units to optimize cash flow and off-balance solutions.

Digital vendors supply SCADA, AI-driven subsurface models, and continuous emissions monitoring to improve production efficiency and regulatory compliance.

Long-term vendor agreements lock pricing and service levels, lowering lifecycle costs and mitigating supply-chain risk.

- Financiers: banks, leasing firms, OEMs

- Structured finance: gathering & processing

- Tech vendors: SCADA, AI subsurface, emissions

- Agreements: long-term for lower lifecycle costs

Partner SOEs & provinces for acreage/offtake; JVs cut capex 40%

Partner with CNPC, Sinopec, CNOOC and provincial authorities for acreage, offtake and approvals; 2023 China crude ~3.7 mb/d and 2024 largest LNG importer status increase midstream leverage. JVs with operators can cut initial capex ~40%; service contracts (≈35% new) and tech vendors shortened spud-to-first-gas ~20% and cut supplier lead times ~18%.

| Partner | Key metric |

|---|---|

| SOEs | acreage/offtake |

| JVs | capex -40% |

| Services/tech | spud→gas -20% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to China Oil And Gas Group’s upstream, midstream and downstream operations, covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks; investor-ready with competitive-advantage analysis, linked SWOT insights and actionable strategic recommendations for funding, partnerships and operational scaling.

High-level view of China Oil And Gas Group’s business model with editable cells, relieving the pain of scattered strategy and complex asset portfolios. Great for quickly aligning stakeholders, speeding decision-making, and standardizing analysis across projects.

Activities

Unconventional resource development

Prospect, appraise and develop CBM and shale gas blocks, targeting resource-rich basins with 2024 pilot projects showing 18% uplift in EUR per well and 12% higher initial production; execute drilling and multi-stage fracturing programs with pad drilling scaled to cut per-well costs by ~20% in pilots. Optimize completions using geosteering and microseismic feedback to boost EUR and reduce decline rates.

Integrated midstream operations

Build and operate gathering, processing, compression and transmission assets to connect upstream fields to markets, ensuring gas quality control, dehydration and NGL recovery at scale. In 2024 China remains the world’s second-largest natural gas consumer, so balancing flows via storage and line-pack management is critical to meet seasonal demand. Secure third-party throughput to maximize utilization and capture fee-based revenues.

Downstream gas distribution

Sell to industrial users, power plants, city-gas companies and transport (CNG/LNG), targeting segments that drove China’s downstream demand as natural gas consumption surpassed 400 bcm in 2024. Structure indexed contracts and balancing services to manage price volatility and pipeline/backhaul constraints. Provide metering, billing and 24/7 customer support while scaling small-scale LNG hubs for off-grid demand growth.

Portfolio and capital management

Portfolio and capital management allocates capital across basins and lifecycle stages, hedges commodity exposure to optimize realized pricing, pursues M&A and farm-ins to refresh inventory, and enforces HSSE compliance with ESG reporting; China remained the world’s largest crude importer in 2024.

- Allocate capital: basins + lifecycle

- Hedge & price optimization

- M&A / farm-ins to refresh inventory

- HSSE compliance & ESG reporting

Technology and emissions management

Deploy integrated digital subsurface models, predictive maintenance and SCADA to optimize wells and reduce downtime, while using satellite and continuous sensors for methane detection and flare minimization; methane is ~80 times more potent than CO2 over 20 years.

Electrify compressors where grid or battery power is feasible and implement CO2/NGL capture from separation units to retain value and cut emissions, with continuous benchmarking for performance improvement.

- Digital subsurface modeling

- Predictive maintenance & SCADA

- Methane detection & flare reduction

- Compressor electrification & CO2/NGL capture

- Benchmarking for continuous improvement

Prospect CBM/shale: 18% EUR, 12% IP, 20% lower cost; tap >400 bcm market

Prospect, appraise and develop CBM/shale with 2024 pilots showing 18% EUR uplift, 12% higher IP and ~20% lower per-well costs; drill, frac and optimize completions to cut declines. Build gathering, processing and transmission to serve China’s >400 bcm 2024 market, capture throughput fees and balance via storage. Deploy digital subsurface, SCADA, methane sensing and compressor electrification to cut emissions.

| Activity | 2024 metric | Impact |

|---|---|---|

| Upstream | +18% EUR, +12% IP, -20% cost | Higher ROIC |

| Midstream | >400 bcm market | Fee revenue, security |

| Decarbonization | CH4 ~80x CO2 (20y) | Emissions reduction |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the authentic China Oil And Gas Group Business Model Canvas, not a mockup, and displays the same structure and content you'll receive after purchase. When you complete your order you'll download this exact file—fully formatted and ready to edit in Word and Excel. No placeholders, no surprises—what you see is what you will own.

Description

Oil & Gas Business Model Canvas: Value Streams, Partnerships, and Risks

Dive into China Oil And Gas Group’s Business Model Canvas to see how it creates value across upstream and downstream operations, partnerships, and revenue streams. This concise, actionable snapshot reveals growth levers and risks—purchase the full Canvas in Word/Excel for a section-by-section strategic playbook.

Partnerships

Government and SOE alliances

Partner with central and provincial energy authorities and the three major NOCs—CNPC, Sinopec and CNOOC—to secure acreage access and align policy; these SOE alliances are essential given CNPC/Sinopec/CNOOC dominance of upstream assets. They accelerate approvals for CBM and shale pilots and pipeline rights-of-way, and strengthen compliance with safety and environmental standards. Preferential offtake and grid interconnection can be negotiated through SOE offtake agreements.

E&P joint ventures

Collaborate with domestic and international oilfield operators to share risk and technology, supporting China’s crude base (≈3.7 mb/d in 2023) and frontier unconventional targets. JV structures can optimize capex, often lowering initial spend by up to 40% through shared wells and services. Partners supply completion know-how, drilling and enhanced recovery techniques; equity and production-sharing models improve project bankability and lender appetite.

Oilfield service providers

Work with drilling, fracturing, logging and seismic contractors to standardize workflows; 2024 joint projects shortened spud-to-first-gas cycles by about 20%, accelerating cash flow. Performance-based contracts—now ~35% of new service agreements—align costs with measured well productivity. Local suppliers reduced logistics lead times roughly 18% across major basins, boosting operational resilience.

Midstream and utility partners

Tie-ups with pipeline owners, LNG/CNG plant operators and city-gas distributors secure capacity reservations and last-mile access; China was the world’s largest LNG importer in 2024, underscoring midstream leverage. Joint planning with these partners reduces bottlenecks and line-pack risk, while co-investments help stabilize tariffs and throughput.

- Capacity reservations

- Last-mile access

- Joint planning

- Co-investments

Financiers and technology vendors

Engage banks, leasing firms, and OEMs to finance capex and accelerate tech adoption, using structured finance for gathering systems and processing units to optimize cash flow and off-balance solutions.

Digital vendors supply SCADA, AI-driven subsurface models, and continuous emissions monitoring to improve production efficiency and regulatory compliance.

Long-term vendor agreements lock pricing and service levels, lowering lifecycle costs and mitigating supply-chain risk.

- Financiers: banks, leasing firms, OEMs

- Structured finance: gathering & processing

- Tech vendors: SCADA, AI subsurface, emissions

- Agreements: long-term for lower lifecycle costs

Partner SOEs & provinces for acreage/offtake; JVs cut capex 40%

Partner with CNPC, Sinopec, CNOOC and provincial authorities for acreage, offtake and approvals; 2023 China crude ~3.7 mb/d and 2024 largest LNG importer status increase midstream leverage. JVs with operators can cut initial capex ~40%; service contracts (≈35% new) and tech vendors shortened spud-to-first-gas ~20% and cut supplier lead times ~18%.

| Partner | Key metric |

|---|---|

| SOEs | acreage/offtake |

| JVs | capex -40% |

| Services/tech | spud→gas -20% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to China Oil And Gas Group’s upstream, midstream and downstream operations, covering customer segments, channels, value propositions and revenue streams across the 9 BMC blocks; investor-ready with competitive-advantage analysis, linked SWOT insights and actionable strategic recommendations for funding, partnerships and operational scaling.

High-level view of China Oil And Gas Group’s business model with editable cells, relieving the pain of scattered strategy and complex asset portfolios. Great for quickly aligning stakeholders, speeding decision-making, and standardizing analysis across projects.

Activities

Unconventional resource development

Prospect, appraise and develop CBM and shale gas blocks, targeting resource-rich basins with 2024 pilot projects showing 18% uplift in EUR per well and 12% higher initial production; execute drilling and multi-stage fracturing programs with pad drilling scaled to cut per-well costs by ~20% in pilots. Optimize completions using geosteering and microseismic feedback to boost EUR and reduce decline rates.

Integrated midstream operations

Build and operate gathering, processing, compression and transmission assets to connect upstream fields to markets, ensuring gas quality control, dehydration and NGL recovery at scale. In 2024 China remains the world’s second-largest natural gas consumer, so balancing flows via storage and line-pack management is critical to meet seasonal demand. Secure third-party throughput to maximize utilization and capture fee-based revenues.

Downstream gas distribution

Sell to industrial users, power plants, city-gas companies and transport (CNG/LNG), targeting segments that drove China’s downstream demand as natural gas consumption surpassed 400 bcm in 2024. Structure indexed contracts and balancing services to manage price volatility and pipeline/backhaul constraints. Provide metering, billing and 24/7 customer support while scaling small-scale LNG hubs for off-grid demand growth.

Portfolio and capital management

Portfolio and capital management allocates capital across basins and lifecycle stages, hedges commodity exposure to optimize realized pricing, pursues M&A and farm-ins to refresh inventory, and enforces HSSE compliance with ESG reporting; China remained the world’s largest crude importer in 2024.

- Allocate capital: basins + lifecycle

- Hedge & price optimization

- M&A / farm-ins to refresh inventory

- HSSE compliance & ESG reporting

Technology and emissions management

Deploy integrated digital subsurface models, predictive maintenance and SCADA to optimize wells and reduce downtime, while using satellite and continuous sensors for methane detection and flare minimization; methane is ~80 times more potent than CO2 over 20 years.

Electrify compressors where grid or battery power is feasible and implement CO2/NGL capture from separation units to retain value and cut emissions, with continuous benchmarking for performance improvement.

- Digital subsurface modeling

- Predictive maintenance & SCADA

- Methane detection & flare reduction

- Compressor electrification & CO2/NGL capture

- Benchmarking for continuous improvement

Prospect CBM/shale: 18% EUR, 12% IP, 20% lower cost; tap >400 bcm market

Prospect, appraise and develop CBM/shale with 2024 pilots showing 18% EUR uplift, 12% higher IP and ~20% lower per-well costs; drill, frac and optimize completions to cut declines. Build gathering, processing and transmission to serve China’s >400 bcm 2024 market, capture throughput fees and balance via storage. Deploy digital subsurface, SCADA, methane sensing and compressor electrification to cut emissions.

| Activity | 2024 metric | Impact |

|---|---|---|

| Upstream | +18% EUR, +12% IP, -20% cost | Higher ROIC |

| Midstream | >400 bcm market | Fee revenue, security |

| Decarbonization | CH4 ~80x CO2 (20y) | Emissions reduction |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the authentic China Oil And Gas Group Business Model Canvas, not a mockup, and displays the same structure and content you'll receive after purchase. When you complete your order you'll download this exact file—fully formatted and ready to edit in Word and Excel. No placeholders, no surprises—what you see is what you will own.