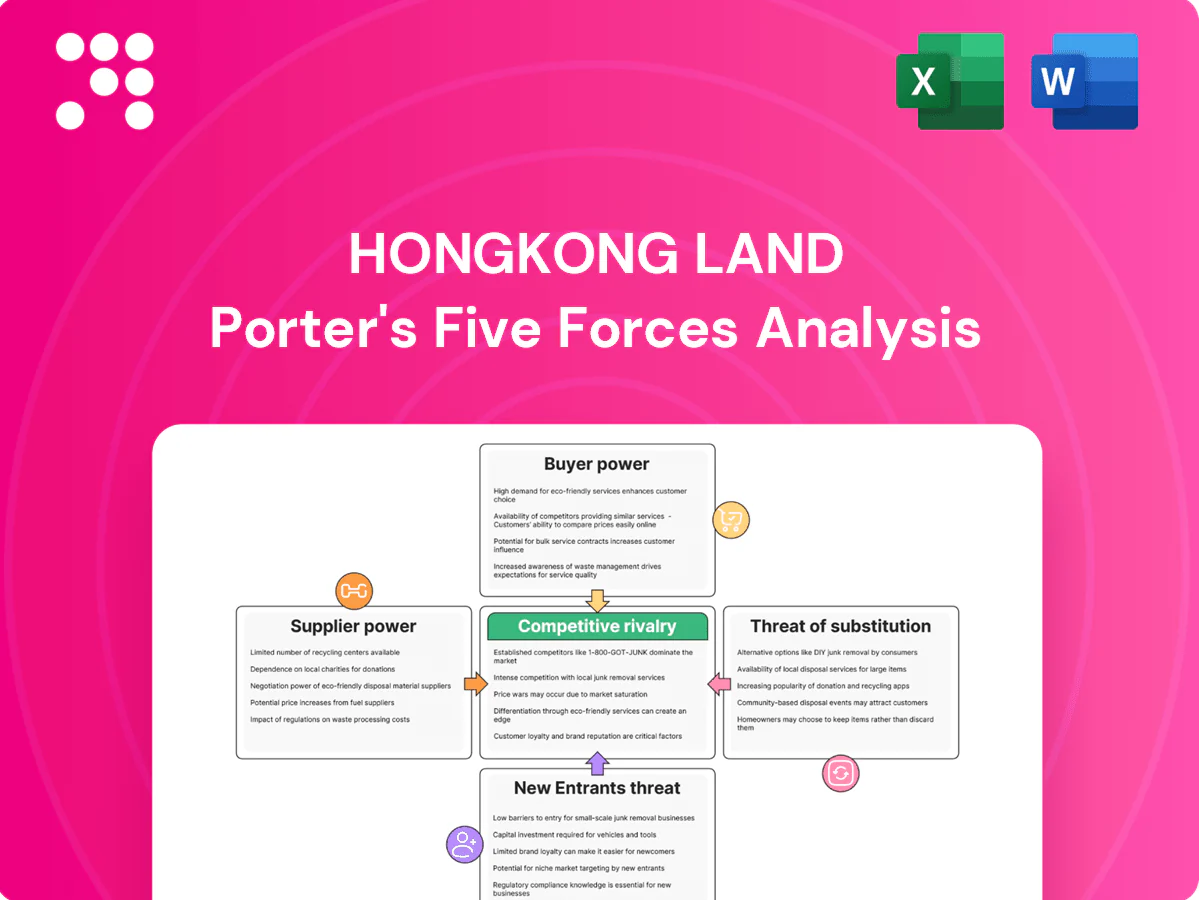

Hongkong Land Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hongkong Land benefits from a prime portfolio and strong brand, but tenant bargaining and market cyclicality heighten competitive pressure; supplier power is moderate while barriers to entry keep new competitors limited. Substitutes like remote work and regional rivals present manageable risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic recommendations.

Suppliers Bargaining Power

Prime land and approvals gatekept

In 2024 access to CBD land in Hong Kong, Singapore and Beijing remained tightly controlled by governments and a few state-linked entities, elevating suppliers’ bargaining power for developers like Hongkong Land.

Zoning rules, plot ratios and mandatory approvals create dependency on public authorities’ timelines, with tender and approval cycles often stretching beyond 12 months.

Scarcity of prime sites enables land vendors to command significant premiums, while long tender cycles delay pipeline replenishment and raise carrying costs for developers.

Tier-1 contractors and fit-out specialists

Large, complex mixed-use assets require a narrow pool of tier-1 contractors and luxury fit-out firms, raising switching costs and concentrating supply among fewer than a dozen specialist firms in Hong Kong by 2024. Capacity constraints during upcycles have pushed tender premiums up to mid-teens percentage points in recent cycles. Hongkong Land’s scale and repeat spend—with a reported portfolio value near US$19.1bn in 2024—gives it negotiation leverage. Use of performance bonds and multi-vendor sourcing partially mitigates supplier concentration risk.

Building materials and ESG specifications

High-grade materials, complex façade systems and LEED/BREEAM-led green tech increase specification rigidity, strengthening supplier bargaining power; steel, cement and MEP items can represent ~40% of core construction costs and experienced c.20% price volatility into 2024, squeezing margins. Framework contracts and hedging have reduced price swings but do not remove long lead-time risks, while tightening sustainability codes heighten reliance on specialized suppliers.

Utilities, property tech, and FM services

Premium assets demand reliable utilities, smart-building systems and top-tier FM; vendor differentiation in proptech and energy optimization concentrates reliance on a few specialists, while long-term O&M contracts (typically 5–15 years) can entrench suppliers and raise switching costs; competitive bidding and strict performance KPIs help contain costs and preserve negotiating leverage.

- Dependence: few specialized proptech/energy vendors

- Contracts: long O&M terms 5–15 years

- Mitigants: competitive tendering, KPI-linked fees

- Risk: vendor lock-in raises supplier power

Financing providers and rating sensitivity

Development and refinancing needs expose Hongkong Land to banks and capital markets pricing power, with rising benchmark yields compressing project IRRs; US 10-year yields averaged about 4.5% in mid-2024, increasing discount rates and financing costs. A strong balance sheet and long-standing reputation improve access and borrowing terms, while diversified funding across bonds, loans and JVs reduces single-lender leverage.

- Banks & markets set pricing

- US 10y ~4.5% (mid-2024) raises discount rates

- Strong balance sheet = better terms

- Funding mix: bonds, loans, JVs lowers concentration

Constrained CBD land and scarce prime sites push supplier premiums and tighten development margins

In 2024 constrained CBD land allocation and scarce prime sites gave suppliers (land vendors, tier‑1 contractors, specialist proptech/green suppliers) elevated bargaining power, raising premiums and switching costs. Hongkong Land’s scale (portfolio ~US$19.1bn in 2024) and competitive tendering mitigate but do not eliminate price and lead‑time risks; financing costs (US 10y ~4.5% mid‑2024) also tighten margins.

| Metric | 2024 value |

|---|---|

| Portfolio value | US$19.1bn |

| US 10y | ~4.5% |

| Construction cost share | ~40% |

| Price volatility | ~20% |

| Tender premiums | mid‑teens% |

| O&M terms | 5–15 yrs |

What is included in the product

Concise Porter's Five Forces analysis tailored to Hongkong Land, assessing competitive rivalry, supplier and buyer power, barriers to entry and threat of substitutes, and highlighting industry-specific drivers, disruptive threats, and implications for pricing and profitability.

Condensed Porter's Five Forces for Hongkong Land—visualize competitive intensity, tenant and supplier bargaining power, threat of new entrants and substitutes, plus regulatory risk in one clear sheet to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Anchor MNC office tenants

Blue-chip MNCs prize Hongkong Land’s central, prestige campuses and integrated services, reducing price sensitivity; Hongkong Land reported c.95% occupancy across its Hong Kong office portfolio in 2024, underscoring stickiness. Their scale and creditworthiness, however, secure rent negotiation power and fit-out incentives, often yielding upfront concessions. Long leases cut churn but concentrate incentives early. Flight-to-quality lifted demand for Grade A space through 2024.

Luxury retail brands

Flagship luxury retailers seek prime frontage and curated tenant mix in Hongkong Land assets, reducing substitutability and reinforcing bargaining power; Cushman & Wakefield (2024) ranks Hong Kong among the top three most expensive retail high streets globally. Top brands command favorable terms and marketing support because they drive footfall and halo effects; Bain (2024) pegs the global personal luxury goods market near €330bn. Percentage-rent structures share upside but introduce revenue volatility, while co-investment in experiences and joint marketing aligns landlord-tenant interests and risk-reward.

Residential buyers in premium segments

High-end buyers demand design, location and developer reputation, tempering price elasticity; Hongkong Land's heritage since 1889 underpins pricing power in downturns. Pre-sales lower funding risk but increase buyer leverage on specs and timelines. Macro rates—US Fed funds at 5.25–5.50% in 2024—can swiftly tilt bargaining power via mortgage costs and sentiment shifts.

Corporate and co-working demand

Flex-space operators aggregate many small occupiers, concentrating negotiating power as coworking supply in Hong Kong grew ~15% in 2024, pressuring landlords to offer shorter terms and incentives. Corporates adopting hybrid work—around 60% of firms in 2024 surveys—are reassessing footprints, demanding expansion/contraction rights that can cut effective rents by up to low‑double digits. Amenity-rich, tech-enabled assets help Hongkong Land defend yields and retain corporate tenants.

- Aggregated demand: flex operators concentrate small tenants

- Hybrid adoption ~60% (2024) drives flexibility demands

- Shorter terms/rights can trim effective rents by low‑double digits

- Amenity-rich buildings support yield protection

Geographic diversification of demand

Geographic diversification across Hong Kong, Singapore and Mainland China broadens tenant pools and reduces dependence on any single market’s bargaining power, though simultaneous regional slowdowns can compress rents across the portfolio.

Strong cross-market brand recognition supports leasing and retention, while differing currency regimes and local regulations create asymmetric negotiating leverage for tenants in each jurisdiction.

- Diversified tenant base across three markets

- Systemic slowdowns can synchronize pricing pressure

- Brand strength improves lease terms

- Currency and regulatory gaps affect local bargaining

HK pricing: office occ 95%, flex supply pressures rents

Blue-chip tenants and luxury retailers give Hongkong Land pricing power; Hong Kong office occupancy ~95% (2024) and retail ranks top‑3 globally (Cushman & Wakefield 2024). Flex operators and hybrid work (~60% adoption in 2024) concentrated bargaining, coworking supply +15% (2024) pressuring incentives. Cross‑market scale and brand mitigate but macro rates (Fed 5.25–5.50% 2024) shift leverage.

| Metric | 2024 | Impact |

|---|---|---|

| HK office occ. | ~95% | High stickiness |

| Hybrid adoption | ~60% | Flex demands |

| Coworking supply | +15% | Incentive pressure |

Preview the Actual Deliverable

Hongkong Land Porter's Five Forces Analysis

This preview shows the exact Hongkong Land Porter’s Five Forces analysis you'll receive—comprehensive, professionally formatted, and ready for immediate use. The file includes competitive intensity, supplier and buyer power, threats of entry and substitutes, and strategic implications. No placeholders or mockups; purchase grants instant access to this same document.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hongkong Land benefits from a prime portfolio and strong brand, but tenant bargaining and market cyclicality heighten competitive pressure; supplier power is moderate while barriers to entry keep new competitors limited. Substitutes like remote work and regional rivals present manageable risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic recommendations.

Suppliers Bargaining Power

Prime land and approvals gatekept

In 2024 access to CBD land in Hong Kong, Singapore and Beijing remained tightly controlled by governments and a few state-linked entities, elevating suppliers’ bargaining power for developers like Hongkong Land.

Zoning rules, plot ratios and mandatory approvals create dependency on public authorities’ timelines, with tender and approval cycles often stretching beyond 12 months.

Scarcity of prime sites enables land vendors to command significant premiums, while long tender cycles delay pipeline replenishment and raise carrying costs for developers.

Tier-1 contractors and fit-out specialists

Large, complex mixed-use assets require a narrow pool of tier-1 contractors and luxury fit-out firms, raising switching costs and concentrating supply among fewer than a dozen specialist firms in Hong Kong by 2024. Capacity constraints during upcycles have pushed tender premiums up to mid-teens percentage points in recent cycles. Hongkong Land’s scale and repeat spend—with a reported portfolio value near US$19.1bn in 2024—gives it negotiation leverage. Use of performance bonds and multi-vendor sourcing partially mitigates supplier concentration risk.

Building materials and ESG specifications

High-grade materials, complex façade systems and LEED/BREEAM-led green tech increase specification rigidity, strengthening supplier bargaining power; steel, cement and MEP items can represent ~40% of core construction costs and experienced c.20% price volatility into 2024, squeezing margins. Framework contracts and hedging have reduced price swings but do not remove long lead-time risks, while tightening sustainability codes heighten reliance on specialized suppliers.

Utilities, property tech, and FM services

Premium assets demand reliable utilities, smart-building systems and top-tier FM; vendor differentiation in proptech and energy optimization concentrates reliance on a few specialists, while long-term O&M contracts (typically 5–15 years) can entrench suppliers and raise switching costs; competitive bidding and strict performance KPIs help contain costs and preserve negotiating leverage.

- Dependence: few specialized proptech/energy vendors

- Contracts: long O&M terms 5–15 years

- Mitigants: competitive tendering, KPI-linked fees

- Risk: vendor lock-in raises supplier power

Financing providers and rating sensitivity

Development and refinancing needs expose Hongkong Land to banks and capital markets pricing power, with rising benchmark yields compressing project IRRs; US 10-year yields averaged about 4.5% in mid-2024, increasing discount rates and financing costs. A strong balance sheet and long-standing reputation improve access and borrowing terms, while diversified funding across bonds, loans and JVs reduces single-lender leverage.

- Banks & markets set pricing

- US 10y ~4.5% (mid-2024) raises discount rates

- Strong balance sheet = better terms

- Funding mix: bonds, loans, JVs lowers concentration

Constrained CBD land and scarce prime sites push supplier premiums and tighten development margins

In 2024 constrained CBD land allocation and scarce prime sites gave suppliers (land vendors, tier‑1 contractors, specialist proptech/green suppliers) elevated bargaining power, raising premiums and switching costs. Hongkong Land’s scale (portfolio ~US$19.1bn in 2024) and competitive tendering mitigate but do not eliminate price and lead‑time risks; financing costs (US 10y ~4.5% mid‑2024) also tighten margins.

| Metric | 2024 value |

|---|---|

| Portfolio value | US$19.1bn |

| US 10y | ~4.5% |

| Construction cost share | ~40% |

| Price volatility | ~20% |

| Tender premiums | mid‑teens% |

| O&M terms | 5–15 yrs |

What is included in the product

Concise Porter's Five Forces analysis tailored to Hongkong Land, assessing competitive rivalry, supplier and buyer power, barriers to entry and threat of substitutes, and highlighting industry-specific drivers, disruptive threats, and implications for pricing and profitability.

Condensed Porter's Five Forces for Hongkong Land—visualize competitive intensity, tenant and supplier bargaining power, threat of new entrants and substitutes, plus regulatory risk in one clear sheet to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Anchor MNC office tenants

Blue-chip MNCs prize Hongkong Land’s central, prestige campuses and integrated services, reducing price sensitivity; Hongkong Land reported c.95% occupancy across its Hong Kong office portfolio in 2024, underscoring stickiness. Their scale and creditworthiness, however, secure rent negotiation power and fit-out incentives, often yielding upfront concessions. Long leases cut churn but concentrate incentives early. Flight-to-quality lifted demand for Grade A space through 2024.

Luxury retail brands

Flagship luxury retailers seek prime frontage and curated tenant mix in Hongkong Land assets, reducing substitutability and reinforcing bargaining power; Cushman & Wakefield (2024) ranks Hong Kong among the top three most expensive retail high streets globally. Top brands command favorable terms and marketing support because they drive footfall and halo effects; Bain (2024) pegs the global personal luxury goods market near €330bn. Percentage-rent structures share upside but introduce revenue volatility, while co-investment in experiences and joint marketing aligns landlord-tenant interests and risk-reward.

Residential buyers in premium segments

High-end buyers demand design, location and developer reputation, tempering price elasticity; Hongkong Land's heritage since 1889 underpins pricing power in downturns. Pre-sales lower funding risk but increase buyer leverage on specs and timelines. Macro rates—US Fed funds at 5.25–5.50% in 2024—can swiftly tilt bargaining power via mortgage costs and sentiment shifts.

Corporate and co-working demand

Flex-space operators aggregate many small occupiers, concentrating negotiating power as coworking supply in Hong Kong grew ~15% in 2024, pressuring landlords to offer shorter terms and incentives. Corporates adopting hybrid work—around 60% of firms in 2024 surveys—are reassessing footprints, demanding expansion/contraction rights that can cut effective rents by up to low‑double digits. Amenity-rich, tech-enabled assets help Hongkong Land defend yields and retain corporate tenants.

- Aggregated demand: flex operators concentrate small tenants

- Hybrid adoption ~60% (2024) drives flexibility demands

- Shorter terms/rights can trim effective rents by low‑double digits

- Amenity-rich buildings support yield protection

Geographic diversification of demand

Geographic diversification across Hong Kong, Singapore and Mainland China broadens tenant pools and reduces dependence on any single market’s bargaining power, though simultaneous regional slowdowns can compress rents across the portfolio.

Strong cross-market brand recognition supports leasing and retention, while differing currency regimes and local regulations create asymmetric negotiating leverage for tenants in each jurisdiction.

- Diversified tenant base across three markets

- Systemic slowdowns can synchronize pricing pressure

- Brand strength improves lease terms

- Currency and regulatory gaps affect local bargaining

HK pricing: office occ 95%, flex supply pressures rents

Blue-chip tenants and luxury retailers give Hongkong Land pricing power; Hong Kong office occupancy ~95% (2024) and retail ranks top‑3 globally (Cushman & Wakefield 2024). Flex operators and hybrid work (~60% adoption in 2024) concentrated bargaining, coworking supply +15% (2024) pressuring incentives. Cross‑market scale and brand mitigate but macro rates (Fed 5.25–5.50% 2024) shift leverage.

| Metric | 2024 | Impact |

|---|---|---|

| HK office occ. | ~95% | High stickiness |

| Hybrid adoption | ~60% | Flex demands |

| Coworking supply | +15% | Incentive pressure |

Preview the Actual Deliverable

Hongkong Land Porter's Five Forces Analysis

This preview shows the exact Hongkong Land Porter’s Five Forces analysis you'll receive—comprehensive, professionally formatted, and ready for immediate use. The file includes competitive intensity, supplier and buyer power, threats of entry and substitutes, and strategic implications. No placeholders or mockups; purchase grants instant access to this same document.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hongkong Land benefits from a prime portfolio and strong brand, but tenant bargaining and market cyclicality heighten competitive pressure; supplier power is moderate while barriers to entry keep new competitors limited. Substitutes like remote work and regional rivals present manageable risks. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore detailed force ratings, visuals, and strategic recommendations.

Suppliers Bargaining Power

Prime land and approvals gatekept

In 2024 access to CBD land in Hong Kong, Singapore and Beijing remained tightly controlled by governments and a few state-linked entities, elevating suppliers’ bargaining power for developers like Hongkong Land.

Zoning rules, plot ratios and mandatory approvals create dependency on public authorities’ timelines, with tender and approval cycles often stretching beyond 12 months.

Scarcity of prime sites enables land vendors to command significant premiums, while long tender cycles delay pipeline replenishment and raise carrying costs for developers.

Tier-1 contractors and fit-out specialists

Large, complex mixed-use assets require a narrow pool of tier-1 contractors and luxury fit-out firms, raising switching costs and concentrating supply among fewer than a dozen specialist firms in Hong Kong by 2024. Capacity constraints during upcycles have pushed tender premiums up to mid-teens percentage points in recent cycles. Hongkong Land’s scale and repeat spend—with a reported portfolio value near US$19.1bn in 2024—gives it negotiation leverage. Use of performance bonds and multi-vendor sourcing partially mitigates supplier concentration risk.

Building materials and ESG specifications

High-grade materials, complex façade systems and LEED/BREEAM-led green tech increase specification rigidity, strengthening supplier bargaining power; steel, cement and MEP items can represent ~40% of core construction costs and experienced c.20% price volatility into 2024, squeezing margins. Framework contracts and hedging have reduced price swings but do not remove long lead-time risks, while tightening sustainability codes heighten reliance on specialized suppliers.

Utilities, property tech, and FM services

Premium assets demand reliable utilities, smart-building systems and top-tier FM; vendor differentiation in proptech and energy optimization concentrates reliance on a few specialists, while long-term O&M contracts (typically 5–15 years) can entrench suppliers and raise switching costs; competitive bidding and strict performance KPIs help contain costs and preserve negotiating leverage.

- Dependence: few specialized proptech/energy vendors

- Contracts: long O&M terms 5–15 years

- Mitigants: competitive tendering, KPI-linked fees

- Risk: vendor lock-in raises supplier power

Financing providers and rating sensitivity

Development and refinancing needs expose Hongkong Land to banks and capital markets pricing power, with rising benchmark yields compressing project IRRs; US 10-year yields averaged about 4.5% in mid-2024, increasing discount rates and financing costs. A strong balance sheet and long-standing reputation improve access and borrowing terms, while diversified funding across bonds, loans and JVs reduces single-lender leverage.

- Banks & markets set pricing

- US 10y ~4.5% (mid-2024) raises discount rates

- Strong balance sheet = better terms

- Funding mix: bonds, loans, JVs lowers concentration

Constrained CBD land and scarce prime sites push supplier premiums and tighten development margins

In 2024 constrained CBD land allocation and scarce prime sites gave suppliers (land vendors, tier‑1 contractors, specialist proptech/green suppliers) elevated bargaining power, raising premiums and switching costs. Hongkong Land’s scale (portfolio ~US$19.1bn in 2024) and competitive tendering mitigate but do not eliminate price and lead‑time risks; financing costs (US 10y ~4.5% mid‑2024) also tighten margins.

| Metric | 2024 value |

|---|---|

| Portfolio value | US$19.1bn |

| US 10y | ~4.5% |

| Construction cost share | ~40% |

| Price volatility | ~20% |

| Tender premiums | mid‑teens% |

| O&M terms | 5–15 yrs |

What is included in the product

Concise Porter's Five Forces analysis tailored to Hongkong Land, assessing competitive rivalry, supplier and buyer power, barriers to entry and threat of substitutes, and highlighting industry-specific drivers, disruptive threats, and implications for pricing and profitability.

Condensed Porter's Five Forces for Hongkong Land—visualize competitive intensity, tenant and supplier bargaining power, threat of new entrants and substitutes, plus regulatory risk in one clear sheet to speed strategic decisions and relieve analysis bottlenecks.

Customers Bargaining Power

Anchor MNC office tenants

Blue-chip MNCs prize Hongkong Land’s central, prestige campuses and integrated services, reducing price sensitivity; Hongkong Land reported c.95% occupancy across its Hong Kong office portfolio in 2024, underscoring stickiness. Their scale and creditworthiness, however, secure rent negotiation power and fit-out incentives, often yielding upfront concessions. Long leases cut churn but concentrate incentives early. Flight-to-quality lifted demand for Grade A space through 2024.

Luxury retail brands

Flagship luxury retailers seek prime frontage and curated tenant mix in Hongkong Land assets, reducing substitutability and reinforcing bargaining power; Cushman & Wakefield (2024) ranks Hong Kong among the top three most expensive retail high streets globally. Top brands command favorable terms and marketing support because they drive footfall and halo effects; Bain (2024) pegs the global personal luxury goods market near €330bn. Percentage-rent structures share upside but introduce revenue volatility, while co-investment in experiences and joint marketing aligns landlord-tenant interests and risk-reward.

Residential buyers in premium segments

High-end buyers demand design, location and developer reputation, tempering price elasticity; Hongkong Land's heritage since 1889 underpins pricing power in downturns. Pre-sales lower funding risk but increase buyer leverage on specs and timelines. Macro rates—US Fed funds at 5.25–5.50% in 2024—can swiftly tilt bargaining power via mortgage costs and sentiment shifts.

Corporate and co-working demand

Flex-space operators aggregate many small occupiers, concentrating negotiating power as coworking supply in Hong Kong grew ~15% in 2024, pressuring landlords to offer shorter terms and incentives. Corporates adopting hybrid work—around 60% of firms in 2024 surveys—are reassessing footprints, demanding expansion/contraction rights that can cut effective rents by up to low‑double digits. Amenity-rich, tech-enabled assets help Hongkong Land defend yields and retain corporate tenants.

- Aggregated demand: flex operators concentrate small tenants

- Hybrid adoption ~60% (2024) drives flexibility demands

- Shorter terms/rights can trim effective rents by low‑double digits

- Amenity-rich buildings support yield protection

Geographic diversification of demand

Geographic diversification across Hong Kong, Singapore and Mainland China broadens tenant pools and reduces dependence on any single market’s bargaining power, though simultaneous regional slowdowns can compress rents across the portfolio.

Strong cross-market brand recognition supports leasing and retention, while differing currency regimes and local regulations create asymmetric negotiating leverage for tenants in each jurisdiction.

- Diversified tenant base across three markets

- Systemic slowdowns can synchronize pricing pressure

- Brand strength improves lease terms

- Currency and regulatory gaps affect local bargaining

HK pricing: office occ 95%, flex supply pressures rents

Blue-chip tenants and luxury retailers give Hongkong Land pricing power; Hong Kong office occupancy ~95% (2024) and retail ranks top‑3 globally (Cushman & Wakefield 2024). Flex operators and hybrid work (~60% adoption in 2024) concentrated bargaining, coworking supply +15% (2024) pressuring incentives. Cross‑market scale and brand mitigate but macro rates (Fed 5.25–5.50% 2024) shift leverage.

| Metric | 2024 | Impact |

|---|---|---|

| HK office occ. | ~95% | High stickiness |

| Hybrid adoption | ~60% | Flex demands |

| Coworking supply | +15% | Incentive pressure |

Preview the Actual Deliverable

Hongkong Land Porter's Five Forces Analysis

This preview shows the exact Hongkong Land Porter’s Five Forces analysis you'll receive—comprehensive, professionally formatted, and ready for immediate use. The file includes competitive intensity, supplier and buyer power, threats of entry and substitutes, and strategic implications. No placeholders or mockups; purchase grants instant access to this same document.