HKT Trust and HKT Porter's Five Forces Analysis

Don't Miss the Bigger Picture

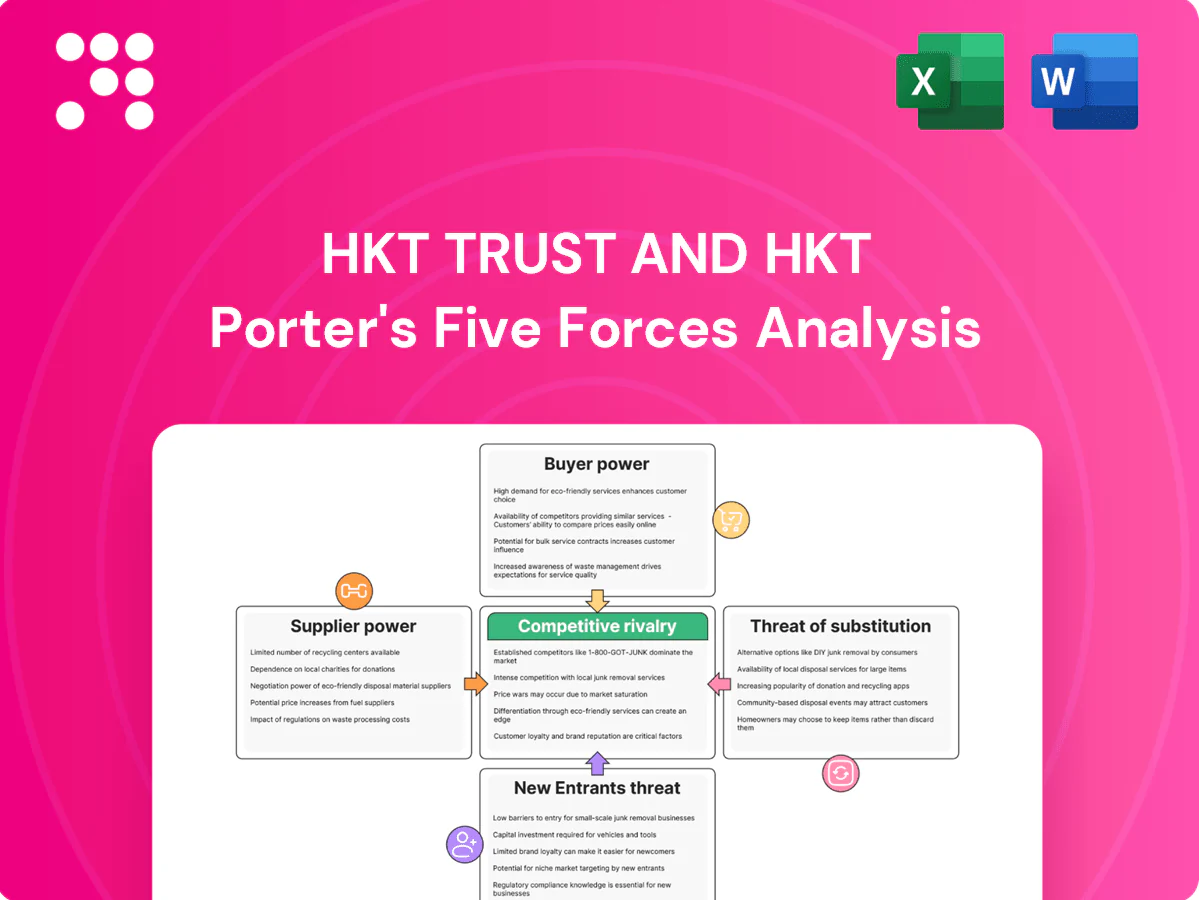

HKT Trust and HKT face a complex telecom ecosystem—this brief outlines supplier and buyer pressures, substitute threats, entry barriers, and rival intensity shaping their margins. Our Porter's Five Forces snapshot highlights where strategic risk and opportunity concentrate. Ready to dig deeper? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Spectrum and regulatory dependence

OFCA controls spectrum licensing, pricing and renewal, concentrating supplier power over a critical input and shaping HKT’s cost base; auctions and annual usage fees feed into capex and capacity planning in a market serving ~7.5 million residents (2024). Policy shifts such as refarming and mid-band/mmWave allocations can shift competitive parity and delay or accelerate HKT’s capex, while compliance and QoS mandates limit HKT’s negotiating leverage.

Network equipment vendor concentration

Core RAN and transport gear remain concentrated: the top three vendors held roughly 70–80% of the global RAN market in 2024, constraining HKT’s switching options. Interoperability, divergent software roadmaps and security certifications create material lock-in and switching costs. Export controls and supply-chain shocks since 2022 have increased lead times and prices for operators. HKT’s multi-vendor sourcing mitigates risk, but supplier bargaining is balanced to slightly unfavorable.

Towers, sites, and real estate landlords

Site access in dense Hong Kong (7.4 million people across 1,106 km2, ~6,700/km2) constrains supply, giving landlords and public bodies leverage on rents and terms. Rooftop rights, street furniture and in‑building DAS permissions create bottlenecks for deployment. 5G small‑cell densification increases dependence on municipal permits. Long‑term leases mitigate but renewal risk keeps supplier power moderate.

Content and media rights holders

Premium video and sports rights holders exert high leverage via exclusivity and few alternatives; the global sports rights market was roughly US$58bn in 2024, keeping marquee rights costly and driving content inflation above ARPU growth for many pay-TV bundles.

HKT can partially offset by in-house and aggregated content, but negotiation cycles, windowing terms and multi-year escalators compress margins and complicate scheduling.

- Rights market 2024: ~US$58bn

- Content inflation > ARPU for pay-TV peers in 2023–24

- Own/aggregated content reduces but does not eliminate marquee-cost exposure

Cloud, IT, and fintech partners

Enterprise solutions rely on hyperscalers, cybersecurity vendors, and payment networks; hyperscalers held about 33% (AWS), 22% (Azure), 11% (GCP) share in 2024 per Synergy Research Group. Certifications, data residency and integration requirements raise switching costs and limit substitution. Co-selling and revenue shares shift economics toward partners, so supplier power is moderate despite HKT’s diversified ecosystem.

- High switching costs: certifications, data residency, integrations

- Partner economics: co-selling, revenue share reduce margins

- Diversification: multiple vendors lower concentration risk

Regulatory control, RAN 70–80% lock‑in; hyperscalers AWS33%/Azure22%/GCP11% pressure

Spectrum licensing and OFCA rules (market ~7.5m residents) concentrate regulatory supplier power and shape capex; top‑3 RAN vendors held ~70–80% of 2024 market, creating lock‑in and higher switching costs. Site landlords and permits in 1,106 km2 Hong Kong tighten deployment leverage; sports rights (~US$58bn global 2024) and hyperscaler dependence (AWS33%, Azure22%, GCP11% in 2024) keep supplier power moderately unfavorable.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Regulator (spectrum) | 7.5m pop market | High capex influence |

| RAN vendors | 70–80% top3 share | Lock‑in, higher prices |

| Content rights | US$58bn global | High cost pressure |

| Hyperscalers | AWS33/Azure22/GCP11% | Moderate dependence |

What is included in the product

Comprehensive Porter's Five Forces analysis for HKT Trust and HKT that uncovers key competitive drivers, buyer/supplier power, substitutes, entrant threats and industry rivalry with data-backed strategic commentary. Tailored insights on disruptive risks, pricing influence and incumbency protections, deliverable in editable Word for investor materials, strategy decks or academic use.

A clear one-sheet summary of HKT Trust’s Porter's Five Forces—perfect for quick decision-making and boardroom slides; customize pressure levels and swap in your own data to reflect regulatory or market changes, with instant spider/radar visualization and no complex code.

Customers Bargaining Power

High consumer price sensitivity

Hong Kong’s mobile and broadband markets are mature and deal-seeking, with mobile penetration exceeding 200% in 2024, driving fierce price competition. Transparent tariffs and frequent promotions amplify switching incentives, while discounts and handset subsidies raise acquisition costs and compress ARPU. Bundling can temper price pressure but must deliver clear, measurable value to retain customers.

Number portability and low switching costs

Simple mobile number portability and HKT’s dense retail footprint enable rapid churn, while SIM-only plans and growing eSIM adoption further reduce switching friction. HKT therefore must increase investment in retention, loyalty programs and converged broadband-TV-mobile bundles to defend share. Effective churn management materially affects ARPU and margin, making customer lifetime value the key profitability driver.

Powerful enterprise procurement

Large corporates and public sector buyers run competitive tenders across connectivity, cloud and managed services, forcing HKT to accept keen pricing on multi-year contracts (typically 3–5 years) that improve revenue visibility but compress margins; stringent SLAs and customization raise delivery costs. In 2024, enterprise RFPs remain the primary sourcing route, while value-added integration and cybersecurity services help HKT retain pricing power and reduce churn.

MVNO-driven alternatives

Multiple MVNOs in Hong Kong anchor price expectations with budget plans, raising end-customer bargaining power even when they lease capacity from MNOs; HKT must leverage superior network quality, 5G features and differentiated service to sustain ARPU and churn control.

Regulatory and consumer advocacy

Regulatory and consumer advocacy in Hong Kong strengthen buyer leverage by enforcing tariff transparency and strong consumer protections, with complaint mechanisms and QoS disclosures raising accountability and reducing churn risk for HKT. Bill shock safeguards and fair‑usage rules limit monetization flexibility, prompting HKT to prioritize clearer communications and CX investments to retain subscribers.

- Tariff transparency boosts buyer power

- QoS disclosures increase oversight

- Bill shock safeguards cap upselling

- HKT responds with clearer communications

Hong Kong mobile penetration >200% compresses ARPU, fuels churn

Hong Kong mobile penetration >200% in 2024 drives intense price sensitivity and frequent switching, compressing ARPU and margins. Simple portability, eSIM growth and dense retail accelerate churn, forcing higher retention spend. Enterprise tenders (typical 3–5 year contracts) boost revenue visibility but tighten pricing; MVNOs and regulation further elevate buyer leverage.

| Metric | 2024 Value |

|---|---|

| Mobile penetration | >200% |

| Enterprise contract length | 3–5 years |

Full Version Awaits

HKT Trust and HKT Porter's Five Forces Analysis

This HKT Trust report delivers a concise strategic and financial overview plus a full Porter’s Five Forces analysis assessing industry rivalry, supplier and buyer power, threat of new entrants, and substitutes specific to HKT’s telecom and services mix. The analysis highlights key competitive pressures, regulatory considerations, and strategic implications for investors and managers. This preview is the exact, fully formatted document you will receive immediately after purchase.

Don't Miss the Bigger Picture

HKT Trust and HKT face a complex telecom ecosystem—this brief outlines supplier and buyer pressures, substitute threats, entry barriers, and rival intensity shaping their margins. Our Porter's Five Forces snapshot highlights where strategic risk and opportunity concentrate. Ready to dig deeper? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Spectrum and regulatory dependence

OFCA controls spectrum licensing, pricing and renewal, concentrating supplier power over a critical input and shaping HKT’s cost base; auctions and annual usage fees feed into capex and capacity planning in a market serving ~7.5 million residents (2024). Policy shifts such as refarming and mid-band/mmWave allocations can shift competitive parity and delay or accelerate HKT’s capex, while compliance and QoS mandates limit HKT’s negotiating leverage.

Network equipment vendor concentration

Core RAN and transport gear remain concentrated: the top three vendors held roughly 70–80% of the global RAN market in 2024, constraining HKT’s switching options. Interoperability, divergent software roadmaps and security certifications create material lock-in and switching costs. Export controls and supply-chain shocks since 2022 have increased lead times and prices for operators. HKT’s multi-vendor sourcing mitigates risk, but supplier bargaining is balanced to slightly unfavorable.

Towers, sites, and real estate landlords

Site access in dense Hong Kong (7.4 million people across 1,106 km2, ~6,700/km2) constrains supply, giving landlords and public bodies leverage on rents and terms. Rooftop rights, street furniture and in‑building DAS permissions create bottlenecks for deployment. 5G small‑cell densification increases dependence on municipal permits. Long‑term leases mitigate but renewal risk keeps supplier power moderate.

Content and media rights holders

Premium video and sports rights holders exert high leverage via exclusivity and few alternatives; the global sports rights market was roughly US$58bn in 2024, keeping marquee rights costly and driving content inflation above ARPU growth for many pay-TV bundles.

HKT can partially offset by in-house and aggregated content, but negotiation cycles, windowing terms and multi-year escalators compress margins and complicate scheduling.

- Rights market 2024: ~US$58bn

- Content inflation > ARPU for pay-TV peers in 2023–24

- Own/aggregated content reduces but does not eliminate marquee-cost exposure

Cloud, IT, and fintech partners

Enterprise solutions rely on hyperscalers, cybersecurity vendors, and payment networks; hyperscalers held about 33% (AWS), 22% (Azure), 11% (GCP) share in 2024 per Synergy Research Group. Certifications, data residency and integration requirements raise switching costs and limit substitution. Co-selling and revenue shares shift economics toward partners, so supplier power is moderate despite HKT’s diversified ecosystem.

- High switching costs: certifications, data residency, integrations

- Partner economics: co-selling, revenue share reduce margins

- Diversification: multiple vendors lower concentration risk

Regulatory control, RAN 70–80% lock‑in; hyperscalers AWS33%/Azure22%/GCP11% pressure

Spectrum licensing and OFCA rules (market ~7.5m residents) concentrate regulatory supplier power and shape capex; top‑3 RAN vendors held ~70–80% of 2024 market, creating lock‑in and higher switching costs. Site landlords and permits in 1,106 km2 Hong Kong tighten deployment leverage; sports rights (~US$58bn global 2024) and hyperscaler dependence (AWS33%, Azure22%, GCP11% in 2024) keep supplier power moderately unfavorable.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Regulator (spectrum) | 7.5m pop market | High capex influence |

| RAN vendors | 70–80% top3 share | Lock‑in, higher prices |

| Content rights | US$58bn global | High cost pressure |

| Hyperscalers | AWS33/Azure22/GCP11% | Moderate dependence |

What is included in the product

Comprehensive Porter's Five Forces analysis for HKT Trust and HKT that uncovers key competitive drivers, buyer/supplier power, substitutes, entrant threats and industry rivalry with data-backed strategic commentary. Tailored insights on disruptive risks, pricing influence and incumbency protections, deliverable in editable Word for investor materials, strategy decks or academic use.

A clear one-sheet summary of HKT Trust’s Porter's Five Forces—perfect for quick decision-making and boardroom slides; customize pressure levels and swap in your own data to reflect regulatory or market changes, with instant spider/radar visualization and no complex code.

Customers Bargaining Power

High consumer price sensitivity

Hong Kong’s mobile and broadband markets are mature and deal-seeking, with mobile penetration exceeding 200% in 2024, driving fierce price competition. Transparent tariffs and frequent promotions amplify switching incentives, while discounts and handset subsidies raise acquisition costs and compress ARPU. Bundling can temper price pressure but must deliver clear, measurable value to retain customers.

Number portability and low switching costs

Simple mobile number portability and HKT’s dense retail footprint enable rapid churn, while SIM-only plans and growing eSIM adoption further reduce switching friction. HKT therefore must increase investment in retention, loyalty programs and converged broadband-TV-mobile bundles to defend share. Effective churn management materially affects ARPU and margin, making customer lifetime value the key profitability driver.

Powerful enterprise procurement

Large corporates and public sector buyers run competitive tenders across connectivity, cloud and managed services, forcing HKT to accept keen pricing on multi-year contracts (typically 3–5 years) that improve revenue visibility but compress margins; stringent SLAs and customization raise delivery costs. In 2024, enterprise RFPs remain the primary sourcing route, while value-added integration and cybersecurity services help HKT retain pricing power and reduce churn.

MVNO-driven alternatives

Multiple MVNOs in Hong Kong anchor price expectations with budget plans, raising end-customer bargaining power even when they lease capacity from MNOs; HKT must leverage superior network quality, 5G features and differentiated service to sustain ARPU and churn control.

Regulatory and consumer advocacy

Regulatory and consumer advocacy in Hong Kong strengthen buyer leverage by enforcing tariff transparency and strong consumer protections, with complaint mechanisms and QoS disclosures raising accountability and reducing churn risk for HKT. Bill shock safeguards and fair‑usage rules limit monetization flexibility, prompting HKT to prioritize clearer communications and CX investments to retain subscribers.

- Tariff transparency boosts buyer power

- QoS disclosures increase oversight

- Bill shock safeguards cap upselling

- HKT responds with clearer communications

Hong Kong mobile penetration >200% compresses ARPU, fuels churn

Hong Kong mobile penetration >200% in 2024 drives intense price sensitivity and frequent switching, compressing ARPU and margins. Simple portability, eSIM growth and dense retail accelerate churn, forcing higher retention spend. Enterprise tenders (typical 3–5 year contracts) boost revenue visibility but tighten pricing; MVNOs and regulation further elevate buyer leverage.

| Metric | 2024 Value |

|---|---|

| Mobile penetration | >200% |

| Enterprise contract length | 3–5 years |

Full Version Awaits

HKT Trust and HKT Porter's Five Forces Analysis

This HKT Trust report delivers a concise strategic and financial overview plus a full Porter’s Five Forces analysis assessing industry rivalry, supplier and buyer power, threat of new entrants, and substitutes specific to HKT’s telecom and services mix. The analysis highlights key competitive pressures, regulatory considerations, and strategic implications for investors and managers. This preview is the exact, fully formatted document you will receive immediately after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

HKT Trust and HKT face a complex telecom ecosystem—this brief outlines supplier and buyer pressures, substitute threats, entry barriers, and rival intensity shaping their margins. Our Porter's Five Forces snapshot highlights where strategic risk and opportunity concentrate. Ready to dig deeper? Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights.

Suppliers Bargaining Power

Spectrum and regulatory dependence

OFCA controls spectrum licensing, pricing and renewal, concentrating supplier power over a critical input and shaping HKT’s cost base; auctions and annual usage fees feed into capex and capacity planning in a market serving ~7.5 million residents (2024). Policy shifts such as refarming and mid-band/mmWave allocations can shift competitive parity and delay or accelerate HKT’s capex, while compliance and QoS mandates limit HKT’s negotiating leverage.

Network equipment vendor concentration

Core RAN and transport gear remain concentrated: the top three vendors held roughly 70–80% of the global RAN market in 2024, constraining HKT’s switching options. Interoperability, divergent software roadmaps and security certifications create material lock-in and switching costs. Export controls and supply-chain shocks since 2022 have increased lead times and prices for operators. HKT’s multi-vendor sourcing mitigates risk, but supplier bargaining is balanced to slightly unfavorable.

Towers, sites, and real estate landlords

Site access in dense Hong Kong (7.4 million people across 1,106 km2, ~6,700/km2) constrains supply, giving landlords and public bodies leverage on rents and terms. Rooftop rights, street furniture and in‑building DAS permissions create bottlenecks for deployment. 5G small‑cell densification increases dependence on municipal permits. Long‑term leases mitigate but renewal risk keeps supplier power moderate.

Content and media rights holders

Premium video and sports rights holders exert high leverage via exclusivity and few alternatives; the global sports rights market was roughly US$58bn in 2024, keeping marquee rights costly and driving content inflation above ARPU growth for many pay-TV bundles.

HKT can partially offset by in-house and aggregated content, but negotiation cycles, windowing terms and multi-year escalators compress margins and complicate scheduling.

- Rights market 2024: ~US$58bn

- Content inflation > ARPU for pay-TV peers in 2023–24

- Own/aggregated content reduces but does not eliminate marquee-cost exposure

Cloud, IT, and fintech partners

Enterprise solutions rely on hyperscalers, cybersecurity vendors, and payment networks; hyperscalers held about 33% (AWS), 22% (Azure), 11% (GCP) share in 2024 per Synergy Research Group. Certifications, data residency and integration requirements raise switching costs and limit substitution. Co-selling and revenue shares shift economics toward partners, so supplier power is moderate despite HKT’s diversified ecosystem.

- High switching costs: certifications, data residency, integrations

- Partner economics: co-selling, revenue share reduce margins

- Diversification: multiple vendors lower concentration risk

Regulatory control, RAN 70–80% lock‑in; hyperscalers AWS33%/Azure22%/GCP11% pressure

Spectrum licensing and OFCA rules (market ~7.5m residents) concentrate regulatory supplier power and shape capex; top‑3 RAN vendors held ~70–80% of 2024 market, creating lock‑in and higher switching costs. Site landlords and permits in 1,106 km2 Hong Kong tighten deployment leverage; sports rights (~US$58bn global 2024) and hyperscaler dependence (AWS33%, Azure22%, GCP11% in 2024) keep supplier power moderately unfavorable.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Regulator (spectrum) | 7.5m pop market | High capex influence |

| RAN vendors | 70–80% top3 share | Lock‑in, higher prices |

| Content rights | US$58bn global | High cost pressure |

| Hyperscalers | AWS33/Azure22/GCP11% | Moderate dependence |

What is included in the product

Comprehensive Porter's Five Forces analysis for HKT Trust and HKT that uncovers key competitive drivers, buyer/supplier power, substitutes, entrant threats and industry rivalry with data-backed strategic commentary. Tailored insights on disruptive risks, pricing influence and incumbency protections, deliverable in editable Word for investor materials, strategy decks or academic use.

A clear one-sheet summary of HKT Trust’s Porter's Five Forces—perfect for quick decision-making and boardroom slides; customize pressure levels and swap in your own data to reflect regulatory or market changes, with instant spider/radar visualization and no complex code.

Customers Bargaining Power

High consumer price sensitivity

Hong Kong’s mobile and broadband markets are mature and deal-seeking, with mobile penetration exceeding 200% in 2024, driving fierce price competition. Transparent tariffs and frequent promotions amplify switching incentives, while discounts and handset subsidies raise acquisition costs and compress ARPU. Bundling can temper price pressure but must deliver clear, measurable value to retain customers.

Number portability and low switching costs

Simple mobile number portability and HKT’s dense retail footprint enable rapid churn, while SIM-only plans and growing eSIM adoption further reduce switching friction. HKT therefore must increase investment in retention, loyalty programs and converged broadband-TV-mobile bundles to defend share. Effective churn management materially affects ARPU and margin, making customer lifetime value the key profitability driver.

Powerful enterprise procurement

Large corporates and public sector buyers run competitive tenders across connectivity, cloud and managed services, forcing HKT to accept keen pricing on multi-year contracts (typically 3–5 years) that improve revenue visibility but compress margins; stringent SLAs and customization raise delivery costs. In 2024, enterprise RFPs remain the primary sourcing route, while value-added integration and cybersecurity services help HKT retain pricing power and reduce churn.

MVNO-driven alternatives

Multiple MVNOs in Hong Kong anchor price expectations with budget plans, raising end-customer bargaining power even when they lease capacity from MNOs; HKT must leverage superior network quality, 5G features and differentiated service to sustain ARPU and churn control.

Regulatory and consumer advocacy

Regulatory and consumer advocacy in Hong Kong strengthen buyer leverage by enforcing tariff transparency and strong consumer protections, with complaint mechanisms and QoS disclosures raising accountability and reducing churn risk for HKT. Bill shock safeguards and fair‑usage rules limit monetization flexibility, prompting HKT to prioritize clearer communications and CX investments to retain subscribers.

- Tariff transparency boosts buyer power

- QoS disclosures increase oversight

- Bill shock safeguards cap upselling

- HKT responds with clearer communications

Hong Kong mobile penetration >200% compresses ARPU, fuels churn

Hong Kong mobile penetration >200% in 2024 drives intense price sensitivity and frequent switching, compressing ARPU and margins. Simple portability, eSIM growth and dense retail accelerate churn, forcing higher retention spend. Enterprise tenders (typical 3–5 year contracts) boost revenue visibility but tighten pricing; MVNOs and regulation further elevate buyer leverage.

| Metric | 2024 Value |

|---|---|

| Mobile penetration | >200% |

| Enterprise contract length | 3–5 years |

Full Version Awaits

HKT Trust and HKT Porter's Five Forces Analysis

This HKT Trust report delivers a concise strategic and financial overview plus a full Porter’s Five Forces analysis assessing industry rivalry, supplier and buyer power, threat of new entrants, and substitutes specific to HKT’s telecom and services mix. The analysis highlights key competitive pressures, regulatory considerations, and strategic implications for investors and managers. This preview is the exact, fully formatted document you will receive immediately after purchase.