Hargreaves Lansdown Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

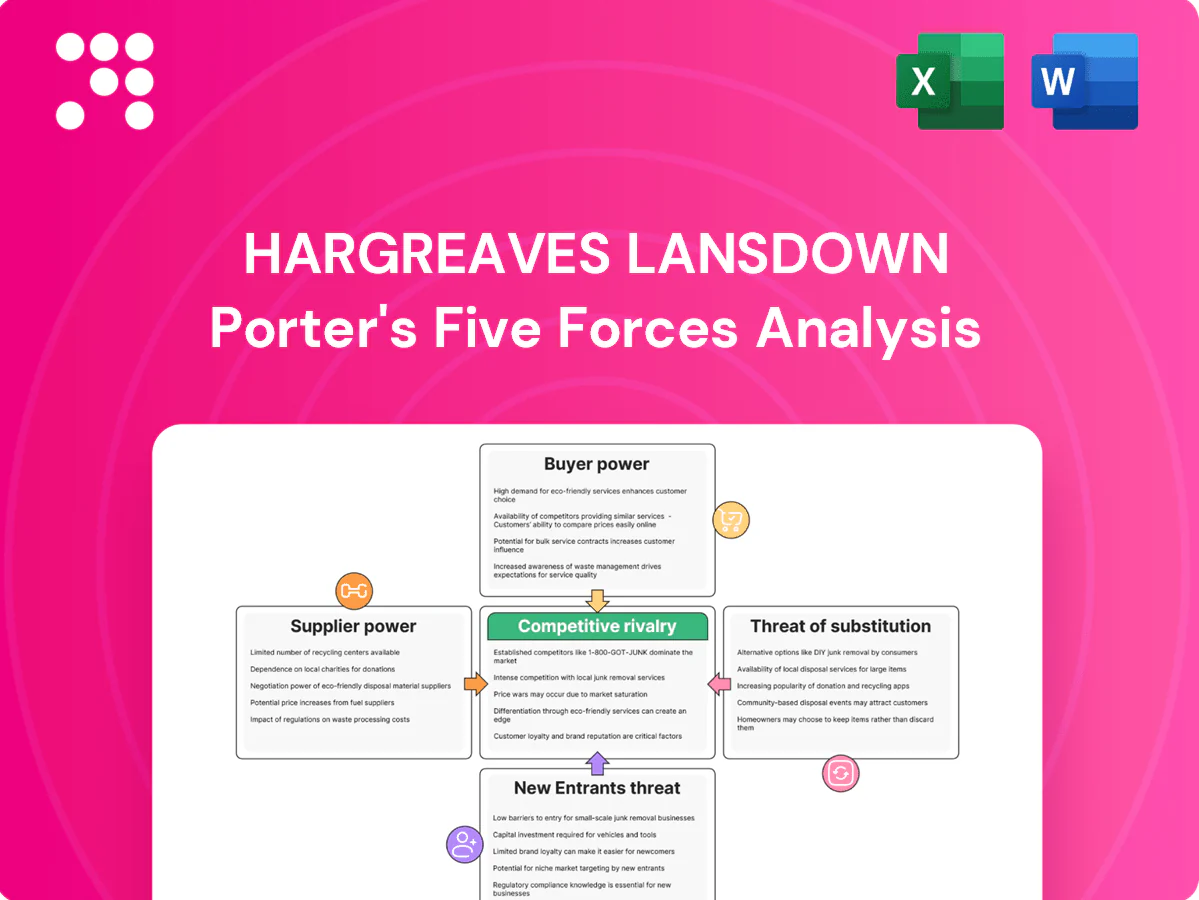

Hargreaves Lansdown faces moderate buyer power, intense industry rivalry, low supplier leverage, growing fintech substitute threats, and significant regulatory barriers; its scale and brand are key defenses but disruption risks persist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hargreaves Lansdown’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated fund and ETF providers

Hargreaves Lansdown relies on major asset managers for flagship funds and ETFs, giving big providers leverage over shelf placement and commercial terms, yet HL's distribution scale — c.1.6m clients and c.£114bn AUA in 2024 — tempers that power. Product substitution within fund and ETF categories limits any single provider's dominance. Co-marketing deals and prioritized platform lists act as negotiation levers for both HL and managers.

Market data and research vendors

Essential data feeds, ratings and research largely come from a small set of vendors (Bloomberg, Refinitiv, Morningstar), with Bloomberg terminals costing about $24,000/year (2024), raising switching costs for HL. Outages or price hikes can compress margins and affect service levels; vendor fee increases of even a few percent hit scale. HL mitigates via multi-sourcing and in-house analytics, but long-term contracts lock pricing while reducing flexibility.

Custody, clearing, and payments infrastructure

Settlement, custody and cash management rely on a small set of regulated counterparties and banks; in 2024 the top five UK banks held c.70% of domestic banking assets, reinforcing their systemic importance and bargaining leverage over service levels and fees. Regulatory constraints on custody switching and settlement finality limit HL’s agility, while scale-based pricing and partnerships across multiple custodians partially mitigate supplier power.

Cloud, cybersecurity, and core tech providers

Mission-critical hosting, security and platform tooling for HL depend on large providers (AWS 32%, Microsoft Azure 23%, Google Cloud 11% global market share in 2024), whose standardized pricing and vendor concentration increase dependency and resilience risk. HL can secure volume discounts but remains exposed to platform changes; building internal capabilities reduces lock-in over time.

- Vendor concentration: high (AWS/Azure/GCP ~66% combined)

- Dependency: resilience and change risk

- Levers: volume discounts

- Mitigation: internal platform investments

Regulators as quasi-suppliers

Regulators act as quasi-suppliers for Hargreaves Lansdown: FCA rule changes such as Consumer Duty (full implementation July 2024) and HMRC-set product limits (ISA allowance £20,000 for 2024/25) effectively supply permissions that reshape product design and revenue models; compliance increases operating costs and complexity, while proactive engagement can influence implementation timelines and regulatory detail.

- Consumer Duty: July 2024

- ISA limit: £20,000 (2024/25)

- Compliance raises OPEX and barrier-to-entry for challengers

Supplier power caps fees and shelf access; £114bn AUA

Hargreaves Lansdown faces concentrated supplier power from major asset managers despite its scale (c.1.6m clients, £114bn AUA in 2024), constraining fees and shelf placement. Critical data vendors (Bloomberg ~$24,000/yr) and dominant cloud providers (AWS 32%, Azure 23%, GCP 11% in 2024) raise switching costs. Banking/custody concentration (top5 UK banks ~70% assets) and regulatory suppliers (Consumer Duty Jul 2024; ISA £20,000 2024/25) further limit flexibility.

| Supplier | Key fact | 2024 metric |

|---|---|---|

| Clients/AUA | Scale | 1.6m / £114bn |

| Data vendor | Cost | Bloomberg ~$24,000/yr |

| Cloud | Market share | AWS32%/Azure23%/GCP11% |

| Banks | Concentration | Top5 ~70% |

| Regulation | Limits | Consumer Duty Jul 2024; ISA £20,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Hargreaves Lansdown highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus disruptive risks and strategic implications.

One-sheet Porter's Five Forces for Hargreaves Lansdown—instantly highlights strategic pressures with a clean radar chart and editable labels, so teams can adapt scenario tabs, copy straight into decks, and make faster decisions without complex tools.

Customers Bargaining Power

Price-sensitive retail investors

Price-sensitive retail investors actively compare platform fees (commonly in the 0.25–0.45% range), FX charges and fund ongoing charges, putting downward pressure on HL’s pricing. The rise of low-cost rivals and passive fund adoption increases sensitivity, forcing HL to justify higher fees via superior service, research tools and competitive cash rates. Transparent pricing and clear value communication are critical to retention.

Low switching frictions improving

ISA and SIPP transfers historically created inertia for Hargreaves Lansdown clients, but since 2024 digital processes and e-signatures have materially shortened move times; the ISA annual allowance for 2024/25 remains £20,000, keeping flows significant. Promotions and transfer-in incentives amplify buyer leverage, while FCA scrutiny of exit fees reduces lock-in. Faster transfers increase the need for continuous value delivery to retain assets.

Multi-homing across platforms

Many UK investors multi-home—about 40% in 2024—diluting platform exclusivity and enabling cherry-picking of the cheapest trades, funds or cash rates; Hargreaves Lansdown, with AUA around £126.6bn (Sept 2024), must compete product-by-product rather than by customer, making cross-selling and ecosystem stickiness key strategic priorities.

Demand for UX, tools, and service

Buyers now demand intuitive apps, real-time data and responsive support; Hargreaves Lansdown serves about 1.6m clients with c.£118bn AUA in 2024, so service lapses cause immediate churn risk and social media backlash. Superior research and guidance reduce pure price sensitivity, while continuous feature upgrades are treated as hygiene, not differentiator.

- UX: real-time pricing, portfolio sync

- Churn: rapid after poor support

- Value: research offsets price wars

- Product: continuous updates expected

Sophisticated segments negotiating value

Defend £126.6bn as ~40% retail multi-homing rises

Retail clients are highly price-sensitive, pressuring HL to defend fees with service and research; about 1.6m clients and AUA £126.6bn (Sept 2024) concentrate bargaining power in high-balance cohorts. Multi-homing (~40% in 2024) and faster digital ISA/SIPP transfers raise churn risk, making continuous product and UX upgrades essential.

| Metric | 2024 |

|---|---|

| Clients | 1.6m |

| AUA | £126.6bn (Sept) |

| Multi-home rate | ~40% |

| ISA allowance | £20,000 |

Preview the Actual Deliverable

Hargreaves Lansdown Porter's Five Forces Analysis

This preview shows the exact Hargreaves Lansdown Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the complete, professionally formatted document, ready for download and use the moment you buy. You’re looking at the actual file, available instantly upon payment. No mockups or samples—this is the deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hargreaves Lansdown faces moderate buyer power, intense industry rivalry, low supplier leverage, growing fintech substitute threats, and significant regulatory barriers; its scale and brand are key defenses but disruption risks persist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hargreaves Lansdown’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated fund and ETF providers

Hargreaves Lansdown relies on major asset managers for flagship funds and ETFs, giving big providers leverage over shelf placement and commercial terms, yet HL's distribution scale — c.1.6m clients and c.£114bn AUA in 2024 — tempers that power. Product substitution within fund and ETF categories limits any single provider's dominance. Co-marketing deals and prioritized platform lists act as negotiation levers for both HL and managers.

Market data and research vendors

Essential data feeds, ratings and research largely come from a small set of vendors (Bloomberg, Refinitiv, Morningstar), with Bloomberg terminals costing about $24,000/year (2024), raising switching costs for HL. Outages or price hikes can compress margins and affect service levels; vendor fee increases of even a few percent hit scale. HL mitigates via multi-sourcing and in-house analytics, but long-term contracts lock pricing while reducing flexibility.

Custody, clearing, and payments infrastructure

Settlement, custody and cash management rely on a small set of regulated counterparties and banks; in 2024 the top five UK banks held c.70% of domestic banking assets, reinforcing their systemic importance and bargaining leverage over service levels and fees. Regulatory constraints on custody switching and settlement finality limit HL’s agility, while scale-based pricing and partnerships across multiple custodians partially mitigate supplier power.

Cloud, cybersecurity, and core tech providers

Mission-critical hosting, security and platform tooling for HL depend on large providers (AWS 32%, Microsoft Azure 23%, Google Cloud 11% global market share in 2024), whose standardized pricing and vendor concentration increase dependency and resilience risk. HL can secure volume discounts but remains exposed to platform changes; building internal capabilities reduces lock-in over time.

- Vendor concentration: high (AWS/Azure/GCP ~66% combined)

- Dependency: resilience and change risk

- Levers: volume discounts

- Mitigation: internal platform investments

Regulators as quasi-suppliers

Regulators act as quasi-suppliers for Hargreaves Lansdown: FCA rule changes such as Consumer Duty (full implementation July 2024) and HMRC-set product limits (ISA allowance £20,000 for 2024/25) effectively supply permissions that reshape product design and revenue models; compliance increases operating costs and complexity, while proactive engagement can influence implementation timelines and regulatory detail.

- Consumer Duty: July 2024

- ISA limit: £20,000 (2024/25)

- Compliance raises OPEX and barrier-to-entry for challengers

Supplier power caps fees and shelf access; £114bn AUA

Hargreaves Lansdown faces concentrated supplier power from major asset managers despite its scale (c.1.6m clients, £114bn AUA in 2024), constraining fees and shelf placement. Critical data vendors (Bloomberg ~$24,000/yr) and dominant cloud providers (AWS 32%, Azure 23%, GCP 11% in 2024) raise switching costs. Banking/custody concentration (top5 UK banks ~70% assets) and regulatory suppliers (Consumer Duty Jul 2024; ISA £20,000 2024/25) further limit flexibility.

| Supplier | Key fact | 2024 metric |

|---|---|---|

| Clients/AUA | Scale | 1.6m / £114bn |

| Data vendor | Cost | Bloomberg ~$24,000/yr |

| Cloud | Market share | AWS32%/Azure23%/GCP11% |

| Banks | Concentration | Top5 ~70% |

| Regulation | Limits | Consumer Duty Jul 2024; ISA £20,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Hargreaves Lansdown highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus disruptive risks and strategic implications.

One-sheet Porter's Five Forces for Hargreaves Lansdown—instantly highlights strategic pressures with a clean radar chart and editable labels, so teams can adapt scenario tabs, copy straight into decks, and make faster decisions without complex tools.

Customers Bargaining Power

Price-sensitive retail investors

Price-sensitive retail investors actively compare platform fees (commonly in the 0.25–0.45% range), FX charges and fund ongoing charges, putting downward pressure on HL’s pricing. The rise of low-cost rivals and passive fund adoption increases sensitivity, forcing HL to justify higher fees via superior service, research tools and competitive cash rates. Transparent pricing and clear value communication are critical to retention.

Low switching frictions improving

ISA and SIPP transfers historically created inertia for Hargreaves Lansdown clients, but since 2024 digital processes and e-signatures have materially shortened move times; the ISA annual allowance for 2024/25 remains £20,000, keeping flows significant. Promotions and transfer-in incentives amplify buyer leverage, while FCA scrutiny of exit fees reduces lock-in. Faster transfers increase the need for continuous value delivery to retain assets.

Multi-homing across platforms

Many UK investors multi-home—about 40% in 2024—diluting platform exclusivity and enabling cherry-picking of the cheapest trades, funds or cash rates; Hargreaves Lansdown, with AUA around £126.6bn (Sept 2024), must compete product-by-product rather than by customer, making cross-selling and ecosystem stickiness key strategic priorities.

Demand for UX, tools, and service

Buyers now demand intuitive apps, real-time data and responsive support; Hargreaves Lansdown serves about 1.6m clients with c.£118bn AUA in 2024, so service lapses cause immediate churn risk and social media backlash. Superior research and guidance reduce pure price sensitivity, while continuous feature upgrades are treated as hygiene, not differentiator.

- UX: real-time pricing, portfolio sync

- Churn: rapid after poor support

- Value: research offsets price wars

- Product: continuous updates expected

Sophisticated segments negotiating value

Defend £126.6bn as ~40% retail multi-homing rises

Retail clients are highly price-sensitive, pressuring HL to defend fees with service and research; about 1.6m clients and AUA £126.6bn (Sept 2024) concentrate bargaining power in high-balance cohorts. Multi-homing (~40% in 2024) and faster digital ISA/SIPP transfers raise churn risk, making continuous product and UX upgrades essential.

| Metric | 2024 |

|---|---|

| Clients | 1.6m |

| AUA | £126.6bn (Sept) |

| Multi-home rate | ~40% |

| ISA allowance | £20,000 |

Preview the Actual Deliverable

Hargreaves Lansdown Porter's Five Forces Analysis

This preview shows the exact Hargreaves Lansdown Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the complete, professionally formatted document, ready for download and use the moment you buy. You’re looking at the actual file, available instantly upon payment. No mockups or samples—this is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hargreaves Lansdown faces moderate buyer power, intense industry rivalry, low supplier leverage, growing fintech substitute threats, and significant regulatory barriers; its scale and brand are key defenses but disruption risks persist. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hargreaves Lansdown’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated fund and ETF providers

Hargreaves Lansdown relies on major asset managers for flagship funds and ETFs, giving big providers leverage over shelf placement and commercial terms, yet HL's distribution scale — c.1.6m clients and c.£114bn AUA in 2024 — tempers that power. Product substitution within fund and ETF categories limits any single provider's dominance. Co-marketing deals and prioritized platform lists act as negotiation levers for both HL and managers.

Market data and research vendors

Essential data feeds, ratings and research largely come from a small set of vendors (Bloomberg, Refinitiv, Morningstar), with Bloomberg terminals costing about $24,000/year (2024), raising switching costs for HL. Outages or price hikes can compress margins and affect service levels; vendor fee increases of even a few percent hit scale. HL mitigates via multi-sourcing and in-house analytics, but long-term contracts lock pricing while reducing flexibility.

Custody, clearing, and payments infrastructure

Settlement, custody and cash management rely on a small set of regulated counterparties and banks; in 2024 the top five UK banks held c.70% of domestic banking assets, reinforcing their systemic importance and bargaining leverage over service levels and fees. Regulatory constraints on custody switching and settlement finality limit HL’s agility, while scale-based pricing and partnerships across multiple custodians partially mitigate supplier power.

Cloud, cybersecurity, and core tech providers

Mission-critical hosting, security and platform tooling for HL depend on large providers (AWS 32%, Microsoft Azure 23%, Google Cloud 11% global market share in 2024), whose standardized pricing and vendor concentration increase dependency and resilience risk. HL can secure volume discounts but remains exposed to platform changes; building internal capabilities reduces lock-in over time.

- Vendor concentration: high (AWS/Azure/GCP ~66% combined)

- Dependency: resilience and change risk

- Levers: volume discounts

- Mitigation: internal platform investments

Regulators as quasi-suppliers

Regulators act as quasi-suppliers for Hargreaves Lansdown: FCA rule changes such as Consumer Duty (full implementation July 2024) and HMRC-set product limits (ISA allowance £20,000 for 2024/25) effectively supply permissions that reshape product design and revenue models; compliance increases operating costs and complexity, while proactive engagement can influence implementation timelines and regulatory detail.

- Consumer Duty: July 2024

- ISA limit: £20,000 (2024/25)

- Compliance raises OPEX and barrier-to-entry for challengers

Supplier power caps fees and shelf access; £114bn AUA

Hargreaves Lansdown faces concentrated supplier power from major asset managers despite its scale (c.1.6m clients, £114bn AUA in 2024), constraining fees and shelf placement. Critical data vendors (Bloomberg ~$24,000/yr) and dominant cloud providers (AWS 32%, Azure 23%, GCP 11% in 2024) raise switching costs. Banking/custody concentration (top5 UK banks ~70% assets) and regulatory suppliers (Consumer Duty Jul 2024; ISA £20,000 2024/25) further limit flexibility.

| Supplier | Key fact | 2024 metric |

|---|---|---|

| Clients/AUA | Scale | 1.6m / £114bn |

| Data vendor | Cost | Bloomberg ~$24,000/yr |

| Cloud | Market share | AWS32%/Azure23%/GCP11% |

| Banks | Concentration | Top5 ~70% |

| Regulation | Limits | Consumer Duty Jul 2024; ISA £20,000 |

What is included in the product

Tailored Porter's Five Forces analysis for Hargreaves Lansdown highlighting competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, plus disruptive risks and strategic implications.

One-sheet Porter's Five Forces for Hargreaves Lansdown—instantly highlights strategic pressures with a clean radar chart and editable labels, so teams can adapt scenario tabs, copy straight into decks, and make faster decisions without complex tools.

Customers Bargaining Power

Price-sensitive retail investors

Price-sensitive retail investors actively compare platform fees (commonly in the 0.25–0.45% range), FX charges and fund ongoing charges, putting downward pressure on HL’s pricing. The rise of low-cost rivals and passive fund adoption increases sensitivity, forcing HL to justify higher fees via superior service, research tools and competitive cash rates. Transparent pricing and clear value communication are critical to retention.

Low switching frictions improving

ISA and SIPP transfers historically created inertia for Hargreaves Lansdown clients, but since 2024 digital processes and e-signatures have materially shortened move times; the ISA annual allowance for 2024/25 remains £20,000, keeping flows significant. Promotions and transfer-in incentives amplify buyer leverage, while FCA scrutiny of exit fees reduces lock-in. Faster transfers increase the need for continuous value delivery to retain assets.

Multi-homing across platforms

Many UK investors multi-home—about 40% in 2024—diluting platform exclusivity and enabling cherry-picking of the cheapest trades, funds or cash rates; Hargreaves Lansdown, with AUA around £126.6bn (Sept 2024), must compete product-by-product rather than by customer, making cross-selling and ecosystem stickiness key strategic priorities.

Demand for UX, tools, and service

Buyers now demand intuitive apps, real-time data and responsive support; Hargreaves Lansdown serves about 1.6m clients with c.£118bn AUA in 2024, so service lapses cause immediate churn risk and social media backlash. Superior research and guidance reduce pure price sensitivity, while continuous feature upgrades are treated as hygiene, not differentiator.

- UX: real-time pricing, portfolio sync

- Churn: rapid after poor support

- Value: research offsets price wars

- Product: continuous updates expected

Sophisticated segments negotiating value

Defend £126.6bn as ~40% retail multi-homing rises

Retail clients are highly price-sensitive, pressuring HL to defend fees with service and research; about 1.6m clients and AUA £126.6bn (Sept 2024) concentrate bargaining power in high-balance cohorts. Multi-homing (~40% in 2024) and faster digital ISA/SIPP transfers raise churn risk, making continuous product and UX upgrades essential.

| Metric | 2024 |

|---|---|

| Clients | 1.6m |

| AUA | £126.6bn (Sept) |

| Multi-home rate | ~40% |

| ISA allowance | £20,000 |

Preview the Actual Deliverable

Hargreaves Lansdown Porter's Five Forces Analysis

This preview shows the exact Hargreaves Lansdown Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. It is the complete, professionally formatted document, ready for download and use the moment you buy. You’re looking at the actual file, available instantly upon payment. No mockups or samples—this is the deliverable.