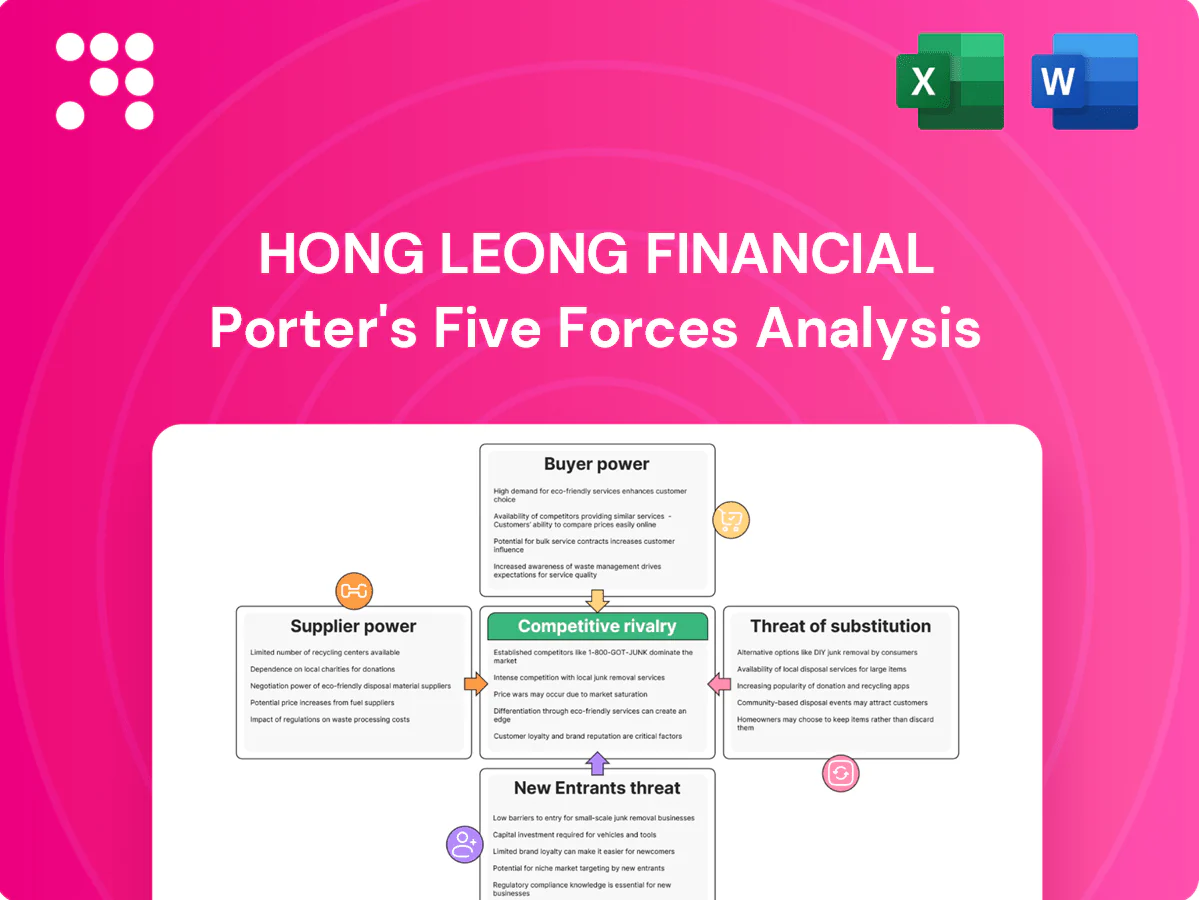

Hong Leong Financial Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Hong Leong Financial faces intense competitive rivalry, shifting buyer power, regulatory pressures, and rising fintech substitution that shape its margins and growth prospects. Our snapshot highlights key tensions across suppliers, entrants, and substitutes but omits granular metrics and scenarios. Want force-by-force ratings, visuals, and strategic implications? This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hong Leong Financial’s competitive dynamics in detail.

Suppliers Bargaining Power

Critical technology vendors

Core banking, cloud, cybersecurity and payment‑rail vendors are concentrated: the top three cloud providers held roughly two‑thirds of the market in 2024 and Visa/Mastercard process about 80% of card volumes, giving suppliers pricing leverage. High migration costs and lock‑in risk can erode margins and delay projects for a universal bank‑insurer like HLFG. Global cybersecurity spending topped USD 200B in 2024, reinforcing vendor bargaining power. Strong vendor management and multi‑vendor strategies are essential to mitigate exposure.

Regulators as quasi‑suppliers

Regulators and market operators supply licenses, liquidity frameworks and access to payment/settlement rails, with Basel III standards enforced in Malaysia including a 100% minimum LCR and a 2.5% capital conservation buffer as of 2024. Policy shifts on capital, liquidity and consumer protection can materially change Hong Leong Financials cost structure; compliance obligations raise input costs via higher capital and operational controls. Constructive regulatory engagement is essential for operational flexibility.

Funding providers and deposit mix

Depositors and wholesale markets set funding costs for Hong Leong Financial, with tightening cycles in 2022–24 driving rate competition and lifting liability costs, strengthening supplier power. HLFG's CASA sat around 39% in 2024, helping reduce reliance on pricier time deposits. A diversified mix of retail deposits, corporate term funding and wholesale lines has limited funding volatility and helped preserve NIM.

Talent and specialist skills

Quant, risk, tech and IB talent remain scarce and mobile, pushing up wages and contractor rates and raising hiring costs for Hong Leong Financial; digital transformation further amplifies demand for engineers and data scientists, increasing competition for scarce skills. Higher attrition can delay projects and raise execution risk, while strong employer branding and targeted upskilling reduce supplier dependence.

- Scarcity: mobile specialist talent

- Demand: engineers & data scientists

- Risk: attrition delays initiatives

- Mitigation: branding & upskilling

Data and market infrastructure

Reliance on credit bureaus like CTOS and Bank Negara Malaysia's CCRIS, market data vendors and Bursa clearinghouses creates measurable cost and access dependencies for Hong Leong Financial; restrictions or price increases can degrade underwriting accuracy and trading execution. Open data policies and regulators promoting data portability can rebalance supplier power but need upfront investment and governance. Building proprietary credit and transaction datasets strengthens pricing models and reduces third-party exposure.

- Dependence: CTOS, CCRIS, Bursa clearinghouses

- Risk: vendor price hikes or access limits impair underwriting/trading

- Policy: open data needs investment to shift power

- Mitigation: proprietary data assets improve bargaining position

Cloud top-3 ~66% & Visa/Mastercard ~80%: Cyber USD 200B, LCR 100%, CASA ~39%

Vendors concentrated: top‑3 cloud ~66% market share and Visa/Mastercard ~80% card volumes in 2024, giving pricing leverage and migration lock‑in. Cybersecurity spend ~USD 200B in 2024 and regulatory inputs (LCR 100%, capital conservation buffer 2.5%) raise supplier power. HLFG CASA ~39% in 2024 cushions funding but specialist talent scarcity increases costs.

| Metric | 2024 |

|---|---|

| Top‑3 cloud share | ~66% |

| Card volume (Visa/Mastercard) | ~80% |

| Cybersecurity spend | USD 200B |

| HLFG CASA | ~39% |

| LCR / Buffer | 100% / 2.5% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hong Leong Financial. Evaluates supplier and buyer power, substitutes, rivalry, and barriers to entry, highlighting disruptive threats and strategic levers to protect market share.

Clear, one-sheet Porter's Five Forces for Hong Leong Financial—instantly highlights competitive pressures and strategic risks to speed boardroom decisions; customize force levels, swap data labels, and visualize impacts with a ready-made spider chart for quick scenario comparison.

Customers Bargaining Power

Multi‑banking corporates

Large corporates and GLCs run competitive RFQs for loans, cash management and markets services, regularly pitting banks against each other and compressing margins and fees. Deep relationships and bespoke treasury or syndication solutions allow Hong Leong to defend yield through cross-sell and structural pricing. Ancillary wallet capture — trade finance, FX flow, and transaction banking — offsets headline rate pressure by locking in fee income and deposit balances.

Rate‑sensitive retail depositors

Rate‑sensitive retail depositors swiftly shift into higher‑yield term deposits and money market funds when rates rise, with Malaysian mobile banking adoption reaching about 85% in 2024, making comparisons and transfers friction‑light. Hong Leong offsets churn through bundled product discounts and ecosystem perks, and a strong CASA proposition (industry CASA ~30% in 2024) helps dampen immediate repricing pressure.

SMEs seeking credit and advisory

SMEs compare financing across banks, DFIs and fintechs, with surveys showing around 70% citing speed and collateral flexibility as decisive; fintech SME lending grew roughly 15% y/y in 2023, tightening bank pricing power. Cross‑sell of payments and insurance raises switching costs—30–40% of SMEs use bundled services—while digital onboarding (often <48 hours) weakens the leverage of price‑only shoppers.

Insurance customers and aggregators

Insurance customers and aggregators raise buyer leverage as 2024 saw bancassurance account for c.25% of Malaysian life gross written premiums and online aggregator referrals supplying roughly 15% of retail leads, increasing price transparency and switching. Persistency risk rises if Hong Leong Financial weakens pricing or service, while differentiated coverage and superior claims experience limit pure price competition. Data-driven underwriting enables segment pricing, reducing blanket discounting.

- Price transparency: aggregator referrals ~15% (2024)

- Bancassurance share: c.25% of life GWP (2024)

- Risk: higher persistency sensitivity

- Defense: product/claims differentiation and segment pricing

Affluent and mass affluent investors

Affluent and mass affluent clients negotiate fees across funds, brokerage and structured products (typical advisory ranges 0.5–1.5% AUM), and can reallocate assets rapidly to global platforms via international custodians. Demonstrable portfolio performance and high-quality advisory sustain fee floors, while open architecture and exclusive product access raise retention and wallet share.

- Fee pressure: 0.5–1.5% AUM

- Mobility: rapid global redeployment

- Value drivers: performance & advisory quality

- Retention: open architecture + exclusives

Customers squeeze margins; mobile banking ~85% and SMEs shift to fintech

Customers exert strong price pressure: corporates run RFQs compressing margins, retail mobile banking adoption ~85% (2024) enables rapid deposit switching despite Hong Leong CASA ~30% (2024), SMEs shift to fintech (SME fintech lending +15% y/y in 2023) while bancassurance c.25% of life GWP and aggregator referrals ~15% (2024) raise transparency; cross‑sell, product differentiation and segment pricing defend margins.

| Metric | Value |

|---|---|

| Mobile banking (2024) | ~85% |

| CASA (industry, 2024) | ~30% |

| Bancassurance (life GWP, 2024) | ~25% |

| Aggregator referrals (2024) | ~15% |

| SME fintech lending (2023) | +15% y/y |

| Advisory fees | 0.5–1.5% AUM |

Same Document Delivered

Hong Leong Financial Porter's Five Forces Analysis

This preview shows the exact Hong Leong Financial Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders and no mockups. The document displayed is the fully formatted, ready-to-use file, available for instant download upon payment. What you see here is precisely what you get.

A Must-Have Tool for Decision-Makers

Hong Leong Financial faces intense competitive rivalry, shifting buyer power, regulatory pressures, and rising fintech substitution that shape its margins and growth prospects. Our snapshot highlights key tensions across suppliers, entrants, and substitutes but omits granular metrics and scenarios. Want force-by-force ratings, visuals, and strategic implications? This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hong Leong Financial’s competitive dynamics in detail.

Suppliers Bargaining Power

Critical technology vendors

Core banking, cloud, cybersecurity and payment‑rail vendors are concentrated: the top three cloud providers held roughly two‑thirds of the market in 2024 and Visa/Mastercard process about 80% of card volumes, giving suppliers pricing leverage. High migration costs and lock‑in risk can erode margins and delay projects for a universal bank‑insurer like HLFG. Global cybersecurity spending topped USD 200B in 2024, reinforcing vendor bargaining power. Strong vendor management and multi‑vendor strategies are essential to mitigate exposure.

Regulators as quasi‑suppliers

Regulators and market operators supply licenses, liquidity frameworks and access to payment/settlement rails, with Basel III standards enforced in Malaysia including a 100% minimum LCR and a 2.5% capital conservation buffer as of 2024. Policy shifts on capital, liquidity and consumer protection can materially change Hong Leong Financials cost structure; compliance obligations raise input costs via higher capital and operational controls. Constructive regulatory engagement is essential for operational flexibility.

Funding providers and deposit mix

Depositors and wholesale markets set funding costs for Hong Leong Financial, with tightening cycles in 2022–24 driving rate competition and lifting liability costs, strengthening supplier power. HLFG's CASA sat around 39% in 2024, helping reduce reliance on pricier time deposits. A diversified mix of retail deposits, corporate term funding and wholesale lines has limited funding volatility and helped preserve NIM.

Talent and specialist skills

Quant, risk, tech and IB talent remain scarce and mobile, pushing up wages and contractor rates and raising hiring costs for Hong Leong Financial; digital transformation further amplifies demand for engineers and data scientists, increasing competition for scarce skills. Higher attrition can delay projects and raise execution risk, while strong employer branding and targeted upskilling reduce supplier dependence.

- Scarcity: mobile specialist talent

- Demand: engineers & data scientists

- Risk: attrition delays initiatives

- Mitigation: branding & upskilling

Data and market infrastructure

Reliance on credit bureaus like CTOS and Bank Negara Malaysia's CCRIS, market data vendors and Bursa clearinghouses creates measurable cost and access dependencies for Hong Leong Financial; restrictions or price increases can degrade underwriting accuracy and trading execution. Open data policies and regulators promoting data portability can rebalance supplier power but need upfront investment and governance. Building proprietary credit and transaction datasets strengthens pricing models and reduces third-party exposure.

- Dependence: CTOS, CCRIS, Bursa clearinghouses

- Risk: vendor price hikes or access limits impair underwriting/trading

- Policy: open data needs investment to shift power

- Mitigation: proprietary data assets improve bargaining position

Cloud top-3 ~66% & Visa/Mastercard ~80%: Cyber USD 200B, LCR 100%, CASA ~39%

Vendors concentrated: top‑3 cloud ~66% market share and Visa/Mastercard ~80% card volumes in 2024, giving pricing leverage and migration lock‑in. Cybersecurity spend ~USD 200B in 2024 and regulatory inputs (LCR 100%, capital conservation buffer 2.5%) raise supplier power. HLFG CASA ~39% in 2024 cushions funding but specialist talent scarcity increases costs.

| Metric | 2024 |

|---|---|

| Top‑3 cloud share | ~66% |

| Card volume (Visa/Mastercard) | ~80% |

| Cybersecurity spend | USD 200B |

| HLFG CASA | ~39% |

| LCR / Buffer | 100% / 2.5% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hong Leong Financial. Evaluates supplier and buyer power, substitutes, rivalry, and barriers to entry, highlighting disruptive threats and strategic levers to protect market share.

Clear, one-sheet Porter's Five Forces for Hong Leong Financial—instantly highlights competitive pressures and strategic risks to speed boardroom decisions; customize force levels, swap data labels, and visualize impacts with a ready-made spider chart for quick scenario comparison.

Customers Bargaining Power

Multi‑banking corporates

Large corporates and GLCs run competitive RFQs for loans, cash management and markets services, regularly pitting banks against each other and compressing margins and fees. Deep relationships and bespoke treasury or syndication solutions allow Hong Leong to defend yield through cross-sell and structural pricing. Ancillary wallet capture — trade finance, FX flow, and transaction banking — offsets headline rate pressure by locking in fee income and deposit balances.

Rate‑sensitive retail depositors

Rate‑sensitive retail depositors swiftly shift into higher‑yield term deposits and money market funds when rates rise, with Malaysian mobile banking adoption reaching about 85% in 2024, making comparisons and transfers friction‑light. Hong Leong offsets churn through bundled product discounts and ecosystem perks, and a strong CASA proposition (industry CASA ~30% in 2024) helps dampen immediate repricing pressure.

SMEs seeking credit and advisory

SMEs compare financing across banks, DFIs and fintechs, with surveys showing around 70% citing speed and collateral flexibility as decisive; fintech SME lending grew roughly 15% y/y in 2023, tightening bank pricing power. Cross‑sell of payments and insurance raises switching costs—30–40% of SMEs use bundled services—while digital onboarding (often <48 hours) weakens the leverage of price‑only shoppers.

Insurance customers and aggregators

Insurance customers and aggregators raise buyer leverage as 2024 saw bancassurance account for c.25% of Malaysian life gross written premiums and online aggregator referrals supplying roughly 15% of retail leads, increasing price transparency and switching. Persistency risk rises if Hong Leong Financial weakens pricing or service, while differentiated coverage and superior claims experience limit pure price competition. Data-driven underwriting enables segment pricing, reducing blanket discounting.

- Price transparency: aggregator referrals ~15% (2024)

- Bancassurance share: c.25% of life GWP (2024)

- Risk: higher persistency sensitivity

- Defense: product/claims differentiation and segment pricing

Affluent and mass affluent investors

Affluent and mass affluent clients negotiate fees across funds, brokerage and structured products (typical advisory ranges 0.5–1.5% AUM), and can reallocate assets rapidly to global platforms via international custodians. Demonstrable portfolio performance and high-quality advisory sustain fee floors, while open architecture and exclusive product access raise retention and wallet share.

- Fee pressure: 0.5–1.5% AUM

- Mobility: rapid global redeployment

- Value drivers: performance & advisory quality

- Retention: open architecture + exclusives

Customers squeeze margins; mobile banking ~85% and SMEs shift to fintech

Customers exert strong price pressure: corporates run RFQs compressing margins, retail mobile banking adoption ~85% (2024) enables rapid deposit switching despite Hong Leong CASA ~30% (2024), SMEs shift to fintech (SME fintech lending +15% y/y in 2023) while bancassurance c.25% of life GWP and aggregator referrals ~15% (2024) raise transparency; cross‑sell, product differentiation and segment pricing defend margins.

| Metric | Value |

|---|---|

| Mobile banking (2024) | ~85% |

| CASA (industry, 2024) | ~30% |

| Bancassurance (life GWP, 2024) | ~25% |

| Aggregator referrals (2024) | ~15% |

| SME fintech lending (2023) | +15% y/y |

| Advisory fees | 0.5–1.5% AUM |

Same Document Delivered

Hong Leong Financial Porter's Five Forces Analysis

This preview shows the exact Hong Leong Financial Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders and no mockups. The document displayed is the fully formatted, ready-to-use file, available for instant download upon payment. What you see here is precisely what you get.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Hong Leong Financial faces intense competitive rivalry, shifting buyer power, regulatory pressures, and rising fintech substitution that shape its margins and growth prospects. Our snapshot highlights key tensions across suppliers, entrants, and substitutes but omits granular metrics and scenarios. Want force-by-force ratings, visuals, and strategic implications? This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hong Leong Financial’s competitive dynamics in detail.

Suppliers Bargaining Power

Critical technology vendors

Core banking, cloud, cybersecurity and payment‑rail vendors are concentrated: the top three cloud providers held roughly two‑thirds of the market in 2024 and Visa/Mastercard process about 80% of card volumes, giving suppliers pricing leverage. High migration costs and lock‑in risk can erode margins and delay projects for a universal bank‑insurer like HLFG. Global cybersecurity spending topped USD 200B in 2024, reinforcing vendor bargaining power. Strong vendor management and multi‑vendor strategies are essential to mitigate exposure.

Regulators as quasi‑suppliers

Regulators and market operators supply licenses, liquidity frameworks and access to payment/settlement rails, with Basel III standards enforced in Malaysia including a 100% minimum LCR and a 2.5% capital conservation buffer as of 2024. Policy shifts on capital, liquidity and consumer protection can materially change Hong Leong Financials cost structure; compliance obligations raise input costs via higher capital and operational controls. Constructive regulatory engagement is essential for operational flexibility.

Funding providers and deposit mix

Depositors and wholesale markets set funding costs for Hong Leong Financial, with tightening cycles in 2022–24 driving rate competition and lifting liability costs, strengthening supplier power. HLFG's CASA sat around 39% in 2024, helping reduce reliance on pricier time deposits. A diversified mix of retail deposits, corporate term funding and wholesale lines has limited funding volatility and helped preserve NIM.

Talent and specialist skills

Quant, risk, tech and IB talent remain scarce and mobile, pushing up wages and contractor rates and raising hiring costs for Hong Leong Financial; digital transformation further amplifies demand for engineers and data scientists, increasing competition for scarce skills. Higher attrition can delay projects and raise execution risk, while strong employer branding and targeted upskilling reduce supplier dependence.

- Scarcity: mobile specialist talent

- Demand: engineers & data scientists

- Risk: attrition delays initiatives

- Mitigation: branding & upskilling

Data and market infrastructure

Reliance on credit bureaus like CTOS and Bank Negara Malaysia's CCRIS, market data vendors and Bursa clearinghouses creates measurable cost and access dependencies for Hong Leong Financial; restrictions or price increases can degrade underwriting accuracy and trading execution. Open data policies and regulators promoting data portability can rebalance supplier power but need upfront investment and governance. Building proprietary credit and transaction datasets strengthens pricing models and reduces third-party exposure.

- Dependence: CTOS, CCRIS, Bursa clearinghouses

- Risk: vendor price hikes or access limits impair underwriting/trading

- Policy: open data needs investment to shift power

- Mitigation: proprietary data assets improve bargaining position

Cloud top-3 ~66% & Visa/Mastercard ~80%: Cyber USD 200B, LCR 100%, CASA ~39%

Vendors concentrated: top‑3 cloud ~66% market share and Visa/Mastercard ~80% card volumes in 2024, giving pricing leverage and migration lock‑in. Cybersecurity spend ~USD 200B in 2024 and regulatory inputs (LCR 100%, capital conservation buffer 2.5%) raise supplier power. HLFG CASA ~39% in 2024 cushions funding but specialist talent scarcity increases costs.

| Metric | 2024 |

|---|---|

| Top‑3 cloud share | ~66% |

| Card volume (Visa/Mastercard) | ~80% |

| Cybersecurity spend | USD 200B |

| HLFG CASA | ~39% |

| LCR / Buffer | 100% / 2.5% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hong Leong Financial. Evaluates supplier and buyer power, substitutes, rivalry, and barriers to entry, highlighting disruptive threats and strategic levers to protect market share.

Clear, one-sheet Porter's Five Forces for Hong Leong Financial—instantly highlights competitive pressures and strategic risks to speed boardroom decisions; customize force levels, swap data labels, and visualize impacts with a ready-made spider chart for quick scenario comparison.

Customers Bargaining Power

Multi‑banking corporates

Large corporates and GLCs run competitive RFQs for loans, cash management and markets services, regularly pitting banks against each other and compressing margins and fees. Deep relationships and bespoke treasury or syndication solutions allow Hong Leong to defend yield through cross-sell and structural pricing. Ancillary wallet capture — trade finance, FX flow, and transaction banking — offsets headline rate pressure by locking in fee income and deposit balances.

Rate‑sensitive retail depositors

Rate‑sensitive retail depositors swiftly shift into higher‑yield term deposits and money market funds when rates rise, with Malaysian mobile banking adoption reaching about 85% in 2024, making comparisons and transfers friction‑light. Hong Leong offsets churn through bundled product discounts and ecosystem perks, and a strong CASA proposition (industry CASA ~30% in 2024) helps dampen immediate repricing pressure.

SMEs seeking credit and advisory

SMEs compare financing across banks, DFIs and fintechs, with surveys showing around 70% citing speed and collateral flexibility as decisive; fintech SME lending grew roughly 15% y/y in 2023, tightening bank pricing power. Cross‑sell of payments and insurance raises switching costs—30–40% of SMEs use bundled services—while digital onboarding (often <48 hours) weakens the leverage of price‑only shoppers.

Insurance customers and aggregators

Insurance customers and aggregators raise buyer leverage as 2024 saw bancassurance account for c.25% of Malaysian life gross written premiums and online aggregator referrals supplying roughly 15% of retail leads, increasing price transparency and switching. Persistency risk rises if Hong Leong Financial weakens pricing or service, while differentiated coverage and superior claims experience limit pure price competition. Data-driven underwriting enables segment pricing, reducing blanket discounting.

- Price transparency: aggregator referrals ~15% (2024)

- Bancassurance share: c.25% of life GWP (2024)

- Risk: higher persistency sensitivity

- Defense: product/claims differentiation and segment pricing

Affluent and mass affluent investors

Affluent and mass affluent clients negotiate fees across funds, brokerage and structured products (typical advisory ranges 0.5–1.5% AUM), and can reallocate assets rapidly to global platforms via international custodians. Demonstrable portfolio performance and high-quality advisory sustain fee floors, while open architecture and exclusive product access raise retention and wallet share.

- Fee pressure: 0.5–1.5% AUM

- Mobility: rapid global redeployment

- Value drivers: performance & advisory quality

- Retention: open architecture + exclusives

Customers squeeze margins; mobile banking ~85% and SMEs shift to fintech

Customers exert strong price pressure: corporates run RFQs compressing margins, retail mobile banking adoption ~85% (2024) enables rapid deposit switching despite Hong Leong CASA ~30% (2024), SMEs shift to fintech (SME fintech lending +15% y/y in 2023) while bancassurance c.25% of life GWP and aggregator referrals ~15% (2024) raise transparency; cross‑sell, product differentiation and segment pricing defend margins.

| Metric | Value |

|---|---|

| Mobile banking (2024) | ~85% |

| CASA (industry, 2024) | ~30% |

| Bancassurance (life GWP, 2024) | ~25% |

| Aggregator referrals (2024) | ~15% |

| SME fintech lending (2023) | +15% y/y |

| Advisory fees | 0.5–1.5% AUM |

Same Document Delivered

Hong Leong Financial Porter's Five Forces Analysis

This preview shows the exact Hong Leong Financial Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders and no mockups. The document displayed is the fully formatted, ready-to-use file, available for instant download upon payment. What you see here is precisely what you get.