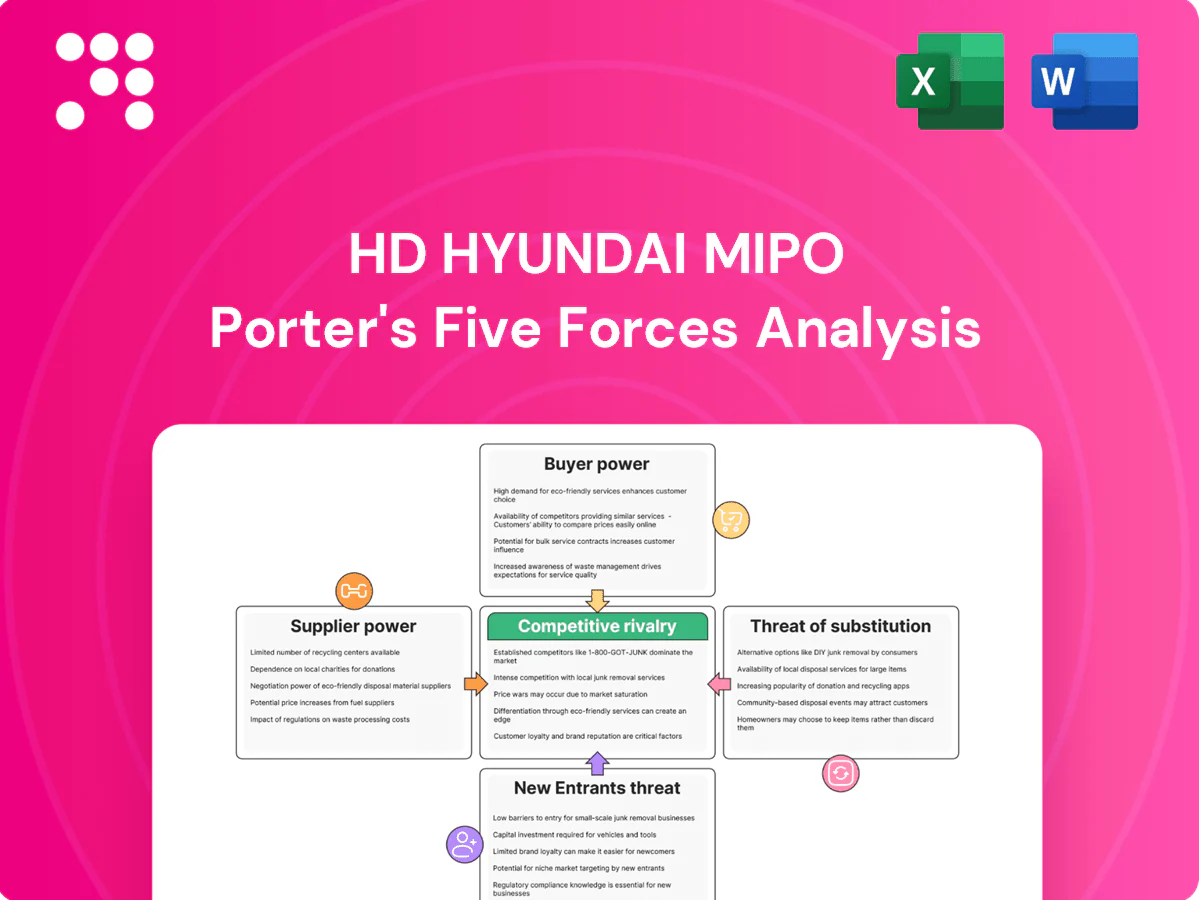

Hd Hyundai Mipo Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Hd Hyundai Mipo faces intense competitive pressures from global shipbuilders, shifting supplier leverage for steel and components, moderate buyer power with large naval and commercial clients, and steady threat from technological substitutes and consolidated rivals; strategic positioning and cost discipline are key. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical components

Marine engines, propulsion and advanced electronics for HD Hyundai Mipo come from a concentrated set of global suppliers—notably MAN Energy Solutions, W?rtsil? and Mitsubishi Heavy Industries—whose 2024 supply dominance and licensing of dual‑fuel tech restrict sourcing flexibility. This concentration gives suppliers pricing power and control over delivery schedules, amplifying schedule-driven margin risk. Any vendor delay materially raises project risk and potential penalty exposures.

Volatile steel inputs

Steel plate is a major cost driver for HD Hyundai Mipo and global hot-rolled coil averaged roughly $600/tonne in 2024, with spot swings near ±20% year-on-year that transmit to plate markets. Multiple mills exist, but required grades and just-in-time delivery narrow practical suppliers. Price volatility squeezes margins on fixed-price contracts, and while hedging and multi-year frame agreements reduce volatility, they do not eliminate exposure.

Certification-driven switching costs

Components must meet classification society rules and yard standards, so vendor qualification is lengthy and costly—typically 6–12 months with certification/testing costs often $50k–$500k. Switching mid-project risks 6–9 month re-approval delays and penalties ranging from $100k–$2M, effectively locking suppliers for program durations and boosting supplier bargaining power at critical milestones.

Green tech dependencies

- High supplier leverage

- Limited proven systems

- Premiums for verified performance

- Integration raises dependence

Long-term agreements and consortia

Yards secure long-term contracts and module bundling to capture volume discounts (often up to 8%) and delivery priority, while joint supplier planning improves design-for-manufacture and lowers rework rates, strengthening negotiating leverage for HD Hyundai Mipo.

These practices temper supplier power but expose yards to renegotiation risk when input markets tighten, as seen in 2024 commodity-driven cost pressures across shipbuilding supply chains.

High supplier power; $600/tonne HRC, ±20% swings; 6–12m qualification locks suppliers

Supplier power is high: key engine suppliers (MAN, W?rtsil?, MHI) and decarbonization vendors limit sourcing and command premiums; 2024 hot-rolled coil averaged ~$600/tonne with ±20% swings. Qualification takes 6–12 months and costs $50k–$500k, locking suppliers mid-program. Long-term contracts and module bundling cut costs (discounts up to 8%) but renegotiation risk rose in 2024.

| Metric | 2024 |

|---|---|

| HRC price | $600/tonne |

| Price volatility | ±20% |

| Qualification | 6–12 months; $50k–$500k |

| Volume discount | Up to 8% |

What is included in the product

Tailored Porter's Five Forces analysis for Hd Hyundai Mipo identifying competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect market share and profitability.

Tailored Porter's Five Forces for HD Hyundai Mipo—a clear one-sheet summary for quick strategic decisions, with editable pressure levels and an instant radar chart for scenario planning, ready to drop into decks or boardroom slides.

Customers Bargaining Power

Large, professional buyers

Shipowners, lessors and liners commonly buy in batches and use competitive tenders, leveraging fleet-scale and market intelligence to push prices down. Large carriers now control roughly 80% of global container capacity (Alphaliner, 2024), boosting their bargaining leverage. They insist on customization and firm performance guarantees, concentrating negotiating power on a few key orders that shape yard utilization and margins.

Cyclical demand swings

Shipping cycles and freight rates dictate order timing, giving buyers strong leverage in downturns as yards cut price and extend terms to fill slots; the Baltic Dry Index remained well below its 2021 peak throughout 2024, underscoring softer demand. When demand is weak yards routinely concede on price and delivery; in booms leverage returns to yards. Mipo’s mid-sized niche smooths order volatility but does not eliminate industry cyclicality.

Specification and ESG leverage

Buyers now dictate fuel choices, emissions targets and digital features, forcing yards to meet IMO goals—IMO’s Initial Strategy seeks at least 50% GHG reduction by 2050 and ~40% carbon-intensity cut by 2030—while compliance and customer ESG demands squeeze pricing and force risk-sharing. Owners push future-fuel readiness but rarely pay full premiums, shifting technical and warranty risk onto the yard.

Delivery slots and financing terms

Buyers extract delivery priority, staged payment milestones and refund guarantees, using bankable refund guarantees (RGs) as a key differentiator when contracting with HD Hyundai Mipo; schedule certainty is often priced aggressively and slippage penalties further strengthen buyer leverage.

- Delivery priority negotiation

- Bankable RGs as differentiator

- Aggressive pricing for schedule certainty

- Slippage penalties increase buyer leverage

Aftermarket and warranty expectations

Owners demand strong lifecycle support, spares, and 12–24 month performance warranties; warranty scope and liquidated damages (commonly 0.5–1% per week, up to ~5% of contract value) are major negotiation levers. Building robust service networks can win orders but often raises bid exposure by roughly 2–5% of contract value, increasing buyer leverage at contract close.

- Warranty period: 12–24 months

- Liquidated damages: 0.5–1%/week, cap ~5%

- Service-network cost exposure: ~2–5% of contract

Large carriers (~80% capacity) use tender leverage, shifting pricing and warranty risk to yards

Buyers—large carriers controlling ~80% of container capacity (Alphaliner, 2024)—use bulk tenders and schedule leverage to press prices and terms.

Market cycles (BDI remained well below its 2021 peak through 2024) shift leverage to buyers in downturns; Mipo’s mid-size niche moderates but does not eliminate volatility.

Buyers force emissions/digital specs, bankable RGs, 12–24m warranties and slippage penalties (LDs 0.5–1%/week, cap ~5%), shifting technical and warranty risk onto yards.

| Metric | Value | Source |

|---|---|---|

| Carrier share | ~80% | Alphaliner 2024 |

| BDI 2024 vs 2021 | Well below 2021 peak | Market data 2024 |

| Warranty | 12–24 months | Industry norms |

| Liquidated damages | 0.5–1%/week, cap ~5% | Contract practice |

| Service-network cost | ~2–5% contract value | Industry estimates |

Preview Before You Purchase

Hd Hyundai Mipo Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for HD Hyundai Mipo you’ll receive—no mockups or placeholders. The document shown is the final, professionally formatted file and will be available for immediate download upon purchase. It contains a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. Use it instantly for strategy, valuation, or reporting needs.

A Must-Have Tool for Decision-Makers

Hd Hyundai Mipo faces intense competitive pressures from global shipbuilders, shifting supplier leverage for steel and components, moderate buyer power with large naval and commercial clients, and steady threat from technological substitutes and consolidated rivals; strategic positioning and cost discipline are key. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical components

Marine engines, propulsion and advanced electronics for HD Hyundai Mipo come from a concentrated set of global suppliers—notably MAN Energy Solutions, W?rtsil? and Mitsubishi Heavy Industries—whose 2024 supply dominance and licensing of dual‑fuel tech restrict sourcing flexibility. This concentration gives suppliers pricing power and control over delivery schedules, amplifying schedule-driven margin risk. Any vendor delay materially raises project risk and potential penalty exposures.

Volatile steel inputs

Steel plate is a major cost driver for HD Hyundai Mipo and global hot-rolled coil averaged roughly $600/tonne in 2024, with spot swings near ±20% year-on-year that transmit to plate markets. Multiple mills exist, but required grades and just-in-time delivery narrow practical suppliers. Price volatility squeezes margins on fixed-price contracts, and while hedging and multi-year frame agreements reduce volatility, they do not eliminate exposure.

Certification-driven switching costs

Components must meet classification society rules and yard standards, so vendor qualification is lengthy and costly—typically 6–12 months with certification/testing costs often $50k–$500k. Switching mid-project risks 6–9 month re-approval delays and penalties ranging from $100k–$2M, effectively locking suppliers for program durations and boosting supplier bargaining power at critical milestones.

Green tech dependencies

- High supplier leverage

- Limited proven systems

- Premiums for verified performance

- Integration raises dependence

Long-term agreements and consortia

Yards secure long-term contracts and module bundling to capture volume discounts (often up to 8%) and delivery priority, while joint supplier planning improves design-for-manufacture and lowers rework rates, strengthening negotiating leverage for HD Hyundai Mipo.

These practices temper supplier power but expose yards to renegotiation risk when input markets tighten, as seen in 2024 commodity-driven cost pressures across shipbuilding supply chains.

High supplier power; $600/tonne HRC, ±20% swings; 6–12m qualification locks suppliers

Supplier power is high: key engine suppliers (MAN, W?rtsil?, MHI) and decarbonization vendors limit sourcing and command premiums; 2024 hot-rolled coil averaged ~$600/tonne with ±20% swings. Qualification takes 6–12 months and costs $50k–$500k, locking suppliers mid-program. Long-term contracts and module bundling cut costs (discounts up to 8%) but renegotiation risk rose in 2024.

| Metric | 2024 |

|---|---|

| HRC price | $600/tonne |

| Price volatility | ±20% |

| Qualification | 6–12 months; $50k–$500k |

| Volume discount | Up to 8% |

What is included in the product

Tailored Porter's Five Forces analysis for Hd Hyundai Mipo identifying competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect market share and profitability.

Tailored Porter's Five Forces for HD Hyundai Mipo—a clear one-sheet summary for quick strategic decisions, with editable pressure levels and an instant radar chart for scenario planning, ready to drop into decks or boardroom slides.

Customers Bargaining Power

Large, professional buyers

Shipowners, lessors and liners commonly buy in batches and use competitive tenders, leveraging fleet-scale and market intelligence to push prices down. Large carriers now control roughly 80% of global container capacity (Alphaliner, 2024), boosting their bargaining leverage. They insist on customization and firm performance guarantees, concentrating negotiating power on a few key orders that shape yard utilization and margins.

Cyclical demand swings

Shipping cycles and freight rates dictate order timing, giving buyers strong leverage in downturns as yards cut price and extend terms to fill slots; the Baltic Dry Index remained well below its 2021 peak throughout 2024, underscoring softer demand. When demand is weak yards routinely concede on price and delivery; in booms leverage returns to yards. Mipo’s mid-sized niche smooths order volatility but does not eliminate industry cyclicality.

Specification and ESG leverage

Buyers now dictate fuel choices, emissions targets and digital features, forcing yards to meet IMO goals—IMO’s Initial Strategy seeks at least 50% GHG reduction by 2050 and ~40% carbon-intensity cut by 2030—while compliance and customer ESG demands squeeze pricing and force risk-sharing. Owners push future-fuel readiness but rarely pay full premiums, shifting technical and warranty risk onto the yard.

Delivery slots and financing terms

Buyers extract delivery priority, staged payment milestones and refund guarantees, using bankable refund guarantees (RGs) as a key differentiator when contracting with HD Hyundai Mipo; schedule certainty is often priced aggressively and slippage penalties further strengthen buyer leverage.

- Delivery priority negotiation

- Bankable RGs as differentiator

- Aggressive pricing for schedule certainty

- Slippage penalties increase buyer leverage

Aftermarket and warranty expectations

Owners demand strong lifecycle support, spares, and 12–24 month performance warranties; warranty scope and liquidated damages (commonly 0.5–1% per week, up to ~5% of contract value) are major negotiation levers. Building robust service networks can win orders but often raises bid exposure by roughly 2–5% of contract value, increasing buyer leverage at contract close.

- Warranty period: 12–24 months

- Liquidated damages: 0.5–1%/week, cap ~5%

- Service-network cost exposure: ~2–5% of contract

Large carriers (~80% capacity) use tender leverage, shifting pricing and warranty risk to yards

Buyers—large carriers controlling ~80% of container capacity (Alphaliner, 2024)—use bulk tenders and schedule leverage to press prices and terms.

Market cycles (BDI remained well below its 2021 peak through 2024) shift leverage to buyers in downturns; Mipo’s mid-size niche moderates but does not eliminate volatility.

Buyers force emissions/digital specs, bankable RGs, 12–24m warranties and slippage penalties (LDs 0.5–1%/week, cap ~5%), shifting technical and warranty risk onto yards.

| Metric | Value | Source |

|---|---|---|

| Carrier share | ~80% | Alphaliner 2024 |

| BDI 2024 vs 2021 | Well below 2021 peak | Market data 2024 |

| Warranty | 12–24 months | Industry norms |

| Liquidated damages | 0.5–1%/week, cap ~5% | Contract practice |

| Service-network cost | ~2–5% contract value | Industry estimates |

Preview Before You Purchase

Hd Hyundai Mipo Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for HD Hyundai Mipo you’ll receive—no mockups or placeholders. The document shown is the final, professionally formatted file and will be available for immediate download upon purchase. It contains a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. Use it instantly for strategy, valuation, or reporting needs.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Hd Hyundai Mipo faces intense competitive pressures from global shipbuilders, shifting supplier leverage for steel and components, moderate buyer power with large naval and commercial clients, and steady threat from technological substitutes and consolidated rivals; strategic positioning and cost discipline are key. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical components

Marine engines, propulsion and advanced electronics for HD Hyundai Mipo come from a concentrated set of global suppliers—notably MAN Energy Solutions, W?rtsil? and Mitsubishi Heavy Industries—whose 2024 supply dominance and licensing of dual‑fuel tech restrict sourcing flexibility. This concentration gives suppliers pricing power and control over delivery schedules, amplifying schedule-driven margin risk. Any vendor delay materially raises project risk and potential penalty exposures.

Volatile steel inputs

Steel plate is a major cost driver for HD Hyundai Mipo and global hot-rolled coil averaged roughly $600/tonne in 2024, with spot swings near ±20% year-on-year that transmit to plate markets. Multiple mills exist, but required grades and just-in-time delivery narrow practical suppliers. Price volatility squeezes margins on fixed-price contracts, and while hedging and multi-year frame agreements reduce volatility, they do not eliminate exposure.

Certification-driven switching costs

Components must meet classification society rules and yard standards, so vendor qualification is lengthy and costly—typically 6–12 months with certification/testing costs often $50k–$500k. Switching mid-project risks 6–9 month re-approval delays and penalties ranging from $100k–$2M, effectively locking suppliers for program durations and boosting supplier bargaining power at critical milestones.

Green tech dependencies

- High supplier leverage

- Limited proven systems

- Premiums for verified performance

- Integration raises dependence

Long-term agreements and consortia

Yards secure long-term contracts and module bundling to capture volume discounts (often up to 8%) and delivery priority, while joint supplier planning improves design-for-manufacture and lowers rework rates, strengthening negotiating leverage for HD Hyundai Mipo.

These practices temper supplier power but expose yards to renegotiation risk when input markets tighten, as seen in 2024 commodity-driven cost pressures across shipbuilding supply chains.

High supplier power; $600/tonne HRC, ±20% swings; 6–12m qualification locks suppliers

Supplier power is high: key engine suppliers (MAN, W?rtsil?, MHI) and decarbonization vendors limit sourcing and command premiums; 2024 hot-rolled coil averaged ~$600/tonne with ±20% swings. Qualification takes 6–12 months and costs $50k–$500k, locking suppliers mid-program. Long-term contracts and module bundling cut costs (discounts up to 8%) but renegotiation risk rose in 2024.

| Metric | 2024 |

|---|---|

| HRC price | $600/tonne |

| Price volatility | ±20% |

| Qualification | 6–12 months; $50k–$500k |

| Volume discount | Up to 8% |

What is included in the product

Tailored Porter's Five Forces analysis for Hd Hyundai Mipo identifying competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and strategic levers to protect market share and profitability.

Tailored Porter's Five Forces for HD Hyundai Mipo—a clear one-sheet summary for quick strategic decisions, with editable pressure levels and an instant radar chart for scenario planning, ready to drop into decks or boardroom slides.

Customers Bargaining Power

Large, professional buyers

Shipowners, lessors and liners commonly buy in batches and use competitive tenders, leveraging fleet-scale and market intelligence to push prices down. Large carriers now control roughly 80% of global container capacity (Alphaliner, 2024), boosting their bargaining leverage. They insist on customization and firm performance guarantees, concentrating negotiating power on a few key orders that shape yard utilization and margins.

Cyclical demand swings

Shipping cycles and freight rates dictate order timing, giving buyers strong leverage in downturns as yards cut price and extend terms to fill slots; the Baltic Dry Index remained well below its 2021 peak throughout 2024, underscoring softer demand. When demand is weak yards routinely concede on price and delivery; in booms leverage returns to yards. Mipo’s mid-sized niche smooths order volatility but does not eliminate industry cyclicality.

Specification and ESG leverage

Buyers now dictate fuel choices, emissions targets and digital features, forcing yards to meet IMO goals—IMO’s Initial Strategy seeks at least 50% GHG reduction by 2050 and ~40% carbon-intensity cut by 2030—while compliance and customer ESG demands squeeze pricing and force risk-sharing. Owners push future-fuel readiness but rarely pay full premiums, shifting technical and warranty risk onto the yard.

Delivery slots and financing terms

Buyers extract delivery priority, staged payment milestones and refund guarantees, using bankable refund guarantees (RGs) as a key differentiator when contracting with HD Hyundai Mipo; schedule certainty is often priced aggressively and slippage penalties further strengthen buyer leverage.

- Delivery priority negotiation

- Bankable RGs as differentiator

- Aggressive pricing for schedule certainty

- Slippage penalties increase buyer leverage

Aftermarket and warranty expectations

Owners demand strong lifecycle support, spares, and 12–24 month performance warranties; warranty scope and liquidated damages (commonly 0.5–1% per week, up to ~5% of contract value) are major negotiation levers. Building robust service networks can win orders but often raises bid exposure by roughly 2–5% of contract value, increasing buyer leverage at contract close.

- Warranty period: 12–24 months

- Liquidated damages: 0.5–1%/week, cap ~5%

- Service-network cost exposure: ~2–5% of contract

Large carriers (~80% capacity) use tender leverage, shifting pricing and warranty risk to yards

Buyers—large carriers controlling ~80% of container capacity (Alphaliner, 2024)—use bulk tenders and schedule leverage to press prices and terms.

Market cycles (BDI remained well below its 2021 peak through 2024) shift leverage to buyers in downturns; Mipo’s mid-size niche moderates but does not eliminate volatility.

Buyers force emissions/digital specs, bankable RGs, 12–24m warranties and slippage penalties (LDs 0.5–1%/week, cap ~5%), shifting technical and warranty risk onto yards.

| Metric | Value | Source |

|---|---|---|

| Carrier share | ~80% | Alphaliner 2024 |

| BDI 2024 vs 2021 | Well below 2021 peak | Market data 2024 |

| Warranty | 12–24 months | Industry norms |

| Liquidated damages | 0.5–1%/week, cap ~5% | Contract practice |

| Service-network cost | ~2–5% contract value | Industry estimates |

Preview Before You Purchase

Hd Hyundai Mipo Porter's Five Forces Analysis

This preview is the exact Porter’s Five Forces analysis for HD Hyundai Mipo you’ll receive—no mockups or placeholders. The document shown is the final, professionally formatted file and will be available for immediate download upon purchase. It contains a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. Use it instantly for strategy, valuation, or reporting needs.