Dr. Sulaiman Al-Habib Medical Services Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

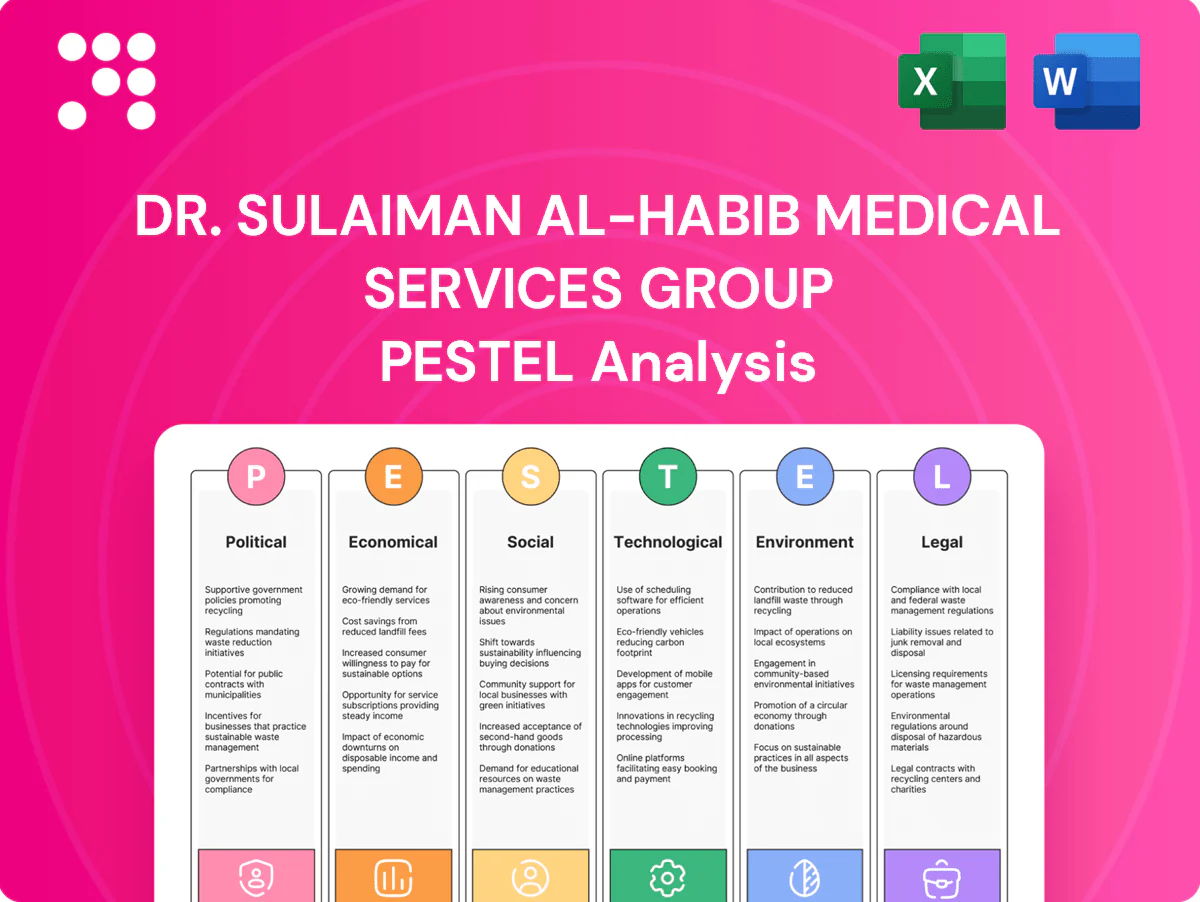

Unlock strategic clarity with our PESTLE analysis of Dr. Sulaiman Al-Habib Medical Services Group—three-plus pages of actionable insight into political, economic, social, technological, legal and environmental forces shaping growth. Ideal for investors and strategists, it highlights risks and opportunities you can act on today. Purchase the full report for the complete, editable analysis and immediate download.

Political factors

Vision 2030 healthcare reforms

Vision 2030 prioritizes healthcare quality, access and private-sector participation, aligning with the national target to raise private-sector contribution to 65% of GDP. This drives PPPs, capacity expansion and clinical specialization that match Dr. Sulaiman Al-Habib Group's growth model. Policy continuity can unlock financing and land access, while shifts in priorities or execution pace could delay project pipelines.

Government healthcare spending

High public health budgets—Saudi public health spending was about 3.6% of GDP per WHO (latest comparable data)—underpin demand and reimbursement stability for Dr. Sulaiman Al‑Habib Medical Services Group.

Centralized procurement reforms and payer programs, including national procurement consolidation, can compress pricing and shift the hospital service mix toward cost‑effective care.

Incentives to expand into underserved regions align with Vision 2030 goals to boost private sector participation in healthcare.

However, budget reprioritization during fiscal tightening could slow expansion and cap revenue growth.

Regulatory centralization and oversight

Stronger centralized authorities like the Saudi MOH streamline standards and accreditation, raising compliance costs but favoring scale players that can absorb them; predictable oversight reduces operational risk and supports expansion planning, while regulatory delays—commonly in licensing and commissioning—can slow new facility openings by months, impacting capex deployment and time-to-revenue.

Regional geopolitical stability

Regional geopolitical stability in the GCC underpins patient flows, staffing and supply chains across a population of about 57 million (UN 2024); tensions risk disrupting cross-border expansion and medical tourism plans, while currency and trade frictions can increase imported equipment costs, making business continuity planning critical for Dr. Sulaiman Al-Habib Medical Services Group.

- Patient flows: GCC ~57M (UN 2024)

- Staffing: reliance on expatriates — vulnerability to border tensions

- Costs: trade/friction raise equipment import prices

- Action: prioritize business continuity planning

Localization and workforce nationalization

- Saudization/Nitaqat compliance

- Need for expatriate specialists vs national hires

- Incentives: training subsidies, localization rewards

- Cost pressure from tight labor markets

Vision 2030 boosts private healthcare to 65% of GDP

Vision 2030 drives private-sector healthcare growth aiming to raise private contribution to 65% of GDP, supporting PPPs and expansion. Saudi population ~35.1M (World Bank 2024) and GCC ~57M (UN 2024) underpin patient pools; public health spending ~3.6% of GDP (WHO). Centralized procurement and Saudization raise compliance and labor costs, while geopolitical risks can affect supply chains and medical tourism.

| Indicator | Value |

|---|---|

| Private-sector GDP target | 65% |

| Saudi population (2024) | 35.1M |

| GCC population (2024) | 57M |

| Public health spend | 3.6% GDP |

What is included in the product

Provides a concise PESTLE evaluation of Dr. Sulaiman Al‑Habib Medical Services Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context, forward-looking insights and practical implications to guide executives, investors and strategists in risk mitigation and opportunity prioritization.

A concise, visually segmented PESTLE summary of Dr. Sulaiman Al‑Habib Medical Services Group that’s easy to drop into presentations, editable for regional or business-line notes, and ideal for quick alignment in planning sessions addressing external risks and market positioning.

Economic factors

Insurance penetration and payer mix

Rising private insurance coverage in Saudi Arabia expands addressable demand for Dr. Sulaiman Al‑Habib as total population reached about 36.8 million (2024) and health spending was ~4.1% of GDP (World Bank, 2023). Shifts in payer mix alter pricing power, case mix and receivables cycles; managed‑care models can compress margins, making strong revenue‑cycle management a key differentiator.

Macroeconomic growth in GCC

Non-oil diversification and population growth (GCC population ~60 million in 2024) drive higher healthcare utilization and outpatient volumes. With non-oil sectors accounting for over 60% of regional GDP in 2024, reliance on diversified revenues supports service expansion. GDP volatility from oil cycles (Brent ~85 USD/bbl in 2024) affects demand for discretionary procedures. Premium service lines and defensive demand preserve resilience, within a GCC healthcare market ~60 billion USD in 2024.

Cost inflation and FX exposure

Imported equipment, consumables, and tech subscriptions for Dr Sulaiman Al‑Habib are FX‑sensitive given the Saudi riyal peg to the US dollar at 3.75, leaving costs exposed to dollar moves. Wage inflation for skilled clinicians in 2024 (headline inflation ~2.6%) compresses margins and raises unit labor costs. Scale purchasing and vendor consolidation can lower per‑unit import and logistics spend. Pricing strategies must respect limited cost‑pass‑through in a competitive private healthcare market.

Capital intensity and financing

Hospital projects demand heavy capex with long payback—typical global benchmarks cite roughly USD 500,000–1,000,000 per acute bed and payback horizons of 7–15 years; interest-rate cycles (central bank rates up ~100–200 bps in recent cycles) materially raise WACC and can defer expansion timing. Asset-light management and operations contracts have raised ROIC by 5–10% in industry case studies, making portfolio mix between greenfield, brownfield and management contracts critical.

- Capex per bed: USD 500k–1m

- Payback: 7–15 years

- ROIC lift via asset-light: +5–10%

- Key levers: greenfield vs brownfield vs management

Medical tourism opportunities

Specialty centers at Dr Sulaiman Al-Habib can capture regional patients seeking advanced care as the global medical tourism market reached about USD 73 billion in 2023 and continued recovery into 2024 boosted cross-border care demand.

Competitive pricing and international accreditations such as JCI support inbound flows, while geopolitics and travel policies remain key determinants of patient volumes.

Service quality, bundled clinical outcomes and concierge experience are decisive for higher-margin inbound cases and repeat referrals.

- Market size: ~USD 73B (2023)

- Accreditation: JCI boosts trust

- Risk: geopolitics/travel policy sensitivity

- Priority: premium service and concierge

Vision 2030 boosts private healthcare to 65% of GDP

Rising private insurance and Saudi population ~36.8M (2024) with health spending ~4.1% of GDP expand Dr Sulaiman Al‑Habib’s addressable market; managed care shifts payer mix and margins. Non‑oil GDP >60% (2024) and GCC healthcare ~USD60B (2024) support volume growth; medical tourism ~USD73B (2023) boosts inbound premium cases. FX exposure (USD peg 3.75) and capex per bed USD500k–1m constrain margins.

| Metric | Value |

|---|---|

| Saudi pop (2024) | 36.8M |

| Health spend | ~4.1% GDP (2023) |

| GCC healthcare (2024) | ~USD60B |

| Medical tourism (2023) | ~USD73B |

| Capex/acute bed | USD500k–1M |

| Brent (2024) | ~USD85/bbl |

Full Version Awaits

Dr. Sulaiman Al-Habib Medical Services Group PESTLE Analysis

The PESTLE analysis of Dr. Sulaiman Al‑Habib Medical Services Group examines political, economic, social, technological, legal, and environmental factors affecting growth and risk. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: the content, layout, and structure visible now are exactly what you’ll download after payment.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE analysis of Dr. Sulaiman Al-Habib Medical Services Group—three-plus pages of actionable insight into political, economic, social, technological, legal and environmental forces shaping growth. Ideal for investors and strategists, it highlights risks and opportunities you can act on today. Purchase the full report for the complete, editable analysis and immediate download.

Political factors

Vision 2030 healthcare reforms

Vision 2030 prioritizes healthcare quality, access and private-sector participation, aligning with the national target to raise private-sector contribution to 65% of GDP. This drives PPPs, capacity expansion and clinical specialization that match Dr. Sulaiman Al-Habib Group's growth model. Policy continuity can unlock financing and land access, while shifts in priorities or execution pace could delay project pipelines.

Government healthcare spending

High public health budgets—Saudi public health spending was about 3.6% of GDP per WHO (latest comparable data)—underpin demand and reimbursement stability for Dr. Sulaiman Al‑Habib Medical Services Group.

Centralized procurement reforms and payer programs, including national procurement consolidation, can compress pricing and shift the hospital service mix toward cost‑effective care.

Incentives to expand into underserved regions align with Vision 2030 goals to boost private sector participation in healthcare.

However, budget reprioritization during fiscal tightening could slow expansion and cap revenue growth.

Regulatory centralization and oversight

Stronger centralized authorities like the Saudi MOH streamline standards and accreditation, raising compliance costs but favoring scale players that can absorb them; predictable oversight reduces operational risk and supports expansion planning, while regulatory delays—commonly in licensing and commissioning—can slow new facility openings by months, impacting capex deployment and time-to-revenue.

Regional geopolitical stability

Regional geopolitical stability in the GCC underpins patient flows, staffing and supply chains across a population of about 57 million (UN 2024); tensions risk disrupting cross-border expansion and medical tourism plans, while currency and trade frictions can increase imported equipment costs, making business continuity planning critical for Dr. Sulaiman Al-Habib Medical Services Group.

- Patient flows: GCC ~57M (UN 2024)

- Staffing: reliance on expatriates — vulnerability to border tensions

- Costs: trade/friction raise equipment import prices

- Action: prioritize business continuity planning

Localization and workforce nationalization

- Saudization/Nitaqat compliance

- Need for expatriate specialists vs national hires

- Incentives: training subsidies, localization rewards

- Cost pressure from tight labor markets

Vision 2030 boosts private healthcare to 65% of GDP

Vision 2030 drives private-sector healthcare growth aiming to raise private contribution to 65% of GDP, supporting PPPs and expansion. Saudi population ~35.1M (World Bank 2024) and GCC ~57M (UN 2024) underpin patient pools; public health spending ~3.6% of GDP (WHO). Centralized procurement and Saudization raise compliance and labor costs, while geopolitical risks can affect supply chains and medical tourism.

| Indicator | Value |

|---|---|

| Private-sector GDP target | 65% |

| Saudi population (2024) | 35.1M |

| GCC population (2024) | 57M |

| Public health spend | 3.6% GDP |

What is included in the product

Provides a concise PESTLE evaluation of Dr. Sulaiman Al‑Habib Medical Services Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context, forward-looking insights and practical implications to guide executives, investors and strategists in risk mitigation and opportunity prioritization.

A concise, visually segmented PESTLE summary of Dr. Sulaiman Al‑Habib Medical Services Group that’s easy to drop into presentations, editable for regional or business-line notes, and ideal for quick alignment in planning sessions addressing external risks and market positioning.

Economic factors

Insurance penetration and payer mix

Rising private insurance coverage in Saudi Arabia expands addressable demand for Dr. Sulaiman Al‑Habib as total population reached about 36.8 million (2024) and health spending was ~4.1% of GDP (World Bank, 2023). Shifts in payer mix alter pricing power, case mix and receivables cycles; managed‑care models can compress margins, making strong revenue‑cycle management a key differentiator.

Macroeconomic growth in GCC

Non-oil diversification and population growth (GCC population ~60 million in 2024) drive higher healthcare utilization and outpatient volumes. With non-oil sectors accounting for over 60% of regional GDP in 2024, reliance on diversified revenues supports service expansion. GDP volatility from oil cycles (Brent ~85 USD/bbl in 2024) affects demand for discretionary procedures. Premium service lines and defensive demand preserve resilience, within a GCC healthcare market ~60 billion USD in 2024.

Cost inflation and FX exposure

Imported equipment, consumables, and tech subscriptions for Dr Sulaiman Al‑Habib are FX‑sensitive given the Saudi riyal peg to the US dollar at 3.75, leaving costs exposed to dollar moves. Wage inflation for skilled clinicians in 2024 (headline inflation ~2.6%) compresses margins and raises unit labor costs. Scale purchasing and vendor consolidation can lower per‑unit import and logistics spend. Pricing strategies must respect limited cost‑pass‑through in a competitive private healthcare market.

Capital intensity and financing

Hospital projects demand heavy capex with long payback—typical global benchmarks cite roughly USD 500,000–1,000,000 per acute bed and payback horizons of 7–15 years; interest-rate cycles (central bank rates up ~100–200 bps in recent cycles) materially raise WACC and can defer expansion timing. Asset-light management and operations contracts have raised ROIC by 5–10% in industry case studies, making portfolio mix between greenfield, brownfield and management contracts critical.

- Capex per bed: USD 500k–1m

- Payback: 7–15 years

- ROIC lift via asset-light: +5–10%

- Key levers: greenfield vs brownfield vs management

Medical tourism opportunities

Specialty centers at Dr Sulaiman Al-Habib can capture regional patients seeking advanced care as the global medical tourism market reached about USD 73 billion in 2023 and continued recovery into 2024 boosted cross-border care demand.

Competitive pricing and international accreditations such as JCI support inbound flows, while geopolitics and travel policies remain key determinants of patient volumes.

Service quality, bundled clinical outcomes and concierge experience are decisive for higher-margin inbound cases and repeat referrals.

- Market size: ~USD 73B (2023)

- Accreditation: JCI boosts trust

- Risk: geopolitics/travel policy sensitivity

- Priority: premium service and concierge

Vision 2030 boosts private healthcare to 65% of GDP

Rising private insurance and Saudi population ~36.8M (2024) with health spending ~4.1% of GDP expand Dr Sulaiman Al‑Habib’s addressable market; managed care shifts payer mix and margins. Non‑oil GDP >60% (2024) and GCC healthcare ~USD60B (2024) support volume growth; medical tourism ~USD73B (2023) boosts inbound premium cases. FX exposure (USD peg 3.75) and capex per bed USD500k–1m constrain margins.

| Metric | Value |

|---|---|

| Saudi pop (2024) | 36.8M |

| Health spend | ~4.1% GDP (2023) |

| GCC healthcare (2024) | ~USD60B |

| Medical tourism (2023) | ~USD73B |

| Capex/acute bed | USD500k–1M |

| Brent (2024) | ~USD85/bbl |

Full Version Awaits

Dr. Sulaiman Al-Habib Medical Services Group PESTLE Analysis

The PESTLE analysis of Dr. Sulaiman Al‑Habib Medical Services Group examines political, economic, social, technological, legal, and environmental factors affecting growth and risk. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: the content, layout, and structure visible now are exactly what you’ll download after payment.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE analysis of Dr. Sulaiman Al-Habib Medical Services Group—three-plus pages of actionable insight into political, economic, social, technological, legal and environmental forces shaping growth. Ideal for investors and strategists, it highlights risks and opportunities you can act on today. Purchase the full report for the complete, editable analysis and immediate download.

Political factors

Vision 2030 healthcare reforms

Vision 2030 prioritizes healthcare quality, access and private-sector participation, aligning with the national target to raise private-sector contribution to 65% of GDP. This drives PPPs, capacity expansion and clinical specialization that match Dr. Sulaiman Al-Habib Group's growth model. Policy continuity can unlock financing and land access, while shifts in priorities or execution pace could delay project pipelines.

Government healthcare spending

High public health budgets—Saudi public health spending was about 3.6% of GDP per WHO (latest comparable data)—underpin demand and reimbursement stability for Dr. Sulaiman Al‑Habib Medical Services Group.

Centralized procurement reforms and payer programs, including national procurement consolidation, can compress pricing and shift the hospital service mix toward cost‑effective care.

Incentives to expand into underserved regions align with Vision 2030 goals to boost private sector participation in healthcare.

However, budget reprioritization during fiscal tightening could slow expansion and cap revenue growth.

Regulatory centralization and oversight

Stronger centralized authorities like the Saudi MOH streamline standards and accreditation, raising compliance costs but favoring scale players that can absorb them; predictable oversight reduces operational risk and supports expansion planning, while regulatory delays—commonly in licensing and commissioning—can slow new facility openings by months, impacting capex deployment and time-to-revenue.

Regional geopolitical stability

Regional geopolitical stability in the GCC underpins patient flows, staffing and supply chains across a population of about 57 million (UN 2024); tensions risk disrupting cross-border expansion and medical tourism plans, while currency and trade frictions can increase imported equipment costs, making business continuity planning critical for Dr. Sulaiman Al-Habib Medical Services Group.

- Patient flows: GCC ~57M (UN 2024)

- Staffing: reliance on expatriates — vulnerability to border tensions

- Costs: trade/friction raise equipment import prices

- Action: prioritize business continuity planning

Localization and workforce nationalization

- Saudization/Nitaqat compliance

- Need for expatriate specialists vs national hires

- Incentives: training subsidies, localization rewards

- Cost pressure from tight labor markets

Vision 2030 boosts private healthcare to 65% of GDP

Vision 2030 drives private-sector healthcare growth aiming to raise private contribution to 65% of GDP, supporting PPPs and expansion. Saudi population ~35.1M (World Bank 2024) and GCC ~57M (UN 2024) underpin patient pools; public health spending ~3.6% of GDP (WHO). Centralized procurement and Saudization raise compliance and labor costs, while geopolitical risks can affect supply chains and medical tourism.

| Indicator | Value |

|---|---|

| Private-sector GDP target | 65% |

| Saudi population (2024) | 35.1M |

| GCC population (2024) | 57M |

| Public health spend | 3.6% GDP |

What is included in the product

Provides a concise PESTLE evaluation of Dr. Sulaiman Al‑Habib Medical Services Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, region-specific regulatory context, forward-looking insights and practical implications to guide executives, investors and strategists in risk mitigation and opportunity prioritization.

A concise, visually segmented PESTLE summary of Dr. Sulaiman Al‑Habib Medical Services Group that’s easy to drop into presentations, editable for regional or business-line notes, and ideal for quick alignment in planning sessions addressing external risks and market positioning.

Economic factors

Insurance penetration and payer mix

Rising private insurance coverage in Saudi Arabia expands addressable demand for Dr. Sulaiman Al‑Habib as total population reached about 36.8 million (2024) and health spending was ~4.1% of GDP (World Bank, 2023). Shifts in payer mix alter pricing power, case mix and receivables cycles; managed‑care models can compress margins, making strong revenue‑cycle management a key differentiator.

Macroeconomic growth in GCC

Non-oil diversification and population growth (GCC population ~60 million in 2024) drive higher healthcare utilization and outpatient volumes. With non-oil sectors accounting for over 60% of regional GDP in 2024, reliance on diversified revenues supports service expansion. GDP volatility from oil cycles (Brent ~85 USD/bbl in 2024) affects demand for discretionary procedures. Premium service lines and defensive demand preserve resilience, within a GCC healthcare market ~60 billion USD in 2024.

Cost inflation and FX exposure

Imported equipment, consumables, and tech subscriptions for Dr Sulaiman Al‑Habib are FX‑sensitive given the Saudi riyal peg to the US dollar at 3.75, leaving costs exposed to dollar moves. Wage inflation for skilled clinicians in 2024 (headline inflation ~2.6%) compresses margins and raises unit labor costs. Scale purchasing and vendor consolidation can lower per‑unit import and logistics spend. Pricing strategies must respect limited cost‑pass‑through in a competitive private healthcare market.

Capital intensity and financing

Hospital projects demand heavy capex with long payback—typical global benchmarks cite roughly USD 500,000–1,000,000 per acute bed and payback horizons of 7–15 years; interest-rate cycles (central bank rates up ~100–200 bps in recent cycles) materially raise WACC and can defer expansion timing. Asset-light management and operations contracts have raised ROIC by 5–10% in industry case studies, making portfolio mix between greenfield, brownfield and management contracts critical.

- Capex per bed: USD 500k–1m

- Payback: 7–15 years

- ROIC lift via asset-light: +5–10%

- Key levers: greenfield vs brownfield vs management

Medical tourism opportunities

Specialty centers at Dr Sulaiman Al-Habib can capture regional patients seeking advanced care as the global medical tourism market reached about USD 73 billion in 2023 and continued recovery into 2024 boosted cross-border care demand.

Competitive pricing and international accreditations such as JCI support inbound flows, while geopolitics and travel policies remain key determinants of patient volumes.

Service quality, bundled clinical outcomes and concierge experience are decisive for higher-margin inbound cases and repeat referrals.

- Market size: ~USD 73B (2023)

- Accreditation: JCI boosts trust

- Risk: geopolitics/travel policy sensitivity

- Priority: premium service and concierge

Vision 2030 boosts private healthcare to 65% of GDP

Rising private insurance and Saudi population ~36.8M (2024) with health spending ~4.1% of GDP expand Dr Sulaiman Al‑Habib’s addressable market; managed care shifts payer mix and margins. Non‑oil GDP >60% (2024) and GCC healthcare ~USD60B (2024) support volume growth; medical tourism ~USD73B (2023) boosts inbound premium cases. FX exposure (USD peg 3.75) and capex per bed USD500k–1m constrain margins.

| Metric | Value |

|---|---|

| Saudi pop (2024) | 36.8M |

| Health spend | ~4.1% GDP (2023) |

| GCC healthcare (2024) | ~USD60B |

| Medical tourism (2023) | ~USD73B |

| Capex/acute bed | USD500k–1M |

| Brent (2024) | ~USD85/bbl |

Full Version Awaits

Dr. Sulaiman Al-Habib Medical Services Group PESTLE Analysis

The PESTLE analysis of Dr. Sulaiman Al‑Habib Medical Services Group examines political, economic, social, technological, legal, and environmental factors affecting growth and risk. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers: the content, layout, and structure visible now are exactly what you’ll download after payment.