Hennes & Mauritz PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping Hennes & Mauritz’s strategic landscape in our concise PESTLE snapshot. This analysis highlights key external risks and growth levers to inform investors and strategists. Purchase the full PESTLE to get actionable, editable insights and data-driven recommendations for immediate use.

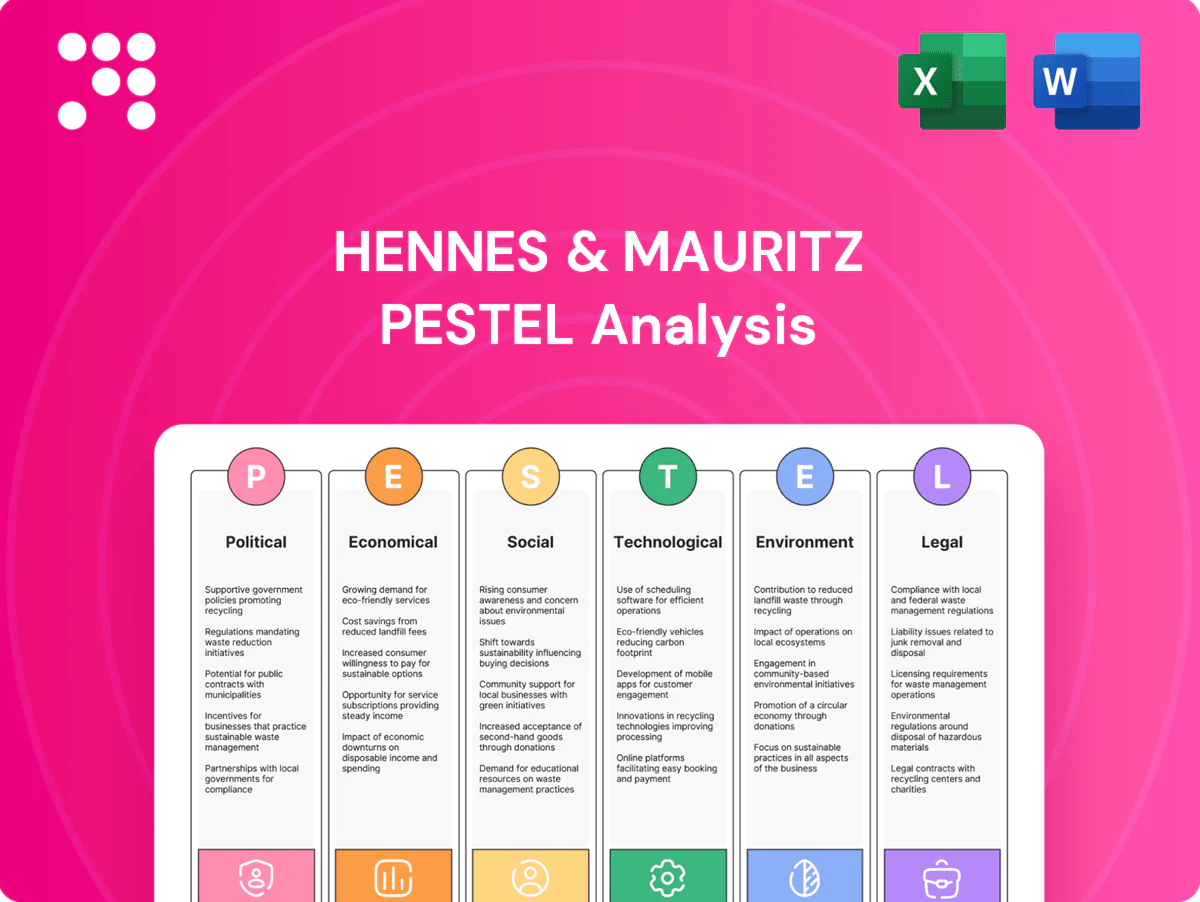

Political factors

Trade policies and tariffs

Changes in trade agreements and tariff regimes directly affect H&M’s sourcing costs and pricing flexibility; with H&M Group net sales SEK 199.3 billion in 2024 and over half of purchases sourced from Asia, a 5–10% tariff swing materially alters margins. Protectionist measures in key markets can slow inventory flow and compress gross margin. Preferential trade agreements boost competitiveness but raise dependence on specific corridors. Continuous lobbying and diversified sourcing mitigate shocks.

Labor standards in sourcing countries

Government labor enforcement in manufacturing hubs like Bangladesh, which employs about 4 million garment workers, shapes supplier compliance and H&M's cost structures. Stricter wage and safety mandates push factory costs and FOB prices higher, while weak enforcement invites reputational damage and activism. H&M must align buying practices with evolving national policies to secure supply continuity and brand trust.

Geopolitical instability and logistics

Conflicts, sanctions and port disruptions (e.g., Red Sea route diversions adding 10–14 days) can delay H&M shipments and trigger rerouting costs; over 70% of H&M sourcing remains Asia‑focused, amplifying lead‑time uncertainty in politically fragile suppliers. Insurance and buffer inventory strategies have become costlier, with shipping insurance premiums rising sharply during 2022–24 (up to ~30% in high‑risk zones), making multi‑hub logistics planning essential for resilience.

Market entry and localization policies

Market entry and localization policies — including foreign investment caps, local content quotas and store licensing — directly shape H&M’s expansion pacing; H&M Group operated about 4,600 stores and e‑commerce in 75 markets in 2024, forcing tailored formats and supply nodes. Many governments push local e‑commerce warehousing to create jobs; tax holidays of 3–5 years or conditional incentives can raise ROI but add compliance costs.

- Foreign investment limits: affect JV vs wholly owned

- Local content requirements: impact sourcing and margins

- Warehousing mandates: raise capex, create jobs

- Tax holidays 3–5 yrs: improve ROI, often conditional

Sustainability and reporting mandates

- CSRD scope ~50,000 companies from 2024

- Due diligence rules push multi-tier supplier transparency

- Non-compliance: sanctions and market access limits

- Early adoption: regulatory and consumer trust edge

Tariffs, Asian sourcing and Red Sea disruptions threaten margins, costs, and compliance

Trade tariffs and protectionism materially affect H&M (net sales SEK 199.3bn 2024) as >50% purchases come from Asia; a 5–10% tariff swing can compress margins. Labor rules in hubs like Bangladesh (≈4m garment workers) raise FOB costs and compliance spend. Geopolitical disruptions (Red Sea diversions +10–14 days) and rising insurance (+~30% 2022–24) increase logistics risk. CSRD expansion (~50,000 firms from 2024) intensifies disclosure and due diligence burdens.

| Risk | Metric |

|---|---|

| Tariff sensitivity | 5–10% margin impact |

| Sourcing concentration | >50% Asia |

| Sales 2024 | SEK 199.3bn |

| Logistics delay | +10–14 days |

| Insurance rise | ~+30% (2022–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hennes & Mauritz across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—linking each to industry and regional specifics. Every section is data-driven, forward-looking, and formatted for direct use in strategy, investor materials, or scenario planning.

A concise, visually segmented PESTLE summary of Hennes & Mauritz for quick reference in meetings, easily droppable into presentations and annotated with region-specific notes to support external risk discussions and fast team alignment.

Economic factors

Consumer demand cycles

Macro slowdowns (IMF 2024 world GDP forecast 3.1%) and real-income squeeze push shoppers toward smaller baskets and value-led SKUs, reducing ASPs and shifting mix to basics. Recovery phases lift discretionary spend on trend-led assortments, boosting sell-through on fast-fashion ranges. H&M’s price architecture must flex via targeted promotions and tiered pricing to protect traffic and margin. Agile inventory and rapid replenishment buffer demand whiplash.

FX volatility and cost base

FX swings between SEK, USD and Asian sourcing currencies materially affect H&M’s COGS and reported EBIT; SEK moved about 10% versus USD in 2024, increasing cost pressure on Asia-heavy sourcing (around 70% of suppliers). H&M hedges a significant portion of forecasted flows (~60%), but prolonged moves still pass through to margins. Pricing power differs by market amid strong competition, while balanced regional currency exposure helps dampen earnings volatility.

Inflation and input costs

Rising energy, freight and raw-materials costs—cotton futures climbed about 40% from 2020–2022 before normalising in 2023—remain key drivers of input-cost inflation for Hennes & Mauritz, increasing sourcing and distribution expenses. Persistent inflation in 2024 has the potential to compress gross margins unless H&M offsets via price increases, product mix shifts or productivity gains. Promotional intensity tends to rise as consumers trade down, pressuring retail margins and inventory turnover. Closer supplier collaboration and design-to-cost programs are critical levers to protect margin and sustainability targets.

Omnichannel profitability

Online growth expands H&Ms reach but increases fulfillment, returns and last-mile costs; ecommerce accounted for about 30% of group sales in 2024 while the group operated roughly 4,900 stores (2024). Physical stores sustain brand presence and enable cost-efficient click-and-collect. Channel-specific assortments raise contribution margins and unified inventory lowers markdowns and stockouts.

- online_share_2024: ~30%

- store_count_2024: ~4,900

- benefit: click-and-collect efficiency

- impact: higher fulfillment & returns costs

Labor markets and wages

Retail and logistics wage inflation is lifting operating expenses in developed markets, with Eurostat reporting EU hourly labour costs up about 4.8% in 2023 and upward momentum into 2024; tight labour pools are constraining store staffing and service levels. Productivity tools and scheduling optimisation can materially offset pressures by improving hours per sales unit, while supplier-country wage shifts — China average wages rose roughly 6.0% in 2023 (NBS) — influence sourcing footprints and nearshoring decisions.

- Operating costs: EU hourly labour costs +4.8% (2023)

- Supplier wages: China wages ~+6.0% (2023)

- Mitigation: scheduling optimisation, productivity tools

- Risk: tighter labour pools → staffing/service strain

Tariffs, Asian sourcing and Red Sea disruptions threaten margins, costs, and compliance

Macro slowdown (IMF 2024 world GDP 3.1%) and real-income squeeze shift demand to value SKUs, pressuring ASPs while recoveries boost fast-fashion sell-through. FX volatility (SEK ~10% vs USD in 2024) and input inflation (cotton +40% 2020–22) raise COGS; H&M hedges ~60% of flows. Ecommerce ~30% of sales (2024) increases fulfillment/returns costs despite click-and-collect benefits.

| Metric | Value |

|---|---|

| World GDP (IMF 2024) | 3.1% |

| Online share (2024) | ~30% |

| Store count (2024) | ~4,900 |

| SEK vs USD (2024) | ~10% move |

| Hedging | ~60% flows |

Same Document Delivered

Hennes & Mauritz PESTLE Analysis

This Hennes & Mauritz PESTLE Analysis delivers a concise, actionable evaluation of political, economic, social, technological, legal and environmental factors affecting H&M. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains real data, structured insights and recommendations to support strategy and investment decisions.

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping Hennes & Mauritz’s strategic landscape in our concise PESTLE snapshot. This analysis highlights key external risks and growth levers to inform investors and strategists. Purchase the full PESTLE to get actionable, editable insights and data-driven recommendations for immediate use.

Political factors

Trade policies and tariffs

Changes in trade agreements and tariff regimes directly affect H&M’s sourcing costs and pricing flexibility; with H&M Group net sales SEK 199.3 billion in 2024 and over half of purchases sourced from Asia, a 5–10% tariff swing materially alters margins. Protectionist measures in key markets can slow inventory flow and compress gross margin. Preferential trade agreements boost competitiveness but raise dependence on specific corridors. Continuous lobbying and diversified sourcing mitigate shocks.

Labor standards in sourcing countries

Government labor enforcement in manufacturing hubs like Bangladesh, which employs about 4 million garment workers, shapes supplier compliance and H&M's cost structures. Stricter wage and safety mandates push factory costs and FOB prices higher, while weak enforcement invites reputational damage and activism. H&M must align buying practices with evolving national policies to secure supply continuity and brand trust.

Geopolitical instability and logistics

Conflicts, sanctions and port disruptions (e.g., Red Sea route diversions adding 10–14 days) can delay H&M shipments and trigger rerouting costs; over 70% of H&M sourcing remains Asia‑focused, amplifying lead‑time uncertainty in politically fragile suppliers. Insurance and buffer inventory strategies have become costlier, with shipping insurance premiums rising sharply during 2022–24 (up to ~30% in high‑risk zones), making multi‑hub logistics planning essential for resilience.

Market entry and localization policies

Market entry and localization policies — including foreign investment caps, local content quotas and store licensing — directly shape H&M’s expansion pacing; H&M Group operated about 4,600 stores and e‑commerce in 75 markets in 2024, forcing tailored formats and supply nodes. Many governments push local e‑commerce warehousing to create jobs; tax holidays of 3–5 years or conditional incentives can raise ROI but add compliance costs.

- Foreign investment limits: affect JV vs wholly owned

- Local content requirements: impact sourcing and margins

- Warehousing mandates: raise capex, create jobs

- Tax holidays 3–5 yrs: improve ROI, often conditional

Sustainability and reporting mandates

- CSRD scope ~50,000 companies from 2024

- Due diligence rules push multi-tier supplier transparency

- Non-compliance: sanctions and market access limits

- Early adoption: regulatory and consumer trust edge

Tariffs, Asian sourcing and Red Sea disruptions threaten margins, costs, and compliance

Trade tariffs and protectionism materially affect H&M (net sales SEK 199.3bn 2024) as >50% purchases come from Asia; a 5–10% tariff swing can compress margins. Labor rules in hubs like Bangladesh (≈4m garment workers) raise FOB costs and compliance spend. Geopolitical disruptions (Red Sea diversions +10–14 days) and rising insurance (+~30% 2022–24) increase logistics risk. CSRD expansion (~50,000 firms from 2024) intensifies disclosure and due diligence burdens.

| Risk | Metric |

|---|---|

| Tariff sensitivity | 5–10% margin impact |

| Sourcing concentration | >50% Asia |

| Sales 2024 | SEK 199.3bn |

| Logistics delay | +10–14 days |

| Insurance rise | ~+30% (2022–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hennes & Mauritz across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—linking each to industry and regional specifics. Every section is data-driven, forward-looking, and formatted for direct use in strategy, investor materials, or scenario planning.

A concise, visually segmented PESTLE summary of Hennes & Mauritz for quick reference in meetings, easily droppable into presentations and annotated with region-specific notes to support external risk discussions and fast team alignment.

Economic factors

Consumer demand cycles

Macro slowdowns (IMF 2024 world GDP forecast 3.1%) and real-income squeeze push shoppers toward smaller baskets and value-led SKUs, reducing ASPs and shifting mix to basics. Recovery phases lift discretionary spend on trend-led assortments, boosting sell-through on fast-fashion ranges. H&M’s price architecture must flex via targeted promotions and tiered pricing to protect traffic and margin. Agile inventory and rapid replenishment buffer demand whiplash.

FX volatility and cost base

FX swings between SEK, USD and Asian sourcing currencies materially affect H&M’s COGS and reported EBIT; SEK moved about 10% versus USD in 2024, increasing cost pressure on Asia-heavy sourcing (around 70% of suppliers). H&M hedges a significant portion of forecasted flows (~60%), but prolonged moves still pass through to margins. Pricing power differs by market amid strong competition, while balanced regional currency exposure helps dampen earnings volatility.

Inflation and input costs

Rising energy, freight and raw-materials costs—cotton futures climbed about 40% from 2020–2022 before normalising in 2023—remain key drivers of input-cost inflation for Hennes & Mauritz, increasing sourcing and distribution expenses. Persistent inflation in 2024 has the potential to compress gross margins unless H&M offsets via price increases, product mix shifts or productivity gains. Promotional intensity tends to rise as consumers trade down, pressuring retail margins and inventory turnover. Closer supplier collaboration and design-to-cost programs are critical levers to protect margin and sustainability targets.

Omnichannel profitability

Online growth expands H&Ms reach but increases fulfillment, returns and last-mile costs; ecommerce accounted for about 30% of group sales in 2024 while the group operated roughly 4,900 stores (2024). Physical stores sustain brand presence and enable cost-efficient click-and-collect. Channel-specific assortments raise contribution margins and unified inventory lowers markdowns and stockouts.

- online_share_2024: ~30%

- store_count_2024: ~4,900

- benefit: click-and-collect efficiency

- impact: higher fulfillment & returns costs

Labor markets and wages

Retail and logistics wage inflation is lifting operating expenses in developed markets, with Eurostat reporting EU hourly labour costs up about 4.8% in 2023 and upward momentum into 2024; tight labour pools are constraining store staffing and service levels. Productivity tools and scheduling optimisation can materially offset pressures by improving hours per sales unit, while supplier-country wage shifts — China average wages rose roughly 6.0% in 2023 (NBS) — influence sourcing footprints and nearshoring decisions.

- Operating costs: EU hourly labour costs +4.8% (2023)

- Supplier wages: China wages ~+6.0% (2023)

- Mitigation: scheduling optimisation, productivity tools

- Risk: tighter labour pools → staffing/service strain

Tariffs, Asian sourcing and Red Sea disruptions threaten margins, costs, and compliance

Macro slowdown (IMF 2024 world GDP 3.1%) and real-income squeeze shift demand to value SKUs, pressuring ASPs while recoveries boost fast-fashion sell-through. FX volatility (SEK ~10% vs USD in 2024) and input inflation (cotton +40% 2020–22) raise COGS; H&M hedges ~60% of flows. Ecommerce ~30% of sales (2024) increases fulfillment/returns costs despite click-and-collect benefits.

| Metric | Value |

|---|---|

| World GDP (IMF 2024) | 3.1% |

| Online share (2024) | ~30% |

| Store count (2024) | ~4,900 |

| SEK vs USD (2024) | ~10% move |

| Hedging | ~60% flows |

Same Document Delivered

Hennes & Mauritz PESTLE Analysis

This Hennes & Mauritz PESTLE Analysis delivers a concise, actionable evaluation of political, economic, social, technological, legal and environmental factors affecting H&M. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains real data, structured insights and recommendations to support strategy and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures are reshaping Hennes & Mauritz’s strategic landscape in our concise PESTLE snapshot. This analysis highlights key external risks and growth levers to inform investors and strategists. Purchase the full PESTLE to get actionable, editable insights and data-driven recommendations for immediate use.

Political factors

Trade policies and tariffs

Changes in trade agreements and tariff regimes directly affect H&M’s sourcing costs and pricing flexibility; with H&M Group net sales SEK 199.3 billion in 2024 and over half of purchases sourced from Asia, a 5–10% tariff swing materially alters margins. Protectionist measures in key markets can slow inventory flow and compress gross margin. Preferential trade agreements boost competitiveness but raise dependence on specific corridors. Continuous lobbying and diversified sourcing mitigate shocks.

Labor standards in sourcing countries

Government labor enforcement in manufacturing hubs like Bangladesh, which employs about 4 million garment workers, shapes supplier compliance and H&M's cost structures. Stricter wage and safety mandates push factory costs and FOB prices higher, while weak enforcement invites reputational damage and activism. H&M must align buying practices with evolving national policies to secure supply continuity and brand trust.

Geopolitical instability and logistics

Conflicts, sanctions and port disruptions (e.g., Red Sea route diversions adding 10–14 days) can delay H&M shipments and trigger rerouting costs; over 70% of H&M sourcing remains Asia‑focused, amplifying lead‑time uncertainty in politically fragile suppliers. Insurance and buffer inventory strategies have become costlier, with shipping insurance premiums rising sharply during 2022–24 (up to ~30% in high‑risk zones), making multi‑hub logistics planning essential for resilience.

Market entry and localization policies

Market entry and localization policies — including foreign investment caps, local content quotas and store licensing — directly shape H&M’s expansion pacing; H&M Group operated about 4,600 stores and e‑commerce in 75 markets in 2024, forcing tailored formats and supply nodes. Many governments push local e‑commerce warehousing to create jobs; tax holidays of 3–5 years or conditional incentives can raise ROI but add compliance costs.

- Foreign investment limits: affect JV vs wholly owned

- Local content requirements: impact sourcing and margins

- Warehousing mandates: raise capex, create jobs

- Tax holidays 3–5 yrs: improve ROI, often conditional

Sustainability and reporting mandates

- CSRD scope ~50,000 companies from 2024

- Due diligence rules push multi-tier supplier transparency

- Non-compliance: sanctions and market access limits

- Early adoption: regulatory and consumer trust edge

Tariffs, Asian sourcing and Red Sea disruptions threaten margins, costs, and compliance

Trade tariffs and protectionism materially affect H&M (net sales SEK 199.3bn 2024) as >50% purchases come from Asia; a 5–10% tariff swing can compress margins. Labor rules in hubs like Bangladesh (≈4m garment workers) raise FOB costs and compliance spend. Geopolitical disruptions (Red Sea diversions +10–14 days) and rising insurance (+~30% 2022–24) increase logistics risk. CSRD expansion (~50,000 firms from 2024) intensifies disclosure and due diligence burdens.

| Risk | Metric |

|---|---|

| Tariff sensitivity | 5–10% margin impact |

| Sourcing concentration | >50% Asia |

| Sales 2024 | SEK 199.3bn |

| Logistics delay | +10–14 days |

| Insurance rise | ~+30% (2022–24) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hennes & Mauritz across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—linking each to industry and regional specifics. Every section is data-driven, forward-looking, and formatted for direct use in strategy, investor materials, or scenario planning.

A concise, visually segmented PESTLE summary of Hennes & Mauritz for quick reference in meetings, easily droppable into presentations and annotated with region-specific notes to support external risk discussions and fast team alignment.

Economic factors

Consumer demand cycles

Macro slowdowns (IMF 2024 world GDP forecast 3.1%) and real-income squeeze push shoppers toward smaller baskets and value-led SKUs, reducing ASPs and shifting mix to basics. Recovery phases lift discretionary spend on trend-led assortments, boosting sell-through on fast-fashion ranges. H&M’s price architecture must flex via targeted promotions and tiered pricing to protect traffic and margin. Agile inventory and rapid replenishment buffer demand whiplash.

FX volatility and cost base

FX swings between SEK, USD and Asian sourcing currencies materially affect H&M’s COGS and reported EBIT; SEK moved about 10% versus USD in 2024, increasing cost pressure on Asia-heavy sourcing (around 70% of suppliers). H&M hedges a significant portion of forecasted flows (~60%), but prolonged moves still pass through to margins. Pricing power differs by market amid strong competition, while balanced regional currency exposure helps dampen earnings volatility.

Inflation and input costs

Rising energy, freight and raw-materials costs—cotton futures climbed about 40% from 2020–2022 before normalising in 2023—remain key drivers of input-cost inflation for Hennes & Mauritz, increasing sourcing and distribution expenses. Persistent inflation in 2024 has the potential to compress gross margins unless H&M offsets via price increases, product mix shifts or productivity gains. Promotional intensity tends to rise as consumers trade down, pressuring retail margins and inventory turnover. Closer supplier collaboration and design-to-cost programs are critical levers to protect margin and sustainability targets.

Omnichannel profitability

Online growth expands H&Ms reach but increases fulfillment, returns and last-mile costs; ecommerce accounted for about 30% of group sales in 2024 while the group operated roughly 4,900 stores (2024). Physical stores sustain brand presence and enable cost-efficient click-and-collect. Channel-specific assortments raise contribution margins and unified inventory lowers markdowns and stockouts.

- online_share_2024: ~30%

- store_count_2024: ~4,900

- benefit: click-and-collect efficiency

- impact: higher fulfillment & returns costs

Labor markets and wages

Retail and logistics wage inflation is lifting operating expenses in developed markets, with Eurostat reporting EU hourly labour costs up about 4.8% in 2023 and upward momentum into 2024; tight labour pools are constraining store staffing and service levels. Productivity tools and scheduling optimisation can materially offset pressures by improving hours per sales unit, while supplier-country wage shifts — China average wages rose roughly 6.0% in 2023 (NBS) — influence sourcing footprints and nearshoring decisions.

- Operating costs: EU hourly labour costs +4.8% (2023)

- Supplier wages: China wages ~+6.0% (2023)

- Mitigation: scheduling optimisation, productivity tools

- Risk: tighter labour pools → staffing/service strain

Tariffs, Asian sourcing and Red Sea disruptions threaten margins, costs, and compliance

Macro slowdown (IMF 2024 world GDP 3.1%) and real-income squeeze shift demand to value SKUs, pressuring ASPs while recoveries boost fast-fashion sell-through. FX volatility (SEK ~10% vs USD in 2024) and input inflation (cotton +40% 2020–22) raise COGS; H&M hedges ~60% of flows. Ecommerce ~30% of sales (2024) increases fulfillment/returns costs despite click-and-collect benefits.

| Metric | Value |

|---|---|

| World GDP (IMF 2024) | 3.1% |

| Online share (2024) | ~30% |

| Store count (2024) | ~4,900 |

| SEK vs USD (2024) | ~10% move |

| Hedging | ~60% flows |

Same Document Delivered

Hennes & Mauritz PESTLE Analysis

This Hennes & Mauritz PESTLE Analysis delivers a concise, actionable evaluation of political, economic, social, technological, legal and environmental factors affecting H&M. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains real data, structured insights and recommendations to support strategy and investment decisions.