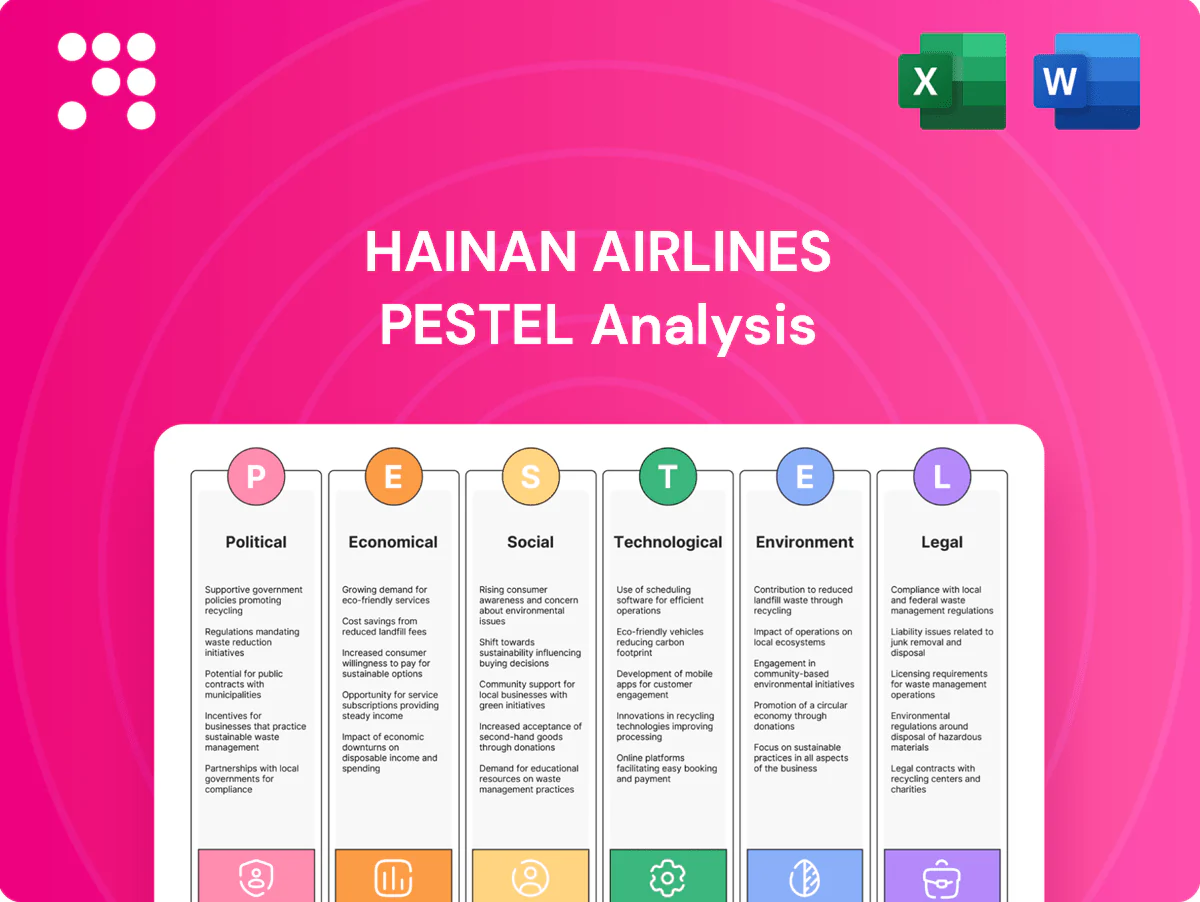

Hainan Airlines PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our focused PESTLE Analysis of Hainan Airlines—three concise sections reveal how politics, economy, society, technology, law, and environment will shape its trajectory. Ideal for investors and strategists who need vetted, actionable intelligence fast. Purchase the full report to get the complete, downloadable breakdown and start making smarter decisions today.

Political factors

State oversight and CAAC policy

CAAC tightly guides route rights, slot allocation, pricing discipline and safety compliance, and its 2024 directives prioritizing Hainan Free Trade Port corridors mean Hainan Airlines must align fleet and network plans with national targets. Policy shifts can rapidly reallocate capacity or favor strategic routes, directly affecting unit revenue and load factors. Supportive CAAC measures can unlock international growth; restrictive rulings compress margins and constrain expansion.

Bilateral air service agreements

Bilateral air service agreements determine Hainan Airlines' access to Europe, North America, Asia and Africa; China had ASAs with over 60 countries in 2024, shaping route opportunities. Negotiation outcomes set permitted frequencies, aircraft gauge and partner access, directly affecting capacity and yields. Favorable pacts enable premium long‑haul connectivity while stalled agreements cap growth; major domestic and foreign carriers actively lobby for the same scarce rights.

Geopolitical tensions and sanctions

US–China and EU–China frictions constrain aircraft procurement, overflight permissions and demand for Hainan Airlines, with IATA reporting global RPKs recovered to 94% of 2019 by July 2024, highlighting sensitivity to cross-border flow changes.

Sanctions and export controls have already disrupted parts and advanced-tech access, increasing supplier risk and delivery delays for airframes and avionics.

Stricter visa regimes and security reviews suppress passenger flow on key routes, while geopolitics drives yield and capacity volatility, complicating short-term network and fleet planning.

National strategies and Hainan FTP

Beijing’s 2020 Hainan Free Trade Port blueprint and the dual circulation strategy (since 2020) aim for an initial high‑level FTP by 2025 and deeper opening by 2035, which should expand tourism and logistics flows to the island.

Preferential tax, duty‑free expansion and visa facilitation lift inbound traffic, letting Hainan Airlines position Haikou and Sanya as international gateways; the pace of policy rollout will drive how much traffic and revenue materialize.

- Tags: policy-milestones-2025

- Tags: dual-circulation-2020

- Tags: gateways-Haikou-Sanya

- Tags: execution-risk

Belt and Road route priorities

Belt and Road route priorities, launched under the BRI in 2013, steer Hainan Airlines toward developing Central Asia, Middle East and Africa links; Hainan was designated a free trade port in 2020, which supports outbound aviation expansion. Political backing can ease bilateral approvals and marketing support, but initial traffic on these corridors is often developmental rather than immediately profitable, requiring patient network investment and active risk management for politically sensitive destinations.

- BRI origin year: 2013

- Hainan FTZ designation: 2020

- Focus regions: Central Asia, Middle East, Africa

- Strategy: patient investment + robust political risk controls

CAAC 2024 shifts networks; ASAs 60+, RPKs at 94% of 2019

CAAC 2024 directives force Hainan Airlines to align fleet and routes with Hainan FTP priorities; CAAC controls slots, pricing and safety. China had ASAs with 60+ countries in 2024, shaping international access. IATA RPKs reached 94% of 2019 by Jul 2024, showing sensitivity to geopolitics and sanctions.

| Metric | Value |

|---|---|

| CAAC 2024 policy | FTP priority |

| ASAs (2024) | 60+ |

| IATA RPKs (Jul 2024) | 94% of 2019 |

What is included in the product

Explores how macro-environmental factors uniquely affect Hainan Airlines across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it highlights threats, opportunities and forward-looking insights to inform strategy, scenario-planning and funding decisions.

A compact, PESTLE‑segmented summary of Hainan Airlines' external environment that can be dropped into presentations, edited for regional or business‑line context, and easily shared across teams to streamline risk discussions and strategic planning.

Economic factors

Fuel price and FX sensitivity

Jet fuel accounted for roughly 25% of Hainan Airlines operating costs, with Brent averaging about $82/bbl in 2024—swings materially lift CASK; USD-denominated expenses and aircraft leases (significant share of capex/leases ~10–15% of opex) expose earnings to RMB/USD ~7.2, hedging mitigates volatility but introduces basis and liquidity risk, while fuel-efficiency measures and fuel surcharges remain key levers.

China travel demand cycles

China's 2023 GDP grew 5.2% (official) and domestic air traffic reached about 543 million passengers in 2023 (CAAC), supporting higher seat factors and yields during strong demand periods. Leisure rebounds and Golden Week spikes create pronounced revenue peaks versus off‑peak softness. Business travel recovery is lifting premium cabin loadings. Macroeconomic slowdowns compress fares and ancillary spend, pressuring margins.

Fleet capex and interest rates

Fleet renewal requires large capex or lease commitments, typically $60–80m for a new narrowbody and $200–300m for a widebody. Higher global policy rates, around 5.25% mid‑2025, raise borrowing costs and lease rentals, squeezing cash flow. Staggered deliveries and sale–leasebacks smooth outflows, while utilization and residual values are the key drivers of ROIC.

Competitive intensity

Rivalry with Air China, China Eastern and China Southern—which together account for roughly 60% of domestic seat capacity—and rising LCC share (~10% in 2024) compresses yields for Hainan Airlines; slot scarcity at Beijing and Shanghai tier-1 airports caps growth and pricing power. Partnerships and codeshares boost connectivity and network economics, while service and on-time reliability remain key differentiators for premium pricing.

- Big-3 capacity share ~60% (2024)

- LCC share ~10% (2024)

- Tier-1 slot constraints limit expansion

- Codeshares improve network yields

- Service/reliability = pricing leverage

Cargo and e-commerce cycles

Post-pandemic cargo yields surged roughly 50% in 2020–22 and by 2024 had largely normalized to about 20–30% above 2019 levels (IATA), while China’s online retail of physical goods reached ~RMB 13.4 trillion in 2023, sustaining parcel volumes into 2024–25 but with mid-single-digit growth. Belly-capacity recovery increased available tonnage, pressuring yields and load factors; cold-chain and special cargo command 15–40% premiums, adding margin diversity for Hainan Airlines.

- Cargo yields: peak +~50% (2020–22), normalized to +20–30% vs 2019 (2024)

- China e-commerce: ~RMB 13.4 trillion online retail (2023), slower growth 2024–25

- Belly recovery: higher capacity → pricing pressure

- Cold-chain/special cargo: +15–40% margin premium

CAAC 2024 shifts networks; ASAs 60+, RPKs at 94% of 2019

Jet fuel ~25% of opex; Brent ~$82/bbl (2024) and RMB/USD ~7.2 expose earnings; hedging and efficiency critical. China demand: 543m domestic pax (2023), GDP +5.2% (2023); Big‑3 ~60% capacity, LCC ~10% (2024). Fleet capex narrowbody $60–80m, widebody $200–300m; policy rates ~5.25% mid‑2025 raise financing cost.

| Metric | Value |

|---|---|

| Jet fuel share | ~25% |

| Brent (2024) | $82/bbl |

| Domestic pax (2023) | 543m |

| Policy rate (mid‑2025) | ~5.25% |

What You See Is What You Get

Hainan Airlines PESTLE Analysis

The Hainan Airlines PESTLE Analysis preview shown here is the exact document you’ll receive after purchase — fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors specific to Hainan Airlines. No placeholders or teasers; this is the final, downloadable file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our focused PESTLE Analysis of Hainan Airlines—three concise sections reveal how politics, economy, society, technology, law, and environment will shape its trajectory. Ideal for investors and strategists who need vetted, actionable intelligence fast. Purchase the full report to get the complete, downloadable breakdown and start making smarter decisions today.

Political factors

State oversight and CAAC policy

CAAC tightly guides route rights, slot allocation, pricing discipline and safety compliance, and its 2024 directives prioritizing Hainan Free Trade Port corridors mean Hainan Airlines must align fleet and network plans with national targets. Policy shifts can rapidly reallocate capacity or favor strategic routes, directly affecting unit revenue and load factors. Supportive CAAC measures can unlock international growth; restrictive rulings compress margins and constrain expansion.

Bilateral air service agreements

Bilateral air service agreements determine Hainan Airlines' access to Europe, North America, Asia and Africa; China had ASAs with over 60 countries in 2024, shaping route opportunities. Negotiation outcomes set permitted frequencies, aircraft gauge and partner access, directly affecting capacity and yields. Favorable pacts enable premium long‑haul connectivity while stalled agreements cap growth; major domestic and foreign carriers actively lobby for the same scarce rights.

Geopolitical tensions and sanctions

US–China and EU–China frictions constrain aircraft procurement, overflight permissions and demand for Hainan Airlines, with IATA reporting global RPKs recovered to 94% of 2019 by July 2024, highlighting sensitivity to cross-border flow changes.

Sanctions and export controls have already disrupted parts and advanced-tech access, increasing supplier risk and delivery delays for airframes and avionics.

Stricter visa regimes and security reviews suppress passenger flow on key routes, while geopolitics drives yield and capacity volatility, complicating short-term network and fleet planning.

National strategies and Hainan FTP

Beijing’s 2020 Hainan Free Trade Port blueprint and the dual circulation strategy (since 2020) aim for an initial high‑level FTP by 2025 and deeper opening by 2035, which should expand tourism and logistics flows to the island.

Preferential tax, duty‑free expansion and visa facilitation lift inbound traffic, letting Hainan Airlines position Haikou and Sanya as international gateways; the pace of policy rollout will drive how much traffic and revenue materialize.

- Tags: policy-milestones-2025

- Tags: dual-circulation-2020

- Tags: gateways-Haikou-Sanya

- Tags: execution-risk

Belt and Road route priorities

Belt and Road route priorities, launched under the BRI in 2013, steer Hainan Airlines toward developing Central Asia, Middle East and Africa links; Hainan was designated a free trade port in 2020, which supports outbound aviation expansion. Political backing can ease bilateral approvals and marketing support, but initial traffic on these corridors is often developmental rather than immediately profitable, requiring patient network investment and active risk management for politically sensitive destinations.

- BRI origin year: 2013

- Hainan FTZ designation: 2020

- Focus regions: Central Asia, Middle East, Africa

- Strategy: patient investment + robust political risk controls

CAAC 2024 shifts networks; ASAs 60+, RPKs at 94% of 2019

CAAC 2024 directives force Hainan Airlines to align fleet and routes with Hainan FTP priorities; CAAC controls slots, pricing and safety. China had ASAs with 60+ countries in 2024, shaping international access. IATA RPKs reached 94% of 2019 by Jul 2024, showing sensitivity to geopolitics and sanctions.

| Metric | Value |

|---|---|

| CAAC 2024 policy | FTP priority |

| ASAs (2024) | 60+ |

| IATA RPKs (Jul 2024) | 94% of 2019 |

What is included in the product

Explores how macro-environmental factors uniquely affect Hainan Airlines across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it highlights threats, opportunities and forward-looking insights to inform strategy, scenario-planning and funding decisions.

A compact, PESTLE‑segmented summary of Hainan Airlines' external environment that can be dropped into presentations, edited for regional or business‑line context, and easily shared across teams to streamline risk discussions and strategic planning.

Economic factors

Fuel price and FX sensitivity

Jet fuel accounted for roughly 25% of Hainan Airlines operating costs, with Brent averaging about $82/bbl in 2024—swings materially lift CASK; USD-denominated expenses and aircraft leases (significant share of capex/leases ~10–15% of opex) expose earnings to RMB/USD ~7.2, hedging mitigates volatility but introduces basis and liquidity risk, while fuel-efficiency measures and fuel surcharges remain key levers.

China travel demand cycles

China's 2023 GDP grew 5.2% (official) and domestic air traffic reached about 543 million passengers in 2023 (CAAC), supporting higher seat factors and yields during strong demand periods. Leisure rebounds and Golden Week spikes create pronounced revenue peaks versus off‑peak softness. Business travel recovery is lifting premium cabin loadings. Macroeconomic slowdowns compress fares and ancillary spend, pressuring margins.

Fleet capex and interest rates

Fleet renewal requires large capex or lease commitments, typically $60–80m for a new narrowbody and $200–300m for a widebody. Higher global policy rates, around 5.25% mid‑2025, raise borrowing costs and lease rentals, squeezing cash flow. Staggered deliveries and sale–leasebacks smooth outflows, while utilization and residual values are the key drivers of ROIC.

Competitive intensity

Rivalry with Air China, China Eastern and China Southern—which together account for roughly 60% of domestic seat capacity—and rising LCC share (~10% in 2024) compresses yields for Hainan Airlines; slot scarcity at Beijing and Shanghai tier-1 airports caps growth and pricing power. Partnerships and codeshares boost connectivity and network economics, while service and on-time reliability remain key differentiators for premium pricing.

- Big-3 capacity share ~60% (2024)

- LCC share ~10% (2024)

- Tier-1 slot constraints limit expansion

- Codeshares improve network yields

- Service/reliability = pricing leverage

Cargo and e-commerce cycles

Post-pandemic cargo yields surged roughly 50% in 2020–22 and by 2024 had largely normalized to about 20–30% above 2019 levels (IATA), while China’s online retail of physical goods reached ~RMB 13.4 trillion in 2023, sustaining parcel volumes into 2024–25 but with mid-single-digit growth. Belly-capacity recovery increased available tonnage, pressuring yields and load factors; cold-chain and special cargo command 15–40% premiums, adding margin diversity for Hainan Airlines.

- Cargo yields: peak +~50% (2020–22), normalized to +20–30% vs 2019 (2024)

- China e-commerce: ~RMB 13.4 trillion online retail (2023), slower growth 2024–25

- Belly recovery: higher capacity → pricing pressure

- Cold-chain/special cargo: +15–40% margin premium

CAAC 2024 shifts networks; ASAs 60+, RPKs at 94% of 2019

Jet fuel ~25% of opex; Brent ~$82/bbl (2024) and RMB/USD ~7.2 expose earnings; hedging and efficiency critical. China demand: 543m domestic pax (2023), GDP +5.2% (2023); Big‑3 ~60% capacity, LCC ~10% (2024). Fleet capex narrowbody $60–80m, widebody $200–300m; policy rates ~5.25% mid‑2025 raise financing cost.

| Metric | Value |

|---|---|

| Jet fuel share | ~25% |

| Brent (2024) | $82/bbl |

| Domestic pax (2023) | 543m |

| Policy rate (mid‑2025) | ~5.25% |

What You See Is What You Get

Hainan Airlines PESTLE Analysis

The Hainan Airlines PESTLE Analysis preview shown here is the exact document you’ll receive after purchase — fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors specific to Hainan Airlines. No placeholders or teasers; this is the final, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our focused PESTLE Analysis of Hainan Airlines—three concise sections reveal how politics, economy, society, technology, law, and environment will shape its trajectory. Ideal for investors and strategists who need vetted, actionable intelligence fast. Purchase the full report to get the complete, downloadable breakdown and start making smarter decisions today.

Political factors

State oversight and CAAC policy

CAAC tightly guides route rights, slot allocation, pricing discipline and safety compliance, and its 2024 directives prioritizing Hainan Free Trade Port corridors mean Hainan Airlines must align fleet and network plans with national targets. Policy shifts can rapidly reallocate capacity or favor strategic routes, directly affecting unit revenue and load factors. Supportive CAAC measures can unlock international growth; restrictive rulings compress margins and constrain expansion.

Bilateral air service agreements

Bilateral air service agreements determine Hainan Airlines' access to Europe, North America, Asia and Africa; China had ASAs with over 60 countries in 2024, shaping route opportunities. Negotiation outcomes set permitted frequencies, aircraft gauge and partner access, directly affecting capacity and yields. Favorable pacts enable premium long‑haul connectivity while stalled agreements cap growth; major domestic and foreign carriers actively lobby for the same scarce rights.

Geopolitical tensions and sanctions

US–China and EU–China frictions constrain aircraft procurement, overflight permissions and demand for Hainan Airlines, with IATA reporting global RPKs recovered to 94% of 2019 by July 2024, highlighting sensitivity to cross-border flow changes.

Sanctions and export controls have already disrupted parts and advanced-tech access, increasing supplier risk and delivery delays for airframes and avionics.

Stricter visa regimes and security reviews suppress passenger flow on key routes, while geopolitics drives yield and capacity volatility, complicating short-term network and fleet planning.

National strategies and Hainan FTP

Beijing’s 2020 Hainan Free Trade Port blueprint and the dual circulation strategy (since 2020) aim for an initial high‑level FTP by 2025 and deeper opening by 2035, which should expand tourism and logistics flows to the island.

Preferential tax, duty‑free expansion and visa facilitation lift inbound traffic, letting Hainan Airlines position Haikou and Sanya as international gateways; the pace of policy rollout will drive how much traffic and revenue materialize.

- Tags: policy-milestones-2025

- Tags: dual-circulation-2020

- Tags: gateways-Haikou-Sanya

- Tags: execution-risk

Belt and Road route priorities

Belt and Road route priorities, launched under the BRI in 2013, steer Hainan Airlines toward developing Central Asia, Middle East and Africa links; Hainan was designated a free trade port in 2020, which supports outbound aviation expansion. Political backing can ease bilateral approvals and marketing support, but initial traffic on these corridors is often developmental rather than immediately profitable, requiring patient network investment and active risk management for politically sensitive destinations.

- BRI origin year: 2013

- Hainan FTZ designation: 2020

- Focus regions: Central Asia, Middle East, Africa

- Strategy: patient investment + robust political risk controls

CAAC 2024 shifts networks; ASAs 60+, RPKs at 94% of 2019

CAAC 2024 directives force Hainan Airlines to align fleet and routes with Hainan FTP priorities; CAAC controls slots, pricing and safety. China had ASAs with 60+ countries in 2024, shaping international access. IATA RPKs reached 94% of 2019 by Jul 2024, showing sensitivity to geopolitics and sanctions.

| Metric | Value |

|---|---|

| CAAC 2024 policy | FTP priority |

| ASAs (2024) | 60+ |

| IATA RPKs (Jul 2024) | 94% of 2019 |

What is included in the product

Explores how macro-environmental factors uniquely affect Hainan Airlines across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and region-specific regulatory context. Designed for executives and investors, it highlights threats, opportunities and forward-looking insights to inform strategy, scenario-planning and funding decisions.

A compact, PESTLE‑segmented summary of Hainan Airlines' external environment that can be dropped into presentations, edited for regional or business‑line context, and easily shared across teams to streamline risk discussions and strategic planning.

Economic factors

Fuel price and FX sensitivity

Jet fuel accounted for roughly 25% of Hainan Airlines operating costs, with Brent averaging about $82/bbl in 2024—swings materially lift CASK; USD-denominated expenses and aircraft leases (significant share of capex/leases ~10–15% of opex) expose earnings to RMB/USD ~7.2, hedging mitigates volatility but introduces basis and liquidity risk, while fuel-efficiency measures and fuel surcharges remain key levers.

China travel demand cycles

China's 2023 GDP grew 5.2% (official) and domestic air traffic reached about 543 million passengers in 2023 (CAAC), supporting higher seat factors and yields during strong demand periods. Leisure rebounds and Golden Week spikes create pronounced revenue peaks versus off‑peak softness. Business travel recovery is lifting premium cabin loadings. Macroeconomic slowdowns compress fares and ancillary spend, pressuring margins.

Fleet capex and interest rates

Fleet renewal requires large capex or lease commitments, typically $60–80m for a new narrowbody and $200–300m for a widebody. Higher global policy rates, around 5.25% mid‑2025, raise borrowing costs and lease rentals, squeezing cash flow. Staggered deliveries and sale–leasebacks smooth outflows, while utilization and residual values are the key drivers of ROIC.

Competitive intensity

Rivalry with Air China, China Eastern and China Southern—which together account for roughly 60% of domestic seat capacity—and rising LCC share (~10% in 2024) compresses yields for Hainan Airlines; slot scarcity at Beijing and Shanghai tier-1 airports caps growth and pricing power. Partnerships and codeshares boost connectivity and network economics, while service and on-time reliability remain key differentiators for premium pricing.

- Big-3 capacity share ~60% (2024)

- LCC share ~10% (2024)

- Tier-1 slot constraints limit expansion

- Codeshares improve network yields

- Service/reliability = pricing leverage

Cargo and e-commerce cycles

Post-pandemic cargo yields surged roughly 50% in 2020–22 and by 2024 had largely normalized to about 20–30% above 2019 levels (IATA), while China’s online retail of physical goods reached ~RMB 13.4 trillion in 2023, sustaining parcel volumes into 2024–25 but with mid-single-digit growth. Belly-capacity recovery increased available tonnage, pressuring yields and load factors; cold-chain and special cargo command 15–40% premiums, adding margin diversity for Hainan Airlines.

- Cargo yields: peak +~50% (2020–22), normalized to +20–30% vs 2019 (2024)

- China e-commerce: ~RMB 13.4 trillion online retail (2023), slower growth 2024–25

- Belly recovery: higher capacity → pricing pressure

- Cold-chain/special cargo: +15–40% margin premium

CAAC 2024 shifts networks; ASAs 60+, RPKs at 94% of 2019

Jet fuel ~25% of opex; Brent ~$82/bbl (2024) and RMB/USD ~7.2 expose earnings; hedging and efficiency critical. China demand: 543m domestic pax (2023), GDP +5.2% (2023); Big‑3 ~60% capacity, LCC ~10% (2024). Fleet capex narrowbody $60–80m, widebody $200–300m; policy rates ~5.25% mid‑2025 raise financing cost.

| Metric | Value |

|---|---|

| Jet fuel share | ~25% |

| Brent (2024) | $82/bbl |

| Domestic pax (2023) | 543m |

| Policy rate (mid‑2025) | ~5.25% |

What You See Is What You Get

Hainan Airlines PESTLE Analysis

The Hainan Airlines PESTLE Analysis preview shown here is the exact document you’ll receive after purchase — fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors specific to Hainan Airlines. No placeholders or teasers; this is the final, downloadable file.