Honle Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

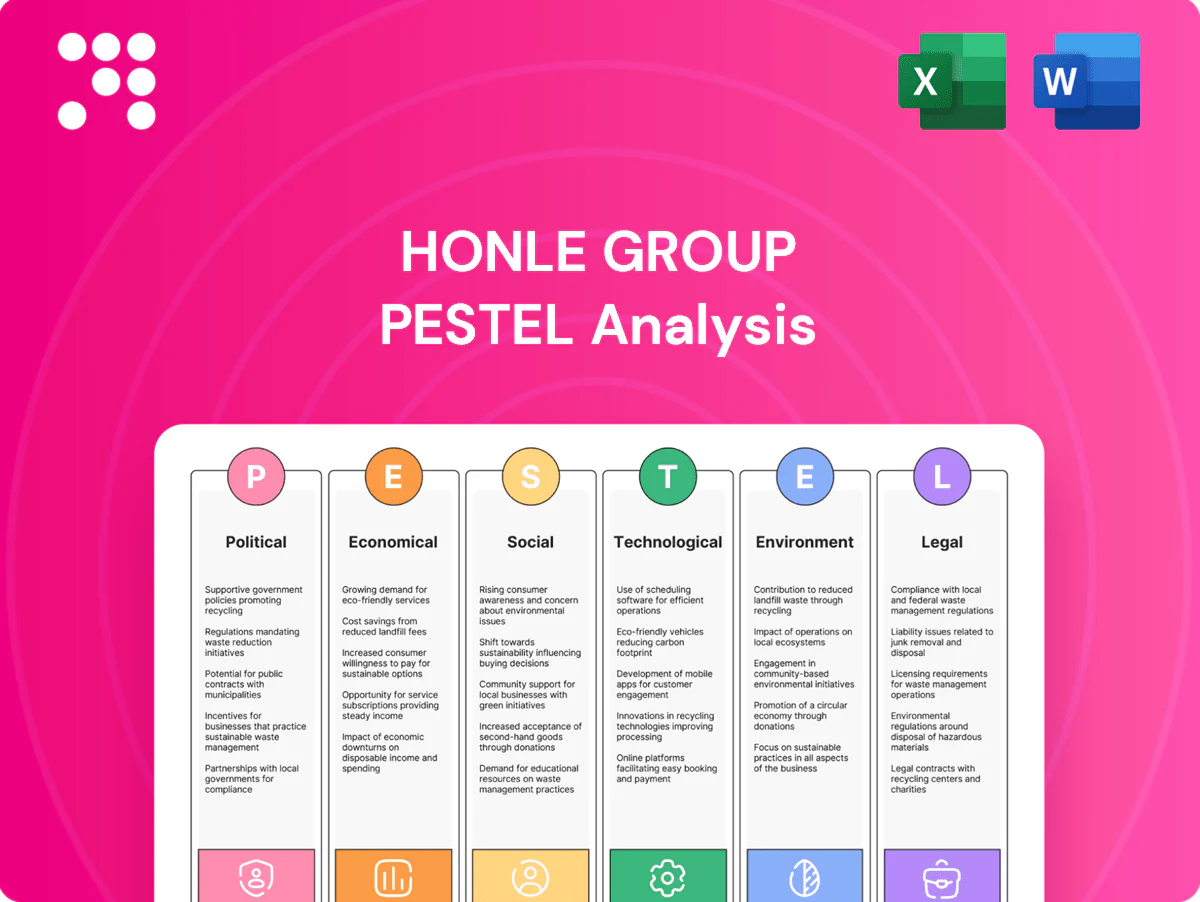

Gain a competitive edge with our concise PESTLE Analysis of Honle Group—three to five actionable insights on political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, this report saves research time and supports smarter decisions. Purchase the full analysis to unlock the complete, editable strategic dossier now.

Political factors

Trade policy volatility

Export-dependent UV equipment faces tariffs, customs delays and standards misalignment across regions, with US Section 301 measures imposing tariffs up to 25% on certain Chinese-sourced components that can materially raise landed costs. Shifts in EU, US and China trade stances—including tightening export controls or new tariffs—can compress margins and disrupt supply chains. Hönle may need multi-country assembly or local service hubs to avoid duties and speed customs clearance. Active monitoring of FTAs and localization incentives is critical to preserve price competitiveness.

Industrial subsidies

Government grants such as the US CHIPS and Science Act (roughly $52 billion) and the US Inflation Reduction Act (~$369 billion) plus EU programmes like Horizon Europe (€95.5 billion) are accelerating customer capex in advanced manufacturing, clean tech and medtech, expanding addressable markets. Geographic allocation of subsidies can advantage competing OEMs unevenly, altering price competition and margin pressure. Hönle can align product roadmaps to subsidy-eligible use cases and boost access via proactive tendering and consortium participation.

Public health priorities

Policies prioritizing infection control and hospital preparedness (EU health spending ~9.9% of GDP in 2023) elevate demand for UV disinfection; procurement cycles and budget rules (annual to multi-year cycles) shape timing and technical specs. Standard-setting by CDC, ECDC and national agencies accelerates adoption curves. Hönle can engage regulators, HTA bodies and hospital infection-control teams to validate efficacy and safety.

Geopolitical supply risk

Semiconductors, specialty glass and electronic components face acute geopolitical supply risk; the global semiconductor market exceeded $500 billion in 2024 and US/EU export controls since 2022 have targeted advanced chips and related inputs, constraining sales to China and Russia.

Sanctions and export controls can block specific inputs or customers; dual-sourcing and regional inventories reduce disruption, while compliance-led screening protects continuity and reputation.

- risk: export controls, sanctions

- fact: semiconductor market >$500B (2024)

- mitigation: dual-sourcing, regional stock

- governance: compliance screening

Energy and industry policy

- Policy: Fit for 55 — 55% GHG reduction target by 2030

- Energy saving: UV vs thermal — up to 70% lower energy

- Electricity cost: ~0.14 EUR/kWh EU-27 (2024)

- Financial: ROI frequently <24 months when policy incentives included

Tariffs, export controls and grants reshape semiconductor UV and energy-saving markets

Tariffs and export controls (US Section 301 up to 25%) raise landed costs and can disrupt supply chains; semiconductors market >$500B (2024) faces tight controls. Grants (CHIPS $52B, IRA $369B, Horizon €95.5B) expand addressable markets. Fit for 55 (55% GHG cut by 2030) and energy savings (UV up to 70%, ROI <24 months) favor Hönle products.

| Risk | Stat | Mitigation |

|---|---|---|

| Tariffs | 25% | Local assembly |

| Subsidy shifts | CHIPS $52B | Align roadmaps |

What is included in the product

Provides a concise PESTLE evaluation of how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect the Honle Group, with each section grounded in current data and industry trends. Designed for executives, investors and strategists to identify threats, opportunities and forward-looking scenarios for decision-making and planning.

A clean, summarized Honle Group PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Capex cyclicality

End-markets such as electronics, printing and automotive drive Honle UV-system orders and are cyclically sensitive: these sectors represent roughly 70% of UV-equipment demand, so downturns typically defer retrofit and upgrade projects by 6–12 months while upswings accelerate new-line bookings. A diversified sector mix smooths order volatility, and service plus consumables—about 25–35% of revenues for leading suppliers—stabilize cash flow in troughs.

FX and interest rates

EUR moves (around 1.08 USD in mid‑2025) shift Honle Group export competitiveness and input costs, with a stronger euro squeezing margins while a weaker euro raises local priced raw material bills. ECB rates near 3.75% lift customer hurdle rates and leasing costs, with corporate borrowing spreads up ~150–200 bps YoY. Active FX hedging, price‑indexed contracts and vendor financing are used to stabilize margins and enable projects in tight credit conditions.

Energy price dynamics

As electricity and gas prices shift, UV versus thermal curing economics swing materially: EU industrial electricity averaged about €0.15/kWh in 2024 while gas prices fell ~60% from 2022 peaks, improving thermal cases but still leaving LED UV attractive. LED UV can cut energy intensity 50–70% per vendor data, strengthening payback assumptions when power costs exceed €0.15/kWh. Regional subsidies or surcharges can change TCO by up to ~20%, so Hönle should model localized energy savings and tariffs in every bid.

Supply chain inflation

- component scarcity

- logistics volatility

- design-to-cost

- long-term agreements

- transparent surcharges

Customer consolidation

Customer consolidation in printing and automotive tiers heightens buyer power as OEMs and large print groups drive scale: global light‑vehicle production recovered to about 80 million units in 2024, concentrating orders to fewer buyers and pressuring pricing.

Standardized global platforms enable larger orders but compress margins, making strategic key‑account management pivotal while value‑added service bundles (installation, certification, lifecycle support) help defend margins.

- Buyer power up: fewer, larger customers

- Platform orders ↑, prices ↓

- Key‑account focus + service bundles = margin defense

Tariffs, export controls and grants reshape semiconductor UV and energy-saving markets

End‑market cyclicality (electronics/printing/auto ~70% demand) causes 6–12 month booking shifts; services/consumables (25–35% revenue) stabilize cash flow. EUR ~1.08 USD and ECB ~3.75% in mid‑2025 pressure margins and financing costs. Energy (EU €0.15/kWh 2024) and supply inflation drive TCO and procurement risks, mitigated by design‑to‑cost and long‑term contracts.

| Metric | Value |

|---|---|

| Auto prod. 2024 | ~80m units |

| EUR/USD mid‑2025 | ~1.08 |

| ECB rate | ~3.75% |

What You See Is What You Get

Honle Group PESTLE Analysis

The preview shown here is the exact Honle Group PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment with clear conclusions and strategic implications. No placeholders or abridgements; the file you download after checkout is identical to this preview.

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our concise PESTLE Analysis of Honle Group—three to five actionable insights on political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, this report saves research time and supports smarter decisions. Purchase the full analysis to unlock the complete, editable strategic dossier now.

Political factors

Trade policy volatility

Export-dependent UV equipment faces tariffs, customs delays and standards misalignment across regions, with US Section 301 measures imposing tariffs up to 25% on certain Chinese-sourced components that can materially raise landed costs. Shifts in EU, US and China trade stances—including tightening export controls or new tariffs—can compress margins and disrupt supply chains. Hönle may need multi-country assembly or local service hubs to avoid duties and speed customs clearance. Active monitoring of FTAs and localization incentives is critical to preserve price competitiveness.

Industrial subsidies

Government grants such as the US CHIPS and Science Act (roughly $52 billion) and the US Inflation Reduction Act (~$369 billion) plus EU programmes like Horizon Europe (€95.5 billion) are accelerating customer capex in advanced manufacturing, clean tech and medtech, expanding addressable markets. Geographic allocation of subsidies can advantage competing OEMs unevenly, altering price competition and margin pressure. Hönle can align product roadmaps to subsidy-eligible use cases and boost access via proactive tendering and consortium participation.

Public health priorities

Policies prioritizing infection control and hospital preparedness (EU health spending ~9.9% of GDP in 2023) elevate demand for UV disinfection; procurement cycles and budget rules (annual to multi-year cycles) shape timing and technical specs. Standard-setting by CDC, ECDC and national agencies accelerates adoption curves. Hönle can engage regulators, HTA bodies and hospital infection-control teams to validate efficacy and safety.

Geopolitical supply risk

Semiconductors, specialty glass and electronic components face acute geopolitical supply risk; the global semiconductor market exceeded $500 billion in 2024 and US/EU export controls since 2022 have targeted advanced chips and related inputs, constraining sales to China and Russia.

Sanctions and export controls can block specific inputs or customers; dual-sourcing and regional inventories reduce disruption, while compliance-led screening protects continuity and reputation.

- risk: export controls, sanctions

- fact: semiconductor market >$500B (2024)

- mitigation: dual-sourcing, regional stock

- governance: compliance screening

Energy and industry policy

- Policy: Fit for 55 — 55% GHG reduction target by 2030

- Energy saving: UV vs thermal — up to 70% lower energy

- Electricity cost: ~0.14 EUR/kWh EU-27 (2024)

- Financial: ROI frequently <24 months when policy incentives included

Tariffs, export controls and grants reshape semiconductor UV and energy-saving markets

Tariffs and export controls (US Section 301 up to 25%) raise landed costs and can disrupt supply chains; semiconductors market >$500B (2024) faces tight controls. Grants (CHIPS $52B, IRA $369B, Horizon €95.5B) expand addressable markets. Fit for 55 (55% GHG cut by 2030) and energy savings (UV up to 70%, ROI <24 months) favor Hönle products.

| Risk | Stat | Mitigation |

|---|---|---|

| Tariffs | 25% | Local assembly |

| Subsidy shifts | CHIPS $52B | Align roadmaps |

What is included in the product

Provides a concise PESTLE evaluation of how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect the Honle Group, with each section grounded in current data and industry trends. Designed for executives, investors and strategists to identify threats, opportunities and forward-looking scenarios for decision-making and planning.

A clean, summarized Honle Group PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Capex cyclicality

End-markets such as electronics, printing and automotive drive Honle UV-system orders and are cyclically sensitive: these sectors represent roughly 70% of UV-equipment demand, so downturns typically defer retrofit and upgrade projects by 6–12 months while upswings accelerate new-line bookings. A diversified sector mix smooths order volatility, and service plus consumables—about 25–35% of revenues for leading suppliers—stabilize cash flow in troughs.

FX and interest rates

EUR moves (around 1.08 USD in mid‑2025) shift Honle Group export competitiveness and input costs, with a stronger euro squeezing margins while a weaker euro raises local priced raw material bills. ECB rates near 3.75% lift customer hurdle rates and leasing costs, with corporate borrowing spreads up ~150–200 bps YoY. Active FX hedging, price‑indexed contracts and vendor financing are used to stabilize margins and enable projects in tight credit conditions.

Energy price dynamics

As electricity and gas prices shift, UV versus thermal curing economics swing materially: EU industrial electricity averaged about €0.15/kWh in 2024 while gas prices fell ~60% from 2022 peaks, improving thermal cases but still leaving LED UV attractive. LED UV can cut energy intensity 50–70% per vendor data, strengthening payback assumptions when power costs exceed €0.15/kWh. Regional subsidies or surcharges can change TCO by up to ~20%, so Hönle should model localized energy savings and tariffs in every bid.

Supply chain inflation

- component scarcity

- logistics volatility

- design-to-cost

- long-term agreements

- transparent surcharges

Customer consolidation

Customer consolidation in printing and automotive tiers heightens buyer power as OEMs and large print groups drive scale: global light‑vehicle production recovered to about 80 million units in 2024, concentrating orders to fewer buyers and pressuring pricing.

Standardized global platforms enable larger orders but compress margins, making strategic key‑account management pivotal while value‑added service bundles (installation, certification, lifecycle support) help defend margins.

- Buyer power up: fewer, larger customers

- Platform orders ↑, prices ↓

- Key‑account focus + service bundles = margin defense

Tariffs, export controls and grants reshape semiconductor UV and energy-saving markets

End‑market cyclicality (electronics/printing/auto ~70% demand) causes 6–12 month booking shifts; services/consumables (25–35% revenue) stabilize cash flow. EUR ~1.08 USD and ECB ~3.75% in mid‑2025 pressure margins and financing costs. Energy (EU €0.15/kWh 2024) and supply inflation drive TCO and procurement risks, mitigated by design‑to‑cost and long‑term contracts.

| Metric | Value |

|---|---|

| Auto prod. 2024 | ~80m units |

| EUR/USD mid‑2025 | ~1.08 |

| ECB rate | ~3.75% |

What You See Is What You Get

Honle Group PESTLE Analysis

The preview shown here is the exact Honle Group PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment with clear conclusions and strategic implications. No placeholders or abridgements; the file you download after checkout is identical to this preview.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our concise PESTLE Analysis of Honle Group—three to five actionable insights on political, economic, social, technological, legal and environmental forces shaping its future. Ideal for investors and strategists, this report saves research time and supports smarter decisions. Purchase the full analysis to unlock the complete, editable strategic dossier now.

Political factors

Trade policy volatility

Export-dependent UV equipment faces tariffs, customs delays and standards misalignment across regions, with US Section 301 measures imposing tariffs up to 25% on certain Chinese-sourced components that can materially raise landed costs. Shifts in EU, US and China trade stances—including tightening export controls or new tariffs—can compress margins and disrupt supply chains. Hönle may need multi-country assembly or local service hubs to avoid duties and speed customs clearance. Active monitoring of FTAs and localization incentives is critical to preserve price competitiveness.

Industrial subsidies

Government grants such as the US CHIPS and Science Act (roughly $52 billion) and the US Inflation Reduction Act (~$369 billion) plus EU programmes like Horizon Europe (€95.5 billion) are accelerating customer capex in advanced manufacturing, clean tech and medtech, expanding addressable markets. Geographic allocation of subsidies can advantage competing OEMs unevenly, altering price competition and margin pressure. Hönle can align product roadmaps to subsidy-eligible use cases and boost access via proactive tendering and consortium participation.

Public health priorities

Policies prioritizing infection control and hospital preparedness (EU health spending ~9.9% of GDP in 2023) elevate demand for UV disinfection; procurement cycles and budget rules (annual to multi-year cycles) shape timing and technical specs. Standard-setting by CDC, ECDC and national agencies accelerates adoption curves. Hönle can engage regulators, HTA bodies and hospital infection-control teams to validate efficacy and safety.

Geopolitical supply risk

Semiconductors, specialty glass and electronic components face acute geopolitical supply risk; the global semiconductor market exceeded $500 billion in 2024 and US/EU export controls since 2022 have targeted advanced chips and related inputs, constraining sales to China and Russia.

Sanctions and export controls can block specific inputs or customers; dual-sourcing and regional inventories reduce disruption, while compliance-led screening protects continuity and reputation.

- risk: export controls, sanctions

- fact: semiconductor market >$500B (2024)

- mitigation: dual-sourcing, regional stock

- governance: compliance screening

Energy and industry policy

- Policy: Fit for 55 — 55% GHG reduction target by 2030

- Energy saving: UV vs thermal — up to 70% lower energy

- Electricity cost: ~0.14 EUR/kWh EU-27 (2024)

- Financial: ROI frequently <24 months when policy incentives included

Tariffs, export controls and grants reshape semiconductor UV and energy-saving markets

Tariffs and export controls (US Section 301 up to 25%) raise landed costs and can disrupt supply chains; semiconductors market >$500B (2024) faces tight controls. Grants (CHIPS $52B, IRA $369B, Horizon €95.5B) expand addressable markets. Fit for 55 (55% GHG cut by 2030) and energy savings (UV up to 70%, ROI <24 months) favor Hönle products.

| Risk | Stat | Mitigation |

|---|---|---|

| Tariffs | 25% | Local assembly |

| Subsidy shifts | CHIPS $52B | Align roadmaps |

What is included in the product

Provides a concise PESTLE evaluation of how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect the Honle Group, with each section grounded in current data and industry trends. Designed for executives, investors and strategists to identify threats, opportunities and forward-looking scenarios for decision-making and planning.

A clean, summarized Honle Group PESTLE that’s visually segmented by category for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Capex cyclicality

End-markets such as electronics, printing and automotive drive Honle UV-system orders and are cyclically sensitive: these sectors represent roughly 70% of UV-equipment demand, so downturns typically defer retrofit and upgrade projects by 6–12 months while upswings accelerate new-line bookings. A diversified sector mix smooths order volatility, and service plus consumables—about 25–35% of revenues for leading suppliers—stabilize cash flow in troughs.

FX and interest rates

EUR moves (around 1.08 USD in mid‑2025) shift Honle Group export competitiveness and input costs, with a stronger euro squeezing margins while a weaker euro raises local priced raw material bills. ECB rates near 3.75% lift customer hurdle rates and leasing costs, with corporate borrowing spreads up ~150–200 bps YoY. Active FX hedging, price‑indexed contracts and vendor financing are used to stabilize margins and enable projects in tight credit conditions.

Energy price dynamics

As electricity and gas prices shift, UV versus thermal curing economics swing materially: EU industrial electricity averaged about €0.15/kWh in 2024 while gas prices fell ~60% from 2022 peaks, improving thermal cases but still leaving LED UV attractive. LED UV can cut energy intensity 50–70% per vendor data, strengthening payback assumptions when power costs exceed €0.15/kWh. Regional subsidies or surcharges can change TCO by up to ~20%, so Hönle should model localized energy savings and tariffs in every bid.

Supply chain inflation

- component scarcity

- logistics volatility

- design-to-cost

- long-term agreements

- transparent surcharges

Customer consolidation

Customer consolidation in printing and automotive tiers heightens buyer power as OEMs and large print groups drive scale: global light‑vehicle production recovered to about 80 million units in 2024, concentrating orders to fewer buyers and pressuring pricing.

Standardized global platforms enable larger orders but compress margins, making strategic key‑account management pivotal while value‑added service bundles (installation, certification, lifecycle support) help defend margins.

- Buyer power up: fewer, larger customers

- Platform orders ↑, prices ↓

- Key‑account focus + service bundles = margin defense

Tariffs, export controls and grants reshape semiconductor UV and energy-saving markets

End‑market cyclicality (electronics/printing/auto ~70% demand) causes 6–12 month booking shifts; services/consumables (25–35% revenue) stabilize cash flow. EUR ~1.08 USD and ECB ~3.75% in mid‑2025 pressure margins and financing costs. Energy (EU €0.15/kWh 2024) and supply inflation drive TCO and procurement risks, mitigated by design‑to‑cost and long‑term contracts.

| Metric | Value |

|---|---|

| Auto prod. 2024 | ~80m units |

| EUR/USD mid‑2025 | ~1.08 |

| ECB rate | ~3.75% |

What You See Is What You Get

Honle Group PESTLE Analysis

The preview shown here is the exact Honle Group PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment with clear conclusions and strategic implications. No placeholders or abridgements; the file you download after checkout is identical to this preview.