Hogan Lovells Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

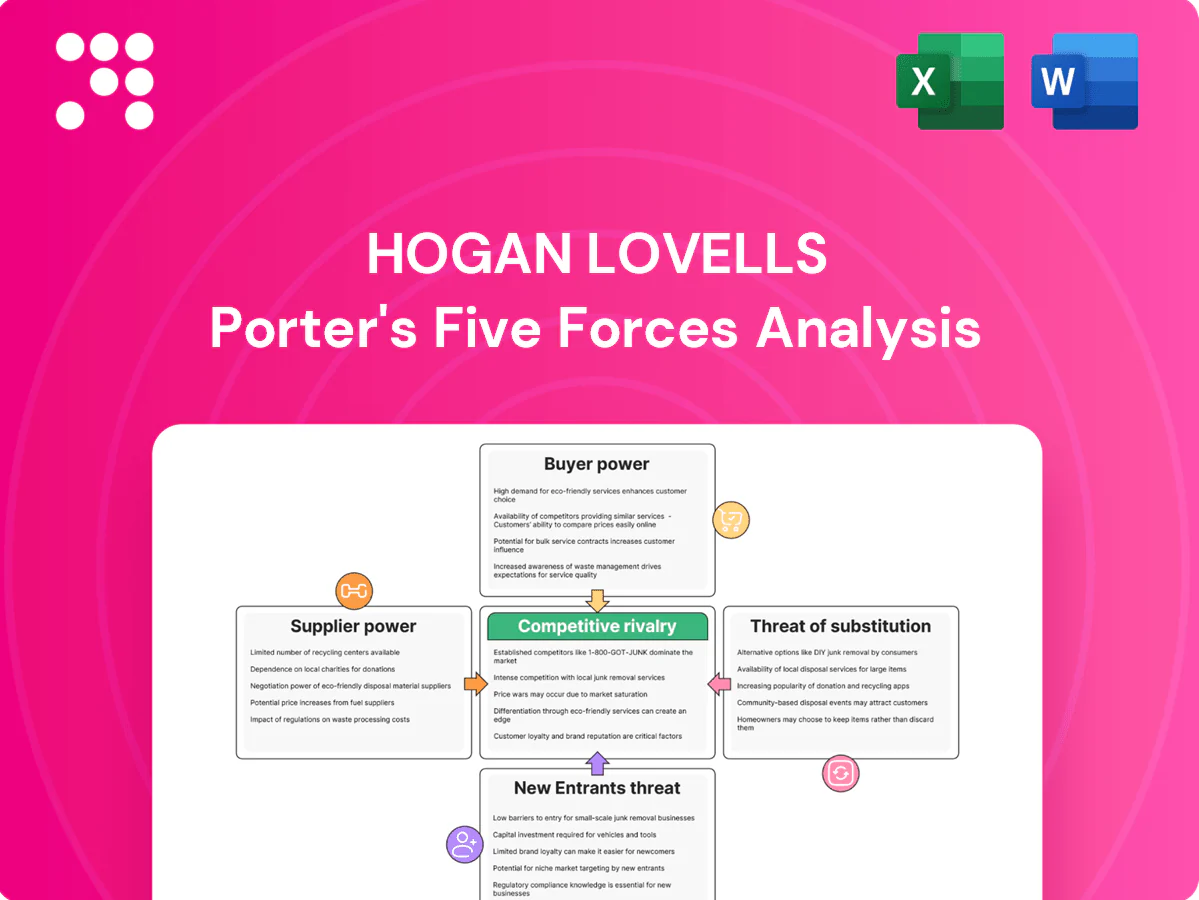

Hogan Lovells faces varied competitive pressures—from client bargaining power and regulatory shifts to niche substitute legal services—impacting margins and growth prospects; this snapshot highlights key tensions but stops short of force-by-force depth. Unlock the full Porter's Five Forces Analysis to get consultant-grade ratings, visuals, and actionable strategy recommendations tailored to Hogan Lovells.

Suppliers Bargaining Power

Elite legal talent scarcity

Top-tier partners and associates are the primary suppliers and their scarcity in 2024 significantly elevates bargaining power; double-digit lateral pay increases reported across major markets have driven compensation and flexible-work demands that squeeze margins. Hogan Lovells must boost investment in training, DEI, and clear career paths to retain talent, while intensified lateral markets increase bidding for specialized skills and raise acquisition costs.

Must-have research and tech

Dependence on Thomson Reuters Westlaw and RELX LexisNexis, which together hold roughly 70–80% of the legal research market (2024), plus eDiscovery and AI platforms, gives suppliers strong leverage. Pricing is commonly bundled into long-term, escalatory contracts. Switching costs are high because of workflow integration and large-scale data migration. Volume discounts and multi-sourcing can partially offset supplier power.

Premium real estate and facilities

Prestige locations in global capitals command rents often 2–3x suburban rates and offer few alternatives, giving landlords in prime districts strong negotiation clout despite hybrid work moderating demand. Office occupancy averaged about 60% of pre-pandemic levels in 2024, reducing but not eliminating landlord leverage. Long leases and substantial fit-out costs heighten switching frictions. Consolidation and hub-and-spoke strategies can rebalance terms.

Specialist vendors and experts

Specialist vendors—court reporters, translators, expert witnesses and niche consultancies—command premiums, with market rates rising c.10% in 2024 as demand from cross-border disputes increased; language and regulatory expertise sharply limit substitutes. Framework agreements and panels lower unit costs but do not guarantee availability for urgent matters, and tight litigation timelines amplify supplier leverage and expedite premium billing.

- Court reporting: premium for urgent/cross-border work

- Translation: scarce language/regulatory combos

- Expert witnesses: niche fees up c.10% in 2024

- Frameworks: cost control, not availability

Referral and alliance networks

Referral and alliance networks let Hogan Lovells plug local counsel into cross-border matters, leveraging its ~2,600 lawyers and 45+ offices in 2024 to underpin multi-jurisdictional delivery; in niche or sanctioned markets, supplier options narrow and dependence rises. Reciprocity and volume drive rate negotiation but strict quality and conflict checks limit substitution, while transparent SLA and conflict management reduce concentration risk.

- Local footprint: 45+ offices (2024)

- Dependence rises in sanctioned/niche markets

- Reciprocity/volume improve rates; quality caps choice

- Transparent SLA/conflict processes lower supplier concentration

Senior lawyer pay 10–20% hikes, research duopoly ~75%, rents 2–3x

Hogan Lovells faces high supplier power from scarce senior lawyers (lateral pay hikes 10–20% in 2024), dominant legal-research vendors (Westlaw/Lexis ~75% market share), premium landlord rents (prime vs suburban 2–3x) and specialist vendors with fees up ~10% in 2024.

| Supplier | 2024 metric |

|---|---|

| Senior lawyers | 10–20% pay rise |

| Legal research | ~75% market share |

| Landlords | 2–3x rent gap |

| Specialists | ~10% fee rise |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Hogan Lovells, uncovering competitive intensity, client and supplier bargaining power, entry barriers, substitute threats, and strategic implications to inform positioning, pricing, and growth decisions.

A concise, one-sheet Hogan Lovells Porter's Five Forces snapshot—tailored to legal and regulatory dynamics and customizable for evolving case law or policy, ideal for rapid strategic decision-making.

Customers Bargaining Power

Consolidated corporate panels

Large corporates and banks consolidate legal spend via panels and RFPs, negotiating AFAs, rate freezes and volume discounts; in 2024 AFAs account for roughly 30% of matters for many firms. Performance scorecards and KPIs increase accountability and drive mid-single-digit fee pressure. Hogan Lovells must demonstrate measurable value and outcomes to retain mandates and avoid displacement.

Moderate switching costs

Switching Hogan Lovells entails onboarding, knowledge transfer and relationship loss, and for complex matters—often spanning 12+ months—these frictions raise effective costs and temper buyer power. For commoditized tasks clients can switch readily, pushing price pressure. Hogan Lovells reported roughly $2.07bn revenue in 2023, and clear playbooks and data rooms create continuity advantages that help lock in clients.

Global, cross-practice needs

Multijurisdictional and regulatory breadth — supported by 49 offices across 22 countries — narrows client alternatives by bundling local regulatory expertise. Buyers still push blended rates across geographies, keeping rate pressure on global firms. Demonstrable coordination and documented local expertise reduce substitution risk. Consistent global quality and integrated teams are essential to resist sustained rate compression.

Outcome and risk sensitivity

High-stakes matters push clients to pay premium for Hogan Lovells' track record rather than lowest price, yet 2024 saw 45% of corporate legal teams pressing for fee predictability and AFAs; data-backed matter scoping and staffing models strengthen price defensibility, and structured post-matter reviews materially redirect future budget allocations.

- Track record over price

- 45% demand AFAs (2024)

- Data-backed scoping = defensibility

- Post-matter reviews drive reallocation

In-house counsel sophistication

In-house counsel sophistication raises buyer leverage as legal ops and procurement use analytics to benchmark spend and outcomes; the ALSP market was about USD 8 billion in 2023, amplifying alternatives to firms. Work is being unbundled: strategic matters remain external while routine work shifts in-house or to ALSPs, making clear value articulation and process efficiency essential. Co-sourcing models align incentives and increase client stickiness.

- Legal ops adoption: benchmarking + analytics

- ALSP market: ~USD 8 billion (2023)

- Co-sourcing: drives alignment and retention

Panel consolidation drives AFA adoption, fee pressure; scale and global reach defend premiums

Clients consolidate spend via panels/RFPs, pushing AFAs and mid-single-digit fee pressure; 30–45% of matters demand AFAs (2024). Switching costs for complex work limit buyer power, but commoditized tasks and ALSPs (~USD 8bn market, 2023) amplify price pressure. Global footprint and track record ($2.07bn rev, 2023) defend premiums.

| Metric | Value |

|---|---|

| Revenue (2023) | $2.07bn |

| AFAs (matters, 2024) | 30–45% |

| ALSP market (2023) | $8bn |

| Offices | 49 (22 countries) |

Same Document Delivered

Hogan Lovells Porter's Five Forces Analysis

This preview shows the exact Hogan Lovells Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the final deliverable, available instantly upon payment.

A Must-Have Tool for Decision-Makers

Hogan Lovells faces varied competitive pressures—from client bargaining power and regulatory shifts to niche substitute legal services—impacting margins and growth prospects; this snapshot highlights key tensions but stops short of force-by-force depth. Unlock the full Porter's Five Forces Analysis to get consultant-grade ratings, visuals, and actionable strategy recommendations tailored to Hogan Lovells.

Suppliers Bargaining Power

Elite legal talent scarcity

Top-tier partners and associates are the primary suppliers and their scarcity in 2024 significantly elevates bargaining power; double-digit lateral pay increases reported across major markets have driven compensation and flexible-work demands that squeeze margins. Hogan Lovells must boost investment in training, DEI, and clear career paths to retain talent, while intensified lateral markets increase bidding for specialized skills and raise acquisition costs.

Must-have research and tech

Dependence on Thomson Reuters Westlaw and RELX LexisNexis, which together hold roughly 70–80% of the legal research market (2024), plus eDiscovery and AI platforms, gives suppliers strong leverage. Pricing is commonly bundled into long-term, escalatory contracts. Switching costs are high because of workflow integration and large-scale data migration. Volume discounts and multi-sourcing can partially offset supplier power.

Premium real estate and facilities

Prestige locations in global capitals command rents often 2–3x suburban rates and offer few alternatives, giving landlords in prime districts strong negotiation clout despite hybrid work moderating demand. Office occupancy averaged about 60% of pre-pandemic levels in 2024, reducing but not eliminating landlord leverage. Long leases and substantial fit-out costs heighten switching frictions. Consolidation and hub-and-spoke strategies can rebalance terms.

Specialist vendors and experts

Specialist vendors—court reporters, translators, expert witnesses and niche consultancies—command premiums, with market rates rising c.10% in 2024 as demand from cross-border disputes increased; language and regulatory expertise sharply limit substitutes. Framework agreements and panels lower unit costs but do not guarantee availability for urgent matters, and tight litigation timelines amplify supplier leverage and expedite premium billing.

- Court reporting: premium for urgent/cross-border work

- Translation: scarce language/regulatory combos

- Expert witnesses: niche fees up c.10% in 2024

- Frameworks: cost control, not availability

Referral and alliance networks

Referral and alliance networks let Hogan Lovells plug local counsel into cross-border matters, leveraging its ~2,600 lawyers and 45+ offices in 2024 to underpin multi-jurisdictional delivery; in niche or sanctioned markets, supplier options narrow and dependence rises. Reciprocity and volume drive rate negotiation but strict quality and conflict checks limit substitution, while transparent SLA and conflict management reduce concentration risk.

- Local footprint: 45+ offices (2024)

- Dependence rises in sanctioned/niche markets

- Reciprocity/volume improve rates; quality caps choice

- Transparent SLA/conflict processes lower supplier concentration

Senior lawyer pay 10–20% hikes, research duopoly ~75%, rents 2–3x

Hogan Lovells faces high supplier power from scarce senior lawyers (lateral pay hikes 10–20% in 2024), dominant legal-research vendors (Westlaw/Lexis ~75% market share), premium landlord rents (prime vs suburban 2–3x) and specialist vendors with fees up ~10% in 2024.

| Supplier | 2024 metric |

|---|---|

| Senior lawyers | 10–20% pay rise |

| Legal research | ~75% market share |

| Landlords | 2–3x rent gap |

| Specialists | ~10% fee rise |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Hogan Lovells, uncovering competitive intensity, client and supplier bargaining power, entry barriers, substitute threats, and strategic implications to inform positioning, pricing, and growth decisions.

A concise, one-sheet Hogan Lovells Porter's Five Forces snapshot—tailored to legal and regulatory dynamics and customizable for evolving case law or policy, ideal for rapid strategic decision-making.

Customers Bargaining Power

Consolidated corporate panels

Large corporates and banks consolidate legal spend via panels and RFPs, negotiating AFAs, rate freezes and volume discounts; in 2024 AFAs account for roughly 30% of matters for many firms. Performance scorecards and KPIs increase accountability and drive mid-single-digit fee pressure. Hogan Lovells must demonstrate measurable value and outcomes to retain mandates and avoid displacement.

Moderate switching costs

Switching Hogan Lovells entails onboarding, knowledge transfer and relationship loss, and for complex matters—often spanning 12+ months—these frictions raise effective costs and temper buyer power. For commoditized tasks clients can switch readily, pushing price pressure. Hogan Lovells reported roughly $2.07bn revenue in 2023, and clear playbooks and data rooms create continuity advantages that help lock in clients.

Global, cross-practice needs

Multijurisdictional and regulatory breadth — supported by 49 offices across 22 countries — narrows client alternatives by bundling local regulatory expertise. Buyers still push blended rates across geographies, keeping rate pressure on global firms. Demonstrable coordination and documented local expertise reduce substitution risk. Consistent global quality and integrated teams are essential to resist sustained rate compression.

Outcome and risk sensitivity

High-stakes matters push clients to pay premium for Hogan Lovells' track record rather than lowest price, yet 2024 saw 45% of corporate legal teams pressing for fee predictability and AFAs; data-backed matter scoping and staffing models strengthen price defensibility, and structured post-matter reviews materially redirect future budget allocations.

- Track record over price

- 45% demand AFAs (2024)

- Data-backed scoping = defensibility

- Post-matter reviews drive reallocation

In-house counsel sophistication

In-house counsel sophistication raises buyer leverage as legal ops and procurement use analytics to benchmark spend and outcomes; the ALSP market was about USD 8 billion in 2023, amplifying alternatives to firms. Work is being unbundled: strategic matters remain external while routine work shifts in-house or to ALSPs, making clear value articulation and process efficiency essential. Co-sourcing models align incentives and increase client stickiness.

- Legal ops adoption: benchmarking + analytics

- ALSP market: ~USD 8 billion (2023)

- Co-sourcing: drives alignment and retention

Panel consolidation drives AFA adoption, fee pressure; scale and global reach defend premiums

Clients consolidate spend via panels/RFPs, pushing AFAs and mid-single-digit fee pressure; 30–45% of matters demand AFAs (2024). Switching costs for complex work limit buyer power, but commoditized tasks and ALSPs (~USD 8bn market, 2023) amplify price pressure. Global footprint and track record ($2.07bn rev, 2023) defend premiums.

| Metric | Value |

|---|---|

| Revenue (2023) | $2.07bn |

| AFAs (matters, 2024) | 30–45% |

| ALSP market (2023) | $8bn |

| Offices | 49 (22 countries) |

Same Document Delivered

Hogan Lovells Porter's Five Forces Analysis

This preview shows the exact Hogan Lovells Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the final deliverable, available instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Hogan Lovells faces varied competitive pressures—from client bargaining power and regulatory shifts to niche substitute legal services—impacting margins and growth prospects; this snapshot highlights key tensions but stops short of force-by-force depth. Unlock the full Porter's Five Forces Analysis to get consultant-grade ratings, visuals, and actionable strategy recommendations tailored to Hogan Lovells.

Suppliers Bargaining Power

Elite legal talent scarcity

Top-tier partners and associates are the primary suppliers and their scarcity in 2024 significantly elevates bargaining power; double-digit lateral pay increases reported across major markets have driven compensation and flexible-work demands that squeeze margins. Hogan Lovells must boost investment in training, DEI, and clear career paths to retain talent, while intensified lateral markets increase bidding for specialized skills and raise acquisition costs.

Must-have research and tech

Dependence on Thomson Reuters Westlaw and RELX LexisNexis, which together hold roughly 70–80% of the legal research market (2024), plus eDiscovery and AI platforms, gives suppliers strong leverage. Pricing is commonly bundled into long-term, escalatory contracts. Switching costs are high because of workflow integration and large-scale data migration. Volume discounts and multi-sourcing can partially offset supplier power.

Premium real estate and facilities

Prestige locations in global capitals command rents often 2–3x suburban rates and offer few alternatives, giving landlords in prime districts strong negotiation clout despite hybrid work moderating demand. Office occupancy averaged about 60% of pre-pandemic levels in 2024, reducing but not eliminating landlord leverage. Long leases and substantial fit-out costs heighten switching frictions. Consolidation and hub-and-spoke strategies can rebalance terms.

Specialist vendors and experts

Specialist vendors—court reporters, translators, expert witnesses and niche consultancies—command premiums, with market rates rising c.10% in 2024 as demand from cross-border disputes increased; language and regulatory expertise sharply limit substitutes. Framework agreements and panels lower unit costs but do not guarantee availability for urgent matters, and tight litigation timelines amplify supplier leverage and expedite premium billing.

- Court reporting: premium for urgent/cross-border work

- Translation: scarce language/regulatory combos

- Expert witnesses: niche fees up c.10% in 2024

- Frameworks: cost control, not availability

Referral and alliance networks

Referral and alliance networks let Hogan Lovells plug local counsel into cross-border matters, leveraging its ~2,600 lawyers and 45+ offices in 2024 to underpin multi-jurisdictional delivery; in niche or sanctioned markets, supplier options narrow and dependence rises. Reciprocity and volume drive rate negotiation but strict quality and conflict checks limit substitution, while transparent SLA and conflict management reduce concentration risk.

- Local footprint: 45+ offices (2024)

- Dependence rises in sanctioned/niche markets

- Reciprocity/volume improve rates; quality caps choice

- Transparent SLA/conflict processes lower supplier concentration

Senior lawyer pay 10–20% hikes, research duopoly ~75%, rents 2–3x

Hogan Lovells faces high supplier power from scarce senior lawyers (lateral pay hikes 10–20% in 2024), dominant legal-research vendors (Westlaw/Lexis ~75% market share), premium landlord rents (prime vs suburban 2–3x) and specialist vendors with fees up ~10% in 2024.

| Supplier | 2024 metric |

|---|---|

| Senior lawyers | 10–20% pay rise |

| Legal research | ~75% market share |

| Landlords | 2–3x rent gap |

| Specialists | ~10% fee rise |

What is included in the product

Comprehensive Porter’s Five Forces analysis tailored to Hogan Lovells, uncovering competitive intensity, client and supplier bargaining power, entry barriers, substitute threats, and strategic implications to inform positioning, pricing, and growth decisions.

A concise, one-sheet Hogan Lovells Porter's Five Forces snapshot—tailored to legal and regulatory dynamics and customizable for evolving case law or policy, ideal for rapid strategic decision-making.

Customers Bargaining Power

Consolidated corporate panels

Large corporates and banks consolidate legal spend via panels and RFPs, negotiating AFAs, rate freezes and volume discounts; in 2024 AFAs account for roughly 30% of matters for many firms. Performance scorecards and KPIs increase accountability and drive mid-single-digit fee pressure. Hogan Lovells must demonstrate measurable value and outcomes to retain mandates and avoid displacement.

Moderate switching costs

Switching Hogan Lovells entails onboarding, knowledge transfer and relationship loss, and for complex matters—often spanning 12+ months—these frictions raise effective costs and temper buyer power. For commoditized tasks clients can switch readily, pushing price pressure. Hogan Lovells reported roughly $2.07bn revenue in 2023, and clear playbooks and data rooms create continuity advantages that help lock in clients.

Global, cross-practice needs

Multijurisdictional and regulatory breadth — supported by 49 offices across 22 countries — narrows client alternatives by bundling local regulatory expertise. Buyers still push blended rates across geographies, keeping rate pressure on global firms. Demonstrable coordination and documented local expertise reduce substitution risk. Consistent global quality and integrated teams are essential to resist sustained rate compression.

Outcome and risk sensitivity

High-stakes matters push clients to pay premium for Hogan Lovells' track record rather than lowest price, yet 2024 saw 45% of corporate legal teams pressing for fee predictability and AFAs; data-backed matter scoping and staffing models strengthen price defensibility, and structured post-matter reviews materially redirect future budget allocations.

- Track record over price

- 45% demand AFAs (2024)

- Data-backed scoping = defensibility

- Post-matter reviews drive reallocation

In-house counsel sophistication

In-house counsel sophistication raises buyer leverage as legal ops and procurement use analytics to benchmark spend and outcomes; the ALSP market was about USD 8 billion in 2023, amplifying alternatives to firms. Work is being unbundled: strategic matters remain external while routine work shifts in-house or to ALSPs, making clear value articulation and process efficiency essential. Co-sourcing models align incentives and increase client stickiness.

- Legal ops adoption: benchmarking + analytics

- ALSP market: ~USD 8 billion (2023)

- Co-sourcing: drives alignment and retention

Panel consolidation drives AFA adoption, fee pressure; scale and global reach defend premiums

Clients consolidate spend via panels/RFPs, pushing AFAs and mid-single-digit fee pressure; 30–45% of matters demand AFAs (2024). Switching costs for complex work limit buyer power, but commoditized tasks and ALSPs (~USD 8bn market, 2023) amplify price pressure. Global footprint and track record ($2.07bn rev, 2023) defend premiums.

| Metric | Value |

|---|---|

| Revenue (2023) | $2.07bn |

| AFAs (matters, 2024) | 30–45% |

| ALSP market (2023) | $8bn |

| Offices | 49 (22 countries) |

Same Document Delivered

Hogan Lovells Porter's Five Forces Analysis

This preview shows the exact Hogan Lovells Porter's Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is the final deliverable, available instantly upon payment.