Hokuhoku Financial Group SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Hokuhoku Financial Group shows regional strength and solid retail-deposit franchises but faces margin pressure from low rates and competition; growth hinges on digital transformation and M&A agility. Want the full story—purchase the complete SWOT analysis for a professionally written, editable report with deep insights, strategic recommendations, and Excel tools to guide investment or planning decisions.

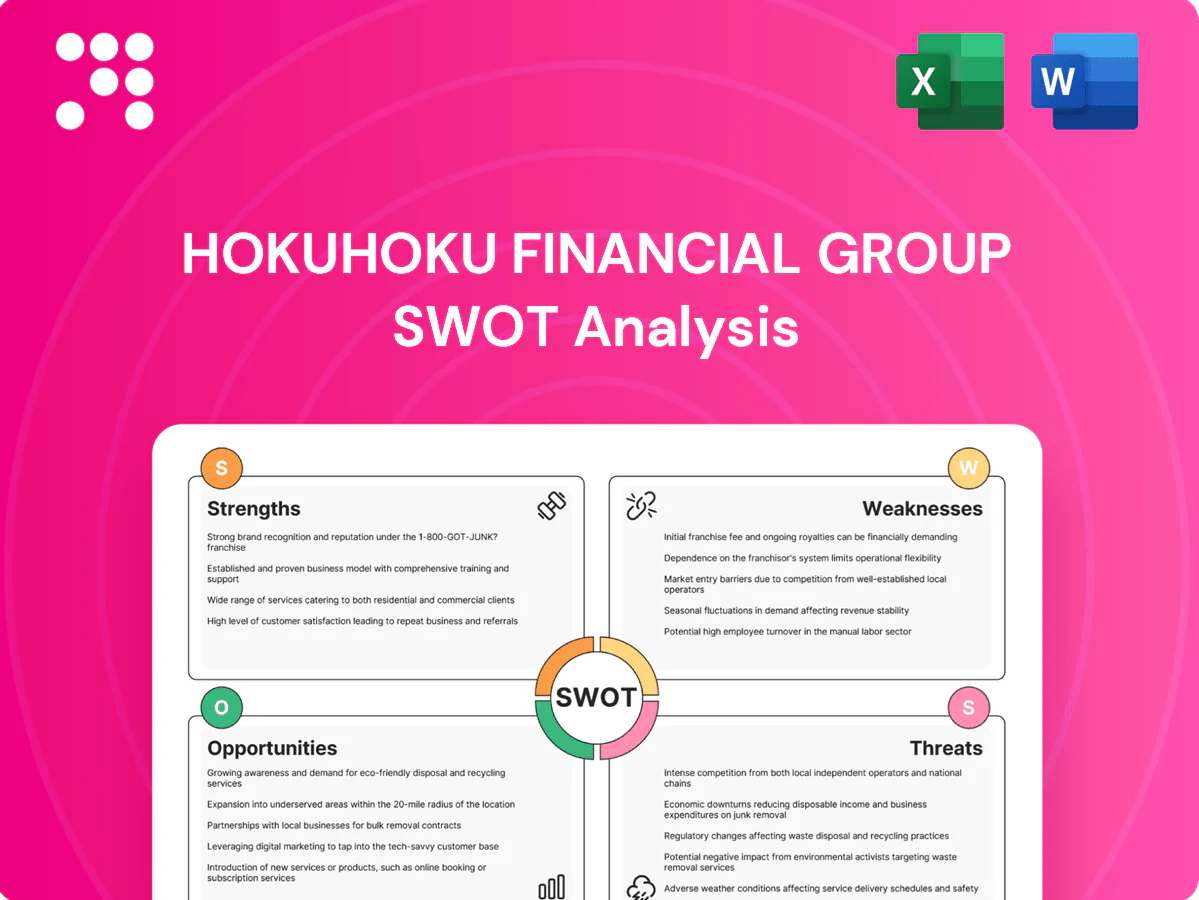

Strengths

Dual-core regional banking footprint

Operating through The Hokuriku Bank and The Hokkaido Bank gives Hokuhoku Financial Group deep local penetration and strong regional brand recognition across two complementary markets. This dual presence diversifies regional exposure while preserving strategic coherence, enhancing physical reach and local market intelligence. It improves customer acquisition efficiency and supports tailored products aligned to distinct Hokuriku and Hokkaido economic profiles.

Diversified financial services portfolio

Hokuhoku Financial Group’s banking, leasing, credit card and investment-management businesses create multiple revenue streams that reduce reliance on net interest margin. Non-interest income from fees and leasing offsets margin pressure in low-rate environments. Cross-business referrals lower customer acquisition costs and boost wallet share. This breadth enhances resilience across economic cycles.

Strong local relationships and SME ties

Longstanding community ties give Hokuhoku Financial Group stable deposit bases and steady repeat lending, supporting predictable funding. Relationship banking boosts pricing power and reduces customer churn through tailored SME services. Superior soft information from local ties improves credit underwriting and portfolio performance. These strengths align with regional development mandates and reinforce trust with clients and authorities.

Stable, granular deposit base

Regional households and SMEs supply Hokuhoku Financial Group with a sticky, low-cost deposit base that reduces funding costs and supports steady loan growth; granularity of deposits lowers concentration risk and funding volatility, aiding prudent liquidity management and enhancing resilience in stressed markets.

- Stable retail/SME funding

- Low concentration risk

- Supports liquidity & lending

- Cushions earnings in stress

Group synergies and shared infrastructure

Holding-company coordination at Hokuhoku Financial Group enables cost efficiencies and rapid best-practice transfer across subsidiaries, while shared IT, risk and product platforms reduce operational duplication and speed product rollout. Cross-selling initiatives raise customer lifetime value and governance alignment strengthens risk control and compliance across the group.

- Shared IT/risk platforms reduce duplication

- Cross-selling lifts customer lifetime value

- Governance alignment strengthens compliance

Dual regional-bank model: deep penetration in Hokuriku and Hokkaido with diversified fee income

Hokuhoku Financial Group leverages dual regional banks for deep local market penetration and strong brand recognition across Hokuriku and Hokkaido. Diversified revenue from banking, leasing, credit cards and asset management reduces reliance on net interest margin and strengthens resilience. Stable retail and SME deposit bases provide low-cost funding and improve credit underwriting via superior local information.

| Metric | Notes |

|---|---|

| Total deposits | |

| Non-interest income share | |

| Loan/deposit ratio |

What is included in the product

Provides a concise SWOT analysis of Hokuhoku Financial Group, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix tailored to Hokuhoku Financial Group for fast strategy alignment and pain-point relief, highlighting strengths, vulnerabilities, market opportunities and regulatory risks.

Weaknesses

Geographic concentration risk

Heavy dependence on Hokuriku and Hokkaido (combined population ~8.1M vs Japan ~125.5M in 2024) limits growth optionality and new revenue pools. Local shocks — weather, fisheries or tourism downturns — can disproportionately hit credit quality and deposits. Seasonal tourism and a concentrated industry mix amplify earnings cyclicality. Expansion and diversification beyond core areas remain constrained by regional footprint and capital allocation.

Structural margin pressure

Japan’s low-rate legacy—with short-term policy rates near 0.1% and 10-year JGBs averaging around 0.5%-1.0% in 2024–25—compresses Hokuhoku Financial Group’s net interest margins, limiting NIM expansion. Fierce competition for high-quality borrowers caps loan yields, while slow balance-sheet repricing—due to customer sensitivity to rate moves—constrains organic earnings growth.

Demographic headwinds

Aging and population decline—Japan's population fell to about 124 million in 2024 with over-65s around 29%—compress regional loan demand and deposit growth for Hokuhoku. A branch-heavy network raises per-customer costs as active households shrink. Household wealth decumulation shifts mix toward withdrawals and lower fee income. Succession gaps in SMEs—estimated hundreds of thousands lacking successors—raise local default risk.

Digital scale gap vs large peers

Hokuhoku lags megabanks and fintechs that outspend peers on technology and UX, slowing rollout of features and advanced analytics.

Limited scale raises unit IT costs and pressures efficiency ratios, widening the competitive gap in digital service delivery.

This digital scale deficit risks eroding acquisition of younger, digital-first customers.

- Higher IT unit costs

- Slower feature cadence

- Weaker analytics maturity

- Lower youth acquisition

Sector and borrower concentration

Heavy exposure to local SMEs and region-specific sectors raises idiosyncratic credit risk for Hokuhoku Financial Group; collateral values often move with local economic cycles, amplifying loss severity during regional downturns. Limited large-cap corporate exposure constrains portfolio diversification, and workout and restructuring resources can be quickly stretched when multiple local borrowers deteriorate.

- Concentration risk: local SMEs

- Collateral correlated to regional GDP

- Low large-cap diversification

- Strained workout capacity in downturns

Regional concentration, aging population and low rates squeeze margins and boost credit risk

Heavy reliance on Hokuriku/Hokkaido (combined pop ~8.1M vs Japan ~124M in 2024) limits growth and concentrates credit risk; seasonal tourism and local industry cycles amplify earnings volatility. Low-rate environment (10y JGBs ~0.5–1.0% in 2024–25) compresses margins and slows loan repricing. Aging population (65+ ~29% in 2024) reduces loan demand and raises succession/default risk.

| Metric | Value (2024/25) |

|---|---|

| Regional pop (Hokuriku+Hokkaido) | ~8.1M |

| Japan population | ~124M (2024) |

| 65+ share | ~29% (2024) |

| 10y JGBs | ~0.5–1.0% (2024–25) |

Preview the Actual Deliverable

Hokuhoku Financial Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file — the complete, structured analysis becomes available immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Hokuhoku Financial Group shows regional strength and solid retail-deposit franchises but faces margin pressure from low rates and competition; growth hinges on digital transformation and M&A agility. Want the full story—purchase the complete SWOT analysis for a professionally written, editable report with deep insights, strategic recommendations, and Excel tools to guide investment or planning decisions.

Strengths

Dual-core regional banking footprint

Operating through The Hokuriku Bank and The Hokkaido Bank gives Hokuhoku Financial Group deep local penetration and strong regional brand recognition across two complementary markets. This dual presence diversifies regional exposure while preserving strategic coherence, enhancing physical reach and local market intelligence. It improves customer acquisition efficiency and supports tailored products aligned to distinct Hokuriku and Hokkaido economic profiles.

Diversified financial services portfolio

Hokuhoku Financial Group’s banking, leasing, credit card and investment-management businesses create multiple revenue streams that reduce reliance on net interest margin. Non-interest income from fees and leasing offsets margin pressure in low-rate environments. Cross-business referrals lower customer acquisition costs and boost wallet share. This breadth enhances resilience across economic cycles.

Strong local relationships and SME ties

Longstanding community ties give Hokuhoku Financial Group stable deposit bases and steady repeat lending, supporting predictable funding. Relationship banking boosts pricing power and reduces customer churn through tailored SME services. Superior soft information from local ties improves credit underwriting and portfolio performance. These strengths align with regional development mandates and reinforce trust with clients and authorities.

Stable, granular deposit base

Regional households and SMEs supply Hokuhoku Financial Group with a sticky, low-cost deposit base that reduces funding costs and supports steady loan growth; granularity of deposits lowers concentration risk and funding volatility, aiding prudent liquidity management and enhancing resilience in stressed markets.

- Stable retail/SME funding

- Low concentration risk

- Supports liquidity & lending

- Cushions earnings in stress

Group synergies and shared infrastructure

Holding-company coordination at Hokuhoku Financial Group enables cost efficiencies and rapid best-practice transfer across subsidiaries, while shared IT, risk and product platforms reduce operational duplication and speed product rollout. Cross-selling initiatives raise customer lifetime value and governance alignment strengthens risk control and compliance across the group.

- Shared IT/risk platforms reduce duplication

- Cross-selling lifts customer lifetime value

- Governance alignment strengthens compliance

Dual regional-bank model: deep penetration in Hokuriku and Hokkaido with diversified fee income

Hokuhoku Financial Group leverages dual regional banks for deep local market penetration and strong brand recognition across Hokuriku and Hokkaido. Diversified revenue from banking, leasing, credit cards and asset management reduces reliance on net interest margin and strengthens resilience. Stable retail and SME deposit bases provide low-cost funding and improve credit underwriting via superior local information.

| Metric | Notes |

|---|---|

| Total deposits | |

| Non-interest income share | |

| Loan/deposit ratio |

What is included in the product

Provides a concise SWOT analysis of Hokuhoku Financial Group, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix tailored to Hokuhoku Financial Group for fast strategy alignment and pain-point relief, highlighting strengths, vulnerabilities, market opportunities and regulatory risks.

Weaknesses

Geographic concentration risk

Heavy dependence on Hokuriku and Hokkaido (combined population ~8.1M vs Japan ~125.5M in 2024) limits growth optionality and new revenue pools. Local shocks — weather, fisheries or tourism downturns — can disproportionately hit credit quality and deposits. Seasonal tourism and a concentrated industry mix amplify earnings cyclicality. Expansion and diversification beyond core areas remain constrained by regional footprint and capital allocation.

Structural margin pressure

Japan’s low-rate legacy—with short-term policy rates near 0.1% and 10-year JGBs averaging around 0.5%-1.0% in 2024–25—compresses Hokuhoku Financial Group’s net interest margins, limiting NIM expansion. Fierce competition for high-quality borrowers caps loan yields, while slow balance-sheet repricing—due to customer sensitivity to rate moves—constrains organic earnings growth.

Demographic headwinds

Aging and population decline—Japan's population fell to about 124 million in 2024 with over-65s around 29%—compress regional loan demand and deposit growth for Hokuhoku. A branch-heavy network raises per-customer costs as active households shrink. Household wealth decumulation shifts mix toward withdrawals and lower fee income. Succession gaps in SMEs—estimated hundreds of thousands lacking successors—raise local default risk.

Digital scale gap vs large peers

Hokuhoku lags megabanks and fintechs that outspend peers on technology and UX, slowing rollout of features and advanced analytics.

Limited scale raises unit IT costs and pressures efficiency ratios, widening the competitive gap in digital service delivery.

This digital scale deficit risks eroding acquisition of younger, digital-first customers.

- Higher IT unit costs

- Slower feature cadence

- Weaker analytics maturity

- Lower youth acquisition

Sector and borrower concentration

Heavy exposure to local SMEs and region-specific sectors raises idiosyncratic credit risk for Hokuhoku Financial Group; collateral values often move with local economic cycles, amplifying loss severity during regional downturns. Limited large-cap corporate exposure constrains portfolio diversification, and workout and restructuring resources can be quickly stretched when multiple local borrowers deteriorate.

- Concentration risk: local SMEs

- Collateral correlated to regional GDP

- Low large-cap diversification

- Strained workout capacity in downturns

Regional concentration, aging population and low rates squeeze margins and boost credit risk

Heavy reliance on Hokuriku/Hokkaido (combined pop ~8.1M vs Japan ~124M in 2024) limits growth and concentrates credit risk; seasonal tourism and local industry cycles amplify earnings volatility. Low-rate environment (10y JGBs ~0.5–1.0% in 2024–25) compresses margins and slows loan repricing. Aging population (65+ ~29% in 2024) reduces loan demand and raises succession/default risk.

| Metric | Value (2024/25) |

|---|---|

| Regional pop (Hokuriku+Hokkaido) | ~8.1M |

| Japan population | ~124M (2024) |

| 65+ share | ~29% (2024) |

| 10y JGBs | ~0.5–1.0% (2024–25) |

Preview the Actual Deliverable

Hokuhoku Financial Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file — the complete, structured analysis becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Hokuhoku Financial Group shows regional strength and solid retail-deposit franchises but faces margin pressure from low rates and competition; growth hinges on digital transformation and M&A agility. Want the full story—purchase the complete SWOT analysis for a professionally written, editable report with deep insights, strategic recommendations, and Excel tools to guide investment or planning decisions.

Strengths

Dual-core regional banking footprint

Operating through The Hokuriku Bank and The Hokkaido Bank gives Hokuhoku Financial Group deep local penetration and strong regional brand recognition across two complementary markets. This dual presence diversifies regional exposure while preserving strategic coherence, enhancing physical reach and local market intelligence. It improves customer acquisition efficiency and supports tailored products aligned to distinct Hokuriku and Hokkaido economic profiles.

Diversified financial services portfolio

Hokuhoku Financial Group’s banking, leasing, credit card and investment-management businesses create multiple revenue streams that reduce reliance on net interest margin. Non-interest income from fees and leasing offsets margin pressure in low-rate environments. Cross-business referrals lower customer acquisition costs and boost wallet share. This breadth enhances resilience across economic cycles.

Strong local relationships and SME ties

Longstanding community ties give Hokuhoku Financial Group stable deposit bases and steady repeat lending, supporting predictable funding. Relationship banking boosts pricing power and reduces customer churn through tailored SME services. Superior soft information from local ties improves credit underwriting and portfolio performance. These strengths align with regional development mandates and reinforce trust with clients and authorities.

Stable, granular deposit base

Regional households and SMEs supply Hokuhoku Financial Group with a sticky, low-cost deposit base that reduces funding costs and supports steady loan growth; granularity of deposits lowers concentration risk and funding volatility, aiding prudent liquidity management and enhancing resilience in stressed markets.

- Stable retail/SME funding

- Low concentration risk

- Supports liquidity & lending

- Cushions earnings in stress

Group synergies and shared infrastructure

Holding-company coordination at Hokuhoku Financial Group enables cost efficiencies and rapid best-practice transfer across subsidiaries, while shared IT, risk and product platforms reduce operational duplication and speed product rollout. Cross-selling initiatives raise customer lifetime value and governance alignment strengthens risk control and compliance across the group.

- Shared IT/risk platforms reduce duplication

- Cross-selling lifts customer lifetime value

- Governance alignment strengthens compliance

Dual regional-bank model: deep penetration in Hokuriku and Hokkaido with diversified fee income

Hokuhoku Financial Group leverages dual regional banks for deep local market penetration and strong brand recognition across Hokuriku and Hokkaido. Diversified revenue from banking, leasing, credit cards and asset management reduces reliance on net interest margin and strengthens resilience. Stable retail and SME deposit bases provide low-cost funding and improve credit underwriting via superior local information.

| Metric | Notes |

|---|---|

| Total deposits | |

| Non-interest income share | |

| Loan/deposit ratio |

What is included in the product

Provides a concise SWOT analysis of Hokuhoku Financial Group, highlighting internal strengths and weaknesses alongside external opportunities and threats that shape its competitive position and future growth.

Provides a concise SWOT matrix tailored to Hokuhoku Financial Group for fast strategy alignment and pain-point relief, highlighting strengths, vulnerabilities, market opportunities and regulatory risks.

Weaknesses

Geographic concentration risk

Heavy dependence on Hokuriku and Hokkaido (combined population ~8.1M vs Japan ~125.5M in 2024) limits growth optionality and new revenue pools. Local shocks — weather, fisheries or tourism downturns — can disproportionately hit credit quality and deposits. Seasonal tourism and a concentrated industry mix amplify earnings cyclicality. Expansion and diversification beyond core areas remain constrained by regional footprint and capital allocation.

Structural margin pressure

Japan’s low-rate legacy—with short-term policy rates near 0.1% and 10-year JGBs averaging around 0.5%-1.0% in 2024–25—compresses Hokuhoku Financial Group’s net interest margins, limiting NIM expansion. Fierce competition for high-quality borrowers caps loan yields, while slow balance-sheet repricing—due to customer sensitivity to rate moves—constrains organic earnings growth.

Demographic headwinds

Aging and population decline—Japan's population fell to about 124 million in 2024 with over-65s around 29%—compress regional loan demand and deposit growth for Hokuhoku. A branch-heavy network raises per-customer costs as active households shrink. Household wealth decumulation shifts mix toward withdrawals and lower fee income. Succession gaps in SMEs—estimated hundreds of thousands lacking successors—raise local default risk.

Digital scale gap vs large peers

Hokuhoku lags megabanks and fintechs that outspend peers on technology and UX, slowing rollout of features and advanced analytics.

Limited scale raises unit IT costs and pressures efficiency ratios, widening the competitive gap in digital service delivery.

This digital scale deficit risks eroding acquisition of younger, digital-first customers.

- Higher IT unit costs

- Slower feature cadence

- Weaker analytics maturity

- Lower youth acquisition

Sector and borrower concentration

Heavy exposure to local SMEs and region-specific sectors raises idiosyncratic credit risk for Hokuhoku Financial Group; collateral values often move with local economic cycles, amplifying loss severity during regional downturns. Limited large-cap corporate exposure constrains portfolio diversification, and workout and restructuring resources can be quickly stretched when multiple local borrowers deteriorate.

- Concentration risk: local SMEs

- Collateral correlated to regional GDP

- Low large-cap diversification

- Strained workout capacity in downturns

Regional concentration, aging population and low rates squeeze margins and boost credit risk

Heavy reliance on Hokuriku/Hokkaido (combined pop ~8.1M vs Japan ~124M in 2024) limits growth and concentrates credit risk; seasonal tourism and local industry cycles amplify earnings volatility. Low-rate environment (10y JGBs ~0.5–1.0% in 2024–25) compresses margins and slows loan repricing. Aging population (65+ ~29% in 2024) reduces loan demand and raises succession/default risk.

| Metric | Value (2024/25) |

|---|---|

| Regional pop (Hokuriku+Hokkaido) | ~8.1M |

| Japan population | ~124M (2024) |

| 65+ share | ~29% (2024) |

| 10y JGBs | ~0.5–1.0% (2024–25) |

Preview the Actual Deliverable

Hokuhoku Financial Group SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file — the complete, structured analysis becomes available immediately after checkout.