North Pacific Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

North Pacific Bank faces evolving competitive dynamics—strong regional rivalry, growing buyer sophistication, and regulatory pressure that shape margins and growth choices. Supplier and substitute risks are moderate but rising as fintech alternatives expand. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore North Pacific Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core tech vendors

Japan’s regional banks depend on three dominant core-banking and payment vendors, concentrating supplier power and raising switching costs. Limited alternatives grant suppliers leverage on pricing and delivery timelines, with core contracts typically spanning 5–10 years. Any outage or upgrade delay can halt customer services and regulatory reporting, as shown in past national incidents. Hokuyo must secure long-term contracts and modular diversification to mitigate this risk.

Funding mix and wholesale markets

Primary funding is anchored by low-cost local deposits, but reliance on supplemental wholesale and interbank lines creates exposure as capital markets and correspondent banks can episodically reprice access. Market stress or shifts in BOJ policy have shown rapid repricing risk in 2023–24. Maintaining LCR and NSFR comfortably above the Basel III minima of 100% is essential to counterbalance this supplier power.

Payment networks and card schemes

Card associations and networks set fees, rules and technical standards that directly affect North Pacific Bank, with interchange and scheme fees typically ranging about 1–3% of transaction value. Compliance and certification (PCI DSS, EMV) impose fixed and variable costs, increasing dependence on networks and raising operating expenses. Changes to interchange or security mandates can compress merchant margins and bank net interest on card portfolios. Co-branding and volume commitments can lower effective fees by tens of basis points.

Talent and specialist skills

IT security, risk and data analytics talent is scarce in regional markets, with ISC2 reporting a 3.4 million global cybersecurity workforce gap in 2024, giving skilled employees and recruiters heightened bargaining power. The bank may face pressure to raise wages or rely on outsourcing to close gaps. Building internal academies and expanding remote hiring can materially reduce dependency on tight local labor pools.

- ISC2 2024: 3.4M global cyber workforce gap

- Scarcity increases recruiter leverage and wage pressure

- Mitigants: internal academies, remote hiring, selective outsourcing

Regulatory infrastructure dependencies

Regulatory infrastructure dependencies give suppliers indirect power over North Pacific Bank as FSA/BOJ mandates and national clearing rules require timed tech and process upgrades, driving capital expenditure and operational shifts. Rule changes in 2024 forced many Japanese banks to accelerate projects, while compliance vendors and auditors materially shape ongoing cost structures. Proactive engagement with regulators and adoption of RegTech (global RegTech market ~USD 12.1 billion in 2024) can reduce compliance burden and capex timing risks.

- FSA/BOJ mandates → forced upgrade timelines

- Clearing systems process trillions JPY → indirect supplier leverage

- Compliance vendors/auditors influence costs

- RegTech adoption (2024 market ~USD 12.1bn) lowers burden

Vendor concentration and funding repricing amplify outage, liquidity and cyber cost risks

Core banking vendors (5–10yr contracts) concentrate supplier power, raising switching costs and outage risk for North Pacific Bank.

Wholesale funding access repriced in 2023–24; maintaining LCR/NSFR above 100% is critical to offset repricing shocks.

Card schemes (1–3% fees) and scarce cyber talent (ISC2 2024 gap 3.4M) add recurring cost pressure.

RegTech market ~USD 12.1bn (2024) offers mitigation via automation and faster compliance.

| Metric | Value |

|---|---|

| Core vendor contract | 5–10 yrs |

| Interchange fees | 1–3% |

| Cyber gap (ISC2 2024) | 3.4M |

| RegTech market 2024 | USD 12.1bn |

What is included in the product

Tailored Porter's Five Forces analysis for North Pacific Bank revealing competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and profitability.

One-sheet Porter's Five Forces for North Pacific Bank—clarifies competitive pressures and relief points for rapid strategic decisions. Customize force levels and swap in your data to map risk, regulation, and new entrants instantly for board-ready slides.

Customers Bargaining Power

SME borrowers with rate sensitivity

Local SME borrowers—part of the 99.7% of Japanese firms—shop rates and collateral across regional banks and shinkin banks, where spreads often range 10–50 bps in 2024; Hokkaido’s sluggish low-growth environment increases price sensitivity. Larger SMEs (top-tier clients) routinely extract concessions on covenants and fees, while relationship banking and advisory services mute pure rate competition.

Retail customers with low switching costs

Digital onboarding and account portability in 2024 have cut switching friction, with open-banking APIs and same-day transfer rails enabling rapid moves between providers. Consumers routinely shop deposit and loan rates online, eroding pricing power. App ecosystems and bundled rewards are increasing loyalty but remain fragile, so targeted bundles and tiered rewards are key to boosting stickiness.

Corporate treasury diversification

Mid-to-large corporates increasingly diversify treasury relationships across megabanks, Japan Post Bank and securities firms, giving buyers greater leverage as the big three banks still command a majority of corporate deposit flows (>60% market share). RFP-driven selection has commoditized cash-management fees and services, with many corporates benchmarking prices annually. Custom APIs and faster-payment rails have emerged in 2024 as key retention tools, preserving share through integration and speed.

Investment product comparison

- Comparable products

- Transparent pricing

- Fee pressure ~0.5–1.0%

- Advisory-driven differentiation

Demographic headwinds in Hokkaido

Demographic headwinds in Hokkaido cut aggregate loan demand as the prefecture’s population fell to about 5.10 million in 2024 and the 65+ cohort reached roughly 33%, shrinking the pool of credit-seeking households. Fewer borrowers increase buyer leverage — remaining customers can demand lower rates or switch banks with little frictions, pressuring margins. Banks become deposit-rich but loan-light, compressing NIMs, though tailored senior services (wealth management, fee-based payments) can help monetize low-yield deposits.

- Hokkaido population ~5.10M (2024)

- 65+ share ~33% (2024)

- Deposit-heavy / loan-light → NIM pressure

- Opportunity: fee income from senior services

Margin squeeze: SME spreads 10–50 bps, fees 0.5–1.0%

Customers wield high price sensitivity: SME spreads 10–50 bps (2024), fee compression ~0.5–1.0% in retail channels, and digital onboarding + open APIs boost switching; Hokkaido pop 5.10M, 65+ ≈33% (2024) increases deposit-heavy/loan-light dynamics. Megabanks hold >60% corporate deposits; robo-advisor AUM > $1T (2024), raising transparency and bargaining power.

| Metric | 2024 |

|---|---|

| SME spread range | 10–50 bps |

| Fee pressure | 0.5–1.0% |

| Hokkaido pop | 5.10M |

| 65+ share | ≈33% |

| Megabanks corp deposit share | >60% |

| Robo AUM | >$1T |

Preview the Actual Deliverable

North Pacific Bank Porter's Five Forces Analysis

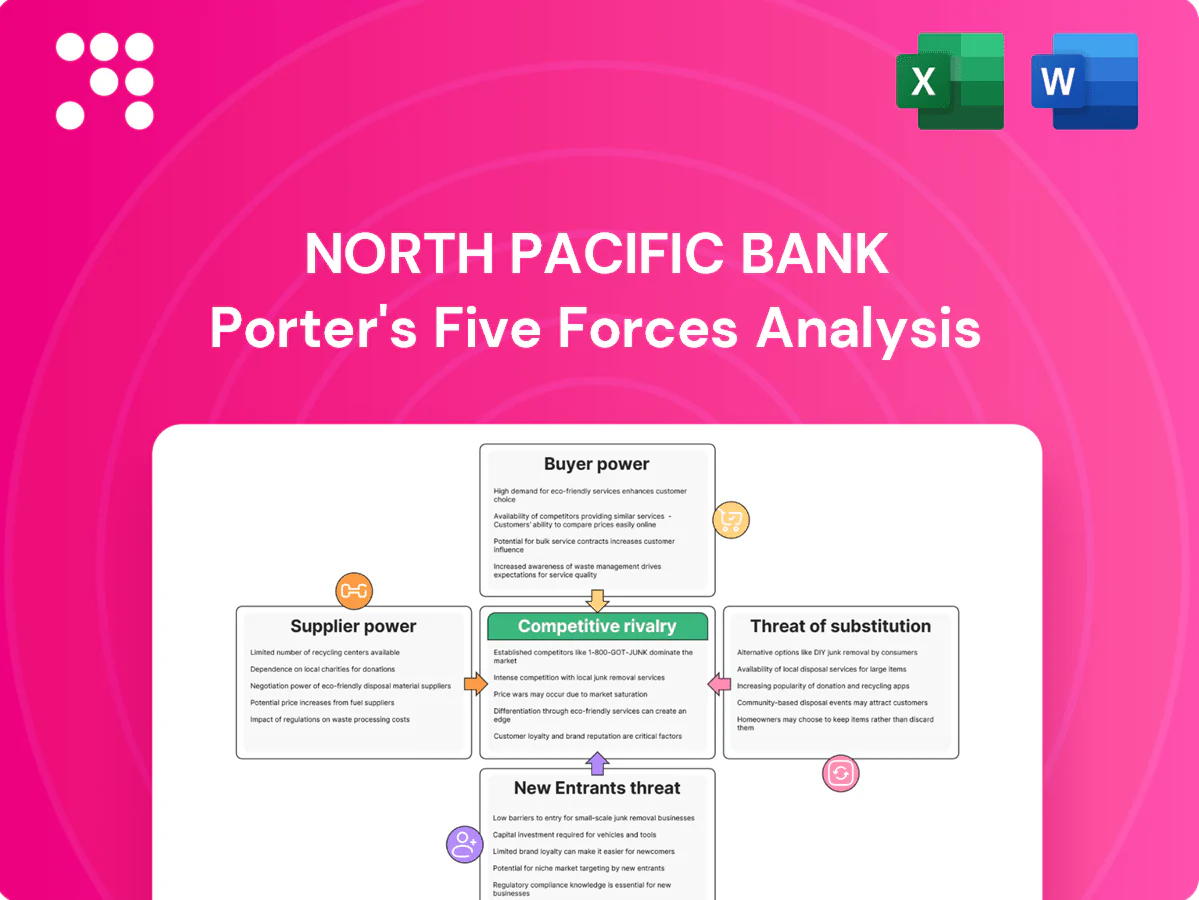

This preview shows the exact Porter's Five Forces analysis of North Pacific Bank you'll receive—no placeholders or samples. The document covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. It's fully formatted and ready to download immediately after purchase.

Go Beyond the Preview—Access the Full Strategic Report

North Pacific Bank faces evolving competitive dynamics—strong regional rivalry, growing buyer sophistication, and regulatory pressure that shape margins and growth choices. Supplier and substitute risks are moderate but rising as fintech alternatives expand. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore North Pacific Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core tech vendors

Japan’s regional banks depend on three dominant core-banking and payment vendors, concentrating supplier power and raising switching costs. Limited alternatives grant suppliers leverage on pricing and delivery timelines, with core contracts typically spanning 5–10 years. Any outage or upgrade delay can halt customer services and regulatory reporting, as shown in past national incidents. Hokuyo must secure long-term contracts and modular diversification to mitigate this risk.

Funding mix and wholesale markets

Primary funding is anchored by low-cost local deposits, but reliance on supplemental wholesale and interbank lines creates exposure as capital markets and correspondent banks can episodically reprice access. Market stress or shifts in BOJ policy have shown rapid repricing risk in 2023–24. Maintaining LCR and NSFR comfortably above the Basel III minima of 100% is essential to counterbalance this supplier power.

Payment networks and card schemes

Card associations and networks set fees, rules and technical standards that directly affect North Pacific Bank, with interchange and scheme fees typically ranging about 1–3% of transaction value. Compliance and certification (PCI DSS, EMV) impose fixed and variable costs, increasing dependence on networks and raising operating expenses. Changes to interchange or security mandates can compress merchant margins and bank net interest on card portfolios. Co-branding and volume commitments can lower effective fees by tens of basis points.

Talent and specialist skills

IT security, risk and data analytics talent is scarce in regional markets, with ISC2 reporting a 3.4 million global cybersecurity workforce gap in 2024, giving skilled employees and recruiters heightened bargaining power. The bank may face pressure to raise wages or rely on outsourcing to close gaps. Building internal academies and expanding remote hiring can materially reduce dependency on tight local labor pools.

- ISC2 2024: 3.4M global cyber workforce gap

- Scarcity increases recruiter leverage and wage pressure

- Mitigants: internal academies, remote hiring, selective outsourcing

Regulatory infrastructure dependencies

Regulatory infrastructure dependencies give suppliers indirect power over North Pacific Bank as FSA/BOJ mandates and national clearing rules require timed tech and process upgrades, driving capital expenditure and operational shifts. Rule changes in 2024 forced many Japanese banks to accelerate projects, while compliance vendors and auditors materially shape ongoing cost structures. Proactive engagement with regulators and adoption of RegTech (global RegTech market ~USD 12.1 billion in 2024) can reduce compliance burden and capex timing risks.

- FSA/BOJ mandates → forced upgrade timelines

- Clearing systems process trillions JPY → indirect supplier leverage

- Compliance vendors/auditors influence costs

- RegTech adoption (2024 market ~USD 12.1bn) lowers burden

Vendor concentration and funding repricing amplify outage, liquidity and cyber cost risks

Core banking vendors (5–10yr contracts) concentrate supplier power, raising switching costs and outage risk for North Pacific Bank.

Wholesale funding access repriced in 2023–24; maintaining LCR/NSFR above 100% is critical to offset repricing shocks.

Card schemes (1–3% fees) and scarce cyber talent (ISC2 2024 gap 3.4M) add recurring cost pressure.

RegTech market ~USD 12.1bn (2024) offers mitigation via automation and faster compliance.

| Metric | Value |

|---|---|

| Core vendor contract | 5–10 yrs |

| Interchange fees | 1–3% |

| Cyber gap (ISC2 2024) | 3.4M |

| RegTech market 2024 | USD 12.1bn |

What is included in the product

Tailored Porter's Five Forces analysis for North Pacific Bank revealing competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and profitability.

One-sheet Porter's Five Forces for North Pacific Bank—clarifies competitive pressures and relief points for rapid strategic decisions. Customize force levels and swap in your data to map risk, regulation, and new entrants instantly for board-ready slides.

Customers Bargaining Power

SME borrowers with rate sensitivity

Local SME borrowers—part of the 99.7% of Japanese firms—shop rates and collateral across regional banks and shinkin banks, where spreads often range 10–50 bps in 2024; Hokkaido’s sluggish low-growth environment increases price sensitivity. Larger SMEs (top-tier clients) routinely extract concessions on covenants and fees, while relationship banking and advisory services mute pure rate competition.

Retail customers with low switching costs

Digital onboarding and account portability in 2024 have cut switching friction, with open-banking APIs and same-day transfer rails enabling rapid moves between providers. Consumers routinely shop deposit and loan rates online, eroding pricing power. App ecosystems and bundled rewards are increasing loyalty but remain fragile, so targeted bundles and tiered rewards are key to boosting stickiness.

Corporate treasury diversification

Mid-to-large corporates increasingly diversify treasury relationships across megabanks, Japan Post Bank and securities firms, giving buyers greater leverage as the big three banks still command a majority of corporate deposit flows (>60% market share). RFP-driven selection has commoditized cash-management fees and services, with many corporates benchmarking prices annually. Custom APIs and faster-payment rails have emerged in 2024 as key retention tools, preserving share through integration and speed.

Investment product comparison

- Comparable products

- Transparent pricing

- Fee pressure ~0.5–1.0%

- Advisory-driven differentiation

Demographic headwinds in Hokkaido

Demographic headwinds in Hokkaido cut aggregate loan demand as the prefecture’s population fell to about 5.10 million in 2024 and the 65+ cohort reached roughly 33%, shrinking the pool of credit-seeking households. Fewer borrowers increase buyer leverage — remaining customers can demand lower rates or switch banks with little frictions, pressuring margins. Banks become deposit-rich but loan-light, compressing NIMs, though tailored senior services (wealth management, fee-based payments) can help monetize low-yield deposits.

- Hokkaido population ~5.10M (2024)

- 65+ share ~33% (2024)

- Deposit-heavy / loan-light → NIM pressure

- Opportunity: fee income from senior services

Margin squeeze: SME spreads 10–50 bps, fees 0.5–1.0%

Customers wield high price sensitivity: SME spreads 10–50 bps (2024), fee compression ~0.5–1.0% in retail channels, and digital onboarding + open APIs boost switching; Hokkaido pop 5.10M, 65+ ≈33% (2024) increases deposit-heavy/loan-light dynamics. Megabanks hold >60% corporate deposits; robo-advisor AUM > $1T (2024), raising transparency and bargaining power.

| Metric | 2024 |

|---|---|

| SME spread range | 10–50 bps |

| Fee pressure | 0.5–1.0% |

| Hokkaido pop | 5.10M |

| 65+ share | ≈33% |

| Megabanks corp deposit share | >60% |

| Robo AUM | >$1T |

Preview the Actual Deliverable

North Pacific Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of North Pacific Bank you'll receive—no placeholders or samples. The document covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. It's fully formatted and ready to download immediately after purchase.

Description

Go Beyond the Preview—Access the Full Strategic Report

North Pacific Bank faces evolving competitive dynamics—strong regional rivalry, growing buyer sophistication, and regulatory pressure that shape margins and growth choices. Supplier and substitute risks are moderate but rising as fintech alternatives expand. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore North Pacific Bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated core tech vendors

Japan’s regional banks depend on three dominant core-banking and payment vendors, concentrating supplier power and raising switching costs. Limited alternatives grant suppliers leverage on pricing and delivery timelines, with core contracts typically spanning 5–10 years. Any outage or upgrade delay can halt customer services and regulatory reporting, as shown in past national incidents. Hokuyo must secure long-term contracts and modular diversification to mitigate this risk.

Funding mix and wholesale markets

Primary funding is anchored by low-cost local deposits, but reliance on supplemental wholesale and interbank lines creates exposure as capital markets and correspondent banks can episodically reprice access. Market stress or shifts in BOJ policy have shown rapid repricing risk in 2023–24. Maintaining LCR and NSFR comfortably above the Basel III minima of 100% is essential to counterbalance this supplier power.

Payment networks and card schemes

Card associations and networks set fees, rules and technical standards that directly affect North Pacific Bank, with interchange and scheme fees typically ranging about 1–3% of transaction value. Compliance and certification (PCI DSS, EMV) impose fixed and variable costs, increasing dependence on networks and raising operating expenses. Changes to interchange or security mandates can compress merchant margins and bank net interest on card portfolios. Co-branding and volume commitments can lower effective fees by tens of basis points.

Talent and specialist skills

IT security, risk and data analytics talent is scarce in regional markets, with ISC2 reporting a 3.4 million global cybersecurity workforce gap in 2024, giving skilled employees and recruiters heightened bargaining power. The bank may face pressure to raise wages or rely on outsourcing to close gaps. Building internal academies and expanding remote hiring can materially reduce dependency on tight local labor pools.

- ISC2 2024: 3.4M global cyber workforce gap

- Scarcity increases recruiter leverage and wage pressure

- Mitigants: internal academies, remote hiring, selective outsourcing

Regulatory infrastructure dependencies

Regulatory infrastructure dependencies give suppliers indirect power over North Pacific Bank as FSA/BOJ mandates and national clearing rules require timed tech and process upgrades, driving capital expenditure and operational shifts. Rule changes in 2024 forced many Japanese banks to accelerate projects, while compliance vendors and auditors materially shape ongoing cost structures. Proactive engagement with regulators and adoption of RegTech (global RegTech market ~USD 12.1 billion in 2024) can reduce compliance burden and capex timing risks.

- FSA/BOJ mandates → forced upgrade timelines

- Clearing systems process trillions JPY → indirect supplier leverage

- Compliance vendors/auditors influence costs

- RegTech adoption (2024 market ~USD 12.1bn) lowers burden

Vendor concentration and funding repricing amplify outage, liquidity and cyber cost risks

Core banking vendors (5–10yr contracts) concentrate supplier power, raising switching costs and outage risk for North Pacific Bank.

Wholesale funding access repriced in 2023–24; maintaining LCR/NSFR above 100% is critical to offset repricing shocks.

Card schemes (1–3% fees) and scarce cyber talent (ISC2 2024 gap 3.4M) add recurring cost pressure.

RegTech market ~USD 12.1bn (2024) offers mitigation via automation and faster compliance.

| Metric | Value |

|---|---|

| Core vendor contract | 5–10 yrs |

| Interchange fees | 1–3% |

| Cyber gap (ISC2 2024) | 3.4M |

| RegTech market 2024 | USD 12.1bn |

What is included in the product

Tailored Porter's Five Forces analysis for North Pacific Bank revealing competitive intensity, buyer and supplier power, threat of new entrants and substitutes, and strategic levers to defend market share and profitability.

One-sheet Porter's Five Forces for North Pacific Bank—clarifies competitive pressures and relief points for rapid strategic decisions. Customize force levels and swap in your data to map risk, regulation, and new entrants instantly for board-ready slides.

Customers Bargaining Power

SME borrowers with rate sensitivity

Local SME borrowers—part of the 99.7% of Japanese firms—shop rates and collateral across regional banks and shinkin banks, where spreads often range 10–50 bps in 2024; Hokkaido’s sluggish low-growth environment increases price sensitivity. Larger SMEs (top-tier clients) routinely extract concessions on covenants and fees, while relationship banking and advisory services mute pure rate competition.

Retail customers with low switching costs

Digital onboarding and account portability in 2024 have cut switching friction, with open-banking APIs and same-day transfer rails enabling rapid moves between providers. Consumers routinely shop deposit and loan rates online, eroding pricing power. App ecosystems and bundled rewards are increasing loyalty but remain fragile, so targeted bundles and tiered rewards are key to boosting stickiness.

Corporate treasury diversification

Mid-to-large corporates increasingly diversify treasury relationships across megabanks, Japan Post Bank and securities firms, giving buyers greater leverage as the big three banks still command a majority of corporate deposit flows (>60% market share). RFP-driven selection has commoditized cash-management fees and services, with many corporates benchmarking prices annually. Custom APIs and faster-payment rails have emerged in 2024 as key retention tools, preserving share through integration and speed.

Investment product comparison

- Comparable products

- Transparent pricing

- Fee pressure ~0.5–1.0%

- Advisory-driven differentiation

Demographic headwinds in Hokkaido

Demographic headwinds in Hokkaido cut aggregate loan demand as the prefecture’s population fell to about 5.10 million in 2024 and the 65+ cohort reached roughly 33%, shrinking the pool of credit-seeking households. Fewer borrowers increase buyer leverage — remaining customers can demand lower rates or switch banks with little frictions, pressuring margins. Banks become deposit-rich but loan-light, compressing NIMs, though tailored senior services (wealth management, fee-based payments) can help monetize low-yield deposits.

- Hokkaido population ~5.10M (2024)

- 65+ share ~33% (2024)

- Deposit-heavy / loan-light → NIM pressure

- Opportunity: fee income from senior services

Margin squeeze: SME spreads 10–50 bps, fees 0.5–1.0%

Customers wield high price sensitivity: SME spreads 10–50 bps (2024), fee compression ~0.5–1.0% in retail channels, and digital onboarding + open APIs boost switching; Hokkaido pop 5.10M, 65+ ≈33% (2024) increases deposit-heavy/loan-light dynamics. Megabanks hold >60% corporate deposits; robo-advisor AUM > $1T (2024), raising transparency and bargaining power.

| Metric | 2024 |

|---|---|

| SME spread range | 10–50 bps |

| Fee pressure | 0.5–1.0% |

| Hokkaido pop | 5.10M |

| 65+ share | ≈33% |

| Megabanks corp deposit share | >60% |

| Robo AUM | >$1T |

Preview the Actual Deliverable

North Pacific Bank Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of North Pacific Bank you'll receive—no placeholders or samples. The document covers competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications. It's fully formatted and ready to download immediately after purchase.