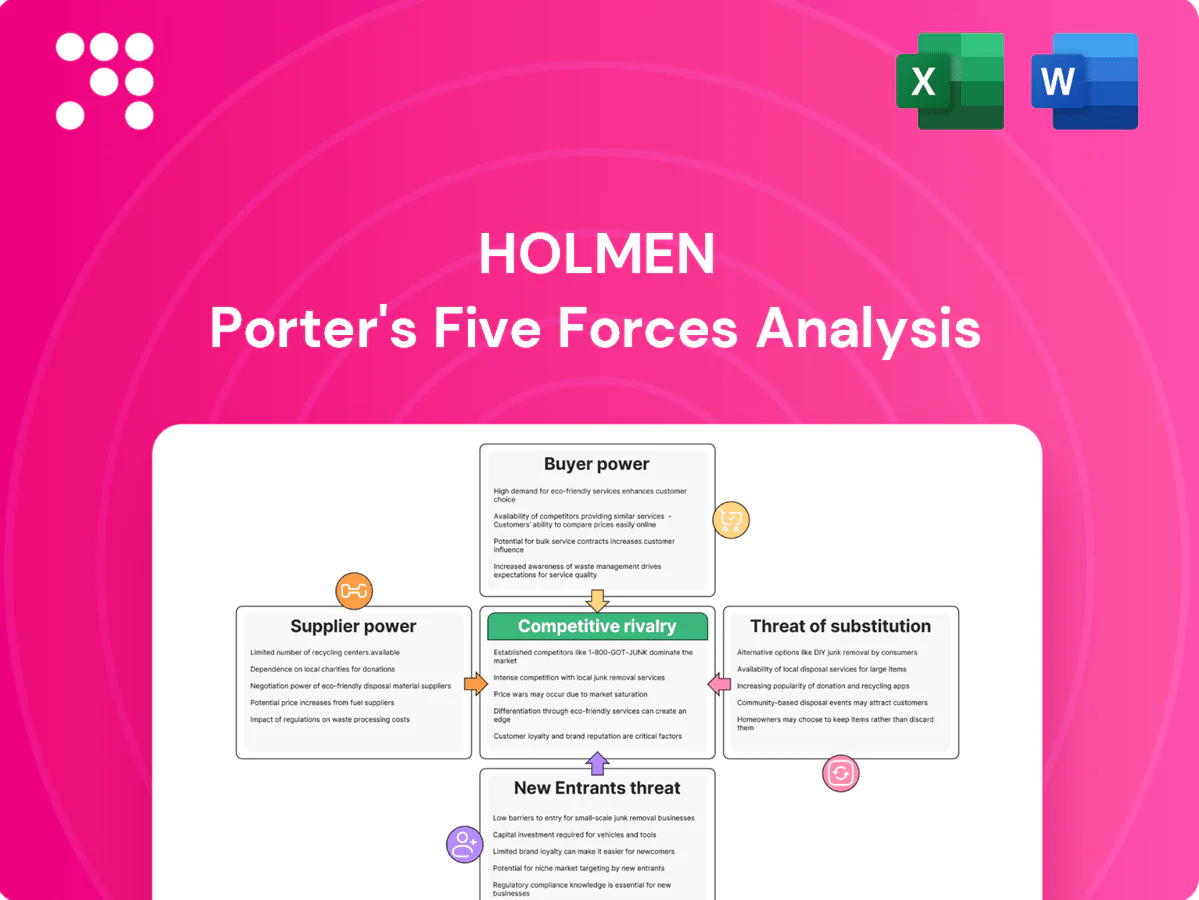

Holmen Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Holmen faces unique pressures from raw-material suppliers, cyclical demand for paper products and growing substitute threats, all shaping its strategic position in forest products and packaging markets. This brief snapshot highlights core competitive dynamics and key vulnerabilities. Unlock the full Porter's Five Forces Analysis to explore Holmen’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Back-integrated fiber reduces dependence

Holmen’s back-integrated model, anchored by roughly 1.3 million hectares of owned forest, internalizes a critical raw material and reduces supplier leverage on fiber, improving cost control and supply certainty versus peers dependent on external pulpwood. This integration shifts bargaining power toward Holmen, though supplier power remains for specialty inputs such as pulp additives where alternatives are limited.

Specialty chemicals and packaging additives

Resin, starch, bleaching agents and coating chemicals are often supplied by a concentrated global set of players; the global specialty chemicals market was roughly $800 billion in 2024, keeping market share and pricing power clustered. Switching costs for Holmen can be material due to qualification, quality variance and machine recalibration, raising supplier leverage. Multi-sourcing and long-term contracts (often 2–5 years) mitigate price risk. Innovation-led suppliers retaining unique chemistries exert moderate bargaining power.

Capital equipment and maintenance OEMs

Paperboard machines, sawmill lines and turbines are concentrated among a few OEMs (notably Valmet and Voith for paper, major turbine makers for power), creating high switching barriers; parts, upgrades and service lock-in sustain supplier influence. Lifecycle agreements commonly trade lower price for uptime guarantees of 98–99%. Holmen’s scale gives some countervailing negotiation leverage.

Energy, logistics, and freight providers

Despite Holmen's own hydro and wind output, Nord Pool day‑ahead averaged ~45 EUR/MWh in 2024, and episodic fuel and grid market swings still push costs; transport capacity and port slots can tighten in peak cycles, boosting logistics supplier leverage by roughly 10–25%. Long‑term rail and port contracts and close customer proximity mitigate spikes, and using multiple carriers reduces single‑provider exposure.

- Energy volatility: Nord Pool ~45 EUR/MWh (2024)

- Logistics tightness: peak cycle supplier power +10–25%

- Mitigants: long‑term contracts, geographic proximity

- Risk control: diversified carriers

Skilled labor and forestry contractors

Technical operators and forestry contractors are scarce across Nordic markets, pushing wage pressure higher, while Holmen-style training pipelines and in-house capability reduce external reliance. Strong union frameworks, with union density around 65–70% in Sweden and Finland (2023–24), add predictability but constrain flexibility. Net effect is moderate supplier power driven by skill scarcity.

- Scarcity raises wages

- Training/in-house offsets reliance

- Union density ~65–70% (2023–24)

- Overall: moderate supplier power

1.3M ha integration cuts fiber power; chemicals keep pricing edge

Holmen’s 1.3M ha back‑integration reduces fiber supplier leverage but specialty chemicals (global market ~$800B in 2024) and OEMs retain pricing power. Energy volatility (Nord Pool ~45 EUR/MWh in 2024) and logistics tighten supplier influence; long‑term contracts mitigate. Skilled operators and unions (65–70% density) create moderate supplier power.

| Item | Metric |

|---|---|

| Owned forest | 1.3M ha |

| Chemicals market | $800B (2024) |

| Nord Pool | ~45 EUR/MWh (2024) |

| Union density | 65–70% (2023–24) |

What is included in the product

Concise Porter's Five Forces analysis for Holmen, examining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and entry barriers shaping its profitability.

A concise, one-sheet Holmen Porter’s Five Forces summary that maps supplier, buyer, rivalry, entry and substitute pressures—ideal for rapid strategic decisions and boardroom slides.

Customers Bargaining Power

Concentrated converters and brand owners

Large converters and FMCG brands buying significant volumes (Holmen reported net sales SEK 24.2bn in 2024) exercise strong bargaining power, insisting on consistent quality, FSC/PEFC credentials and transparent pricing; framework agreements and supplier qualification raise switching costs and focus negotiations on price and service levels, while Holmen’s premium board grades reduce pure price pressure by commanding quality premia.

Construction distributors and builders

Construction distributors and builders are highly price sensitive and cyclical, pushing margins down in downturns as substitution to other timber suppliers is feasible. Certifications and dimensional consistency provide some stickiness; Holmen’s ownership of about 430,000 hectares of productive forest and certified supply chains supports customer confidence. Regional proximity and reliable deliveries further strengthen Holmen’s position against buyer leverage.

Graphical paper customers shrinking

Declining print demand — global graphic paper consumption is down roughly 50% since 2000 — amplifies buyer leverage as installed capacity now exceeds needs, letting customers solicit competitive bids amid structural overcapacity. Grade-specific machine constraints limit immediate switching for some buyers, but Holmen faces pressure to differentiate through service, sustainability credentials and tailored product specs to preserve margins.

Sustainability and traceability demands

Buyers increasingly mandate FSC/PEFC certification, low-carbon energy and recyclability, creating compliance thresholds that strengthen their negotiation leverage. Holmen’s roughly 1.1 million hectares of certified forest and near‑100% renewable energy usage offset that leverage, lowering switching risk and supporting premium pricing. Compliance-driven procurement reduces churn and can justify higher margins.

Contract duration and indexation

Long-term, index-linked contracts in Holmen’s pulp and paper business provide buyers with price visibility while Holmen secures stable volumes; indexation typically references pulp, energy and freight to allocate cost swings across the chain. Effective clause design reduces buyer leverage in volatile markets by tying payments to objective market inputs, aligning risk rather than leaving it solely with Holmen or the customer.

- Holmen: Swedish pulp and paper producer

- Indexation anchors price risk to pulp/energy/freight

- Long-term contracts = volume stability

- Well-designed clauses dilute buyer power

Buyer pressure offset by premiums, FSC/PEFC and 1.1M ha certified forest

Large volume buyers (Holmen net sales SEK 24.2bn 2024) exert strong price and compliance pressure, but Holmen’s premium grades, FSC/PEFC credentials and index‑linked long contracts limit pure price erosion; near‑100% renewables and 1.1M ha certified forests lower switching risk while 50% decline in graphic paper since 2000 raises buyer leverage in that segment.

| Metric | Value |

|---|---|

| Net sales 2024 | SEK 24.2bn |

| Certified forest | ~1.1M ha |

| Owned productive forest | ~430k ha |

| Renewable energy | ~100% |

| Graphic paper demand decline | ~50% since 2000 |

What You See Is What You Get

Holmen Porter's Five Forces Analysis

This preview shows the exact Holmen Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the same professionally written, fully formatted analysis file, ready for download and immediate use. You're looking at the actual deliverable; once you buy, you get instant access to this exact document.

A Must-Have Tool for Decision-Makers

Holmen faces unique pressures from raw-material suppliers, cyclical demand for paper products and growing substitute threats, all shaping its strategic position in forest products and packaging markets. This brief snapshot highlights core competitive dynamics and key vulnerabilities. Unlock the full Porter's Five Forces Analysis to explore Holmen’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Back-integrated fiber reduces dependence

Holmen’s back-integrated model, anchored by roughly 1.3 million hectares of owned forest, internalizes a critical raw material and reduces supplier leverage on fiber, improving cost control and supply certainty versus peers dependent on external pulpwood. This integration shifts bargaining power toward Holmen, though supplier power remains for specialty inputs such as pulp additives where alternatives are limited.

Specialty chemicals and packaging additives

Resin, starch, bleaching agents and coating chemicals are often supplied by a concentrated global set of players; the global specialty chemicals market was roughly $800 billion in 2024, keeping market share and pricing power clustered. Switching costs for Holmen can be material due to qualification, quality variance and machine recalibration, raising supplier leverage. Multi-sourcing and long-term contracts (often 2–5 years) mitigate price risk. Innovation-led suppliers retaining unique chemistries exert moderate bargaining power.

Capital equipment and maintenance OEMs

Paperboard machines, sawmill lines and turbines are concentrated among a few OEMs (notably Valmet and Voith for paper, major turbine makers for power), creating high switching barriers; parts, upgrades and service lock-in sustain supplier influence. Lifecycle agreements commonly trade lower price for uptime guarantees of 98–99%. Holmen’s scale gives some countervailing negotiation leverage.

Energy, logistics, and freight providers

Despite Holmen's own hydro and wind output, Nord Pool day‑ahead averaged ~45 EUR/MWh in 2024, and episodic fuel and grid market swings still push costs; transport capacity and port slots can tighten in peak cycles, boosting logistics supplier leverage by roughly 10–25%. Long‑term rail and port contracts and close customer proximity mitigate spikes, and using multiple carriers reduces single‑provider exposure.

- Energy volatility: Nord Pool ~45 EUR/MWh (2024)

- Logistics tightness: peak cycle supplier power +10–25%

- Mitigants: long‑term contracts, geographic proximity

- Risk control: diversified carriers

Skilled labor and forestry contractors

Technical operators and forestry contractors are scarce across Nordic markets, pushing wage pressure higher, while Holmen-style training pipelines and in-house capability reduce external reliance. Strong union frameworks, with union density around 65–70% in Sweden and Finland (2023–24), add predictability but constrain flexibility. Net effect is moderate supplier power driven by skill scarcity.

- Scarcity raises wages

- Training/in-house offsets reliance

- Union density ~65–70% (2023–24)

- Overall: moderate supplier power

1.3M ha integration cuts fiber power; chemicals keep pricing edge

Holmen’s 1.3M ha back‑integration reduces fiber supplier leverage but specialty chemicals (global market ~$800B in 2024) and OEMs retain pricing power. Energy volatility (Nord Pool ~45 EUR/MWh in 2024) and logistics tighten supplier influence; long‑term contracts mitigate. Skilled operators and unions (65–70% density) create moderate supplier power.

| Item | Metric |

|---|---|

| Owned forest | 1.3M ha |

| Chemicals market | $800B (2024) |

| Nord Pool | ~45 EUR/MWh (2024) |

| Union density | 65–70% (2023–24) |

What is included in the product

Concise Porter's Five Forces analysis for Holmen, examining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and entry barriers shaping its profitability.

A concise, one-sheet Holmen Porter’s Five Forces summary that maps supplier, buyer, rivalry, entry and substitute pressures—ideal for rapid strategic decisions and boardroom slides.

Customers Bargaining Power

Concentrated converters and brand owners

Large converters and FMCG brands buying significant volumes (Holmen reported net sales SEK 24.2bn in 2024) exercise strong bargaining power, insisting on consistent quality, FSC/PEFC credentials and transparent pricing; framework agreements and supplier qualification raise switching costs and focus negotiations on price and service levels, while Holmen’s premium board grades reduce pure price pressure by commanding quality premia.

Construction distributors and builders

Construction distributors and builders are highly price sensitive and cyclical, pushing margins down in downturns as substitution to other timber suppliers is feasible. Certifications and dimensional consistency provide some stickiness; Holmen’s ownership of about 430,000 hectares of productive forest and certified supply chains supports customer confidence. Regional proximity and reliable deliveries further strengthen Holmen’s position against buyer leverage.

Graphical paper customers shrinking

Declining print demand — global graphic paper consumption is down roughly 50% since 2000 — amplifies buyer leverage as installed capacity now exceeds needs, letting customers solicit competitive bids amid structural overcapacity. Grade-specific machine constraints limit immediate switching for some buyers, but Holmen faces pressure to differentiate through service, sustainability credentials and tailored product specs to preserve margins.

Sustainability and traceability demands

Buyers increasingly mandate FSC/PEFC certification, low-carbon energy and recyclability, creating compliance thresholds that strengthen their negotiation leverage. Holmen’s roughly 1.1 million hectares of certified forest and near‑100% renewable energy usage offset that leverage, lowering switching risk and supporting premium pricing. Compliance-driven procurement reduces churn and can justify higher margins.

Contract duration and indexation

Long-term, index-linked contracts in Holmen’s pulp and paper business provide buyers with price visibility while Holmen secures stable volumes; indexation typically references pulp, energy and freight to allocate cost swings across the chain. Effective clause design reduces buyer leverage in volatile markets by tying payments to objective market inputs, aligning risk rather than leaving it solely with Holmen or the customer.

- Holmen: Swedish pulp and paper producer

- Indexation anchors price risk to pulp/energy/freight

- Long-term contracts = volume stability

- Well-designed clauses dilute buyer power

Buyer pressure offset by premiums, FSC/PEFC and 1.1M ha certified forest

Large volume buyers (Holmen net sales SEK 24.2bn 2024) exert strong price and compliance pressure, but Holmen’s premium grades, FSC/PEFC credentials and index‑linked long contracts limit pure price erosion; near‑100% renewables and 1.1M ha certified forests lower switching risk while 50% decline in graphic paper since 2000 raises buyer leverage in that segment.

| Metric | Value |

|---|---|

| Net sales 2024 | SEK 24.2bn |

| Certified forest | ~1.1M ha |

| Owned productive forest | ~430k ha |

| Renewable energy | ~100% |

| Graphic paper demand decline | ~50% since 2000 |

What You See Is What You Get

Holmen Porter's Five Forces Analysis

This preview shows the exact Holmen Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the same professionally written, fully formatted analysis file, ready for download and immediate use. You're looking at the actual deliverable; once you buy, you get instant access to this exact document.

Description

A Must-Have Tool for Decision-Makers

Holmen faces unique pressures from raw-material suppliers, cyclical demand for paper products and growing substitute threats, all shaping its strategic position in forest products and packaging markets. This brief snapshot highlights core competitive dynamics and key vulnerabilities. Unlock the full Porter's Five Forces Analysis to explore Holmen’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Back-integrated fiber reduces dependence

Holmen’s back-integrated model, anchored by roughly 1.3 million hectares of owned forest, internalizes a critical raw material and reduces supplier leverage on fiber, improving cost control and supply certainty versus peers dependent on external pulpwood. This integration shifts bargaining power toward Holmen, though supplier power remains for specialty inputs such as pulp additives where alternatives are limited.

Specialty chemicals and packaging additives

Resin, starch, bleaching agents and coating chemicals are often supplied by a concentrated global set of players; the global specialty chemicals market was roughly $800 billion in 2024, keeping market share and pricing power clustered. Switching costs for Holmen can be material due to qualification, quality variance and machine recalibration, raising supplier leverage. Multi-sourcing and long-term contracts (often 2–5 years) mitigate price risk. Innovation-led suppliers retaining unique chemistries exert moderate bargaining power.

Capital equipment and maintenance OEMs

Paperboard machines, sawmill lines and turbines are concentrated among a few OEMs (notably Valmet and Voith for paper, major turbine makers for power), creating high switching barriers; parts, upgrades and service lock-in sustain supplier influence. Lifecycle agreements commonly trade lower price for uptime guarantees of 98–99%. Holmen’s scale gives some countervailing negotiation leverage.

Energy, logistics, and freight providers

Despite Holmen's own hydro and wind output, Nord Pool day‑ahead averaged ~45 EUR/MWh in 2024, and episodic fuel and grid market swings still push costs; transport capacity and port slots can tighten in peak cycles, boosting logistics supplier leverage by roughly 10–25%. Long‑term rail and port contracts and close customer proximity mitigate spikes, and using multiple carriers reduces single‑provider exposure.

- Energy volatility: Nord Pool ~45 EUR/MWh (2024)

- Logistics tightness: peak cycle supplier power +10–25%

- Mitigants: long‑term contracts, geographic proximity

- Risk control: diversified carriers

Skilled labor and forestry contractors

Technical operators and forestry contractors are scarce across Nordic markets, pushing wage pressure higher, while Holmen-style training pipelines and in-house capability reduce external reliance. Strong union frameworks, with union density around 65–70% in Sweden and Finland (2023–24), add predictability but constrain flexibility. Net effect is moderate supplier power driven by skill scarcity.

- Scarcity raises wages

- Training/in-house offsets reliance

- Union density ~65–70% (2023–24)

- Overall: moderate supplier power

1.3M ha integration cuts fiber power; chemicals keep pricing edge

Holmen’s 1.3M ha back‑integration reduces fiber supplier leverage but specialty chemicals (global market ~$800B in 2024) and OEMs retain pricing power. Energy volatility (Nord Pool ~45 EUR/MWh in 2024) and logistics tighten supplier influence; long‑term contracts mitigate. Skilled operators and unions (65–70% density) create moderate supplier power.

| Item | Metric |

|---|---|

| Owned forest | 1.3M ha |

| Chemicals market | $800B (2024) |

| Nord Pool | ~45 EUR/MWh (2024) |

| Union density | 65–70% (2023–24) |

What is included in the product

Concise Porter's Five Forces analysis for Holmen, examining competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifying disruptive forces and entry barriers shaping its profitability.

A concise, one-sheet Holmen Porter’s Five Forces summary that maps supplier, buyer, rivalry, entry and substitute pressures—ideal for rapid strategic decisions and boardroom slides.

Customers Bargaining Power

Concentrated converters and brand owners

Large converters and FMCG brands buying significant volumes (Holmen reported net sales SEK 24.2bn in 2024) exercise strong bargaining power, insisting on consistent quality, FSC/PEFC credentials and transparent pricing; framework agreements and supplier qualification raise switching costs and focus negotiations on price and service levels, while Holmen’s premium board grades reduce pure price pressure by commanding quality premia.

Construction distributors and builders

Construction distributors and builders are highly price sensitive and cyclical, pushing margins down in downturns as substitution to other timber suppliers is feasible. Certifications and dimensional consistency provide some stickiness; Holmen’s ownership of about 430,000 hectares of productive forest and certified supply chains supports customer confidence. Regional proximity and reliable deliveries further strengthen Holmen’s position against buyer leverage.

Graphical paper customers shrinking

Declining print demand — global graphic paper consumption is down roughly 50% since 2000 — amplifies buyer leverage as installed capacity now exceeds needs, letting customers solicit competitive bids amid structural overcapacity. Grade-specific machine constraints limit immediate switching for some buyers, but Holmen faces pressure to differentiate through service, sustainability credentials and tailored product specs to preserve margins.

Sustainability and traceability demands

Buyers increasingly mandate FSC/PEFC certification, low-carbon energy and recyclability, creating compliance thresholds that strengthen their negotiation leverage. Holmen’s roughly 1.1 million hectares of certified forest and near‑100% renewable energy usage offset that leverage, lowering switching risk and supporting premium pricing. Compliance-driven procurement reduces churn and can justify higher margins.

Contract duration and indexation

Long-term, index-linked contracts in Holmen’s pulp and paper business provide buyers with price visibility while Holmen secures stable volumes; indexation typically references pulp, energy and freight to allocate cost swings across the chain. Effective clause design reduces buyer leverage in volatile markets by tying payments to objective market inputs, aligning risk rather than leaving it solely with Holmen or the customer.

- Holmen: Swedish pulp and paper producer

- Indexation anchors price risk to pulp/energy/freight

- Long-term contracts = volume stability

- Well-designed clauses dilute buyer power

Buyer pressure offset by premiums, FSC/PEFC and 1.1M ha certified forest

Large volume buyers (Holmen net sales SEK 24.2bn 2024) exert strong price and compliance pressure, but Holmen’s premium grades, FSC/PEFC credentials and index‑linked long contracts limit pure price erosion; near‑100% renewables and 1.1M ha certified forests lower switching risk while 50% decline in graphic paper since 2000 raises buyer leverage in that segment.

| Metric | Value |

|---|---|

| Net sales 2024 | SEK 24.2bn |

| Certified forest | ~1.1M ha |

| Owned productive forest | ~430k ha |

| Renewable energy | ~100% |

| Graphic paper demand decline | ~50% since 2000 |

What You See Is What You Get

Holmen Porter's Five Forces Analysis

This preview shows the exact Holmen Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed is the same professionally written, fully formatted analysis file, ready for download and immediate use. You're looking at the actual deliverable; once you buy, you get instant access to this exact document.