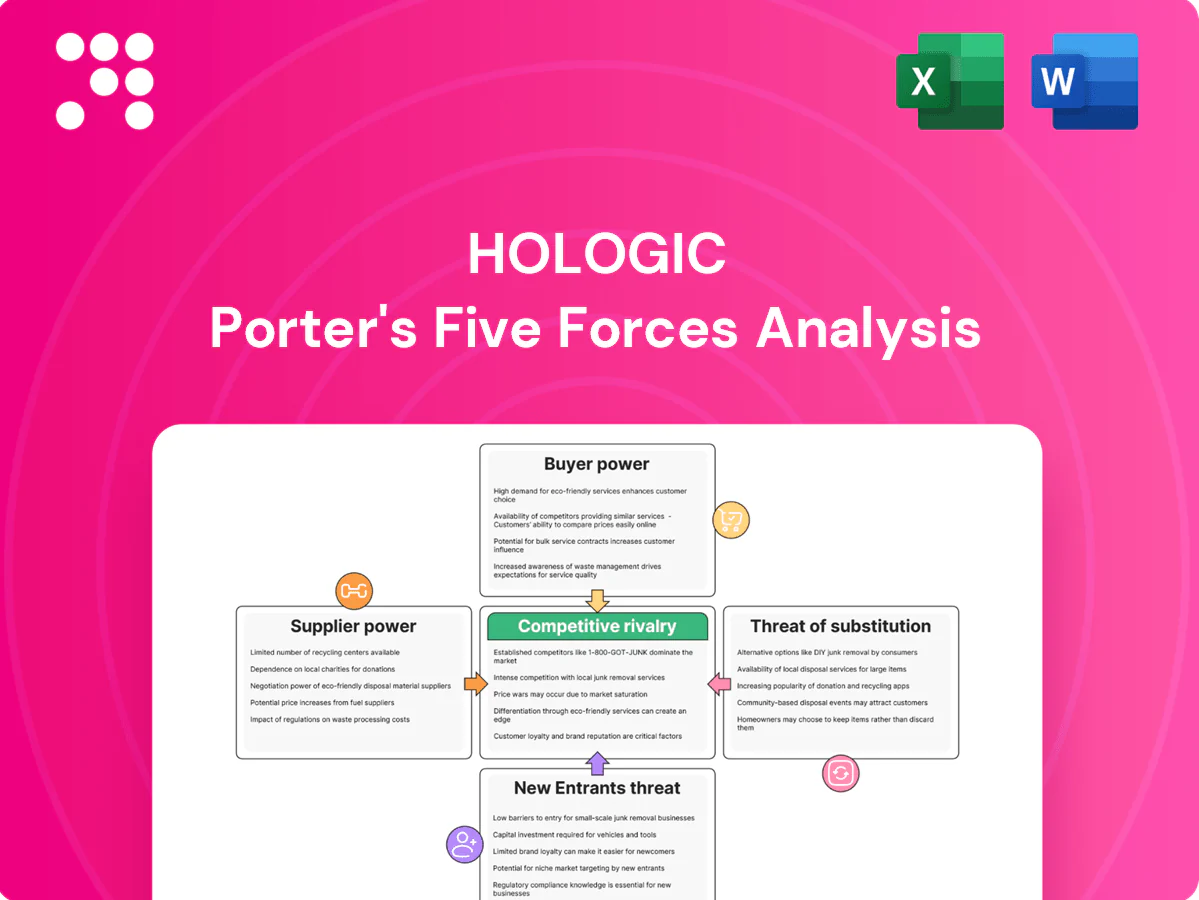

Hologic Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Hologic operates in a competitive medical diagnostics market where supplier consolidation, rapid tech change and regulatory scrutiny shape margins. Buyer negotiation, reimbursement pressure and threat of substitutes from integrated platforms heighten strategic risk, while its R&D and installed base provide defensible advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hologic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components and reagents

Imaging systems require precision optics, detectors and X-ray tubes sourced from a small set of specialized vendors, increasing supplier leverage. Diagnostics depend on enzymes, antibodies and oligos with tight quality specs and few qualified sources, so any supply hiccup can halt assays or device production. Dual-sourcing is feasible but time-consuming due to lengthy validation and regulatory requalification.

Regulatory-grade quality constraints

Materials for Hologic products must meet FDA, ISO 13485, and GMP standards, which narrows the pool of approved suppliers and raises entry barriers. Switching suppliers typically triggers revalidation and possible regulatory filings, materially increasing switching costs and time-to-market. This regulatory lock-in strengthens incumbent suppliers’ negotiating leverage. Long-term agreements can reduce but not eliminate that supplier power.

Capacity and lead-time risk

Global shocks pushed semiconductor lead times to over 20 weeks in 2021–22, stressing supply of chips, plastics and sterile disposables; many diagnostics reagents carry 6–12 month shelf lives, limiting stockpiling. Sudden test demand spikes can rapidly exhaust reagent inventories, while scarce suppliers often prioritize higher‑margin customers, leaving firms like Hologic exposed to capacity and lead‑time risk.

Proprietary subsystems and software

Proprietary subsystems and firmware in Hologic equipment embed vendor dependence, with custom tooling and calibration raising practical switching friction; Hologic reported FY2024 revenue of about $3.95 billion, reflecting pricing power in durable capital segments. Interoperability standards are improving but not universal in medtech, so suppliers can enforce price firmness and strict service terms. This raises supplier bargaining power and limits buyer leverage.

- Vendor lock-in: proprietary firmware

- Switching friction: custom tooling/calibration

- Standards gap: partial interoperability

- Commercial impact: price firmness, strict service terms

Countervailing scale and partnerships

Hologic’s scale in women’s health—reporting roughly $4.5B in fiscal 2024 revenue—gives it purchasing clout and forecasting credibility with suppliers; strategic co-development deals secure allocations and pricing. Supplier scorecards and diversification programs reduce single-point failure, while vertical integration remains selective due to capital intensity and complexity.

- Scale: $4.5B (FY2024)

- Co-development: allocation/pricing leverage

- Risk: supplier diversification

- Vertical integration: selective

Narrow supplier base and >20-week chip delays heighten reagent and switching risk despite $3.95B

Supplier base is narrow for optics, chips and reagents, giving vendors measurable leverage; regulatory revalidation and custom firmware raise switching costs and time-to-market. Semiconductor lead times spiked over 20 weeks (2021–22) and many reagents have 6–12 month shelf lives, limiting stockpiling. Hologic reported FY2024 revenue of about $3.95 billion, which aids negotiation but does not eliminate supplier risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.95B |

| Chip lead times (2021–22) | >20 weeks |

| Reagent shelf life | 6–12 months |

| Switching impact | Regulatory revalidation (months) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hologic; analyzes supplier and buyer power, substitutes, rivalry, and barriers to entry, highlighting disruptive threats and strategic levers.

Clear, one-sheet Porter's Five Forces tailored to Hologic—instantly highlights supplier, buyer, competitive and regulatory pressures to speed strategic decisions and reduce analysis friction.

Customers Bargaining Power

Consolidated buyers and GPOs

IDNs, hospital chains, reference labs and GPOs—which account for over 90% of U.S. hospital purchasing—aggregate demand and negotiate aggressively, forcing discounts, rebates and service-included contracts. National tenders outside the U.S. intensify price pressure, often compressing bids by double digits. Multiyear frameworks lock in lower pricing while giving suppliers predictable volume visibility.

High switching costs from installed base

Imaging and diagnostic platforms create strong lock-in as trained staff, integrated workflows and multi-year service contracts raise practical switching costs; Hologic reported fiscal 2024 revenue near $4.6 billion, driven largely by recurring consumables and assays. Consumable assay menus reinforce recurring usage, often representing the majority of diagnostic revenue and margins. Switching platforms forces retraining, downtime and revalidation that can take weeks to months, reducing buyer power post-install. Competitive trade-in programs can recover some spend but rarely erase integration barriers.

Clinical performance and reimbursement sensitivity

Buyers prioritize sensitivity, specificity and guideline alignment over price when evaluating Hologic's diagnostic platforms, especially given Hologic's FY2024 revenue of about $4.1 billion which ties commercial success to clinical performance. Reimbursement rates and CPT coding drive hospital purchasing thresholds and utilization, with CMS payment policies materially affecting volume. If reimbursements tighten, purchasers press for lower prices or delay upgrades, but robust peer-reviewed clinical data limits concessions by defending value.

Total cost of ownership focus

Providers now focus on total cost of ownership, demanding ≈99% uptime, fast service responsiveness and low consumable cost per test; predictable SLAs and remote diagnostics let Hologic and peers command premiums by reducing downtime and repeat visits.

- Uptime: ≈99% expected

- Remote diagnostics: lowers onsite service time

- Bundled pricing: reduces perceived per-test cost

- Poor service: triggers rapid renegotiation

Alternative sourcing options

In diagnostics, large labs such as LabCorp and Quest Diagnostics, each with revenues above $10 billion in 2024, routinely multi-source across platforms to hedge supply and technology risk, increasing buyer leverage. Imaging purchasers solicit head-to-head bids from major OEMs, driving competitive procurement and price/terms pressure. Unique assays and differentiated imaging features, however, limit substitutability and preserve supplier margins.

IDN/GPO tenders pressure prices; consumables and $4.1B diagnostics sustain pricing power

IDNs, GPOs and large labs (LabCorp, Quest >$10B 2024) exert strong price pressure via tenders and multi-year contracts, but Hologic’s FY2024 revenue (~$4.6B total, diagnostics ~$4.1B) and consumable-led margins create lock-in through high switching costs, SLAs (~99% uptime) and clinical differentiation that preserve pricing power.

| Metric | 2024 |

|---|---|

| Hologic revenue | $4.6B total; $4.1B diagnostics |

| LabCorp/Quest | >$10B each |

| Uptime | ≈99% |

Same Document Delivered

Hologic Porter's Five Forces Analysis

This preview shows the exact Hologic Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted. The report delivers a detailed assessment of supplier power, buyer power, threat of new entrants, substitutes, and competitive rivalry with data-driven insights specific to Hologic’s medtech position. You’ll get this same ready-to-use file instantly upon payment.

Don't Miss the Bigger Picture

Hologic operates in a competitive medical diagnostics market where supplier consolidation, rapid tech change and regulatory scrutiny shape margins. Buyer negotiation, reimbursement pressure and threat of substitutes from integrated platforms heighten strategic risk, while its R&D and installed base provide defensible advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hologic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components and reagents

Imaging systems require precision optics, detectors and X-ray tubes sourced from a small set of specialized vendors, increasing supplier leverage. Diagnostics depend on enzymes, antibodies and oligos with tight quality specs and few qualified sources, so any supply hiccup can halt assays or device production. Dual-sourcing is feasible but time-consuming due to lengthy validation and regulatory requalification.

Regulatory-grade quality constraints

Materials for Hologic products must meet FDA, ISO 13485, and GMP standards, which narrows the pool of approved suppliers and raises entry barriers. Switching suppliers typically triggers revalidation and possible regulatory filings, materially increasing switching costs and time-to-market. This regulatory lock-in strengthens incumbent suppliers’ negotiating leverage. Long-term agreements can reduce but not eliminate that supplier power.

Capacity and lead-time risk

Global shocks pushed semiconductor lead times to over 20 weeks in 2021–22, stressing supply of chips, plastics and sterile disposables; many diagnostics reagents carry 6–12 month shelf lives, limiting stockpiling. Sudden test demand spikes can rapidly exhaust reagent inventories, while scarce suppliers often prioritize higher‑margin customers, leaving firms like Hologic exposed to capacity and lead‑time risk.

Proprietary subsystems and software

Proprietary subsystems and firmware in Hologic equipment embed vendor dependence, with custom tooling and calibration raising practical switching friction; Hologic reported FY2024 revenue of about $3.95 billion, reflecting pricing power in durable capital segments. Interoperability standards are improving but not universal in medtech, so suppliers can enforce price firmness and strict service terms. This raises supplier bargaining power and limits buyer leverage.

- Vendor lock-in: proprietary firmware

- Switching friction: custom tooling/calibration

- Standards gap: partial interoperability

- Commercial impact: price firmness, strict service terms

Countervailing scale and partnerships

Hologic’s scale in women’s health—reporting roughly $4.5B in fiscal 2024 revenue—gives it purchasing clout and forecasting credibility with suppliers; strategic co-development deals secure allocations and pricing. Supplier scorecards and diversification programs reduce single-point failure, while vertical integration remains selective due to capital intensity and complexity.

- Scale: $4.5B (FY2024)

- Co-development: allocation/pricing leverage

- Risk: supplier diversification

- Vertical integration: selective

Narrow supplier base and >20-week chip delays heighten reagent and switching risk despite $3.95B

Supplier base is narrow for optics, chips and reagents, giving vendors measurable leverage; regulatory revalidation and custom firmware raise switching costs and time-to-market. Semiconductor lead times spiked over 20 weeks (2021–22) and many reagents have 6–12 month shelf lives, limiting stockpiling. Hologic reported FY2024 revenue of about $3.95 billion, which aids negotiation but does not eliminate supplier risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.95B |

| Chip lead times (2021–22) | >20 weeks |

| Reagent shelf life | 6–12 months |

| Switching impact | Regulatory revalidation (months) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hologic; analyzes supplier and buyer power, substitutes, rivalry, and barriers to entry, highlighting disruptive threats and strategic levers.

Clear, one-sheet Porter's Five Forces tailored to Hologic—instantly highlights supplier, buyer, competitive and regulatory pressures to speed strategic decisions and reduce analysis friction.

Customers Bargaining Power

Consolidated buyers and GPOs

IDNs, hospital chains, reference labs and GPOs—which account for over 90% of U.S. hospital purchasing—aggregate demand and negotiate aggressively, forcing discounts, rebates and service-included contracts. National tenders outside the U.S. intensify price pressure, often compressing bids by double digits. Multiyear frameworks lock in lower pricing while giving suppliers predictable volume visibility.

High switching costs from installed base

Imaging and diagnostic platforms create strong lock-in as trained staff, integrated workflows and multi-year service contracts raise practical switching costs; Hologic reported fiscal 2024 revenue near $4.6 billion, driven largely by recurring consumables and assays. Consumable assay menus reinforce recurring usage, often representing the majority of diagnostic revenue and margins. Switching platforms forces retraining, downtime and revalidation that can take weeks to months, reducing buyer power post-install. Competitive trade-in programs can recover some spend but rarely erase integration barriers.

Clinical performance and reimbursement sensitivity

Buyers prioritize sensitivity, specificity and guideline alignment over price when evaluating Hologic's diagnostic platforms, especially given Hologic's FY2024 revenue of about $4.1 billion which ties commercial success to clinical performance. Reimbursement rates and CPT coding drive hospital purchasing thresholds and utilization, with CMS payment policies materially affecting volume. If reimbursements tighten, purchasers press for lower prices or delay upgrades, but robust peer-reviewed clinical data limits concessions by defending value.

Total cost of ownership focus

Providers now focus on total cost of ownership, demanding ≈99% uptime, fast service responsiveness and low consumable cost per test; predictable SLAs and remote diagnostics let Hologic and peers command premiums by reducing downtime and repeat visits.

- Uptime: ≈99% expected

- Remote diagnostics: lowers onsite service time

- Bundled pricing: reduces perceived per-test cost

- Poor service: triggers rapid renegotiation

Alternative sourcing options

In diagnostics, large labs such as LabCorp and Quest Diagnostics, each with revenues above $10 billion in 2024, routinely multi-source across platforms to hedge supply and technology risk, increasing buyer leverage. Imaging purchasers solicit head-to-head bids from major OEMs, driving competitive procurement and price/terms pressure. Unique assays and differentiated imaging features, however, limit substitutability and preserve supplier margins.

IDN/GPO tenders pressure prices; consumables and $4.1B diagnostics sustain pricing power

IDNs, GPOs and large labs (LabCorp, Quest >$10B 2024) exert strong price pressure via tenders and multi-year contracts, but Hologic’s FY2024 revenue (~$4.6B total, diagnostics ~$4.1B) and consumable-led margins create lock-in through high switching costs, SLAs (~99% uptime) and clinical differentiation that preserve pricing power.

| Metric | 2024 |

|---|---|

| Hologic revenue | $4.6B total; $4.1B diagnostics |

| LabCorp/Quest | >$10B each |

| Uptime | ≈99% |

Same Document Delivered

Hologic Porter's Five Forces Analysis

This preview shows the exact Hologic Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted. The report delivers a detailed assessment of supplier power, buyer power, threat of new entrants, substitutes, and competitive rivalry with data-driven insights specific to Hologic’s medtech position. You’ll get this same ready-to-use file instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Hologic operates in a competitive medical diagnostics market where supplier consolidation, rapid tech change and regulatory scrutiny shape margins. Buyer negotiation, reimbursement pressure and threat of substitutes from integrated platforms heighten strategic risk, while its R&D and installed base provide defensible advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hologic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized components and reagents

Imaging systems require precision optics, detectors and X-ray tubes sourced from a small set of specialized vendors, increasing supplier leverage. Diagnostics depend on enzymes, antibodies and oligos with tight quality specs and few qualified sources, so any supply hiccup can halt assays or device production. Dual-sourcing is feasible but time-consuming due to lengthy validation and regulatory requalification.

Regulatory-grade quality constraints

Materials for Hologic products must meet FDA, ISO 13485, and GMP standards, which narrows the pool of approved suppliers and raises entry barriers. Switching suppliers typically triggers revalidation and possible regulatory filings, materially increasing switching costs and time-to-market. This regulatory lock-in strengthens incumbent suppliers’ negotiating leverage. Long-term agreements can reduce but not eliminate that supplier power.

Capacity and lead-time risk

Global shocks pushed semiconductor lead times to over 20 weeks in 2021–22, stressing supply of chips, plastics and sterile disposables; many diagnostics reagents carry 6–12 month shelf lives, limiting stockpiling. Sudden test demand spikes can rapidly exhaust reagent inventories, while scarce suppliers often prioritize higher‑margin customers, leaving firms like Hologic exposed to capacity and lead‑time risk.

Proprietary subsystems and software

Proprietary subsystems and firmware in Hologic equipment embed vendor dependence, with custom tooling and calibration raising practical switching friction; Hologic reported FY2024 revenue of about $3.95 billion, reflecting pricing power in durable capital segments. Interoperability standards are improving but not universal in medtech, so suppliers can enforce price firmness and strict service terms. This raises supplier bargaining power and limits buyer leverage.

- Vendor lock-in: proprietary firmware

- Switching friction: custom tooling/calibration

- Standards gap: partial interoperability

- Commercial impact: price firmness, strict service terms

Countervailing scale and partnerships

Hologic’s scale in women’s health—reporting roughly $4.5B in fiscal 2024 revenue—gives it purchasing clout and forecasting credibility with suppliers; strategic co-development deals secure allocations and pricing. Supplier scorecards and diversification programs reduce single-point failure, while vertical integration remains selective due to capital intensity and complexity.

- Scale: $4.5B (FY2024)

- Co-development: allocation/pricing leverage

- Risk: supplier diversification

- Vertical integration: selective

Narrow supplier base and >20-week chip delays heighten reagent and switching risk despite $3.95B

Supplier base is narrow for optics, chips and reagents, giving vendors measurable leverage; regulatory revalidation and custom firmware raise switching costs and time-to-market. Semiconductor lead times spiked over 20 weeks (2021–22) and many reagents have 6–12 month shelf lives, limiting stockpiling. Hologic reported FY2024 revenue of about $3.95 billion, which aids negotiation but does not eliminate supplier risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $3.95B |

| Chip lead times (2021–22) | >20 weeks |

| Reagent shelf life | 6–12 months |

| Switching impact | Regulatory revalidation (months) |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Hologic; analyzes supplier and buyer power, substitutes, rivalry, and barriers to entry, highlighting disruptive threats and strategic levers.

Clear, one-sheet Porter's Five Forces tailored to Hologic—instantly highlights supplier, buyer, competitive and regulatory pressures to speed strategic decisions and reduce analysis friction.

Customers Bargaining Power

Consolidated buyers and GPOs

IDNs, hospital chains, reference labs and GPOs—which account for over 90% of U.S. hospital purchasing—aggregate demand and negotiate aggressively, forcing discounts, rebates and service-included contracts. National tenders outside the U.S. intensify price pressure, often compressing bids by double digits. Multiyear frameworks lock in lower pricing while giving suppliers predictable volume visibility.

High switching costs from installed base

Imaging and diagnostic platforms create strong lock-in as trained staff, integrated workflows and multi-year service contracts raise practical switching costs; Hologic reported fiscal 2024 revenue near $4.6 billion, driven largely by recurring consumables and assays. Consumable assay menus reinforce recurring usage, often representing the majority of diagnostic revenue and margins. Switching platforms forces retraining, downtime and revalidation that can take weeks to months, reducing buyer power post-install. Competitive trade-in programs can recover some spend but rarely erase integration barriers.

Clinical performance and reimbursement sensitivity

Buyers prioritize sensitivity, specificity and guideline alignment over price when evaluating Hologic's diagnostic platforms, especially given Hologic's FY2024 revenue of about $4.1 billion which ties commercial success to clinical performance. Reimbursement rates and CPT coding drive hospital purchasing thresholds and utilization, with CMS payment policies materially affecting volume. If reimbursements tighten, purchasers press for lower prices or delay upgrades, but robust peer-reviewed clinical data limits concessions by defending value.

Total cost of ownership focus

Providers now focus on total cost of ownership, demanding ≈99% uptime, fast service responsiveness and low consumable cost per test; predictable SLAs and remote diagnostics let Hologic and peers command premiums by reducing downtime and repeat visits.

- Uptime: ≈99% expected

- Remote diagnostics: lowers onsite service time

- Bundled pricing: reduces perceived per-test cost

- Poor service: triggers rapid renegotiation

Alternative sourcing options

In diagnostics, large labs such as LabCorp and Quest Diagnostics, each with revenues above $10 billion in 2024, routinely multi-source across platforms to hedge supply and technology risk, increasing buyer leverage. Imaging purchasers solicit head-to-head bids from major OEMs, driving competitive procurement and price/terms pressure. Unique assays and differentiated imaging features, however, limit substitutability and preserve supplier margins.

IDN/GPO tenders pressure prices; consumables and $4.1B diagnostics sustain pricing power

IDNs, GPOs and large labs (LabCorp, Quest >$10B 2024) exert strong price pressure via tenders and multi-year contracts, but Hologic’s FY2024 revenue (~$4.6B total, diagnostics ~$4.1B) and consumable-led margins create lock-in through high switching costs, SLAs (~99% uptime) and clinical differentiation that preserve pricing power.

| Metric | 2024 |

|---|---|

| Hologic revenue | $4.6B total; $4.1B diagnostics |

| LabCorp/Quest | >$10B each |

| Uptime | ≈99% |

Same Document Delivered

Hologic Porter's Five Forces Analysis

This preview shows the exact Hologic Porter’s Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted. The report delivers a detailed assessment of supplier power, buyer power, threat of new entrants, substitutes, and competitive rivalry with data-driven insights specific to Hologic’s medtech position. You’ll get this same ready-to-use file instantly upon payment.