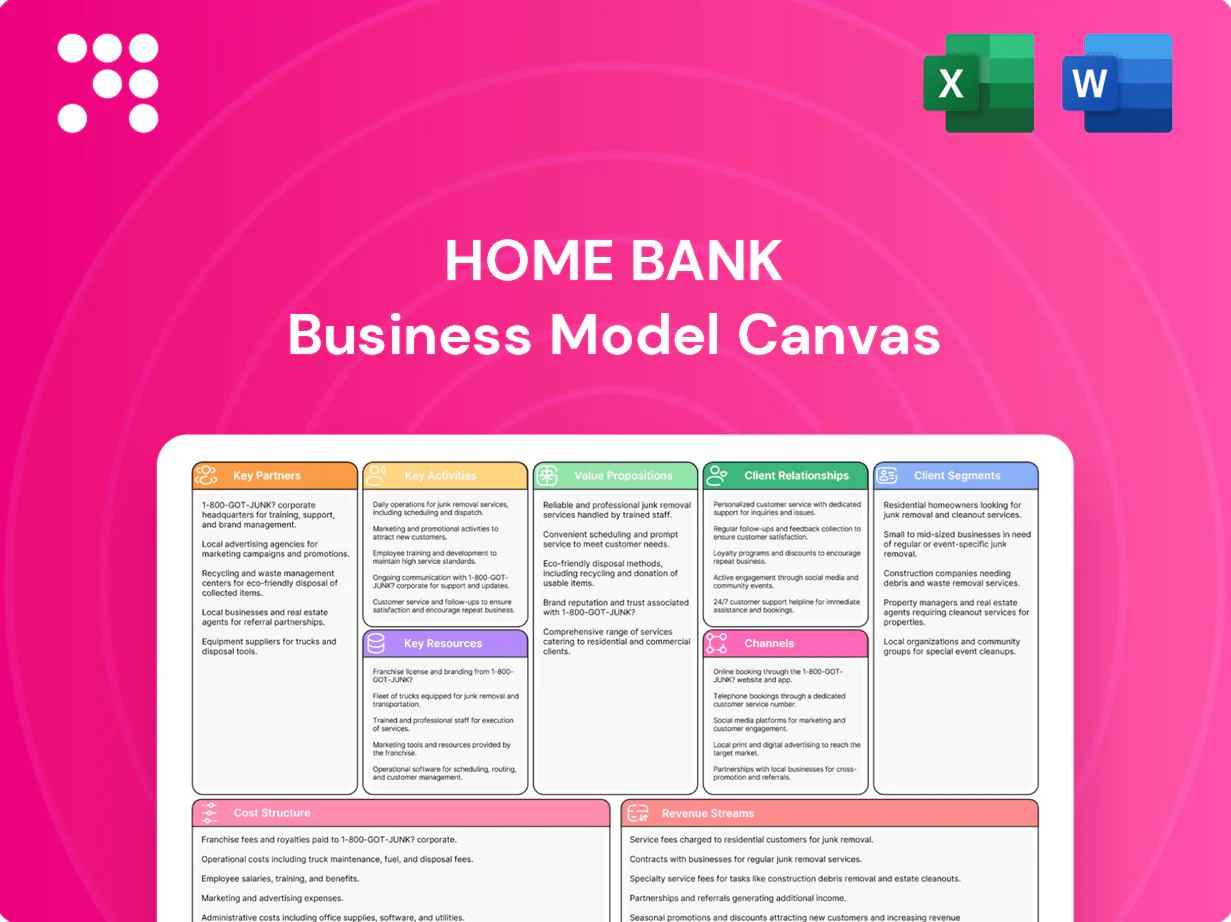

Home Bank Business Model Canvas

Retail Bank Business Model Canvas: Strategic Blueprint and Editable Download

Unlock the full strategic blueprint behind Home Bank’s business model. This concise Business Model Canvas maps customer segments, value propositions, key partners and revenue streams to show how the bank scales profitably. Ideal for investors, strategists and founders—download the editable Word/Excel canvas for actionable insights.

Partnerships

Correspondent banks

Partner with regional and national correspondent banks for liquidity, syndications, and treasury services to scale deal size and speed settlements. These relationships enable larger credits and faster settlements and provide access to specialized products not built in-house. This supports balance-sheet flexibility across Arkansas, Florida, Alabama, and Texas (4 states).

Fintech providers

Fintech providers supply core banking, digital banking, fraud detection, and data analytics modules that accelerate feature rollouts and reduce time-to-market, with SLA targets commonly set at 99.9% uptime. Partnerships improve security and UX across mobile and online channels while enabling rapid A/B testing and incremental launches. In 2024 many banks prioritized API-first fintech integrations to shorten deployment cycles and maintain regulatory compliance. Vendor SLAs and compliance clauses help manage uptime, incident response, and auditability.

Payment networks

Home Bank partners with Visa and Mastercard plus ACH and The Clearing House RTP (launched 2017) to enable card issuing, merchant services and instant transfers; card interchange typically ranges about 1–3% per transaction and RTP delivers real‑time settlement. These partnerships expand fee revenue via interchange and treasury services while improving client convenience and stickiness through instant payments.

Real estate ecosystem

Home Bank partners with developers, brokers, title firms and appraisers to streamline commercial real estate lending and construction draws, improving pipeline visibility and underwriting accuracy. These integrations enable faster credit decisions and tighter risk controls. U.S. commercial real estate mortgage debt outstanding was roughly 4 trillion dollars in 2024, highlighting market scale.

- Developer + Broker integrations

- Title & appraiser workflows

- Faster draws, better underwriting

- Local market intelligence in core states

Regulatory and insurance

Coordinate with regulators, auditors, and FDIC insurance partners to ensure safety, soundness, and policy adherence; FDIC insures deposits up to 250,000 and Basel III CET1 minimum is 4.5% with a 2.5% conservation buffer (total 7%) in 2024. This partnership strengthens risk management and reporting discipline and builds depositor trust and institutional credibility.

- Regulatory coordination: CET1 min 4.5% + 2.5% buffer

- Insurance: FDIC coverage 250,000 per depositor

- Controls: enhanced audit and reporting cadence

Partner banks, fintechs, and payment partners speed liquidity, 99.9% SLA and real-time settlement

Partner banks provide liquidity and syndications for larger credits across AR, FL, AL, TX; correspondent lines increase settlement speed. Fintechs (API‑first) supply core, fraud, analytics with 99.9% SLA targets. Card/ACH/RTP partners drive interchange (1–3%) and real‑time settlement; CRE ecosystem partners speed underwriting.

| Partner | Role | 2024 Metric |

|---|---|---|

| Correspondents | Liquidity | Lines supporting $bn deals |

| Fintechs | Digital core | 99.9% SLA |

What is included in the product

A concise, pre-written Business Model Canvas for Home Bank covering customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks. Designed for presentations and funding discussions, it includes narratives, competitive advantages and linked SWOT insights to support strategic decisions and validation using real-world bank operations.

High-level view of Home Bank’s business model with editable cells, relieving the pain of fragmented strategy documents and siloed insights. Shareable and editable for team collaboration and quick scenario testing to speed decisions and board-ready deliverables.

Activities

Deposit gathering

Attract and retain low-cost deposits via branches and digital channels to keep retail deposits as the core funding source (typically >50% of liabilities) and capture rising digital flows. Optimize mix across retail, business and public funds to enhance stability while meeting Basel III LCR >=100%. Price dynamically—with market rates around 5.25–5.50% in mid-2024—to manage deposit betas and liquidity. Support loan growth and funding stability through diversified, low-cost funding.

Lending operations

Originate diversified C&I, CRE, construction, and consumer loans with disciplined underwriting and collateral management, targeting 5–8% portfolio CAGR in core markets to match 2024 industry growth trends.

Monitor portfolios with covenant tracking, sector concentration limits, and stress-testing; aim to keep nonperforming assets below 1.0% and net charge-offs near 0.25% as benchmarked by peer community banks in 2024.

Drive prudent growth in target markets through calibrated pricing, relationship lending, and regional CRE underwriting, aligning new originations with regulatory liquidity and capital metrics recorded in 2024.

Risk & compliance

Manage credit, interest-rate, liquidity and operational risks to meet regulatory minima under Basel III (CET1 minimum 4.5%) and maintain an LCR at or above the 100% regulatory floor; target NPLs well below 1% for retail portfolios. Maintain AML/BSA, KYC and fair lending programs with timely SARs and enhanced due diligence. Perform annual CCAR-style stress testing and ongoing model validation. Report key metrics promptly to regulators and the board, typically monthly.

Treasury services

Treasury services deliver cash management, ACH/wires, merchant acquiring and lockbox to deepen client relationships and fee income while integrating with client ERPs and APIs. In 2024 US ACH volumes exceeded 30 billion transactions, underscoring scale for fee and float optimization. These services enhance clients' working-capital efficiency, reducing DSO and improving liquidity.

- Cash management: real-time sweeps

- ACH/wires: 30B+ US ACH 2024

- Merchant & lockbox: fee diversification

- ERP/API integration: automated cash flow

Digital delivery

Enhance mobile, online and API platforms to support 78% mobile adoption in 2024, reduce onboarding time via eKYC by ~70% and cut drop-off ~30%, use analytics to boost offer conversion 15–25%, and maintain cybersecurity with 99.99% uptime SLAs and continuous threat detection.

- mobile_adoption_2024:78%

- eKYC_time_cut:70%

- conversion_uplift_analytics:15-25%

- uptime_SLA:99.99%

Grow retail deposits >50% liabilities; manage rates ~5.25-5.50%

Attract/retain low-cost retail deposits (>50% liabilities) via branches and digital channels; manage deposit beta with market rates ~5.25–5.50% (mid-2024). Originate diversified C&I, CRE, construction, consumer loans targeting 5–8% CAGR; keep NPLs <1.0% and net charge-offs ~0.25%. Run Basel III controls (CET1 ≥4.5%, LCR ≥100%), treasury cash management, and digital platforms (mobile adoption 78%).

| Metric | 2024 |

|---|---|

| Retail deposits | >50% liabilities |

| Fed funds | 5.25–5.50% |

| Loan CAGR target | 5–8% |

| NPL | <1.0% |

| Net charge-offs | ~0.25% |

| ACH volume | 30B+ |

| Mobile adoption | 78% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Home Bank Business Model Canvas, not a mockup or sample, and shows the same content and structure you’ll receive after purchase. When you complete your order you’ll get the full, editable file—formatted exactly as seen—ready for presentation, editing, or sharing. No surprises, just the complete deliverable in the same layout and detail.

Retail Bank Business Model Canvas: Strategic Blueprint and Editable Download

Unlock the full strategic blueprint behind Home Bank’s business model. This concise Business Model Canvas maps customer segments, value propositions, key partners and revenue streams to show how the bank scales profitably. Ideal for investors, strategists and founders—download the editable Word/Excel canvas for actionable insights.

Partnerships

Correspondent banks

Partner with regional and national correspondent banks for liquidity, syndications, and treasury services to scale deal size and speed settlements. These relationships enable larger credits and faster settlements and provide access to specialized products not built in-house. This supports balance-sheet flexibility across Arkansas, Florida, Alabama, and Texas (4 states).

Fintech providers

Fintech providers supply core banking, digital banking, fraud detection, and data analytics modules that accelerate feature rollouts and reduce time-to-market, with SLA targets commonly set at 99.9% uptime. Partnerships improve security and UX across mobile and online channels while enabling rapid A/B testing and incremental launches. In 2024 many banks prioritized API-first fintech integrations to shorten deployment cycles and maintain regulatory compliance. Vendor SLAs and compliance clauses help manage uptime, incident response, and auditability.

Payment networks

Home Bank partners with Visa and Mastercard plus ACH and The Clearing House RTP (launched 2017) to enable card issuing, merchant services and instant transfers; card interchange typically ranges about 1–3% per transaction and RTP delivers real‑time settlement. These partnerships expand fee revenue via interchange and treasury services while improving client convenience and stickiness through instant payments.

Real estate ecosystem

Home Bank partners with developers, brokers, title firms and appraisers to streamline commercial real estate lending and construction draws, improving pipeline visibility and underwriting accuracy. These integrations enable faster credit decisions and tighter risk controls. U.S. commercial real estate mortgage debt outstanding was roughly 4 trillion dollars in 2024, highlighting market scale.

- Developer + Broker integrations

- Title & appraiser workflows

- Faster draws, better underwriting

- Local market intelligence in core states

Regulatory and insurance

Coordinate with regulators, auditors, and FDIC insurance partners to ensure safety, soundness, and policy adherence; FDIC insures deposits up to 250,000 and Basel III CET1 minimum is 4.5% with a 2.5% conservation buffer (total 7%) in 2024. This partnership strengthens risk management and reporting discipline and builds depositor trust and institutional credibility.

- Regulatory coordination: CET1 min 4.5% + 2.5% buffer

- Insurance: FDIC coverage 250,000 per depositor

- Controls: enhanced audit and reporting cadence

Partner banks, fintechs, and payment partners speed liquidity, 99.9% SLA and real-time settlement

Partner banks provide liquidity and syndications for larger credits across AR, FL, AL, TX; correspondent lines increase settlement speed. Fintechs (API‑first) supply core, fraud, analytics with 99.9% SLA targets. Card/ACH/RTP partners drive interchange (1–3%) and real‑time settlement; CRE ecosystem partners speed underwriting.

| Partner | Role | 2024 Metric |

|---|---|---|

| Correspondents | Liquidity | Lines supporting $bn deals |

| Fintechs | Digital core | 99.9% SLA |

What is included in the product

A concise, pre-written Business Model Canvas for Home Bank covering customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks. Designed for presentations and funding discussions, it includes narratives, competitive advantages and linked SWOT insights to support strategic decisions and validation using real-world bank operations.

High-level view of Home Bank’s business model with editable cells, relieving the pain of fragmented strategy documents and siloed insights. Shareable and editable for team collaboration and quick scenario testing to speed decisions and board-ready deliverables.

Activities

Deposit gathering

Attract and retain low-cost deposits via branches and digital channels to keep retail deposits as the core funding source (typically >50% of liabilities) and capture rising digital flows. Optimize mix across retail, business and public funds to enhance stability while meeting Basel III LCR >=100%. Price dynamically—with market rates around 5.25–5.50% in mid-2024—to manage deposit betas and liquidity. Support loan growth and funding stability through diversified, low-cost funding.

Lending operations

Originate diversified C&I, CRE, construction, and consumer loans with disciplined underwriting and collateral management, targeting 5–8% portfolio CAGR in core markets to match 2024 industry growth trends.

Monitor portfolios with covenant tracking, sector concentration limits, and stress-testing; aim to keep nonperforming assets below 1.0% and net charge-offs near 0.25% as benchmarked by peer community banks in 2024.

Drive prudent growth in target markets through calibrated pricing, relationship lending, and regional CRE underwriting, aligning new originations with regulatory liquidity and capital metrics recorded in 2024.

Risk & compliance

Manage credit, interest-rate, liquidity and operational risks to meet regulatory minima under Basel III (CET1 minimum 4.5%) and maintain an LCR at or above the 100% regulatory floor; target NPLs well below 1% for retail portfolios. Maintain AML/BSA, KYC and fair lending programs with timely SARs and enhanced due diligence. Perform annual CCAR-style stress testing and ongoing model validation. Report key metrics promptly to regulators and the board, typically monthly.

Treasury services

Treasury services deliver cash management, ACH/wires, merchant acquiring and lockbox to deepen client relationships and fee income while integrating with client ERPs and APIs. In 2024 US ACH volumes exceeded 30 billion transactions, underscoring scale for fee and float optimization. These services enhance clients' working-capital efficiency, reducing DSO and improving liquidity.

- Cash management: real-time sweeps

- ACH/wires: 30B+ US ACH 2024

- Merchant & lockbox: fee diversification

- ERP/API integration: automated cash flow

Digital delivery

Enhance mobile, online and API platforms to support 78% mobile adoption in 2024, reduce onboarding time via eKYC by ~70% and cut drop-off ~30%, use analytics to boost offer conversion 15–25%, and maintain cybersecurity with 99.99% uptime SLAs and continuous threat detection.

- mobile_adoption_2024:78%

- eKYC_time_cut:70%

- conversion_uplift_analytics:15-25%

- uptime_SLA:99.99%

Grow retail deposits >50% liabilities; manage rates ~5.25-5.50%

Attract/retain low-cost retail deposits (>50% liabilities) via branches and digital channels; manage deposit beta with market rates ~5.25–5.50% (mid-2024). Originate diversified C&I, CRE, construction, consumer loans targeting 5–8% CAGR; keep NPLs <1.0% and net charge-offs ~0.25%. Run Basel III controls (CET1 ≥4.5%, LCR ≥100%), treasury cash management, and digital platforms (mobile adoption 78%).

| Metric | 2024 |

|---|---|

| Retail deposits | >50% liabilities |

| Fed funds | 5.25–5.50% |

| Loan CAGR target | 5–8% |

| NPL | <1.0% |

| Net charge-offs | ~0.25% |

| ACH volume | 30B+ |

| Mobile adoption | 78% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Home Bank Business Model Canvas, not a mockup or sample, and shows the same content and structure you’ll receive after purchase. When you complete your order you’ll get the full, editable file—formatted exactly as seen—ready for presentation, editing, or sharing. No surprises, just the complete deliverable in the same layout and detail.

Description

Retail Bank Business Model Canvas: Strategic Blueprint and Editable Download

Unlock the full strategic blueprint behind Home Bank’s business model. This concise Business Model Canvas maps customer segments, value propositions, key partners and revenue streams to show how the bank scales profitably. Ideal for investors, strategists and founders—download the editable Word/Excel canvas for actionable insights.

Partnerships

Correspondent banks

Partner with regional and national correspondent banks for liquidity, syndications, and treasury services to scale deal size and speed settlements. These relationships enable larger credits and faster settlements and provide access to specialized products not built in-house. This supports balance-sheet flexibility across Arkansas, Florida, Alabama, and Texas (4 states).

Fintech providers

Fintech providers supply core banking, digital banking, fraud detection, and data analytics modules that accelerate feature rollouts and reduce time-to-market, with SLA targets commonly set at 99.9% uptime. Partnerships improve security and UX across mobile and online channels while enabling rapid A/B testing and incremental launches. In 2024 many banks prioritized API-first fintech integrations to shorten deployment cycles and maintain regulatory compliance. Vendor SLAs and compliance clauses help manage uptime, incident response, and auditability.

Payment networks

Home Bank partners with Visa and Mastercard plus ACH and The Clearing House RTP (launched 2017) to enable card issuing, merchant services and instant transfers; card interchange typically ranges about 1–3% per transaction and RTP delivers real‑time settlement. These partnerships expand fee revenue via interchange and treasury services while improving client convenience and stickiness through instant payments.

Real estate ecosystem

Home Bank partners with developers, brokers, title firms and appraisers to streamline commercial real estate lending and construction draws, improving pipeline visibility and underwriting accuracy. These integrations enable faster credit decisions and tighter risk controls. U.S. commercial real estate mortgage debt outstanding was roughly 4 trillion dollars in 2024, highlighting market scale.

- Developer + Broker integrations

- Title & appraiser workflows

- Faster draws, better underwriting

- Local market intelligence in core states

Regulatory and insurance

Coordinate with regulators, auditors, and FDIC insurance partners to ensure safety, soundness, and policy adherence; FDIC insures deposits up to 250,000 and Basel III CET1 minimum is 4.5% with a 2.5% conservation buffer (total 7%) in 2024. This partnership strengthens risk management and reporting discipline and builds depositor trust and institutional credibility.

- Regulatory coordination: CET1 min 4.5% + 2.5% buffer

- Insurance: FDIC coverage 250,000 per depositor

- Controls: enhanced audit and reporting cadence

Partner banks, fintechs, and payment partners speed liquidity, 99.9% SLA and real-time settlement

Partner banks provide liquidity and syndications for larger credits across AR, FL, AL, TX; correspondent lines increase settlement speed. Fintechs (API‑first) supply core, fraud, analytics with 99.9% SLA targets. Card/ACH/RTP partners drive interchange (1–3%) and real‑time settlement; CRE ecosystem partners speed underwriting.

| Partner | Role | 2024 Metric |

|---|---|---|

| Correspondents | Liquidity | Lines supporting $bn deals |

| Fintechs | Digital core | 99.9% SLA |

What is included in the product

A concise, pre-written Business Model Canvas for Home Bank covering customer segments, channels, value propositions and revenue streams across the 9 classic BMC blocks. Designed for presentations and funding discussions, it includes narratives, competitive advantages and linked SWOT insights to support strategic decisions and validation using real-world bank operations.

High-level view of Home Bank’s business model with editable cells, relieving the pain of fragmented strategy documents and siloed insights. Shareable and editable for team collaboration and quick scenario testing to speed decisions and board-ready deliverables.

Activities

Deposit gathering

Attract and retain low-cost deposits via branches and digital channels to keep retail deposits as the core funding source (typically >50% of liabilities) and capture rising digital flows. Optimize mix across retail, business and public funds to enhance stability while meeting Basel III LCR >=100%. Price dynamically—with market rates around 5.25–5.50% in mid-2024—to manage deposit betas and liquidity. Support loan growth and funding stability through diversified, low-cost funding.

Lending operations

Originate diversified C&I, CRE, construction, and consumer loans with disciplined underwriting and collateral management, targeting 5–8% portfolio CAGR in core markets to match 2024 industry growth trends.

Monitor portfolios with covenant tracking, sector concentration limits, and stress-testing; aim to keep nonperforming assets below 1.0% and net charge-offs near 0.25% as benchmarked by peer community banks in 2024.

Drive prudent growth in target markets through calibrated pricing, relationship lending, and regional CRE underwriting, aligning new originations with regulatory liquidity and capital metrics recorded in 2024.

Risk & compliance

Manage credit, interest-rate, liquidity and operational risks to meet regulatory minima under Basel III (CET1 minimum 4.5%) and maintain an LCR at or above the 100% regulatory floor; target NPLs well below 1% for retail portfolios. Maintain AML/BSA, KYC and fair lending programs with timely SARs and enhanced due diligence. Perform annual CCAR-style stress testing and ongoing model validation. Report key metrics promptly to regulators and the board, typically monthly.

Treasury services

Treasury services deliver cash management, ACH/wires, merchant acquiring and lockbox to deepen client relationships and fee income while integrating with client ERPs and APIs. In 2024 US ACH volumes exceeded 30 billion transactions, underscoring scale for fee and float optimization. These services enhance clients' working-capital efficiency, reducing DSO and improving liquidity.

- Cash management: real-time sweeps

- ACH/wires: 30B+ US ACH 2024

- Merchant & lockbox: fee diversification

- ERP/API integration: automated cash flow

Digital delivery

Enhance mobile, online and API platforms to support 78% mobile adoption in 2024, reduce onboarding time via eKYC by ~70% and cut drop-off ~30%, use analytics to boost offer conversion 15–25%, and maintain cybersecurity with 99.99% uptime SLAs and continuous threat detection.

- mobile_adoption_2024:78%

- eKYC_time_cut:70%

- conversion_uplift_analytics:15-25%

- uptime_SLA:99.99%

Grow retail deposits >50% liabilities; manage rates ~5.25-5.50%

Attract/retain low-cost retail deposits (>50% liabilities) via branches and digital channels; manage deposit beta with market rates ~5.25–5.50% (mid-2024). Originate diversified C&I, CRE, construction, consumer loans targeting 5–8% CAGR; keep NPLs <1.0% and net charge-offs ~0.25%. Run Basel III controls (CET1 ≥4.5%, LCR ≥100%), treasury cash management, and digital platforms (mobile adoption 78%).

| Metric | 2024 |

|---|---|

| Retail deposits | >50% liabilities |

| Fed funds | 5.25–5.50% |

| Loan CAGR target | 5–8% |

| NPL | <1.0% |

| Net charge-offs | ~0.25% |

| ACH volume | 30B+ |

| Mobile adoption | 78% |

Full Version Awaits

Business Model Canvas

The document previewed here is the actual Home Bank Business Model Canvas, not a mockup or sample, and shows the same content and structure you’ll receive after purchase. When you complete your order you’ll get the full, editable file—formatted exactly as seen—ready for presentation, editing, or sharing. No surprises, just the complete deliverable in the same layout and detail.