HORIBA PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our HORIBA PESTLE Analysis—three to five concise, expert-driven sentences revealing how political, economic, social, technological, legal, and environmental forces shape HORIBA's prospects. Use these insights to anticipate risks, identify growth levers, and sharpen investment or strategic decisions. Purchase the full report for detailed, ready-to-use intelligence and immediate download.

Political factors

Trade policy and export controls

Shifts in US–China–EU trade policy and coordinated export controls (US, Netherlands, Japan, UK) since 2022 materially affect cross-border sales of instruments and parts, especially in semiconductor and emissions-testing segments. Controls target advanced chip-related and vehicle-testing technologies and impose licensing that can delay shipments and add compliance costs running into millions. HORIBA must offer controllable product variants and robust compliance processes, plus proactive country-of-origin planning and dual-sourcing to cut political risk.

Industrial and healthcare subsidies

Government funding such as the US Inflation Reduction Act (~369 billion USD clean-energy credits), CHIPS Act (about 52 billion USD for semiconductors) and EU Chips mobilization (~43 billion EUR), plus ~8 billion USD for US hydrogen hubs, is expanding test and metrology demand across EV, hydrogen, semiconductor and diagnostics supply chains. The global IVD market is ~100 billion USD (2024) and semiconductor equipment ~100+ billion USD, creating procurement windows under national chip and medical infrastructure programs. HORIBA can align product roadmaps to subsidy-eligible projects to speed adoption, while localizing manufacturing and R&D increases eligibility and tender win rates.

Environmental and emissions policy

Tighter air-quality and vehicle-emission rules—notably Euro 7 finalized in 2023 with staged implementation 2025–2027 and China VI rollouts through 2023—boost demand for analyzers and regulatory testing systems. Divergent regional standards force configurable platforms and certification expertise across markets. Policy reversals or delays can shift orders by quarters and impact revenue timing. Continuous regulator engagement helps anticipate rule changes and secure pipeline visibility.

Geopolitical stability and supply security

Geopolitical conflicts and sanctions increasingly disrupt logistics and access to critical components such as sensors and electronics, with the global semiconductor market at about $614 billion in 2024 (WSTS), amplifying supply risk for HORIBA. Energy security policies—EU gas storage ~96% in late 2024—shift industrial spending cycles and capital allocation for instrument manufacturers. HORIBA should map critical suppliers, hold strategic inventory for sanctioned/high‑risk regions, and expand regional manufacturing footprints to mitigate cross‑border disruptions.

- Map suppliers

- Strategic inventory

- Regional manufacturing

- Monitor semiconductor market ($614B, 2024)

Public procurement and standards diplomacy

National labs, hospitals and universities buy via regulated tenders where OECD estimates public procurement around 12% of GDP, so HORIBA’s tender compliance and transparent bidding materially raise win rates and reduce political scrutiny. Country standards bodies (ISO, JIS, CEN) shape testing protocols that dictate product specs, and early participation in standards committees can embed HORIBA methods into market requirements.

- Procurement share ~12% GDP

- Target: national labs/hospitals/universities

- Standards influence specs (ISO/JIS/CEN)

- Standards committee engagement embeds methods

- Transparent bidding increases win probability, lowers scrutiny

Trade controls, state funding and emissions rules reshape semiconductor and testing supply chains

Shifts in US–China–EU trade controls since 2022 raise licensing/compliance costs and delay shipments for semiconductor and vehicle-testing products. Large state funding (IRA ~$369B, CHIPS ~$52B, EU chips ~43B EUR) expands test demand. Tightening emission rules (Euro 7, China VI) and public procurement (~12% GDP) favor localized manufacturing and tender readiness.

| Metric | Value | Relevance |

|---|---|---|

| Semiconductor market | $614B (2024) | High supply risk, demand driver |

| IVD market | $100B (2024) | Diagnostics demand |

| Public procurement | ~12% GDP | Tender focus |

What is included in the product

Explores how macro-environmental forces uniquely affect HORIBA across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking scenarios and sector-specific examples to help executives, investors and strategists identify risks, opportunities and actionable responses.

A concise, visually segmented HORIBA PESTLE summary that’s editable and shareable for quick alignment across teams, easy insertion into presentations, and focused support for external risk and market-positioning discussions.

Economic factors

Cyclical demand in auto and semiconductor

Auto testing and wafer metrology track capex and model cycles: global vehicle production recovered from about 77M units in 2023 to roughly 80M in 2024, while semiconductor equipment billings swung sharply after a 2022 peak, pressuring orders and lead times. Downturns compress HORIBA orders; upswings push long‑lead projects and backlog growth. HORIBA needs flexible capacity and service revenue streams to smooth volatility and uses scenario planning to protect cash and backlog quality.

Currency fluctuations (JPY, USD, EUR, CNY)

As a Japan-based exporter, HORIBA faces yen volatility (USD/JPY ≈155, EUR/USD ≈1.10, USD/CNY ≈7.3 in mid‑2025) that can compress margins and alter price competitiveness. Natural hedging—local cost bases and invoicing in customer currency—helps stabilize reported earnings. Financial hedges and regional production footprints further balance FX exposure. Transparent surcharge mechanisms protect gross margin by passing short-term FX moves to customers.

Healthcare spending resilience

Diagnostics demand is less cyclical and the global IVD market was about USD 90–95 billion in 2024, but revenue remains sensitive to reimbursement rules and constrained hospital budgets. Emerging markets show faster healthcare spend expansion (roughly 5–7% CAGR in many EMs) offering volume growth amid strong price pressure. Service contracts and reagent pull-through drive recurring revenue, with reagents often representing over 50% of consumable sales in diagnostics. Local partnerships expand distribution, improving access and affordability in price-sensitive regions.

Inflation and input costs

Inflation in 2024 (US CPI ~3.4%) and ongoing supply tightness continue to pressure components, rare gases (neon/helium) and electronics inputs, creating scarcity-driven cost spikes. HORIBA mitigates margin erosion via index-linked pricing and design-to-cost programs while vendor consolidation risks prompt multi-sourcing and strategic long-term agreements. Inventory optimization balances carrying cost with supply assurance, targeting lower stock turns but higher availability.

- Components scarcity: prioritize multi-sourcing

- Rare gases: secure long-term contracts

- Index-linked pricing: protects margins

- Inventory: trade-off between carrying cost and service level

Productivity and labor markets

Tight engineering labor markets (Japan unemployment ~2.5% in 2024) push wage inflation and can extend product development timelines; HORIBA mitigates this via automation and digital service models that raise throughput and support gross margins. Global R&D hubs broaden talent access while targeted training and retention programs safeguard institutional know-how.

- Labor tightness: Japan unemployment ~2.5% (2024)

- Automation adoption: IFR robot installs +8% (2024)

- R&D hubs: diversified talent pool

- Retention: targeted training protects know-how

Trade controls, state funding and emissions rules reshape semiconductor and testing supply chains

HORIBA revenue sensitive to auto (global vehicle prod ~80M in 2024) and semiconductor capex cycles; downturns cut orders while recoveries expand long‑lead backlog. FX volatility (USD/JPY ≈155 mid‑2025) and US CPI ~3.4% (2024) squeeze margins; diagnostics (IVD market ~USD 90–95bn in 2024) offers recurring reagent revenue. Japan unemployment ~2.5% (2024) tightens engineering labor.

| Metric | Value |

|---|---|

| Global vehicle prod (2024) | ~80M |

| IVD market (2024) | USD 90–95bn |

| USD/JPY (mid‑2025) | ≈155 |

| US CPI (2024) | ~3.4% |

| Japan unemployment (2024) | ~2.5% |

Preview the Actual Deliverable

HORIBA PESTLE Analysis

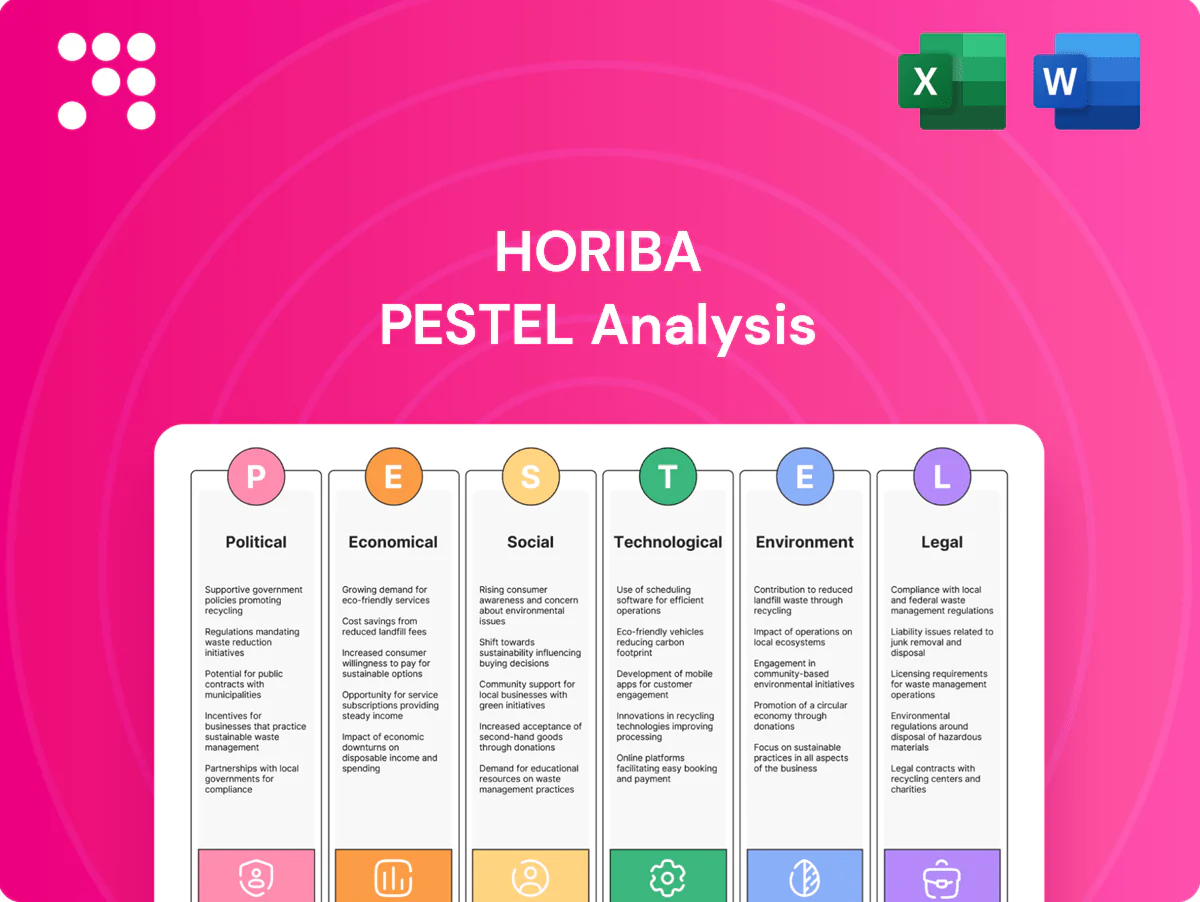

The preview shown here is the exact HORIBA PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file you’ll get instantly after payment. No placeholders or teasers—this is the real, professionally structured report you’ll own.

Skip the Research. Get the Strategy.

Unlock strategic clarity with our HORIBA PESTLE Analysis—three to five concise, expert-driven sentences revealing how political, economic, social, technological, legal, and environmental forces shape HORIBA's prospects. Use these insights to anticipate risks, identify growth levers, and sharpen investment or strategic decisions. Purchase the full report for detailed, ready-to-use intelligence and immediate download.

Political factors

Trade policy and export controls

Shifts in US–China–EU trade policy and coordinated export controls (US, Netherlands, Japan, UK) since 2022 materially affect cross-border sales of instruments and parts, especially in semiconductor and emissions-testing segments. Controls target advanced chip-related and vehicle-testing technologies and impose licensing that can delay shipments and add compliance costs running into millions. HORIBA must offer controllable product variants and robust compliance processes, plus proactive country-of-origin planning and dual-sourcing to cut political risk.

Industrial and healthcare subsidies

Government funding such as the US Inflation Reduction Act (~369 billion USD clean-energy credits), CHIPS Act (about 52 billion USD for semiconductors) and EU Chips mobilization (~43 billion EUR), plus ~8 billion USD for US hydrogen hubs, is expanding test and metrology demand across EV, hydrogen, semiconductor and diagnostics supply chains. The global IVD market is ~100 billion USD (2024) and semiconductor equipment ~100+ billion USD, creating procurement windows under national chip and medical infrastructure programs. HORIBA can align product roadmaps to subsidy-eligible projects to speed adoption, while localizing manufacturing and R&D increases eligibility and tender win rates.

Environmental and emissions policy

Tighter air-quality and vehicle-emission rules—notably Euro 7 finalized in 2023 with staged implementation 2025–2027 and China VI rollouts through 2023—boost demand for analyzers and regulatory testing systems. Divergent regional standards force configurable platforms and certification expertise across markets. Policy reversals or delays can shift orders by quarters and impact revenue timing. Continuous regulator engagement helps anticipate rule changes and secure pipeline visibility.

Geopolitical stability and supply security

Geopolitical conflicts and sanctions increasingly disrupt logistics and access to critical components such as sensors and electronics, with the global semiconductor market at about $614 billion in 2024 (WSTS), amplifying supply risk for HORIBA. Energy security policies—EU gas storage ~96% in late 2024—shift industrial spending cycles and capital allocation for instrument manufacturers. HORIBA should map critical suppliers, hold strategic inventory for sanctioned/high‑risk regions, and expand regional manufacturing footprints to mitigate cross‑border disruptions.

- Map suppliers

- Strategic inventory

- Regional manufacturing

- Monitor semiconductor market ($614B, 2024)

Public procurement and standards diplomacy

National labs, hospitals and universities buy via regulated tenders where OECD estimates public procurement around 12% of GDP, so HORIBA’s tender compliance and transparent bidding materially raise win rates and reduce political scrutiny. Country standards bodies (ISO, JIS, CEN) shape testing protocols that dictate product specs, and early participation in standards committees can embed HORIBA methods into market requirements.

- Procurement share ~12% GDP

- Target: national labs/hospitals/universities

- Standards influence specs (ISO/JIS/CEN)

- Standards committee engagement embeds methods

- Transparent bidding increases win probability, lowers scrutiny

Trade controls, state funding and emissions rules reshape semiconductor and testing supply chains

Shifts in US–China–EU trade controls since 2022 raise licensing/compliance costs and delay shipments for semiconductor and vehicle-testing products. Large state funding (IRA ~$369B, CHIPS ~$52B, EU chips ~43B EUR) expands test demand. Tightening emission rules (Euro 7, China VI) and public procurement (~12% GDP) favor localized manufacturing and tender readiness.

| Metric | Value | Relevance |

|---|---|---|

| Semiconductor market | $614B (2024) | High supply risk, demand driver |

| IVD market | $100B (2024) | Diagnostics demand |

| Public procurement | ~12% GDP | Tender focus |

What is included in the product

Explores how macro-environmental forces uniquely affect HORIBA across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking scenarios and sector-specific examples to help executives, investors and strategists identify risks, opportunities and actionable responses.

A concise, visually segmented HORIBA PESTLE summary that’s editable and shareable for quick alignment across teams, easy insertion into presentations, and focused support for external risk and market-positioning discussions.

Economic factors

Cyclical demand in auto and semiconductor

Auto testing and wafer metrology track capex and model cycles: global vehicle production recovered from about 77M units in 2023 to roughly 80M in 2024, while semiconductor equipment billings swung sharply after a 2022 peak, pressuring orders and lead times. Downturns compress HORIBA orders; upswings push long‑lead projects and backlog growth. HORIBA needs flexible capacity and service revenue streams to smooth volatility and uses scenario planning to protect cash and backlog quality.

Currency fluctuations (JPY, USD, EUR, CNY)

As a Japan-based exporter, HORIBA faces yen volatility (USD/JPY ≈155, EUR/USD ≈1.10, USD/CNY ≈7.3 in mid‑2025) that can compress margins and alter price competitiveness. Natural hedging—local cost bases and invoicing in customer currency—helps stabilize reported earnings. Financial hedges and regional production footprints further balance FX exposure. Transparent surcharge mechanisms protect gross margin by passing short-term FX moves to customers.

Healthcare spending resilience

Diagnostics demand is less cyclical and the global IVD market was about USD 90–95 billion in 2024, but revenue remains sensitive to reimbursement rules and constrained hospital budgets. Emerging markets show faster healthcare spend expansion (roughly 5–7% CAGR in many EMs) offering volume growth amid strong price pressure. Service contracts and reagent pull-through drive recurring revenue, with reagents often representing over 50% of consumable sales in diagnostics. Local partnerships expand distribution, improving access and affordability in price-sensitive regions.

Inflation and input costs

Inflation in 2024 (US CPI ~3.4%) and ongoing supply tightness continue to pressure components, rare gases (neon/helium) and electronics inputs, creating scarcity-driven cost spikes. HORIBA mitigates margin erosion via index-linked pricing and design-to-cost programs while vendor consolidation risks prompt multi-sourcing and strategic long-term agreements. Inventory optimization balances carrying cost with supply assurance, targeting lower stock turns but higher availability.

- Components scarcity: prioritize multi-sourcing

- Rare gases: secure long-term contracts

- Index-linked pricing: protects margins

- Inventory: trade-off between carrying cost and service level

Productivity and labor markets

Tight engineering labor markets (Japan unemployment ~2.5% in 2024) push wage inflation and can extend product development timelines; HORIBA mitigates this via automation and digital service models that raise throughput and support gross margins. Global R&D hubs broaden talent access while targeted training and retention programs safeguard institutional know-how.

- Labor tightness: Japan unemployment ~2.5% (2024)

- Automation adoption: IFR robot installs +8% (2024)

- R&D hubs: diversified talent pool

- Retention: targeted training protects know-how

Trade controls, state funding and emissions rules reshape semiconductor and testing supply chains

HORIBA revenue sensitive to auto (global vehicle prod ~80M in 2024) and semiconductor capex cycles; downturns cut orders while recoveries expand long‑lead backlog. FX volatility (USD/JPY ≈155 mid‑2025) and US CPI ~3.4% (2024) squeeze margins; diagnostics (IVD market ~USD 90–95bn in 2024) offers recurring reagent revenue. Japan unemployment ~2.5% (2024) tightens engineering labor.

| Metric | Value |

|---|---|

| Global vehicle prod (2024) | ~80M |

| IVD market (2024) | USD 90–95bn |

| USD/JPY (mid‑2025) | ≈155 |

| US CPI (2024) | ~3.4% |

| Japan unemployment (2024) | ~2.5% |

Preview the Actual Deliverable

HORIBA PESTLE Analysis

The preview shown here is the exact HORIBA PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file you’ll get instantly after payment. No placeholders or teasers—this is the real, professionally structured report you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our HORIBA PESTLE Analysis—three to five concise, expert-driven sentences revealing how political, economic, social, technological, legal, and environmental forces shape HORIBA's prospects. Use these insights to anticipate risks, identify growth levers, and sharpen investment or strategic decisions. Purchase the full report for detailed, ready-to-use intelligence and immediate download.

Political factors

Trade policy and export controls

Shifts in US–China–EU trade policy and coordinated export controls (US, Netherlands, Japan, UK) since 2022 materially affect cross-border sales of instruments and parts, especially in semiconductor and emissions-testing segments. Controls target advanced chip-related and vehicle-testing technologies and impose licensing that can delay shipments and add compliance costs running into millions. HORIBA must offer controllable product variants and robust compliance processes, plus proactive country-of-origin planning and dual-sourcing to cut political risk.

Industrial and healthcare subsidies

Government funding such as the US Inflation Reduction Act (~369 billion USD clean-energy credits), CHIPS Act (about 52 billion USD for semiconductors) and EU Chips mobilization (~43 billion EUR), plus ~8 billion USD for US hydrogen hubs, is expanding test and metrology demand across EV, hydrogen, semiconductor and diagnostics supply chains. The global IVD market is ~100 billion USD (2024) and semiconductor equipment ~100+ billion USD, creating procurement windows under national chip and medical infrastructure programs. HORIBA can align product roadmaps to subsidy-eligible projects to speed adoption, while localizing manufacturing and R&D increases eligibility and tender win rates.

Environmental and emissions policy

Tighter air-quality and vehicle-emission rules—notably Euro 7 finalized in 2023 with staged implementation 2025–2027 and China VI rollouts through 2023—boost demand for analyzers and regulatory testing systems. Divergent regional standards force configurable platforms and certification expertise across markets. Policy reversals or delays can shift orders by quarters and impact revenue timing. Continuous regulator engagement helps anticipate rule changes and secure pipeline visibility.

Geopolitical stability and supply security

Geopolitical conflicts and sanctions increasingly disrupt logistics and access to critical components such as sensors and electronics, with the global semiconductor market at about $614 billion in 2024 (WSTS), amplifying supply risk for HORIBA. Energy security policies—EU gas storage ~96% in late 2024—shift industrial spending cycles and capital allocation for instrument manufacturers. HORIBA should map critical suppliers, hold strategic inventory for sanctioned/high‑risk regions, and expand regional manufacturing footprints to mitigate cross‑border disruptions.

- Map suppliers

- Strategic inventory

- Regional manufacturing

- Monitor semiconductor market ($614B, 2024)

Public procurement and standards diplomacy

National labs, hospitals and universities buy via regulated tenders where OECD estimates public procurement around 12% of GDP, so HORIBA’s tender compliance and transparent bidding materially raise win rates and reduce political scrutiny. Country standards bodies (ISO, JIS, CEN) shape testing protocols that dictate product specs, and early participation in standards committees can embed HORIBA methods into market requirements.

- Procurement share ~12% GDP

- Target: national labs/hospitals/universities

- Standards influence specs (ISO/JIS/CEN)

- Standards committee engagement embeds methods

- Transparent bidding increases win probability, lowers scrutiny

Trade controls, state funding and emissions rules reshape semiconductor and testing supply chains

Shifts in US–China–EU trade controls since 2022 raise licensing/compliance costs and delay shipments for semiconductor and vehicle-testing products. Large state funding (IRA ~$369B, CHIPS ~$52B, EU chips ~43B EUR) expands test demand. Tightening emission rules (Euro 7, China VI) and public procurement (~12% GDP) favor localized manufacturing and tender readiness.

| Metric | Value | Relevance |

|---|---|---|

| Semiconductor market | $614B (2024) | High supply risk, demand driver |

| IVD market | $100B (2024) | Diagnostics demand |

| Public procurement | ~12% GDP | Tender focus |

What is included in the product

Explores how macro-environmental forces uniquely affect HORIBA across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends, forward-looking scenarios and sector-specific examples to help executives, investors and strategists identify risks, opportunities and actionable responses.

A concise, visually segmented HORIBA PESTLE summary that’s editable and shareable for quick alignment across teams, easy insertion into presentations, and focused support for external risk and market-positioning discussions.

Economic factors

Cyclical demand in auto and semiconductor

Auto testing and wafer metrology track capex and model cycles: global vehicle production recovered from about 77M units in 2023 to roughly 80M in 2024, while semiconductor equipment billings swung sharply after a 2022 peak, pressuring orders and lead times. Downturns compress HORIBA orders; upswings push long‑lead projects and backlog growth. HORIBA needs flexible capacity and service revenue streams to smooth volatility and uses scenario planning to protect cash and backlog quality.

Currency fluctuations (JPY, USD, EUR, CNY)

As a Japan-based exporter, HORIBA faces yen volatility (USD/JPY ≈155, EUR/USD ≈1.10, USD/CNY ≈7.3 in mid‑2025) that can compress margins and alter price competitiveness. Natural hedging—local cost bases and invoicing in customer currency—helps stabilize reported earnings. Financial hedges and regional production footprints further balance FX exposure. Transparent surcharge mechanisms protect gross margin by passing short-term FX moves to customers.

Healthcare spending resilience

Diagnostics demand is less cyclical and the global IVD market was about USD 90–95 billion in 2024, but revenue remains sensitive to reimbursement rules and constrained hospital budgets. Emerging markets show faster healthcare spend expansion (roughly 5–7% CAGR in many EMs) offering volume growth amid strong price pressure. Service contracts and reagent pull-through drive recurring revenue, with reagents often representing over 50% of consumable sales in diagnostics. Local partnerships expand distribution, improving access and affordability in price-sensitive regions.

Inflation and input costs

Inflation in 2024 (US CPI ~3.4%) and ongoing supply tightness continue to pressure components, rare gases (neon/helium) and electronics inputs, creating scarcity-driven cost spikes. HORIBA mitigates margin erosion via index-linked pricing and design-to-cost programs while vendor consolidation risks prompt multi-sourcing and strategic long-term agreements. Inventory optimization balances carrying cost with supply assurance, targeting lower stock turns but higher availability.

- Components scarcity: prioritize multi-sourcing

- Rare gases: secure long-term contracts

- Index-linked pricing: protects margins

- Inventory: trade-off between carrying cost and service level

Productivity and labor markets

Tight engineering labor markets (Japan unemployment ~2.5% in 2024) push wage inflation and can extend product development timelines; HORIBA mitigates this via automation and digital service models that raise throughput and support gross margins. Global R&D hubs broaden talent access while targeted training and retention programs safeguard institutional know-how.

- Labor tightness: Japan unemployment ~2.5% (2024)

- Automation adoption: IFR robot installs +8% (2024)

- R&D hubs: diversified talent pool

- Retention: targeted training protects know-how

Trade controls, state funding and emissions rules reshape semiconductor and testing supply chains

HORIBA revenue sensitive to auto (global vehicle prod ~80M in 2024) and semiconductor capex cycles; downturns cut orders while recoveries expand long‑lead backlog. FX volatility (USD/JPY ≈155 mid‑2025) and US CPI ~3.4% (2024) squeeze margins; diagnostics (IVD market ~USD 90–95bn in 2024) offers recurring reagent revenue. Japan unemployment ~2.5% (2024) tightens engineering labor.

| Metric | Value |

|---|---|

| Global vehicle prod (2024) | ~80M |

| IVD market (2024) | USD 90–95bn |

| USD/JPY (mid‑2025) | ≈155 |

| US CPI (2024) | ~3.4% |

| Japan unemployment (2024) | ~2.5% |

Preview the Actual Deliverable

HORIBA PESTLE Analysis

The preview shown here is the exact HORIBA PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file you’ll get instantly after payment. No placeholders or teasers—this is the real, professionally structured report you’ll own.