Horstman Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

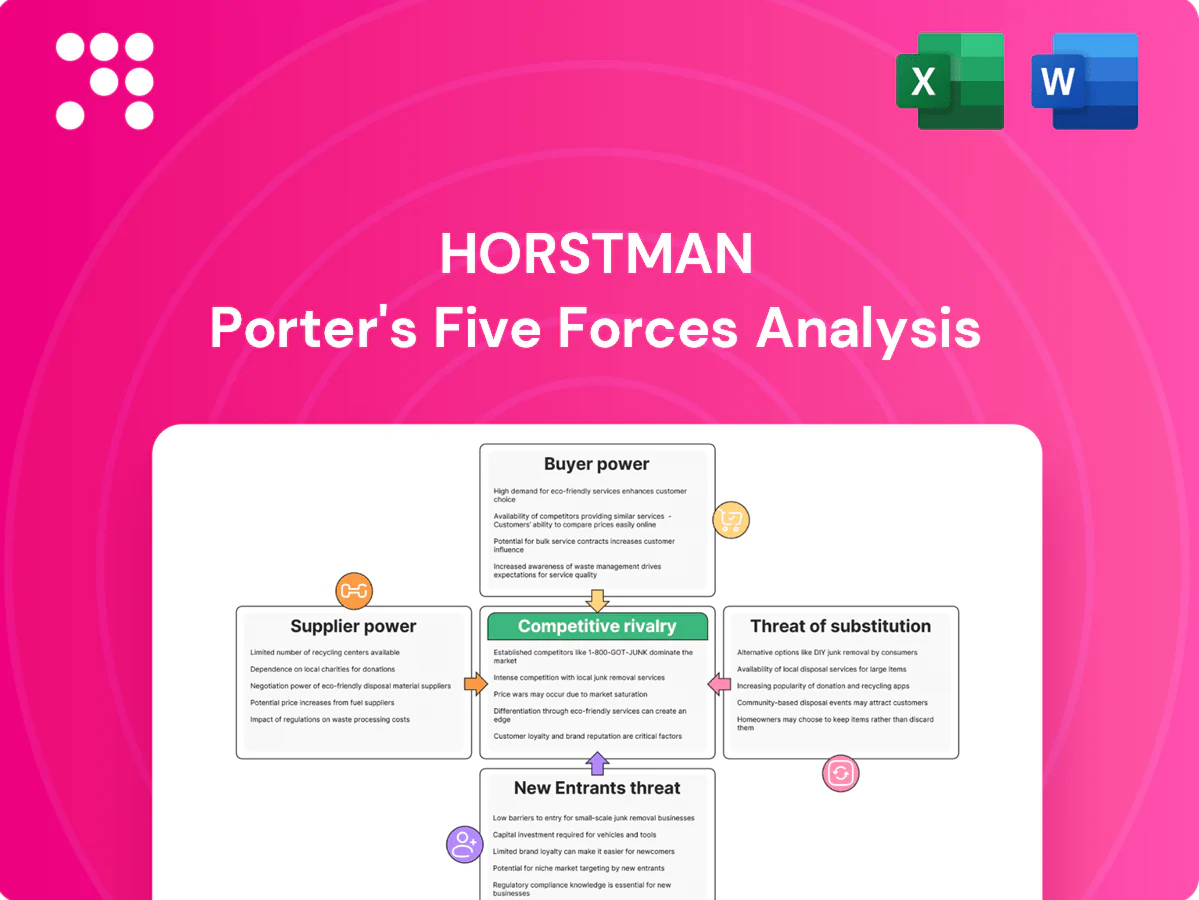

Horstman's competitive landscape shows concentrated supplier leverage, moderate buyer power, and significant rivalry shaping margins and growth prospects. Our snapshot highlights key pressures—from substitute threats to entry barriers—that influence pricing and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Horstman’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials and components

Horstman depends on high-spec steels, titanium, precision seals, hydro-pneumatic valves, accumulators and advanced dampers sourced from fewer than 5 qualified suppliers, giving those vendors outsized leverage. Supplier concentration plus AS9100/ITAR-style defense certifications raise bargaining power, while qualification timelines of 12–24 months and the mission-critical cost of quality lapses (programs commonly worth millions) sharply increase switching costs.

Compliance and export controls

ITAR and EAR controls, plus NATO AQAP 2110 and defense quality standards as of 2024 narrow the approved vendor pool, concentrating supply power among compliant firms.

Compliance overhead—extended due diligence, facility audits and export licensing—makes onboarding slow and costly, letting incumbent vendors demand firmer commercial terms.

Stringent documentation and traceability requirements increase switching costs and give suppliers with proven audit histories greater negotiating leverage.

Process and testing intensity

Heat treatment, precision machining, NDT and endurance testing are key bottlenecks: 2024 industry data show surge lead times stretching to 6–12 weeks and testing rig availability cutting effective throughput by about 30%, giving specialized suppliers bargaining power. Limited access to calibration labs and bespoke test rigs concentrates leverage with a handful of vendors, while expedited slots in 2024 attracted premiums of roughly 25–50%, pressuring input costs and delivery schedules.

Mitigation via partnerships

- Long-term agreements: stabilize pricing and capacity

- Dual-sourcing: lowers dependency and supply risk

- VAVE: trims supplier margins via cost reduction

- Co-development/shared IP: aligns incentives for custom parts

- Forecast visibility (FY2024 DoD ~858B): improves planning

- Sole-source items: retain supplier leverage

Macroeconomic and energy sensitivity

- Rapid pass-through: higher input-cost realization

- Indexation clauses: locked escalators

- Currency risk: ~10% USD strength impact (2024)

- Supplier leverage: stronger on price and contract terms

Fewer than 5 suppliers, 12–24 month quals and 25–50% expedite premiums

Supplier concentration (<5 qualified vendors), defense certifications (AS9100/ITAR/AQAP) and 12–24 month qualifications give suppliers strong leverage; 6–12 week bottlenecks and 25–50% expedited premiums raise costs and switching frictions. Long-term contracts, dual-sourcing and co-development lower but do not eliminate supplier power; DoD FY2024 ~858B and Brent ~$86/bbl affect demand and input costs.

| Metric | 2024 Value |

|---|---|

| Qualified suppliers | <5 |

| Qualification time | 12–24 months |

| Lead times | 6–12 weeks |

| Expedite premium | 25–50% |

| DoD budget | $858B |

| Brent | $86/bbl |

| USD strength | ~10% |

What is included in the product

Comprehensive Porter’s Five Forces assessment for Horstman, uncovering competitive intensity, buyer and supplier leverage, entry barriers, substitutes, and disruptive threats to its market position.

A concise Horstman Porter’s Five Forces one-sheet that distills competitive pressure into clear scores and a radar view—ideal for quick strategic decisions and seamless slide integration.

Customers Bargaining Power

Concentrated buyers and primes

Defense ministries and a handful of OEM primes (Lockheed, Boeing, Northrop, Raytheon, BAE) dominate demand, with the US DoD alone at about $858 billion in FY2024, giving buyers scale and program control that drives strong bargaining power. Primes bundle subsystems across programs and use competitive tenders and frame agreements to compress supplier pricing. Strict past-performance prerequisites further limit supplier leverage in negotiations.

High switching and integration costs

Suspension systems are platform-integrated, directly affecting mobility, survivability and logistics, so qualification cycles typically run 12–36 months and certification costs commonly exceed $1m per platform. Once qualified, buyers face costly requalification and retrofit logistics that can exceed $5m in program costs, reducing buyer power after award. Pre-award, buyers exploit competition to extract price, lead-time and warranty concessions.

Contract structures and risk allocation

Firm-fixed-price and performance-based logistics contracts shift cost and reliability risk to suppliers, forcing bidders to absorb warranty and spares costs; in practice FFPs now represent a growing share of major 2024 procurement awards as buyers push risk transfer. Cost-plus deals ease price pressure but require full cost transparency and audit access. Incentive fees—commonly 5–15%—link payout to availability and MTBF, increasing buyer oversight, while remedies and liquidated damages strengthen purchaser leverage.

Lifecycle and sustainment leverage

- Spare parts leverage

- Design openness via commonality

- Supplier-held obsolescence risk

- Multi-year options as bargaining chips

Geopolitics and offsets

Industrial participation requirements—for example India’s defence offset policy mandating 30% local content on qualifying deals—force tech transfer and local sourcing, while export approvals and national‑security reviews (eg ITAR/EAR) add months to closing and reshape contractual protections. Procurement budget stop‑go cycles create pricing pressure during lulls, though urgent operational needs can temporarily weaken buyer leverage.

- Offsets: India 30% local content

- Export reviews: add months, reshape terms

- Budget cycles: stop‑go pricing pressure

- Urgent ops: temporary buyer softness

Buyers hold pre-award leverage; requal > $1m, sustain 70-80%

Defense buyers (US DoD $858B FY2024, plus OEM primes) exert strong pre-award leverage via competitive tenders, FFP/perf‑based contracts and offsets, while post-award requalification costs (> $1m per platform) and 70–80% lifecycle sustainment shares reduce buyer power over spares/upgrades.

| Driver | Metric | 2024 |

|---|---|---|

| Major buyer spend | US DoD | $858B |

| Lifecycle sustainment | % of program cost | 70–80% |

| Qualification cost | Per platform | >$1m |

| Offsets | India local content | 30% |

What You See Is What You Get

Horstman Porter's Five Forces Analysis

This Horstman Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase, with no placeholders or mockups. It contains a complete, professional evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes. You’ll be able to download and use this same file instantly upon payment.

A Must-Have Tool for Decision-Makers

Horstman's competitive landscape shows concentrated supplier leverage, moderate buyer power, and significant rivalry shaping margins and growth prospects. Our snapshot highlights key pressures—from substitute threats to entry barriers—that influence pricing and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Horstman’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials and components

Horstman depends on high-spec steels, titanium, precision seals, hydro-pneumatic valves, accumulators and advanced dampers sourced from fewer than 5 qualified suppliers, giving those vendors outsized leverage. Supplier concentration plus AS9100/ITAR-style defense certifications raise bargaining power, while qualification timelines of 12–24 months and the mission-critical cost of quality lapses (programs commonly worth millions) sharply increase switching costs.

Compliance and export controls

ITAR and EAR controls, plus NATO AQAP 2110 and defense quality standards as of 2024 narrow the approved vendor pool, concentrating supply power among compliant firms.

Compliance overhead—extended due diligence, facility audits and export licensing—makes onboarding slow and costly, letting incumbent vendors demand firmer commercial terms.

Stringent documentation and traceability requirements increase switching costs and give suppliers with proven audit histories greater negotiating leverage.

Process and testing intensity

Heat treatment, precision machining, NDT and endurance testing are key bottlenecks: 2024 industry data show surge lead times stretching to 6–12 weeks and testing rig availability cutting effective throughput by about 30%, giving specialized suppliers bargaining power. Limited access to calibration labs and bespoke test rigs concentrates leverage with a handful of vendors, while expedited slots in 2024 attracted premiums of roughly 25–50%, pressuring input costs and delivery schedules.

Mitigation via partnerships

- Long-term agreements: stabilize pricing and capacity

- Dual-sourcing: lowers dependency and supply risk

- VAVE: trims supplier margins via cost reduction

- Co-development/shared IP: aligns incentives for custom parts

- Forecast visibility (FY2024 DoD ~858B): improves planning

- Sole-source items: retain supplier leverage

Macroeconomic and energy sensitivity

- Rapid pass-through: higher input-cost realization

- Indexation clauses: locked escalators

- Currency risk: ~10% USD strength impact (2024)

- Supplier leverage: stronger on price and contract terms

Fewer than 5 suppliers, 12–24 month quals and 25–50% expedite premiums

Supplier concentration (<5 qualified vendors), defense certifications (AS9100/ITAR/AQAP) and 12–24 month qualifications give suppliers strong leverage; 6–12 week bottlenecks and 25–50% expedited premiums raise costs and switching frictions. Long-term contracts, dual-sourcing and co-development lower but do not eliminate supplier power; DoD FY2024 ~858B and Brent ~$86/bbl affect demand and input costs.

| Metric | 2024 Value |

|---|---|

| Qualified suppliers | <5 |

| Qualification time | 12–24 months |

| Lead times | 6–12 weeks |

| Expedite premium | 25–50% |

| DoD budget | $858B |

| Brent | $86/bbl |

| USD strength | ~10% |

What is included in the product

Comprehensive Porter’s Five Forces assessment for Horstman, uncovering competitive intensity, buyer and supplier leverage, entry barriers, substitutes, and disruptive threats to its market position.

A concise Horstman Porter’s Five Forces one-sheet that distills competitive pressure into clear scores and a radar view—ideal for quick strategic decisions and seamless slide integration.

Customers Bargaining Power

Concentrated buyers and primes

Defense ministries and a handful of OEM primes (Lockheed, Boeing, Northrop, Raytheon, BAE) dominate demand, with the US DoD alone at about $858 billion in FY2024, giving buyers scale and program control that drives strong bargaining power. Primes bundle subsystems across programs and use competitive tenders and frame agreements to compress supplier pricing. Strict past-performance prerequisites further limit supplier leverage in negotiations.

High switching and integration costs

Suspension systems are platform-integrated, directly affecting mobility, survivability and logistics, so qualification cycles typically run 12–36 months and certification costs commonly exceed $1m per platform. Once qualified, buyers face costly requalification and retrofit logistics that can exceed $5m in program costs, reducing buyer power after award. Pre-award, buyers exploit competition to extract price, lead-time and warranty concessions.

Contract structures and risk allocation

Firm-fixed-price and performance-based logistics contracts shift cost and reliability risk to suppliers, forcing bidders to absorb warranty and spares costs; in practice FFPs now represent a growing share of major 2024 procurement awards as buyers push risk transfer. Cost-plus deals ease price pressure but require full cost transparency and audit access. Incentive fees—commonly 5–15%—link payout to availability and MTBF, increasing buyer oversight, while remedies and liquidated damages strengthen purchaser leverage.

Lifecycle and sustainment leverage

- Spare parts leverage

- Design openness via commonality

- Supplier-held obsolescence risk

- Multi-year options as bargaining chips

Geopolitics and offsets

Industrial participation requirements—for example India’s defence offset policy mandating 30% local content on qualifying deals—force tech transfer and local sourcing, while export approvals and national‑security reviews (eg ITAR/EAR) add months to closing and reshape contractual protections. Procurement budget stop‑go cycles create pricing pressure during lulls, though urgent operational needs can temporarily weaken buyer leverage.

- Offsets: India 30% local content

- Export reviews: add months, reshape terms

- Budget cycles: stop‑go pricing pressure

- Urgent ops: temporary buyer softness

Buyers hold pre-award leverage; requal > $1m, sustain 70-80%

Defense buyers (US DoD $858B FY2024, plus OEM primes) exert strong pre-award leverage via competitive tenders, FFP/perf‑based contracts and offsets, while post-award requalification costs (> $1m per platform) and 70–80% lifecycle sustainment shares reduce buyer power over spares/upgrades.

| Driver | Metric | 2024 |

|---|---|---|

| Major buyer spend | US DoD | $858B |

| Lifecycle sustainment | % of program cost | 70–80% |

| Qualification cost | Per platform | >$1m |

| Offsets | India local content | 30% |

What You See Is What You Get

Horstman Porter's Five Forces Analysis

This Horstman Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase, with no placeholders or mockups. It contains a complete, professional evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes. You’ll be able to download and use this same file instantly upon payment.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Horstman's competitive landscape shows concentrated supplier leverage, moderate buyer power, and significant rivalry shaping margins and growth prospects. Our snapshot highlights key pressures—from substitute threats to entry barriers—that influence pricing and strategic choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Horstman’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials and components

Horstman depends on high-spec steels, titanium, precision seals, hydro-pneumatic valves, accumulators and advanced dampers sourced from fewer than 5 qualified suppliers, giving those vendors outsized leverage. Supplier concentration plus AS9100/ITAR-style defense certifications raise bargaining power, while qualification timelines of 12–24 months and the mission-critical cost of quality lapses (programs commonly worth millions) sharply increase switching costs.

Compliance and export controls

ITAR and EAR controls, plus NATO AQAP 2110 and defense quality standards as of 2024 narrow the approved vendor pool, concentrating supply power among compliant firms.

Compliance overhead—extended due diligence, facility audits and export licensing—makes onboarding slow and costly, letting incumbent vendors demand firmer commercial terms.

Stringent documentation and traceability requirements increase switching costs and give suppliers with proven audit histories greater negotiating leverage.

Process and testing intensity

Heat treatment, precision machining, NDT and endurance testing are key bottlenecks: 2024 industry data show surge lead times stretching to 6–12 weeks and testing rig availability cutting effective throughput by about 30%, giving specialized suppliers bargaining power. Limited access to calibration labs and bespoke test rigs concentrates leverage with a handful of vendors, while expedited slots in 2024 attracted premiums of roughly 25–50%, pressuring input costs and delivery schedules.

Mitigation via partnerships

- Long-term agreements: stabilize pricing and capacity

- Dual-sourcing: lowers dependency and supply risk

- VAVE: trims supplier margins via cost reduction

- Co-development/shared IP: aligns incentives for custom parts

- Forecast visibility (FY2024 DoD ~858B): improves planning

- Sole-source items: retain supplier leverage

Macroeconomic and energy sensitivity

- Rapid pass-through: higher input-cost realization

- Indexation clauses: locked escalators

- Currency risk: ~10% USD strength impact (2024)

- Supplier leverage: stronger on price and contract terms

Fewer than 5 suppliers, 12–24 month quals and 25–50% expedite premiums

Supplier concentration (<5 qualified vendors), defense certifications (AS9100/ITAR/AQAP) and 12–24 month qualifications give suppliers strong leverage; 6–12 week bottlenecks and 25–50% expedited premiums raise costs and switching frictions. Long-term contracts, dual-sourcing and co-development lower but do not eliminate supplier power; DoD FY2024 ~858B and Brent ~$86/bbl affect demand and input costs.

| Metric | 2024 Value |

|---|---|

| Qualified suppliers | <5 |

| Qualification time | 12–24 months |

| Lead times | 6–12 weeks |

| Expedite premium | 25–50% |

| DoD budget | $858B |

| Brent | $86/bbl |

| USD strength | ~10% |

What is included in the product

Comprehensive Porter’s Five Forces assessment for Horstman, uncovering competitive intensity, buyer and supplier leverage, entry barriers, substitutes, and disruptive threats to its market position.

A concise Horstman Porter’s Five Forces one-sheet that distills competitive pressure into clear scores and a radar view—ideal for quick strategic decisions and seamless slide integration.

Customers Bargaining Power

Concentrated buyers and primes

Defense ministries and a handful of OEM primes (Lockheed, Boeing, Northrop, Raytheon, BAE) dominate demand, with the US DoD alone at about $858 billion in FY2024, giving buyers scale and program control that drives strong bargaining power. Primes bundle subsystems across programs and use competitive tenders and frame agreements to compress supplier pricing. Strict past-performance prerequisites further limit supplier leverage in negotiations.

High switching and integration costs

Suspension systems are platform-integrated, directly affecting mobility, survivability and logistics, so qualification cycles typically run 12–36 months and certification costs commonly exceed $1m per platform. Once qualified, buyers face costly requalification and retrofit logistics that can exceed $5m in program costs, reducing buyer power after award. Pre-award, buyers exploit competition to extract price, lead-time and warranty concessions.

Contract structures and risk allocation

Firm-fixed-price and performance-based logistics contracts shift cost and reliability risk to suppliers, forcing bidders to absorb warranty and spares costs; in practice FFPs now represent a growing share of major 2024 procurement awards as buyers push risk transfer. Cost-plus deals ease price pressure but require full cost transparency and audit access. Incentive fees—commonly 5–15%—link payout to availability and MTBF, increasing buyer oversight, while remedies and liquidated damages strengthen purchaser leverage.

Lifecycle and sustainment leverage

- Spare parts leverage

- Design openness via commonality

- Supplier-held obsolescence risk

- Multi-year options as bargaining chips

Geopolitics and offsets

Industrial participation requirements—for example India’s defence offset policy mandating 30% local content on qualifying deals—force tech transfer and local sourcing, while export approvals and national‑security reviews (eg ITAR/EAR) add months to closing and reshape contractual protections. Procurement budget stop‑go cycles create pricing pressure during lulls, though urgent operational needs can temporarily weaken buyer leverage.

- Offsets: India 30% local content

- Export reviews: add months, reshape terms

- Budget cycles: stop‑go pricing pressure

- Urgent ops: temporary buyer softness

Buyers hold pre-award leverage; requal > $1m, sustain 70-80%

Defense buyers (US DoD $858B FY2024, plus OEM primes) exert strong pre-award leverage via competitive tenders, FFP/perf‑based contracts and offsets, while post-award requalification costs (> $1m per platform) and 70–80% lifecycle sustainment shares reduce buyer power over spares/upgrades.

| Driver | Metric | 2024 |

|---|---|---|

| Major buyer spend | US DoD | $858B |

| Lifecycle sustainment | % of program cost | 70–80% |

| Qualification cost | Per platform | >$1m |

| Offsets | India local content | 30% |

What You See Is What You Get

Horstman Porter's Five Forces Analysis

This Horstman Porter’s Five Forces Analysis preview is the exact, fully formatted document you’ll receive immediately after purchase, with no placeholders or mockups. It contains a complete, professional evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitutes. You’ll be able to download and use this same file instantly upon payment.