HPB Business Model Canvas

Unlock a strategic Business Model Canvas: concise value, revenue and scaling playbook

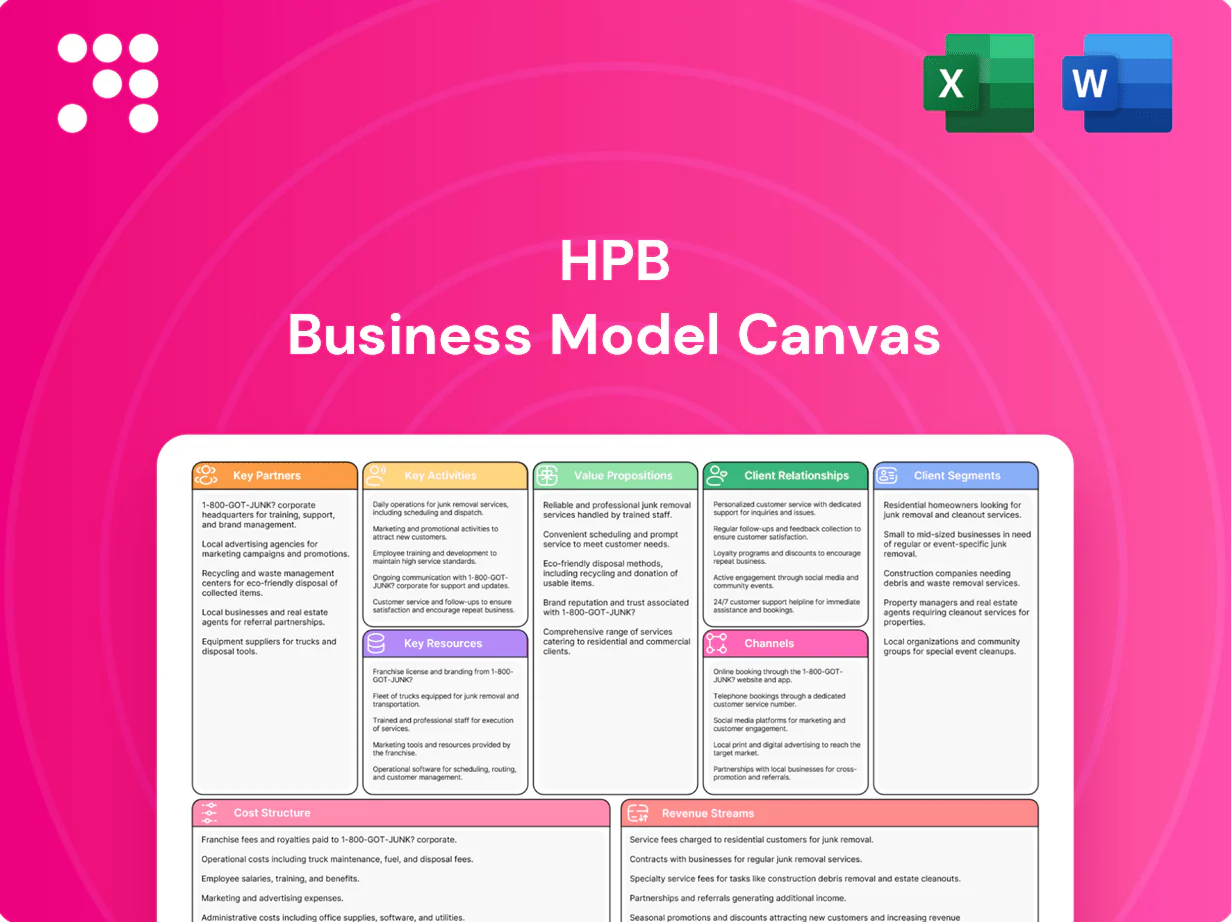

Unlock HPB's strategic blueprint with our concise Business Model Canvas. This full version maps value propositions, customer segments, revenue engines and cost drivers to show how HPB wins and scales. Perfect for investors, founders and consultants seeking actionable insights. Download the editable Word/Excel files to benchmark or adapt these proven tactics.

Partnerships

Hrvatska Pošta distribution

Leveraging Hrvatska Pošta's network of over 1,000 post offices across Croatia extends HPB reach into smaller towns and rural areas, covering a population of about 3.9 million (2024). Shared locations provide basic banking services and customer onboarding, lowering acquisition costs while boosting convenience. The partnership strengthens HPB brand visibility nationwide and improves access in underserved municipalities.

Card schemes (Visa, Mastercard)

Global card schemes (Visa, Mastercard) enable issuing and acquiring across 200+ countries and territories and 100M+ merchant locations, providing PCI DSS security standards and formal dispute-resolution frameworks; co-marketing programs drive card adoption and spend while interchange fees and scheme incentives (rebates, volume bonuses) materially improve issuer and acquirer economics.

Fintechs and core banking vendors

Technology partners accelerate digital feature rollout for HPB, with APIs, core systems, and analytics improving speed, reliability and personalization; fintech collaboration can cut time-to-market for new services and expand product breadth. Managed services can optimize IT cost and resilience—Gartner (2024) found managed services often reduce IT costs by 20–30% while improving uptime and scalability.

Correspondent and partner banks

Correspondent and partner banks enable HPB to execute cross-border payments and trade finance, supporting FX liquidity and settlement essential for Croatian clients to transact globally. BIS data shows global daily FX turnover at about 7.5 trillion USD (2022), while World Bank noted a ~20 percent decline in correspondent relationships since 2011, making targeted partnerships strategic.

- cross-border payments

- trade finance support

- FX liquidity & settlement

- diversified funding & risk-sharing

Regulators and credit bureaus

Close cooperation with HNB, HANFA and compliance bodies in 2024 ensures HPB adheres to evolving regulatory standards, reducing enforcement and conduct risk while aligning with EU supervisory expectations. Credit bureaus supply timely borrower data for underwriting and ongoing monitoring, improving loss forecasting and portfolio segmentation. This data-driven oversight lowers credit risk and enhances portfolio quality, while transparent governance sustains long-term trust.

- Regulatory alignment: HNB/HANFA oversight (2024)

- Data source: credit bureaus for underwriting/monitoring

- Impact: lower default risk, stronger portfolio metrics

- Governance: transparency drives depositor/investor confidence

Postal network reaches ~3.9M; global card acceptance and IT partners cut costs, speed rollout

HPB leverages 1,000+ Hrvatska Pošta branches to reach ~3.9M people (2024), lowering acquisition costs and improving rural access. Card schemes (Visa, Mastercard) provide acceptance in 200+ countries and 100M+ merchant locations, improving interchange economics. Tech partners cut IT costs 20–30% (Gartner 2024) and speed digital rollout; correspondent banks support FX and trade amid ~20% decline in relationships since 2011.

| Partner | Role | Key metric | Impact |

|---|---|---|---|

| Hrvatska Pošta | Distribution | 1,000+ branches; 3.9M pop (2024) | Lower CAC; rural access |

| Card schemes | Payments | 200+ countries; 100M+ merchants | Revenue; acceptance |

| Tech partners | Digital/IT | -20–30% IT cost (Gartner 2024) | Faster launch; resilience |

| Correspondent banks | Cross-border | FX turnover $7.5T/day (2022) | Settlement; liquidity |

| Regulators & bureaus | Compliance/Data | HNB/HANFA oversight (2024) | Lower conduct/credit risk |

What is included in the product

Comprehensive HPB Business Model Canvas organized into the 9 classic blocks, detailing customer segments, channels, value propositions and operations; includes competitive analysis, SWOT-linked insights and polished narrative ideal for investor presentations and decision-making.

Streamlines strategic planning with a clean, editable one-page Business Model Canvas that saves hours of formatting, clarifies core components for quick review, and enables effortless team collaboration and side-by-side comparisons.

Activities

Deposit gathering

Attracting current and savings accounts provides HPB with stable, low-cost funding; in 2024 banks prioritized deposit stability amid tightening markets. Pricing, targeted campaigns and advisory services drive balance growth and customer stickiness. Active liquidity management aligns deposit maturities with lending needs and regulatory LCR requirements. Segmented offers improve retention and reduce overall cost of funds.

Lending and underwriting

Consumer, mortgage, SME and corporate lending drive HPB interest income, with higher lending yields in a 2024 rate environment where the ECB policy rate was around 4%.

Risk-based pricing and robust scoring models preserve margins by differentiating spreads across credit tiers and limiting loss given default.

Ongoing monitoring and early-warning DELTA metrics sustain asset quality while efficient end-to-end processing shortens turnaround times and raises customer satisfaction.

Payments and cash management

Executing SEPA, card, instant and domestic transfers is core — SEPA covers 36 countries and roughly 450 million people (2024). For businesses, cash pooling, collections and reconciliation add measurable treasury value and stickiness. Reliability matters: industry SLAs target 99.9–99.99% uptime to preserve trust. Fee income scales with volume; a 0.1% take on €10bn generates €10m.

Digital product development

- eKYC: faster onboarding

- PFM: higher retention

- Analytics: personalized NBA

- UX: increased adoption & cross-sell

Risk, compliance, and treasury

ALM balances liquidity, interest-rate and currency risks to meet Basel III minimums (LCR and NSFR ≥100%); portfolio rebalancing uses money‑market and repo operations. AML/KYC, fraud prevention and regulatory reporting follow FATF recommendations and local laws to safeguard operations. Hedging and investments (FX forwards, IRS, short-term securities) optimize surplus returns while stress testing (severe plausible scenarios) sustains resilience.

- ALM: LCR/NSFR ≥100%

- Compliance: FATF-aligned AML/KYC

- Hedging: FX, IRS, repos

- Resilience: regular stress tests

Deposits fund lending at ~4%; pricing, scoring & payments protect margins

Stable deposits fund lending in a 2024 ECB rate ~4%; targeted pricing and campaigns boost stickiness. Risk-based pricing, scoring and DELTA monitoring protect margins and asset quality. Payments, digital banking and ALM (LCR/NSFR ≥100%) deliver fee income, efficiency and resilience.

| Metric | 2024 value |

|---|---|

| ECB policy rate | ~4% |

| SEPA coverage | 36 countries / 450M |

| Mobile banking users | 4.7B |

| Fee example | 0.1% of €10bn = €10M |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact HPB Business Model Canvas you'll receive; it's not a mockup or sample. Upon purchase you'll get the complete, editable file identical in structure and content, formatted for immediate use in Word and Excel. No hidden pages or surprises—ready to present, customize, and implement.

Unlock a strategic Business Model Canvas: concise value, revenue and scaling playbook

Unlock HPB's strategic blueprint with our concise Business Model Canvas. This full version maps value propositions, customer segments, revenue engines and cost drivers to show how HPB wins and scales. Perfect for investors, founders and consultants seeking actionable insights. Download the editable Word/Excel files to benchmark or adapt these proven tactics.

Partnerships

Hrvatska Pošta distribution

Leveraging Hrvatska Pošta's network of over 1,000 post offices across Croatia extends HPB reach into smaller towns and rural areas, covering a population of about 3.9 million (2024). Shared locations provide basic banking services and customer onboarding, lowering acquisition costs while boosting convenience. The partnership strengthens HPB brand visibility nationwide and improves access in underserved municipalities.

Card schemes (Visa, Mastercard)

Global card schemes (Visa, Mastercard) enable issuing and acquiring across 200+ countries and territories and 100M+ merchant locations, providing PCI DSS security standards and formal dispute-resolution frameworks; co-marketing programs drive card adoption and spend while interchange fees and scheme incentives (rebates, volume bonuses) materially improve issuer and acquirer economics.

Fintechs and core banking vendors

Technology partners accelerate digital feature rollout for HPB, with APIs, core systems, and analytics improving speed, reliability and personalization; fintech collaboration can cut time-to-market for new services and expand product breadth. Managed services can optimize IT cost and resilience—Gartner (2024) found managed services often reduce IT costs by 20–30% while improving uptime and scalability.

Correspondent and partner banks

Correspondent and partner banks enable HPB to execute cross-border payments and trade finance, supporting FX liquidity and settlement essential for Croatian clients to transact globally. BIS data shows global daily FX turnover at about 7.5 trillion USD (2022), while World Bank noted a ~20 percent decline in correspondent relationships since 2011, making targeted partnerships strategic.

- cross-border payments

- trade finance support

- FX liquidity & settlement

- diversified funding & risk-sharing

Regulators and credit bureaus

Close cooperation with HNB, HANFA and compliance bodies in 2024 ensures HPB adheres to evolving regulatory standards, reducing enforcement and conduct risk while aligning with EU supervisory expectations. Credit bureaus supply timely borrower data for underwriting and ongoing monitoring, improving loss forecasting and portfolio segmentation. This data-driven oversight lowers credit risk and enhances portfolio quality, while transparent governance sustains long-term trust.

- Regulatory alignment: HNB/HANFA oversight (2024)

- Data source: credit bureaus for underwriting/monitoring

- Impact: lower default risk, stronger portfolio metrics

- Governance: transparency drives depositor/investor confidence

Postal network reaches ~3.9M; global card acceptance and IT partners cut costs, speed rollout

HPB leverages 1,000+ Hrvatska Pošta branches to reach ~3.9M people (2024), lowering acquisition costs and improving rural access. Card schemes (Visa, Mastercard) provide acceptance in 200+ countries and 100M+ merchant locations, improving interchange economics. Tech partners cut IT costs 20–30% (Gartner 2024) and speed digital rollout; correspondent banks support FX and trade amid ~20% decline in relationships since 2011.

| Partner | Role | Key metric | Impact |

|---|---|---|---|

| Hrvatska Pošta | Distribution | 1,000+ branches; 3.9M pop (2024) | Lower CAC; rural access |

| Card schemes | Payments | 200+ countries; 100M+ merchants | Revenue; acceptance |

| Tech partners | Digital/IT | -20–30% IT cost (Gartner 2024) | Faster launch; resilience |

| Correspondent banks | Cross-border | FX turnover $7.5T/day (2022) | Settlement; liquidity |

| Regulators & bureaus | Compliance/Data | HNB/HANFA oversight (2024) | Lower conduct/credit risk |

What is included in the product

Comprehensive HPB Business Model Canvas organized into the 9 classic blocks, detailing customer segments, channels, value propositions and operations; includes competitive analysis, SWOT-linked insights and polished narrative ideal for investor presentations and decision-making.

Streamlines strategic planning with a clean, editable one-page Business Model Canvas that saves hours of formatting, clarifies core components for quick review, and enables effortless team collaboration and side-by-side comparisons.

Activities

Deposit gathering

Attracting current and savings accounts provides HPB with stable, low-cost funding; in 2024 banks prioritized deposit stability amid tightening markets. Pricing, targeted campaigns and advisory services drive balance growth and customer stickiness. Active liquidity management aligns deposit maturities with lending needs and regulatory LCR requirements. Segmented offers improve retention and reduce overall cost of funds.

Lending and underwriting

Consumer, mortgage, SME and corporate lending drive HPB interest income, with higher lending yields in a 2024 rate environment where the ECB policy rate was around 4%.

Risk-based pricing and robust scoring models preserve margins by differentiating spreads across credit tiers and limiting loss given default.

Ongoing monitoring and early-warning DELTA metrics sustain asset quality while efficient end-to-end processing shortens turnaround times and raises customer satisfaction.

Payments and cash management

Executing SEPA, card, instant and domestic transfers is core — SEPA covers 36 countries and roughly 450 million people (2024). For businesses, cash pooling, collections and reconciliation add measurable treasury value and stickiness. Reliability matters: industry SLAs target 99.9–99.99% uptime to preserve trust. Fee income scales with volume; a 0.1% take on €10bn generates €10m.

Digital product development

- eKYC: faster onboarding

- PFM: higher retention

- Analytics: personalized NBA

- UX: increased adoption & cross-sell

Risk, compliance, and treasury

ALM balances liquidity, interest-rate and currency risks to meet Basel III minimums (LCR and NSFR ≥100%); portfolio rebalancing uses money‑market and repo operations. AML/KYC, fraud prevention and regulatory reporting follow FATF recommendations and local laws to safeguard operations. Hedging and investments (FX forwards, IRS, short-term securities) optimize surplus returns while stress testing (severe plausible scenarios) sustains resilience.

- ALM: LCR/NSFR ≥100%

- Compliance: FATF-aligned AML/KYC

- Hedging: FX, IRS, repos

- Resilience: regular stress tests

Deposits fund lending at ~4%; pricing, scoring & payments protect margins

Stable deposits fund lending in a 2024 ECB rate ~4%; targeted pricing and campaigns boost stickiness. Risk-based pricing, scoring and DELTA monitoring protect margins and asset quality. Payments, digital banking and ALM (LCR/NSFR ≥100%) deliver fee income, efficiency and resilience.

| Metric | 2024 value |

|---|---|

| ECB policy rate | ~4% |

| SEPA coverage | 36 countries / 450M |

| Mobile banking users | 4.7B |

| Fee example | 0.1% of €10bn = €10M |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact HPB Business Model Canvas you'll receive; it's not a mockup or sample. Upon purchase you'll get the complete, editable file identical in structure and content, formatted for immediate use in Word and Excel. No hidden pages or surprises—ready to present, customize, and implement.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a strategic Business Model Canvas: concise value, revenue and scaling playbook

Unlock HPB's strategic blueprint with our concise Business Model Canvas. This full version maps value propositions, customer segments, revenue engines and cost drivers to show how HPB wins and scales. Perfect for investors, founders and consultants seeking actionable insights. Download the editable Word/Excel files to benchmark or adapt these proven tactics.

Partnerships

Hrvatska Pošta distribution

Leveraging Hrvatska Pošta's network of over 1,000 post offices across Croatia extends HPB reach into smaller towns and rural areas, covering a population of about 3.9 million (2024). Shared locations provide basic banking services and customer onboarding, lowering acquisition costs while boosting convenience. The partnership strengthens HPB brand visibility nationwide and improves access in underserved municipalities.

Card schemes (Visa, Mastercard)

Global card schemes (Visa, Mastercard) enable issuing and acquiring across 200+ countries and territories and 100M+ merchant locations, providing PCI DSS security standards and formal dispute-resolution frameworks; co-marketing programs drive card adoption and spend while interchange fees and scheme incentives (rebates, volume bonuses) materially improve issuer and acquirer economics.

Fintechs and core banking vendors

Technology partners accelerate digital feature rollout for HPB, with APIs, core systems, and analytics improving speed, reliability and personalization; fintech collaboration can cut time-to-market for new services and expand product breadth. Managed services can optimize IT cost and resilience—Gartner (2024) found managed services often reduce IT costs by 20–30% while improving uptime and scalability.

Correspondent and partner banks

Correspondent and partner banks enable HPB to execute cross-border payments and trade finance, supporting FX liquidity and settlement essential for Croatian clients to transact globally. BIS data shows global daily FX turnover at about 7.5 trillion USD (2022), while World Bank noted a ~20 percent decline in correspondent relationships since 2011, making targeted partnerships strategic.

- cross-border payments

- trade finance support

- FX liquidity & settlement

- diversified funding & risk-sharing

Regulators and credit bureaus

Close cooperation with HNB, HANFA and compliance bodies in 2024 ensures HPB adheres to evolving regulatory standards, reducing enforcement and conduct risk while aligning with EU supervisory expectations. Credit bureaus supply timely borrower data for underwriting and ongoing monitoring, improving loss forecasting and portfolio segmentation. This data-driven oversight lowers credit risk and enhances portfolio quality, while transparent governance sustains long-term trust.

- Regulatory alignment: HNB/HANFA oversight (2024)

- Data source: credit bureaus for underwriting/monitoring

- Impact: lower default risk, stronger portfolio metrics

- Governance: transparency drives depositor/investor confidence

Postal network reaches ~3.9M; global card acceptance and IT partners cut costs, speed rollout

HPB leverages 1,000+ Hrvatska Pošta branches to reach ~3.9M people (2024), lowering acquisition costs and improving rural access. Card schemes (Visa, Mastercard) provide acceptance in 200+ countries and 100M+ merchant locations, improving interchange economics. Tech partners cut IT costs 20–30% (Gartner 2024) and speed digital rollout; correspondent banks support FX and trade amid ~20% decline in relationships since 2011.

| Partner | Role | Key metric | Impact |

|---|---|---|---|

| Hrvatska Pošta | Distribution | 1,000+ branches; 3.9M pop (2024) | Lower CAC; rural access |

| Card schemes | Payments | 200+ countries; 100M+ merchants | Revenue; acceptance |

| Tech partners | Digital/IT | -20–30% IT cost (Gartner 2024) | Faster launch; resilience |

| Correspondent banks | Cross-border | FX turnover $7.5T/day (2022) | Settlement; liquidity |

| Regulators & bureaus | Compliance/Data | HNB/HANFA oversight (2024) | Lower conduct/credit risk |

What is included in the product

Comprehensive HPB Business Model Canvas organized into the 9 classic blocks, detailing customer segments, channels, value propositions and operations; includes competitive analysis, SWOT-linked insights and polished narrative ideal for investor presentations and decision-making.

Streamlines strategic planning with a clean, editable one-page Business Model Canvas that saves hours of formatting, clarifies core components for quick review, and enables effortless team collaboration and side-by-side comparisons.

Activities

Deposit gathering

Attracting current and savings accounts provides HPB with stable, low-cost funding; in 2024 banks prioritized deposit stability amid tightening markets. Pricing, targeted campaigns and advisory services drive balance growth and customer stickiness. Active liquidity management aligns deposit maturities with lending needs and regulatory LCR requirements. Segmented offers improve retention and reduce overall cost of funds.

Lending and underwriting

Consumer, mortgage, SME and corporate lending drive HPB interest income, with higher lending yields in a 2024 rate environment where the ECB policy rate was around 4%.

Risk-based pricing and robust scoring models preserve margins by differentiating spreads across credit tiers and limiting loss given default.

Ongoing monitoring and early-warning DELTA metrics sustain asset quality while efficient end-to-end processing shortens turnaround times and raises customer satisfaction.

Payments and cash management

Executing SEPA, card, instant and domestic transfers is core — SEPA covers 36 countries and roughly 450 million people (2024). For businesses, cash pooling, collections and reconciliation add measurable treasury value and stickiness. Reliability matters: industry SLAs target 99.9–99.99% uptime to preserve trust. Fee income scales with volume; a 0.1% take on €10bn generates €10m.

Digital product development

- eKYC: faster onboarding

- PFM: higher retention

- Analytics: personalized NBA

- UX: increased adoption & cross-sell

Risk, compliance, and treasury

ALM balances liquidity, interest-rate and currency risks to meet Basel III minimums (LCR and NSFR ≥100%); portfolio rebalancing uses money‑market and repo operations. AML/KYC, fraud prevention and regulatory reporting follow FATF recommendations and local laws to safeguard operations. Hedging and investments (FX forwards, IRS, short-term securities) optimize surplus returns while stress testing (severe plausible scenarios) sustains resilience.

- ALM: LCR/NSFR ≥100%

- Compliance: FATF-aligned AML/KYC

- Hedging: FX, IRS, repos

- Resilience: regular stress tests

Deposits fund lending at ~4%; pricing, scoring & payments protect margins

Stable deposits fund lending in a 2024 ECB rate ~4%; targeted pricing and campaigns boost stickiness. Risk-based pricing, scoring and DELTA monitoring protect margins and asset quality. Payments, digital banking and ALM (LCR/NSFR ≥100%) deliver fee income, efficiency and resilience.

| Metric | 2024 value |

|---|---|

| ECB policy rate | ~4% |

| SEPA coverage | 36 countries / 450M |

| Mobile banking users | 4.7B |

| Fee example | 0.1% of €10bn = €10M |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact HPB Business Model Canvas you'll receive; it's not a mockup or sample. Upon purchase you'll get the complete, editable file identical in structure and content, formatted for immediate use in Word and Excel. No hidden pages or surprises—ready to present, customize, and implement.