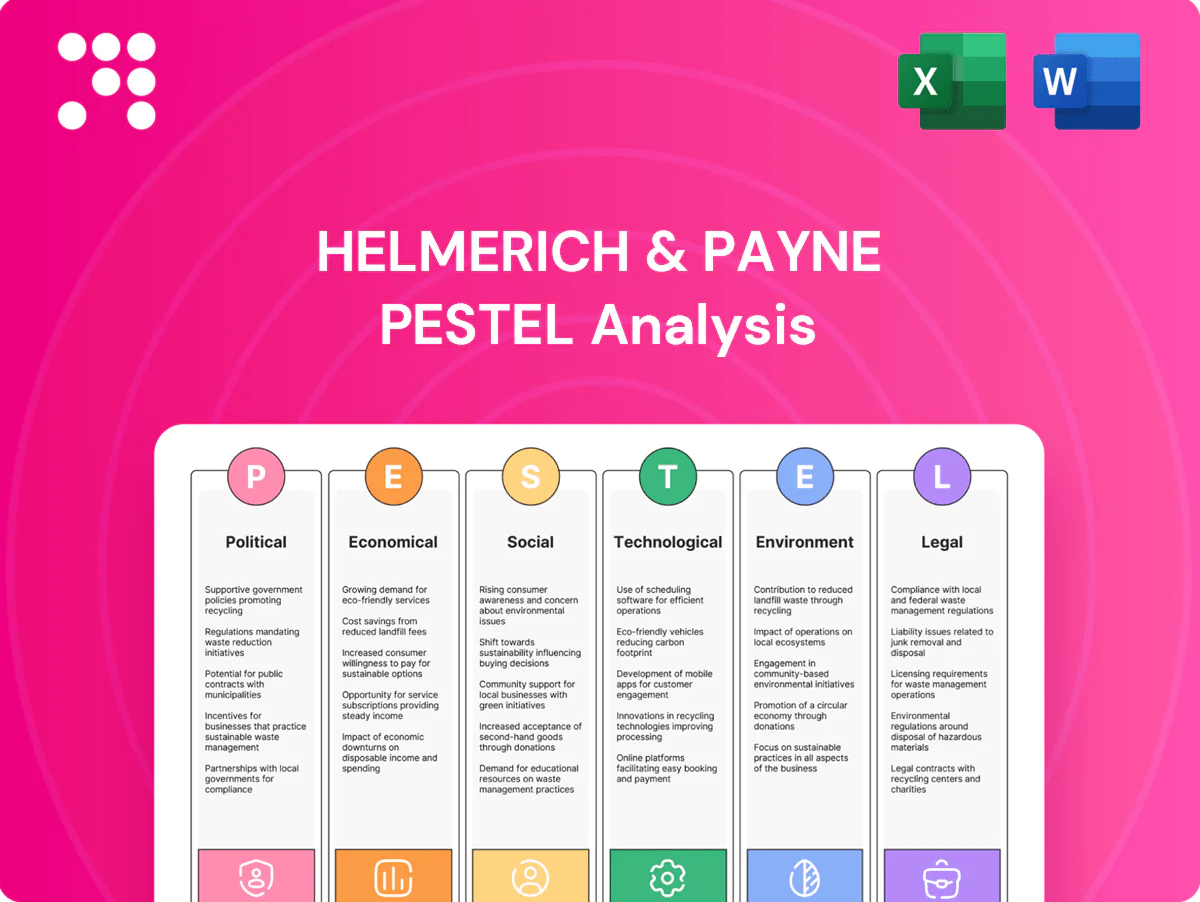

Helmerich & Payne PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Understand how political, economic and technological forces shape Helmerich & Payne's drilling and services outlook in our concise PESTLE overview. We highlight regulatory risks, commodity cycles, ESG pressures and innovation trends that could alter margins and market share. Buy the full PESTLE for a detailed, editable report you can use in investment models, strategy decks, or board discussions.

Political factors

Energy policy shifts and permitting

Changes in federal and state drilling permits, NEPA reviews (environmental assessments often 6–12 months; environmental impact statements commonly 3–7 years) and public land leasing timelines can accelerate or delay rig deployments, directly affecting Helmerich & Payne utilization and scheduling. H&P must navigate differing permit windows and compliance across jurisdictions; faster approvals boost rig utilization while tighter rules raise compliance costs and project risk. Strategic planning requires scenario buffers for policy swings and timeline variability.

Geopolitical stability and OPEC+ decisions

OPEC+ supply-management moves and geopolitical disruptions drive oil-price volatility—Brent averaged about $86/bbl in 2024—directly affecting E&P capex and rig demand, with higher prices lifting utilization while mid-year shocks can stall programs. H&P’s operations across North America, Latin America and the Middle East dilute localized risk, and tracking macro signals lets management reallocate fleets proactively.

Local content and nationalization pressures abroad

International markets often impose local hiring, procurement or JV requirements that can reach up to 50% of project inputs in countries with strict nationalization rules, raising operating costs and timeline uncertainty for Helmerich & Payne (HP).

Compliance alters cost structure and schedule predictability; H&P mitigates this via local training programs and partnerships to transfer skills while maintaining H&P technical standards.

Regulatory missteps can trigger fines, license suspension or contract loss, increasing sovereign risk exposure and potential revenue volatility.

Infrastructure and energy-security priorities

Government focus on domestic energy security—backed by policies like the Inflation Reduction Act (approx. $369 billion in energy/climate spending)—can accelerate pipeline, grid and basin projects, reducing bottlenecks and incentivizing drilling; conversely, strong decarbonization mandates can divert capital away from hydrocarbons, forcing H&P to align rig and service capacity with prevailing policy thrusts.

- Policy tailwinds: IRA $369B boosts infrastructure and transition projects

- Risk: decarbonization can reallocate capex away from drilling

- Action: match rig capacity to policy direction and market demand

Trade, tariffs, and equipment flows

Tariffs such as the US 25% steel and 10% aluminum Section 232 duties and 2022–23 US export controls on advanced electronics raise rig upgrade and spare-part costs and add customs delays that complicate international redeployments; H&P cites supply‑chain diversification and higher on‑site inventory in 2024 filings to mitigate shocks, and contract pricing requires pass‑through clauses where feasible.

- Tariffs: 25% steel, 10% aluminum

- Export controls: 2022–23 US semiconductor rules

- Mitigation: diversification + higher inventory (noted in 2024 filings)

- Action: include pass‑through pricing

Permits delay, local content 50%, Brent $86

Federal/state permit timing (NEPA 6–12m; EIS 3–7y) and local content rules (up to 50%) drive H&P scheduling, costs and JV structures. Brent averaged ~$86/bbl in 2024, moving E&P capex and rig demand. IRA energy/climate funding ~$369B (supporting infrastructure) offsets some decarbonization risk. US tariffs (steel 25%, aluminum 10%) and 2022–23 export controls raise upgrade and spare-part costs.

| Factor | 2024/2025 Data |

|---|---|

| Permits/NEPA | 6–12m; EIS 3–7y |

| Oil price | Brent ~$86/bbl (2024) |

| Policy funding | IRA ~$369B |

| Tariffs | Steel 25%, Al 10% |

| Local content | Up to 50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Helmerich & Payne across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and industry trends. Designed for executives and investors, it highlights region-specific risks and opportunities, provides forward-looking insights for scenario planning, and is formatted for direct inclusion in plans or decks.

A concise, visually segmented PESTLE summary of Helmerich & Payne that’s easily dropped into presentations or shared across teams, enabling quick alignment, clearer external risk discussions, and fast decision-making during planning sessions.

Economic factors

Commodity price cycles and E&P capex

Brent trading near $85/bbl and WTI around $82/bbl in mid‑2025 drives operator spending and uplifts rig dayrates, with Tier‑1 rigs commanding premiums often above $40,000/day. Prolonged upcycles support higher utilization and pricing power; downturns rapidly squeeze margins and idle fleets. H&P benefits from operator preference for high‑spec rigs but remains exposed to customers’ cash flows. Even in strong price tapes, E&P capital discipline has moderated fleet growth.

Inflation and cost-of-service dynamics

Labor, steel and parts inflation — with U.S. CPI 2024 at 3.4% (BLS) and WTI averaging about $80/bbl in 2024 (EIA) — can squeeze H&P margins where contracts lack escalators. Index-linked pricing and rig efficiency gains have offset much input-cost rise, while improved supply-chain reliability cuts downtime and cost overruns. Rigorous cost control preserves returns across cycles.

Interest rates and capital access

Higher interest rates (Fed funds ~5.25–5.50% in 2024–25) raise borrowing costs for Helmerich & Payne and its clients, tempering fleet upgrades and drilling program economics; reduced activity pressure was reflected in a 2024 U.S. land rig backdrop near 700 rigs (Baker Hughes). Lower rates would improve project IRRs and refinancing options. H&P’s strong balance sheet and liquidity enable counter-cyclical investments and strategic rig reactivations.

Utilization mix and dayrate spread

High-spec super-spec rigs command premium dayrates versus legacy assets, often 20–40% higher, lifting H&P's average revenue per day as mix shifts toward automation-ready fleets; industry super-spec utilization exceeded 70% in 2024. Idle or sub-spec rigs depress averages and carry holding costs, and rig-upgrade ROI hinges on sustained multi-quarter demand visibility.

- Premium spread: 20–40%

- Super-spec utilization: >70% (2024)

- Idle rigs: holding-cost drag

- Upgrade ROI: requires sustained demand

USD strength and international earnings

USD strength (DXY ~105 average in 2024) reduces translated international revenues for Helmerich & Payne and weakens local-cost competitiveness, putting pressure on international margins.

Active FX hedging programs and securing contracts denominated in USD where feasible help smooth revenue swings and cut volatility; geographic diversification spreads currency risk across regions.

Permits delay, local content 50%, Brent $86

Brent ~85/bbl and WTI ~82/bbl (mid‑2025) lift dayrates—Tier‑1 rigs >$40k/day—with super‑spec utilization >70% (2024); downturns quickly squeeze margins. U.S. CPI 2024 3.4% and Fed funds ~5.25–5.50% raise costs and temper capex; U.S. land rigs ~700 (2024). DXY ~105 (2024) pressures international revenues; H&P liquidity supports selective reactivations.

| Metric | Value |

|---|---|

| Brent/WTI | 85/82 (mid‑2025) |

| Fed funds | 5.25–5.50% (2024–25) |

| CPI | 3.4% (2024) |

| DXY | ~105 (2024) |

Preview the Actual Deliverable

Helmerich & Payne PESTLE Analysis

The Helmerich & Payne PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are delivered exactly as shown with no placeholders or teasers. What you see is the final, professional file you’ll be able to download immediately after buying.

Plan Smarter. Present Sharper. Compete Stronger.

Understand how political, economic and technological forces shape Helmerich & Payne's drilling and services outlook in our concise PESTLE overview. We highlight regulatory risks, commodity cycles, ESG pressures and innovation trends that could alter margins and market share. Buy the full PESTLE for a detailed, editable report you can use in investment models, strategy decks, or board discussions.

Political factors

Energy policy shifts and permitting

Changes in federal and state drilling permits, NEPA reviews (environmental assessments often 6–12 months; environmental impact statements commonly 3–7 years) and public land leasing timelines can accelerate or delay rig deployments, directly affecting Helmerich & Payne utilization and scheduling. H&P must navigate differing permit windows and compliance across jurisdictions; faster approvals boost rig utilization while tighter rules raise compliance costs and project risk. Strategic planning requires scenario buffers for policy swings and timeline variability.

Geopolitical stability and OPEC+ decisions

OPEC+ supply-management moves and geopolitical disruptions drive oil-price volatility—Brent averaged about $86/bbl in 2024—directly affecting E&P capex and rig demand, with higher prices lifting utilization while mid-year shocks can stall programs. H&P’s operations across North America, Latin America and the Middle East dilute localized risk, and tracking macro signals lets management reallocate fleets proactively.

Local content and nationalization pressures abroad

International markets often impose local hiring, procurement or JV requirements that can reach up to 50% of project inputs in countries with strict nationalization rules, raising operating costs and timeline uncertainty for Helmerich & Payne (HP).

Compliance alters cost structure and schedule predictability; H&P mitigates this via local training programs and partnerships to transfer skills while maintaining H&P technical standards.

Regulatory missteps can trigger fines, license suspension or contract loss, increasing sovereign risk exposure and potential revenue volatility.

Infrastructure and energy-security priorities

Government focus on domestic energy security—backed by policies like the Inflation Reduction Act (approx. $369 billion in energy/climate spending)—can accelerate pipeline, grid and basin projects, reducing bottlenecks and incentivizing drilling; conversely, strong decarbonization mandates can divert capital away from hydrocarbons, forcing H&P to align rig and service capacity with prevailing policy thrusts.

- Policy tailwinds: IRA $369B boosts infrastructure and transition projects

- Risk: decarbonization can reallocate capex away from drilling

- Action: match rig capacity to policy direction and market demand

Trade, tariffs, and equipment flows

Tariffs such as the US 25% steel and 10% aluminum Section 232 duties and 2022–23 US export controls on advanced electronics raise rig upgrade and spare-part costs and add customs delays that complicate international redeployments; H&P cites supply‑chain diversification and higher on‑site inventory in 2024 filings to mitigate shocks, and contract pricing requires pass‑through clauses where feasible.

- Tariffs: 25% steel, 10% aluminum

- Export controls: 2022–23 US semiconductor rules

- Mitigation: diversification + higher inventory (noted in 2024 filings)

- Action: include pass‑through pricing

Permits delay, local content 50%, Brent $86

Federal/state permit timing (NEPA 6–12m; EIS 3–7y) and local content rules (up to 50%) drive H&P scheduling, costs and JV structures. Brent averaged ~$86/bbl in 2024, moving E&P capex and rig demand. IRA energy/climate funding ~$369B (supporting infrastructure) offsets some decarbonization risk. US tariffs (steel 25%, aluminum 10%) and 2022–23 export controls raise upgrade and spare-part costs.

| Factor | 2024/2025 Data |

|---|---|

| Permits/NEPA | 6–12m; EIS 3–7y |

| Oil price | Brent ~$86/bbl (2024) |

| Policy funding | IRA ~$369B |

| Tariffs | Steel 25%, Al 10% |

| Local content | Up to 50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Helmerich & Payne across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and industry trends. Designed for executives and investors, it highlights region-specific risks and opportunities, provides forward-looking insights for scenario planning, and is formatted for direct inclusion in plans or decks.

A concise, visually segmented PESTLE summary of Helmerich & Payne that’s easily dropped into presentations or shared across teams, enabling quick alignment, clearer external risk discussions, and fast decision-making during planning sessions.

Economic factors

Commodity price cycles and E&P capex

Brent trading near $85/bbl and WTI around $82/bbl in mid‑2025 drives operator spending and uplifts rig dayrates, with Tier‑1 rigs commanding premiums often above $40,000/day. Prolonged upcycles support higher utilization and pricing power; downturns rapidly squeeze margins and idle fleets. H&P benefits from operator preference for high‑spec rigs but remains exposed to customers’ cash flows. Even in strong price tapes, E&P capital discipline has moderated fleet growth.

Inflation and cost-of-service dynamics

Labor, steel and parts inflation — with U.S. CPI 2024 at 3.4% (BLS) and WTI averaging about $80/bbl in 2024 (EIA) — can squeeze H&P margins where contracts lack escalators. Index-linked pricing and rig efficiency gains have offset much input-cost rise, while improved supply-chain reliability cuts downtime and cost overruns. Rigorous cost control preserves returns across cycles.

Interest rates and capital access

Higher interest rates (Fed funds ~5.25–5.50% in 2024–25) raise borrowing costs for Helmerich & Payne and its clients, tempering fleet upgrades and drilling program economics; reduced activity pressure was reflected in a 2024 U.S. land rig backdrop near 700 rigs (Baker Hughes). Lower rates would improve project IRRs and refinancing options. H&P’s strong balance sheet and liquidity enable counter-cyclical investments and strategic rig reactivations.

Utilization mix and dayrate spread

High-spec super-spec rigs command premium dayrates versus legacy assets, often 20–40% higher, lifting H&P's average revenue per day as mix shifts toward automation-ready fleets; industry super-spec utilization exceeded 70% in 2024. Idle or sub-spec rigs depress averages and carry holding costs, and rig-upgrade ROI hinges on sustained multi-quarter demand visibility.

- Premium spread: 20–40%

- Super-spec utilization: >70% (2024)

- Idle rigs: holding-cost drag

- Upgrade ROI: requires sustained demand

USD strength and international earnings

USD strength (DXY ~105 average in 2024) reduces translated international revenues for Helmerich & Payne and weakens local-cost competitiveness, putting pressure on international margins.

Active FX hedging programs and securing contracts denominated in USD where feasible help smooth revenue swings and cut volatility; geographic diversification spreads currency risk across regions.

Permits delay, local content 50%, Brent $86

Brent ~85/bbl and WTI ~82/bbl (mid‑2025) lift dayrates—Tier‑1 rigs >$40k/day—with super‑spec utilization >70% (2024); downturns quickly squeeze margins. U.S. CPI 2024 3.4% and Fed funds ~5.25–5.50% raise costs and temper capex; U.S. land rigs ~700 (2024). DXY ~105 (2024) pressures international revenues; H&P liquidity supports selective reactivations.

| Metric | Value |

|---|---|

| Brent/WTI | 85/82 (mid‑2025) |

| Fed funds | 5.25–5.50% (2024–25) |

| CPI | 3.4% (2024) |

| DXY | ~105 (2024) |

Preview the Actual Deliverable

Helmerich & Payne PESTLE Analysis

The Helmerich & Payne PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are delivered exactly as shown with no placeholders or teasers. What you see is the final, professional file you’ll be able to download immediately after buying.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Understand how political, economic and technological forces shape Helmerich & Payne's drilling and services outlook in our concise PESTLE overview. We highlight regulatory risks, commodity cycles, ESG pressures and innovation trends that could alter margins and market share. Buy the full PESTLE for a detailed, editable report you can use in investment models, strategy decks, or board discussions.

Political factors

Energy policy shifts and permitting

Changes in federal and state drilling permits, NEPA reviews (environmental assessments often 6–12 months; environmental impact statements commonly 3–7 years) and public land leasing timelines can accelerate or delay rig deployments, directly affecting Helmerich & Payne utilization and scheduling. H&P must navigate differing permit windows and compliance across jurisdictions; faster approvals boost rig utilization while tighter rules raise compliance costs and project risk. Strategic planning requires scenario buffers for policy swings and timeline variability.

Geopolitical stability and OPEC+ decisions

OPEC+ supply-management moves and geopolitical disruptions drive oil-price volatility—Brent averaged about $86/bbl in 2024—directly affecting E&P capex and rig demand, with higher prices lifting utilization while mid-year shocks can stall programs. H&P’s operations across North America, Latin America and the Middle East dilute localized risk, and tracking macro signals lets management reallocate fleets proactively.

Local content and nationalization pressures abroad

International markets often impose local hiring, procurement or JV requirements that can reach up to 50% of project inputs in countries with strict nationalization rules, raising operating costs and timeline uncertainty for Helmerich & Payne (HP).

Compliance alters cost structure and schedule predictability; H&P mitigates this via local training programs and partnerships to transfer skills while maintaining H&P technical standards.

Regulatory missteps can trigger fines, license suspension or contract loss, increasing sovereign risk exposure and potential revenue volatility.

Infrastructure and energy-security priorities

Government focus on domestic energy security—backed by policies like the Inflation Reduction Act (approx. $369 billion in energy/climate spending)—can accelerate pipeline, grid and basin projects, reducing bottlenecks and incentivizing drilling; conversely, strong decarbonization mandates can divert capital away from hydrocarbons, forcing H&P to align rig and service capacity with prevailing policy thrusts.

- Policy tailwinds: IRA $369B boosts infrastructure and transition projects

- Risk: decarbonization can reallocate capex away from drilling

- Action: match rig capacity to policy direction and market demand

Trade, tariffs, and equipment flows

Tariffs such as the US 25% steel and 10% aluminum Section 232 duties and 2022–23 US export controls on advanced electronics raise rig upgrade and spare-part costs and add customs delays that complicate international redeployments; H&P cites supply‑chain diversification and higher on‑site inventory in 2024 filings to mitigate shocks, and contract pricing requires pass‑through clauses where feasible.

- Tariffs: 25% steel, 10% aluminum

- Export controls: 2022–23 US semiconductor rules

- Mitigation: diversification + higher inventory (noted in 2024 filings)

- Action: include pass‑through pricing

Permits delay, local content 50%, Brent $86

Federal/state permit timing (NEPA 6–12m; EIS 3–7y) and local content rules (up to 50%) drive H&P scheduling, costs and JV structures. Brent averaged ~$86/bbl in 2024, moving E&P capex and rig demand. IRA energy/climate funding ~$369B (supporting infrastructure) offsets some decarbonization risk. US tariffs (steel 25%, aluminum 10%) and 2022–23 export controls raise upgrade and spare-part costs.

| Factor | 2024/2025 Data |

|---|---|

| Permits/NEPA | 6–12m; EIS 3–7y |

| Oil price | Brent ~$86/bbl (2024) |

| Policy funding | IRA ~$369B |

| Tariffs | Steel 25%, Al 10% |

| Local content | Up to 50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Helmerich & Payne across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current data and industry trends. Designed for executives and investors, it highlights region-specific risks and opportunities, provides forward-looking insights for scenario planning, and is formatted for direct inclusion in plans or decks.

A concise, visually segmented PESTLE summary of Helmerich & Payne that’s easily dropped into presentations or shared across teams, enabling quick alignment, clearer external risk discussions, and fast decision-making during planning sessions.

Economic factors

Commodity price cycles and E&P capex

Brent trading near $85/bbl and WTI around $82/bbl in mid‑2025 drives operator spending and uplifts rig dayrates, with Tier‑1 rigs commanding premiums often above $40,000/day. Prolonged upcycles support higher utilization and pricing power; downturns rapidly squeeze margins and idle fleets. H&P benefits from operator preference for high‑spec rigs but remains exposed to customers’ cash flows. Even in strong price tapes, E&P capital discipline has moderated fleet growth.

Inflation and cost-of-service dynamics

Labor, steel and parts inflation — with U.S. CPI 2024 at 3.4% (BLS) and WTI averaging about $80/bbl in 2024 (EIA) — can squeeze H&P margins where contracts lack escalators. Index-linked pricing and rig efficiency gains have offset much input-cost rise, while improved supply-chain reliability cuts downtime and cost overruns. Rigorous cost control preserves returns across cycles.

Interest rates and capital access

Higher interest rates (Fed funds ~5.25–5.50% in 2024–25) raise borrowing costs for Helmerich & Payne and its clients, tempering fleet upgrades and drilling program economics; reduced activity pressure was reflected in a 2024 U.S. land rig backdrop near 700 rigs (Baker Hughes). Lower rates would improve project IRRs and refinancing options. H&P’s strong balance sheet and liquidity enable counter-cyclical investments and strategic rig reactivations.

Utilization mix and dayrate spread

High-spec super-spec rigs command premium dayrates versus legacy assets, often 20–40% higher, lifting H&P's average revenue per day as mix shifts toward automation-ready fleets; industry super-spec utilization exceeded 70% in 2024. Idle or sub-spec rigs depress averages and carry holding costs, and rig-upgrade ROI hinges on sustained multi-quarter demand visibility.

- Premium spread: 20–40%

- Super-spec utilization: >70% (2024)

- Idle rigs: holding-cost drag

- Upgrade ROI: requires sustained demand

USD strength and international earnings

USD strength (DXY ~105 average in 2024) reduces translated international revenues for Helmerich & Payne and weakens local-cost competitiveness, putting pressure on international margins.

Active FX hedging programs and securing contracts denominated in USD where feasible help smooth revenue swings and cut volatility; geographic diversification spreads currency risk across regions.

Permits delay, local content 50%, Brent $86

Brent ~85/bbl and WTI ~82/bbl (mid‑2025) lift dayrates—Tier‑1 rigs >$40k/day—with super‑spec utilization >70% (2024); downturns quickly squeeze margins. U.S. CPI 2024 3.4% and Fed funds ~5.25–5.50% raise costs and temper capex; U.S. land rigs ~700 (2024). DXY ~105 (2024) pressures international revenues; H&P liquidity supports selective reactivations.

| Metric | Value |

|---|---|

| Brent/WTI | 85/82 (mid‑2025) |

| Fed funds | 5.25–5.50% (2024–25) |

| CPI | 3.4% (2024) |

| DXY | ~105 (2024) |

Preview the Actual Deliverable

Helmerich & Payne PESTLE Analysis

The Helmerich & Payne PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are delivered exactly as shown with no placeholders or teasers. What you see is the final, professional file you’ll be able to download immediately after buying.