Hengtong Optic-Electric Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Hengtong Optic‑Electric faces intense competitive rivalry from global fiber‑optic players, moderate supplier leverage for key materials, rising buyer sophistication, and manageable threat from new entrants thanks to scale and IP; substitutes exert limited pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

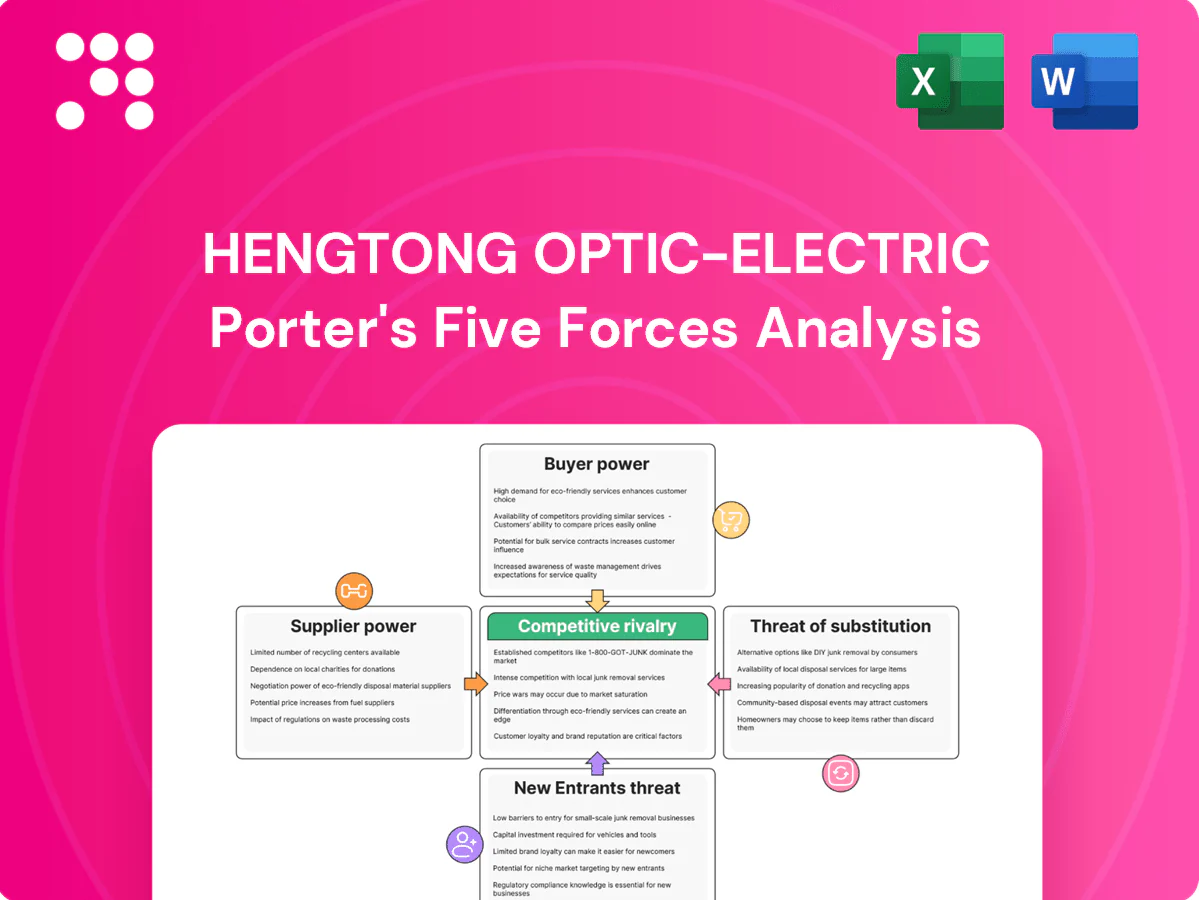

Suppliers Bargaining Power

Preform and specialty input concentration

Optical fiber preforms, specialty coatings and high‑purity chemicals are sourced from a relatively concentrated supplier base, giving upstream vendors meaningful leverage over pricing and supply timing. Hengtong reduces exposure through in‑house preform and coating capabilities and selective dual‑sourcing where feasible. Lengthy qualification cycles and tight material specs limit short‑term switching flexibility. Any supplier disruption quickly depresses draw‑tower utilization and extends customer lead times.

Commodity metals and polymer volatility

Copper, aluminum and XLPE saw pronounced 2024 swings (roughly ±20%, ±15% and ±25% respectively), allowing suppliers to pass costs in tight markets. Hedging and index-linked contracts reduce but do not eliminate exposure, especially during inventory drawdowns. Suppliers gain leverage when stocks are low and energy costs spike, intensifying margin pressure on Hengtong’s long-duration fixed-price projects.

Specialized equipment and spare parts

Draw towers, sheathing lines and submarine armoring equipment for Hengtong come from niche OEMs with few alternatives, concentrating supply and raising bargaining power. Bespoke spares and upgrades often carry lead times of 3–6 months, giving vendors negotiating room while preventive maintenance planning reduces but cannot eliminate dependency. Technology lock-in from proprietary components can elevate lifecycle costs and limit supplier switching.

Logistics and marine assets constraints

Heavy reels, export logistics and scarce port slots leave Hengtong dependent on freight providers; for submarine projects the global fleet of specialized cable-lay vessels remained under 30 in 2024, tightening availability and pricing for vessels and jointing teams. Weather and port congestion amplify schedule risk premiums and delay-driven costs, while early booking and developing in-house laying/jointing capabilities rebalance supplier leverage.

- Reliance on freight providers for heavy reels and port slots

- Under 30 specialized cable-lay vessels globally in 2024 — higher supplier pricing

- Weather/port congestion increase schedule risk premiums

- Early booking and in-house logistics/jointing reduce supplier power

Switching costs and qualification barriers

Material and component changes typically trigger telecom and utility requalification cycles of roughly 6–18 months, slowing supplier substitution and raising switching costs. Approved vendor lists in critical projects lock incumbents into supply chains, while framework agreements and multi-year volume commitments trade lower prices for delivery reliability. Supplier co-funded R&D (common in fiber/OSP) further entrenches dependencies.

- requalification: 6–18 months

- frameworks: multi-year volume/price trade-offs

- r&d partnerships: deepen supplier lock-in

Suppliers wield medium-high leverage as commodity swings and long lead times raise costs

Suppliers exert medium‑to‑high bargaining power: concentrated fiber/coat vendors, niche OEMs and freight providers (under 30 cable‑lay vessels in 2024) limit alternatives and raise prices. Commodity swings (copper ±20%, aluminum ±15%, XLPE ±25% in 2024) and long requalification/lead times (6–18 months; spares 3–6 months) amplify leverage despite Hengtong’s in‑house and dual‑sourcing mitigants.

| Metric | 2024/Range |

|---|---|

| Subsea vessels | <30 |

| Copper/Al/XLPE swings | ±20%/±15%/±25% |

| Spare lead times | 3–6 months |

| Requalification | 6–18 months |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and market entry risks specific to Hengtong Optic‑Electric, identifies disruptive threats and strategic barriers shaping pricing and profitability, and is fully editable for inclusion in reports, investor decks, or academic projects.

One-sheet Porter's Five Forces for Hengtong Optic‑Electric—clarifies competitive pressures and supplier/customer risks at a glance, ready to drop into investor decks or strategy sessions.

Customers Bargaining Power

Mega-buyers and tender dynamics

Tier-1 telcos, utilities and EPCs run large, highly competitive tenders that compress margins for suppliers like Hengtong; volume concentration gives buyers outsized negotiating leverage. Buyers commonly stagger awards across multiple vendors to sustain price pressure and extract better terms. Payment schedules, extended payment days and demand for performance bonds further tilt bargaining power toward customers.

Specification-driven procurement

As of 2024 strict technical standards—IEC, ITU, national grid codes and submarine specifications—limit product differentiation to compliance and demonstrated reliability. Buyers routinely leverage compliance to press for price concessions once minimum specs are met. Bespoke designs for harsh environments and tailored testing protocols reduce price sensitivity. Proven quality with demonstrable low failure rates supports sustained pricing premiums.

Switching and qualification hurdles

Long qualification cycles, typically 6–18 months with factory audits, temper buyer switching frequency for Hengtong products; for critical HV/EHV and subsea links buyers favor incumbents with proven track records. Utilities and EPCs commonly mandate multi-sourcing, keeping 2–3 competitive alternatives over project lifecycles. Performance guarantees and liquidated damages, often set at 0.1–0.5% per day, give buyers significant post-award leverage.

Total cost and service bundling

Buyers benchmark total cost not just cable price but installation, O&M and lifecycle losses (single‑mode fiber attenuation ~0.2–0.35 dB/km); in 2024 the global optical fiber market was ~= USD 8.9bn, keeping service and lifecycle costs central to procurement.

Turnkey EPC and integrated warranties increase solution stickiness and cut buyer leverage, while unbundled buys let customers cherry‑pick low‑cost components and squeeze margins.

Service SLAs, logistics speed and warranty terms are primary negotiation levers that can shift economics by double‑digit percentages over project lifecycles.

- Benchmarking: total cost of ownership over lifecycle

- Bundling: turnkey EPC raises switching costs

- Unbundling: component sourcing lowers buyer prices

- Levers: SLAs, logistics, warranty terms

Regional policies and localization

Regional local content rules and subsidies push buyers toward suppliers meeting localization thresholds, raising customer bargaining power as state-linked infrastructure procurers can steer contracts via policy; Hengtong’s global footprint helps it meet many such thresholds. Trade barriers restrict alternative suppliers and can raise accepted price levels, increasing negotiation leverage for compliant vendors.

- Local content tilts sourcing

- State buyers add policy leverage

- Hengtong offsets via localization

- Trade barriers limit options, lift prices

Tier-1 telcos compress optical-fiber margins; market USD 8.9bn

Tier‑1 telcos, utilities and EPCs concentrate volumes and run aggressive tenders, compressing margins; qualification cycles of 6–18 months and multi‑sourcing limit switching but buyers still extract concessions. Buyers benchmark TCO (2024 global optical fiber market ≈ USD 8.9bn), use SLAs, payment terms and liquidated damages (0.1–0.5%/day) as levers.

| Metric | 2024 |

|---|---|

| Market size | USD 8.9bn |

| Qualification | 6–18 months |

| LDs | 0.1–0.5%/day |

Preview Before You Purchase

Hengtong Optic-Electric Porter's Five Forces Analysis

This preview displays the exact Hengtong Optic‑Electric Porter’s Five Forces analysis you’ll receive after purchase—fully formatted and ready for immediate use. No samples, no placeholders: the file available for download upon payment is precisely this complete, professionally written document. Use it as-is for decision making, reporting, or further research.

Go Beyond the Preview—Access the Full Strategic Report

Hengtong Optic‑Electric faces intense competitive rivalry from global fiber‑optic players, moderate supplier leverage for key materials, rising buyer sophistication, and manageable threat from new entrants thanks to scale and IP; substitutes exert limited pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Preform and specialty input concentration

Optical fiber preforms, specialty coatings and high‑purity chemicals are sourced from a relatively concentrated supplier base, giving upstream vendors meaningful leverage over pricing and supply timing. Hengtong reduces exposure through in‑house preform and coating capabilities and selective dual‑sourcing where feasible. Lengthy qualification cycles and tight material specs limit short‑term switching flexibility. Any supplier disruption quickly depresses draw‑tower utilization and extends customer lead times.

Commodity metals and polymer volatility

Copper, aluminum and XLPE saw pronounced 2024 swings (roughly ±20%, ±15% and ±25% respectively), allowing suppliers to pass costs in tight markets. Hedging and index-linked contracts reduce but do not eliminate exposure, especially during inventory drawdowns. Suppliers gain leverage when stocks are low and energy costs spike, intensifying margin pressure on Hengtong’s long-duration fixed-price projects.

Specialized equipment and spare parts

Draw towers, sheathing lines and submarine armoring equipment for Hengtong come from niche OEMs with few alternatives, concentrating supply and raising bargaining power. Bespoke spares and upgrades often carry lead times of 3–6 months, giving vendors negotiating room while preventive maintenance planning reduces but cannot eliminate dependency. Technology lock-in from proprietary components can elevate lifecycle costs and limit supplier switching.

Logistics and marine assets constraints

Heavy reels, export logistics and scarce port slots leave Hengtong dependent on freight providers; for submarine projects the global fleet of specialized cable-lay vessels remained under 30 in 2024, tightening availability and pricing for vessels and jointing teams. Weather and port congestion amplify schedule risk premiums and delay-driven costs, while early booking and developing in-house laying/jointing capabilities rebalance supplier leverage.

- Reliance on freight providers for heavy reels and port slots

- Under 30 specialized cable-lay vessels globally in 2024 — higher supplier pricing

- Weather/port congestion increase schedule risk premiums

- Early booking and in-house logistics/jointing reduce supplier power

Switching costs and qualification barriers

Material and component changes typically trigger telecom and utility requalification cycles of roughly 6–18 months, slowing supplier substitution and raising switching costs. Approved vendor lists in critical projects lock incumbents into supply chains, while framework agreements and multi-year volume commitments trade lower prices for delivery reliability. Supplier co-funded R&D (common in fiber/OSP) further entrenches dependencies.

- requalification: 6–18 months

- frameworks: multi-year volume/price trade-offs

- r&d partnerships: deepen supplier lock-in

Suppliers wield medium-high leverage as commodity swings and long lead times raise costs

Suppliers exert medium‑to‑high bargaining power: concentrated fiber/coat vendors, niche OEMs and freight providers (under 30 cable‑lay vessels in 2024) limit alternatives and raise prices. Commodity swings (copper ±20%, aluminum ±15%, XLPE ±25% in 2024) and long requalification/lead times (6–18 months; spares 3–6 months) amplify leverage despite Hengtong’s in‑house and dual‑sourcing mitigants.

| Metric | 2024/Range |

|---|---|

| Subsea vessels | <30 |

| Copper/Al/XLPE swings | ±20%/±15%/±25% |

| Spare lead times | 3–6 months |

| Requalification | 6–18 months |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and market entry risks specific to Hengtong Optic‑Electric, identifies disruptive threats and strategic barriers shaping pricing and profitability, and is fully editable for inclusion in reports, investor decks, or academic projects.

One-sheet Porter's Five Forces for Hengtong Optic‑Electric—clarifies competitive pressures and supplier/customer risks at a glance, ready to drop into investor decks or strategy sessions.

Customers Bargaining Power

Mega-buyers and tender dynamics

Tier-1 telcos, utilities and EPCs run large, highly competitive tenders that compress margins for suppliers like Hengtong; volume concentration gives buyers outsized negotiating leverage. Buyers commonly stagger awards across multiple vendors to sustain price pressure and extract better terms. Payment schedules, extended payment days and demand for performance bonds further tilt bargaining power toward customers.

Specification-driven procurement

As of 2024 strict technical standards—IEC, ITU, national grid codes and submarine specifications—limit product differentiation to compliance and demonstrated reliability. Buyers routinely leverage compliance to press for price concessions once minimum specs are met. Bespoke designs for harsh environments and tailored testing protocols reduce price sensitivity. Proven quality with demonstrable low failure rates supports sustained pricing premiums.

Switching and qualification hurdles

Long qualification cycles, typically 6–18 months with factory audits, temper buyer switching frequency for Hengtong products; for critical HV/EHV and subsea links buyers favor incumbents with proven track records. Utilities and EPCs commonly mandate multi-sourcing, keeping 2–3 competitive alternatives over project lifecycles. Performance guarantees and liquidated damages, often set at 0.1–0.5% per day, give buyers significant post-award leverage.

Total cost and service bundling

Buyers benchmark total cost not just cable price but installation, O&M and lifecycle losses (single‑mode fiber attenuation ~0.2–0.35 dB/km); in 2024 the global optical fiber market was ~= USD 8.9bn, keeping service and lifecycle costs central to procurement.

Turnkey EPC and integrated warranties increase solution stickiness and cut buyer leverage, while unbundled buys let customers cherry‑pick low‑cost components and squeeze margins.

Service SLAs, logistics speed and warranty terms are primary negotiation levers that can shift economics by double‑digit percentages over project lifecycles.

- Benchmarking: total cost of ownership over lifecycle

- Bundling: turnkey EPC raises switching costs

- Unbundling: component sourcing lowers buyer prices

- Levers: SLAs, logistics, warranty terms

Regional policies and localization

Regional local content rules and subsidies push buyers toward suppliers meeting localization thresholds, raising customer bargaining power as state-linked infrastructure procurers can steer contracts via policy; Hengtong’s global footprint helps it meet many such thresholds. Trade barriers restrict alternative suppliers and can raise accepted price levels, increasing negotiation leverage for compliant vendors.

- Local content tilts sourcing

- State buyers add policy leverage

- Hengtong offsets via localization

- Trade barriers limit options, lift prices

Tier-1 telcos compress optical-fiber margins; market USD 8.9bn

Tier‑1 telcos, utilities and EPCs concentrate volumes and run aggressive tenders, compressing margins; qualification cycles of 6–18 months and multi‑sourcing limit switching but buyers still extract concessions. Buyers benchmark TCO (2024 global optical fiber market ≈ USD 8.9bn), use SLAs, payment terms and liquidated damages (0.1–0.5%/day) as levers.

| Metric | 2024 |

|---|---|

| Market size | USD 8.9bn |

| Qualification | 6–18 months |

| LDs | 0.1–0.5%/day |

Preview Before You Purchase

Hengtong Optic-Electric Porter's Five Forces Analysis

This preview displays the exact Hengtong Optic‑Electric Porter’s Five Forces analysis you’ll receive after purchase—fully formatted and ready for immediate use. No samples, no placeholders: the file available for download upon payment is precisely this complete, professionally written document. Use it as-is for decision making, reporting, or further research.

Description

Go Beyond the Preview—Access the Full Strategic Report

Hengtong Optic‑Electric faces intense competitive rivalry from global fiber‑optic players, moderate supplier leverage for key materials, rising buyer sophistication, and manageable threat from new entrants thanks to scale and IP; substitutes exert limited pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications.

Suppliers Bargaining Power

Preform and specialty input concentration

Optical fiber preforms, specialty coatings and high‑purity chemicals are sourced from a relatively concentrated supplier base, giving upstream vendors meaningful leverage over pricing and supply timing. Hengtong reduces exposure through in‑house preform and coating capabilities and selective dual‑sourcing where feasible. Lengthy qualification cycles and tight material specs limit short‑term switching flexibility. Any supplier disruption quickly depresses draw‑tower utilization and extends customer lead times.

Commodity metals and polymer volatility

Copper, aluminum and XLPE saw pronounced 2024 swings (roughly ±20%, ±15% and ±25% respectively), allowing suppliers to pass costs in tight markets. Hedging and index-linked contracts reduce but do not eliminate exposure, especially during inventory drawdowns. Suppliers gain leverage when stocks are low and energy costs spike, intensifying margin pressure on Hengtong’s long-duration fixed-price projects.

Specialized equipment and spare parts

Draw towers, sheathing lines and submarine armoring equipment for Hengtong come from niche OEMs with few alternatives, concentrating supply and raising bargaining power. Bespoke spares and upgrades often carry lead times of 3–6 months, giving vendors negotiating room while preventive maintenance planning reduces but cannot eliminate dependency. Technology lock-in from proprietary components can elevate lifecycle costs and limit supplier switching.

Logistics and marine assets constraints

Heavy reels, export logistics and scarce port slots leave Hengtong dependent on freight providers; for submarine projects the global fleet of specialized cable-lay vessels remained under 30 in 2024, tightening availability and pricing for vessels and jointing teams. Weather and port congestion amplify schedule risk premiums and delay-driven costs, while early booking and developing in-house laying/jointing capabilities rebalance supplier leverage.

- Reliance on freight providers for heavy reels and port slots

- Under 30 specialized cable-lay vessels globally in 2024 — higher supplier pricing

- Weather/port congestion increase schedule risk premiums

- Early booking and in-house logistics/jointing reduce supplier power

Switching costs and qualification barriers

Material and component changes typically trigger telecom and utility requalification cycles of roughly 6–18 months, slowing supplier substitution and raising switching costs. Approved vendor lists in critical projects lock incumbents into supply chains, while framework agreements and multi-year volume commitments trade lower prices for delivery reliability. Supplier co-funded R&D (common in fiber/OSP) further entrenches dependencies.

- requalification: 6–18 months

- frameworks: multi-year volume/price trade-offs

- r&d partnerships: deepen supplier lock-in

Suppliers wield medium-high leverage as commodity swings and long lead times raise costs

Suppliers exert medium‑to‑high bargaining power: concentrated fiber/coat vendors, niche OEMs and freight providers (under 30 cable‑lay vessels in 2024) limit alternatives and raise prices. Commodity swings (copper ±20%, aluminum ±15%, XLPE ±25% in 2024) and long requalification/lead times (6–18 months; spares 3–6 months) amplify leverage despite Hengtong’s in‑house and dual‑sourcing mitigants.

| Metric | 2024/Range |

|---|---|

| Subsea vessels | <30 |

| Copper/Al/XLPE swings | ±20%/±15%/±25% |

| Spare lead times | 3–6 months |

| Requalification | 6–18 months |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, substitutes, and market entry risks specific to Hengtong Optic‑Electric, identifies disruptive threats and strategic barriers shaping pricing and profitability, and is fully editable for inclusion in reports, investor decks, or academic projects.

One-sheet Porter's Five Forces for Hengtong Optic‑Electric—clarifies competitive pressures and supplier/customer risks at a glance, ready to drop into investor decks or strategy sessions.

Customers Bargaining Power

Mega-buyers and tender dynamics

Tier-1 telcos, utilities and EPCs run large, highly competitive tenders that compress margins for suppliers like Hengtong; volume concentration gives buyers outsized negotiating leverage. Buyers commonly stagger awards across multiple vendors to sustain price pressure and extract better terms. Payment schedules, extended payment days and demand for performance bonds further tilt bargaining power toward customers.

Specification-driven procurement

As of 2024 strict technical standards—IEC, ITU, national grid codes and submarine specifications—limit product differentiation to compliance and demonstrated reliability. Buyers routinely leverage compliance to press for price concessions once minimum specs are met. Bespoke designs for harsh environments and tailored testing protocols reduce price sensitivity. Proven quality with demonstrable low failure rates supports sustained pricing premiums.

Switching and qualification hurdles

Long qualification cycles, typically 6–18 months with factory audits, temper buyer switching frequency for Hengtong products; for critical HV/EHV and subsea links buyers favor incumbents with proven track records. Utilities and EPCs commonly mandate multi-sourcing, keeping 2–3 competitive alternatives over project lifecycles. Performance guarantees and liquidated damages, often set at 0.1–0.5% per day, give buyers significant post-award leverage.

Total cost and service bundling

Buyers benchmark total cost not just cable price but installation, O&M and lifecycle losses (single‑mode fiber attenuation ~0.2–0.35 dB/km); in 2024 the global optical fiber market was ~= USD 8.9bn, keeping service and lifecycle costs central to procurement.

Turnkey EPC and integrated warranties increase solution stickiness and cut buyer leverage, while unbundled buys let customers cherry‑pick low‑cost components and squeeze margins.

Service SLAs, logistics speed and warranty terms are primary negotiation levers that can shift economics by double‑digit percentages over project lifecycles.

- Benchmarking: total cost of ownership over lifecycle

- Bundling: turnkey EPC raises switching costs

- Unbundling: component sourcing lowers buyer prices

- Levers: SLAs, logistics, warranty terms

Regional policies and localization

Regional local content rules and subsidies push buyers toward suppliers meeting localization thresholds, raising customer bargaining power as state-linked infrastructure procurers can steer contracts via policy; Hengtong’s global footprint helps it meet many such thresholds. Trade barriers restrict alternative suppliers and can raise accepted price levels, increasing negotiation leverage for compliant vendors.

- Local content tilts sourcing

- State buyers add policy leverage

- Hengtong offsets via localization

- Trade barriers limit options, lift prices

Tier-1 telcos compress optical-fiber margins; market USD 8.9bn

Tier‑1 telcos, utilities and EPCs concentrate volumes and run aggressive tenders, compressing margins; qualification cycles of 6–18 months and multi‑sourcing limit switching but buyers still extract concessions. Buyers benchmark TCO (2024 global optical fiber market ≈ USD 8.9bn), use SLAs, payment terms and liquidated damages (0.1–0.5%/day) as levers.

| Metric | 2024 |

|---|---|

| Market size | USD 8.9bn |

| Qualification | 6–18 months |

| LDs | 0.1–0.5%/day |

Preview Before You Purchase

Hengtong Optic-Electric Porter's Five Forces Analysis

This preview displays the exact Hengtong Optic‑Electric Porter’s Five Forces analysis you’ll receive after purchase—fully formatted and ready for immediate use. No samples, no placeholders: the file available for download upon payment is precisely this complete, professionally written document. Use it as-is for decision making, reporting, or further research.