JM Huber Porter's Five Forces Analysis

From Overview to Strategy Blueprint

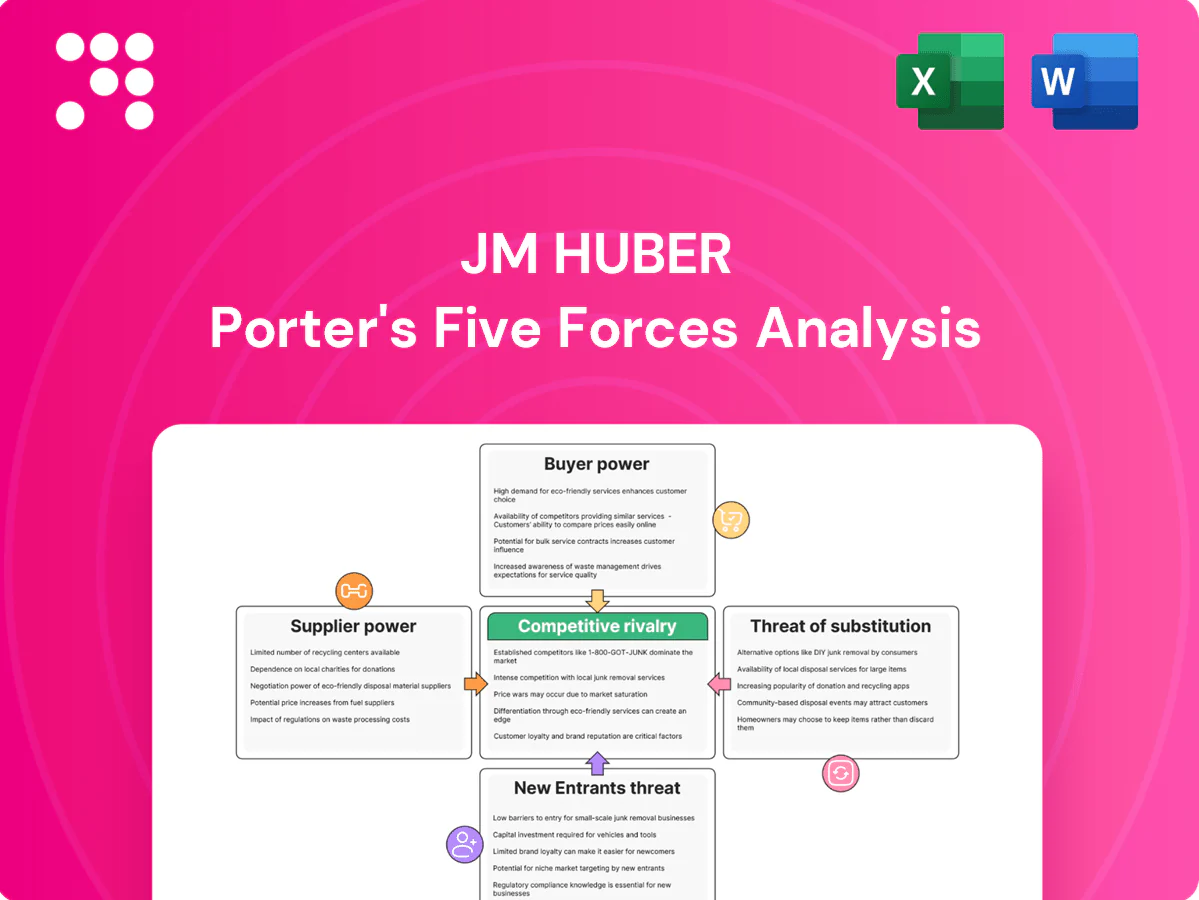

JM Huber’s Porter’s Five Forces snapshot highlights supplier and buyer power, competitive rivalry across specialty chemicals, threats from substitutes and new entrants, and regulatory pressures shaping margins. This brief preview only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to JM Huber.

Suppliers Bargaining Power

Raw material concentration

Huber depends on minerals (ATH, Mg(OH)2), wood fiber/resins and seaweed/fermentation inputs (seaweed largely sourced from Indonesia/Philippines), concentrating supply and giving select suppliers leverage; regional concentration (over 70% of industrial carrageenan/seaweed origin) and limited ATH mining regions mean disruptions—weather, 2023–24 geopolitics or export quotas—can tighten supply and push prices significantly; multi-sourcing and qualification lower but do not eliminate this risk.

Quality and certification

As of 2024, food-grade hydrocolloids and engineered woods require strict specs and certifications such as ISO 22000, HACCP and FDA GRAS, limiting eligible suppliers and increasing their bargaining power. Supplier switches demand audits and re-qualification, often taking several months and costing up to six-figure sums. Fewer qualified vendors concentrate supply power, while long-term contracts and volume guarantees help JM Huber rebalance leverage.

Logistics and energy sensitivity

Freight and energy are major cost components for minerals and wood products, and spikes in fuel or shipping congestion allow upstream suppliers to pass through costs to buyers. Huber’s global footprint gives routing flexibility and alternative ports but does not fully insulate against market-wide bottlenecks. Index-linked supply contracts lower short-term volatility yet institutionalize supplier pricing power across cycles.

Sustainability constraints

Responsible forestry and seaweed harvesting add regulatory and certification compliance, concentrating suppliers with verified sustainable practices—over 200 million hectares are FSC-certified globally (FSC, 2023)—allowing those suppliers to command price premiums. Huber’s public sustainability commitments tighten its eligible supplier pool, prompting co-development of traceability systems that can trade higher unit costs for greater security of supply.

- Compliance burden: higher certification and audit costs

- Supplier scarcity: certified pool limited despite 200M+ ha FSC

- Price leverage: verified suppliers can charge premiums

- Mitigation: co-develop traceability to swap price for supply security

Switching and specialization

Specialty grades like surface-treated ATH and tailored gums create strong stickiness because reformulation and process tweaks to accept new suppliers are costly, raising the bargaining power of qualified suppliers.

Dual-qualifying critical inputs is an effective mitigation, reducing single-supplier dependence and improving negotiating leverage.

- Supplier stickiness: specialty grades raise switching costs

- Cost barrier: reformulation/process changes are expensive

- Supplier influence: qualified vendors command better terms

- Mitigation: dual-qualification lowers concentration risk

Supply risk: >70% origin concentration; requalification may cost six figures

Supplier power is high: over 70% of industrial seaweed/carrageenan originates from Indonesia/Philippines, and ATH mining is regionally concentrated, making supply disruptions in 2023–24 impactful; certified suppliers command premiums as Huber limits eligible vendors. Requalification often takes months and can cost up to six-figure sums; long-term contracts and dual-qualification partially mitigate risk.

| Metric | Value | Source/Note |

|---|---|---|

| Seaweed origin concentration | >70% | 2024 industry data |

| FSC-certified area | 200M+ ha | FSC, 2023 |

| Requalification cost | Up to six-figure USD | Huber disclosures/industry |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to JM Huber that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for JM Huber delivers a clean, copy-ready summary and radar visual to instantly spot competitive pressure, and lets you tweak force levels or swap in new data for rapid scenario testing. Ideal for busy decision-makers who need a simple, no-code tool to translate market signals into actionable strategic moves.

Customers Bargaining Power

Large enterprise customers

Construction distributors, OEMs, and global CPG/food companies buy Huber products at scale, creating concentrated volume that drives aggressive price negotiations and rebate expectations. Centralized procurement structures among these large buyers intensify margin pressure through tougher contract terms and longer payment cycles. Huber offsets bargaining pressure by emphasizing product performance, application support, and premium service to protect pricing and retention.

Specification lock-in

By 2024, engineered woods and hydrocolloids are frequently specified in codes and product recipes, creating specification lock-in that materially raises buyer switching costs once formulations are validated. Buyers still leverage requalification cycles to solicit competitive bids, periodically reducing supplier leverage. JM Huber preserves stickiness by investing in technical service and application support, accelerating requalification timelines and lowering customer incentive to switch.

Price sensitivity cycles

Construction and industrial demand is cyclical, amplifying buyer price sensitivity in downturns as firms trim projects; global construction output was about $13 trillion in 2023, putting volume risk squarely on suppliers. Buyers pursue downsizing, substitute blends or extended payment terms to preserve cash, increasing bargaining leverage. In up-cycles availability and service trump price, so JM Huber uses dynamic pricing and allocation policies to manage swings and protect margins.

Private label and reformulation

Savvy buyers push private-label or reformulated hydrocolloid blends to cut costs; North American private-label penetration reached about 18–20% in 2024, increasing margin pressure. Hydrocolloid systems can be swapped to lower-cost chemistries if performance tolerances allow, and engineered-wood customers routinely mix SKUs to value-engineer builds. Huber’s application labs and demonstrated value-in-use help defend pricing and specification stickiness.

- Private-label penetration ~18–20% (2024)

- Hydrocolloid reformulation lowers COGS if specs permit

- Engineered-wood SKU mixing for value-engineering

- Huber labs preserve specification and margin

Contracting and terms

Annual and biannual contracts with indexation, volume tiers, and SLAs concentrate bargaining power by linking price to raw-material indices while locking volumes and service levels; buyers counter this via multi-sourcing and should-cost models, pressuring margins. Huber trades committed volumes for price stability and priority supply, using penalties and lead-time guarantees to allocate risk and protect throughput.

- Contract cadence: annual/biannual

- Levers: indexation, volume tiers, SLAs

- Buyer tools: multi-sourcing, should-cost

- Huber response: volume for priority, penalties, lead-time guarantees

Concentrated OEM demand, 18–20% private-label and $13T construction fuel price pressure

Large OEMs, distributors and CPG buyers concentrate volume and drive rebates and longer payment terms; private-label penetration ~18–20% (2024) and global construction output ~$13T (2023) amplify price sensitivity. Specification lock-in for engineered woods and hydrocolloids raises switching costs, but requalification cycles and reformulation risk keep margins contested. Huber defends pricing via labs, SLAs, indexed contracts and prioritized supply.

| Metric | Value |

|---|---|

| Private-label penetration | 18–20% (2024) |

| Global construction output | $13T (2023) |

| Contract cadence | Annual/biannual |

Preview Before You Purchase

JM Huber Porter's Five Forces Analysis

This preview shows the exact JM Huber Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is precisely the deliverable available for instant access.

From Overview to Strategy Blueprint

JM Huber’s Porter’s Five Forces snapshot highlights supplier and buyer power, competitive rivalry across specialty chemicals, threats from substitutes and new entrants, and regulatory pressures shaping margins. This brief preview only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to JM Huber.

Suppliers Bargaining Power

Raw material concentration

Huber depends on minerals (ATH, Mg(OH)2), wood fiber/resins and seaweed/fermentation inputs (seaweed largely sourced from Indonesia/Philippines), concentrating supply and giving select suppliers leverage; regional concentration (over 70% of industrial carrageenan/seaweed origin) and limited ATH mining regions mean disruptions—weather, 2023–24 geopolitics or export quotas—can tighten supply and push prices significantly; multi-sourcing and qualification lower but do not eliminate this risk.

Quality and certification

As of 2024, food-grade hydrocolloids and engineered woods require strict specs and certifications such as ISO 22000, HACCP and FDA GRAS, limiting eligible suppliers and increasing their bargaining power. Supplier switches demand audits and re-qualification, often taking several months and costing up to six-figure sums. Fewer qualified vendors concentrate supply power, while long-term contracts and volume guarantees help JM Huber rebalance leverage.

Logistics and energy sensitivity

Freight and energy are major cost components for minerals and wood products, and spikes in fuel or shipping congestion allow upstream suppliers to pass through costs to buyers. Huber’s global footprint gives routing flexibility and alternative ports but does not fully insulate against market-wide bottlenecks. Index-linked supply contracts lower short-term volatility yet institutionalize supplier pricing power across cycles.

Sustainability constraints

Responsible forestry and seaweed harvesting add regulatory and certification compliance, concentrating suppliers with verified sustainable practices—over 200 million hectares are FSC-certified globally (FSC, 2023)—allowing those suppliers to command price premiums. Huber’s public sustainability commitments tighten its eligible supplier pool, prompting co-development of traceability systems that can trade higher unit costs for greater security of supply.

- Compliance burden: higher certification and audit costs

- Supplier scarcity: certified pool limited despite 200M+ ha FSC

- Price leverage: verified suppliers can charge premiums

- Mitigation: co-develop traceability to swap price for supply security

Switching and specialization

Specialty grades like surface-treated ATH and tailored gums create strong stickiness because reformulation and process tweaks to accept new suppliers are costly, raising the bargaining power of qualified suppliers.

Dual-qualifying critical inputs is an effective mitigation, reducing single-supplier dependence and improving negotiating leverage.

- Supplier stickiness: specialty grades raise switching costs

- Cost barrier: reformulation/process changes are expensive

- Supplier influence: qualified vendors command better terms

- Mitigation: dual-qualification lowers concentration risk

Supply risk: >70% origin concentration; requalification may cost six figures

Supplier power is high: over 70% of industrial seaweed/carrageenan originates from Indonesia/Philippines, and ATH mining is regionally concentrated, making supply disruptions in 2023–24 impactful; certified suppliers command premiums as Huber limits eligible vendors. Requalification often takes months and can cost up to six-figure sums; long-term contracts and dual-qualification partially mitigate risk.

| Metric | Value | Source/Note |

|---|---|---|

| Seaweed origin concentration | >70% | 2024 industry data |

| FSC-certified area | 200M+ ha | FSC, 2023 |

| Requalification cost | Up to six-figure USD | Huber disclosures/industry |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to JM Huber that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for JM Huber delivers a clean, copy-ready summary and radar visual to instantly spot competitive pressure, and lets you tweak force levels or swap in new data for rapid scenario testing. Ideal for busy decision-makers who need a simple, no-code tool to translate market signals into actionable strategic moves.

Customers Bargaining Power

Large enterprise customers

Construction distributors, OEMs, and global CPG/food companies buy Huber products at scale, creating concentrated volume that drives aggressive price negotiations and rebate expectations. Centralized procurement structures among these large buyers intensify margin pressure through tougher contract terms and longer payment cycles. Huber offsets bargaining pressure by emphasizing product performance, application support, and premium service to protect pricing and retention.

Specification lock-in

By 2024, engineered woods and hydrocolloids are frequently specified in codes and product recipes, creating specification lock-in that materially raises buyer switching costs once formulations are validated. Buyers still leverage requalification cycles to solicit competitive bids, periodically reducing supplier leverage. JM Huber preserves stickiness by investing in technical service and application support, accelerating requalification timelines and lowering customer incentive to switch.

Price sensitivity cycles

Construction and industrial demand is cyclical, amplifying buyer price sensitivity in downturns as firms trim projects; global construction output was about $13 trillion in 2023, putting volume risk squarely on suppliers. Buyers pursue downsizing, substitute blends or extended payment terms to preserve cash, increasing bargaining leverage. In up-cycles availability and service trump price, so JM Huber uses dynamic pricing and allocation policies to manage swings and protect margins.

Private label and reformulation

Savvy buyers push private-label or reformulated hydrocolloid blends to cut costs; North American private-label penetration reached about 18–20% in 2024, increasing margin pressure. Hydrocolloid systems can be swapped to lower-cost chemistries if performance tolerances allow, and engineered-wood customers routinely mix SKUs to value-engineer builds. Huber’s application labs and demonstrated value-in-use help defend pricing and specification stickiness.

- Private-label penetration ~18–20% (2024)

- Hydrocolloid reformulation lowers COGS if specs permit

- Engineered-wood SKU mixing for value-engineering

- Huber labs preserve specification and margin

Contracting and terms

Annual and biannual contracts with indexation, volume tiers, and SLAs concentrate bargaining power by linking price to raw-material indices while locking volumes and service levels; buyers counter this via multi-sourcing and should-cost models, pressuring margins. Huber trades committed volumes for price stability and priority supply, using penalties and lead-time guarantees to allocate risk and protect throughput.

- Contract cadence: annual/biannual

- Levers: indexation, volume tiers, SLAs

- Buyer tools: multi-sourcing, should-cost

- Huber response: volume for priority, penalties, lead-time guarantees

Concentrated OEM demand, 18–20% private-label and $13T construction fuel price pressure

Large OEMs, distributors and CPG buyers concentrate volume and drive rebates and longer payment terms; private-label penetration ~18–20% (2024) and global construction output ~$13T (2023) amplify price sensitivity. Specification lock-in for engineered woods and hydrocolloids raises switching costs, but requalification cycles and reformulation risk keep margins contested. Huber defends pricing via labs, SLAs, indexed contracts and prioritized supply.

| Metric | Value |

|---|---|

| Private-label penetration | 18–20% (2024) |

| Global construction output | $13T (2023) |

| Contract cadence | Annual/biannual |

Preview Before You Purchase

JM Huber Porter's Five Forces Analysis

This preview shows the exact JM Huber Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is precisely the deliverable available for instant access.

Description

From Overview to Strategy Blueprint

JM Huber’s Porter’s Five Forces snapshot highlights supplier and buyer power, competitive rivalry across specialty chemicals, threats from substitutes and new entrants, and regulatory pressures shaping margins. This brief preview only scratches the surface. Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to JM Huber.

Suppliers Bargaining Power

Raw material concentration

Huber depends on minerals (ATH, Mg(OH)2), wood fiber/resins and seaweed/fermentation inputs (seaweed largely sourced from Indonesia/Philippines), concentrating supply and giving select suppliers leverage; regional concentration (over 70% of industrial carrageenan/seaweed origin) and limited ATH mining regions mean disruptions—weather, 2023–24 geopolitics or export quotas—can tighten supply and push prices significantly; multi-sourcing and qualification lower but do not eliminate this risk.

Quality and certification

As of 2024, food-grade hydrocolloids and engineered woods require strict specs and certifications such as ISO 22000, HACCP and FDA GRAS, limiting eligible suppliers and increasing their bargaining power. Supplier switches demand audits and re-qualification, often taking several months and costing up to six-figure sums. Fewer qualified vendors concentrate supply power, while long-term contracts and volume guarantees help JM Huber rebalance leverage.

Logistics and energy sensitivity

Freight and energy are major cost components for minerals and wood products, and spikes in fuel or shipping congestion allow upstream suppliers to pass through costs to buyers. Huber’s global footprint gives routing flexibility and alternative ports but does not fully insulate against market-wide bottlenecks. Index-linked supply contracts lower short-term volatility yet institutionalize supplier pricing power across cycles.

Sustainability constraints

Responsible forestry and seaweed harvesting add regulatory and certification compliance, concentrating suppliers with verified sustainable practices—over 200 million hectares are FSC-certified globally (FSC, 2023)—allowing those suppliers to command price premiums. Huber’s public sustainability commitments tighten its eligible supplier pool, prompting co-development of traceability systems that can trade higher unit costs for greater security of supply.

- Compliance burden: higher certification and audit costs

- Supplier scarcity: certified pool limited despite 200M+ ha FSC

- Price leverage: verified suppliers can charge premiums

- Mitigation: co-develop traceability to swap price for supply security

Switching and specialization

Specialty grades like surface-treated ATH and tailored gums create strong stickiness because reformulation and process tweaks to accept new suppliers are costly, raising the bargaining power of qualified suppliers.

Dual-qualifying critical inputs is an effective mitigation, reducing single-supplier dependence and improving negotiating leverage.

- Supplier stickiness: specialty grades raise switching costs

- Cost barrier: reformulation/process changes are expensive

- Supplier influence: qualified vendors command better terms

- Mitigation: dual-qualification lowers concentration risk

Supply risk: >70% origin concentration; requalification may cost six figures

Supplier power is high: over 70% of industrial seaweed/carrageenan originates from Indonesia/Philippines, and ATH mining is regionally concentrated, making supply disruptions in 2023–24 impactful; certified suppliers command premiums as Huber limits eligible vendors. Requalification often takes months and can cost up to six-figure sums; long-term contracts and dual-qualification partially mitigate risk.

| Metric | Value | Source/Note |

|---|---|---|

| Seaweed origin concentration | >70% | 2024 industry data |

| FSC-certified area | 200M+ ha | FSC, 2023 |

| Requalification cost | Up to six-figure USD | Huber disclosures/industry |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to JM Huber that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect margins and market share.

One-sheet Porter's Five Forces for JM Huber delivers a clean, copy-ready summary and radar visual to instantly spot competitive pressure, and lets you tweak force levels or swap in new data for rapid scenario testing. Ideal for busy decision-makers who need a simple, no-code tool to translate market signals into actionable strategic moves.

Customers Bargaining Power

Large enterprise customers

Construction distributors, OEMs, and global CPG/food companies buy Huber products at scale, creating concentrated volume that drives aggressive price negotiations and rebate expectations. Centralized procurement structures among these large buyers intensify margin pressure through tougher contract terms and longer payment cycles. Huber offsets bargaining pressure by emphasizing product performance, application support, and premium service to protect pricing and retention.

Specification lock-in

By 2024, engineered woods and hydrocolloids are frequently specified in codes and product recipes, creating specification lock-in that materially raises buyer switching costs once formulations are validated. Buyers still leverage requalification cycles to solicit competitive bids, periodically reducing supplier leverage. JM Huber preserves stickiness by investing in technical service and application support, accelerating requalification timelines and lowering customer incentive to switch.

Price sensitivity cycles

Construction and industrial demand is cyclical, amplifying buyer price sensitivity in downturns as firms trim projects; global construction output was about $13 trillion in 2023, putting volume risk squarely on suppliers. Buyers pursue downsizing, substitute blends or extended payment terms to preserve cash, increasing bargaining leverage. In up-cycles availability and service trump price, so JM Huber uses dynamic pricing and allocation policies to manage swings and protect margins.

Private label and reformulation

Savvy buyers push private-label or reformulated hydrocolloid blends to cut costs; North American private-label penetration reached about 18–20% in 2024, increasing margin pressure. Hydrocolloid systems can be swapped to lower-cost chemistries if performance tolerances allow, and engineered-wood customers routinely mix SKUs to value-engineer builds. Huber’s application labs and demonstrated value-in-use help defend pricing and specification stickiness.

- Private-label penetration ~18–20% (2024)

- Hydrocolloid reformulation lowers COGS if specs permit

- Engineered-wood SKU mixing for value-engineering

- Huber labs preserve specification and margin

Contracting and terms

Annual and biannual contracts with indexation, volume tiers, and SLAs concentrate bargaining power by linking price to raw-material indices while locking volumes and service levels; buyers counter this via multi-sourcing and should-cost models, pressuring margins. Huber trades committed volumes for price stability and priority supply, using penalties and lead-time guarantees to allocate risk and protect throughput.

- Contract cadence: annual/biannual

- Levers: indexation, volume tiers, SLAs

- Buyer tools: multi-sourcing, should-cost

- Huber response: volume for priority, penalties, lead-time guarantees

Concentrated OEM demand, 18–20% private-label and $13T construction fuel price pressure

Large OEMs, distributors and CPG buyers concentrate volume and drive rebates and longer payment terms; private-label penetration ~18–20% (2024) and global construction output ~$13T (2023) amplify price sensitivity. Specification lock-in for engineered woods and hydrocolloids raises switching costs, but requalification cycles and reformulation risk keep margins contested. Huber defends pricing via labs, SLAs, indexed contracts and prioritized supply.

| Metric | Value |

|---|---|

| Private-label penetration | 18–20% (2024) |

| Global construction output | $13T (2023) |

| Contract cadence | Annual/biannual |

Preview Before You Purchase

JM Huber Porter's Five Forces Analysis

This preview shows the exact JM Huber Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The full document is fully formatted, professionally written, and ready for download and use the moment you buy. What you see here is precisely the deliverable available for instant access.