Hugo Boss Porter's Five Forces Analysis

From Overview to Strategy Blueprint

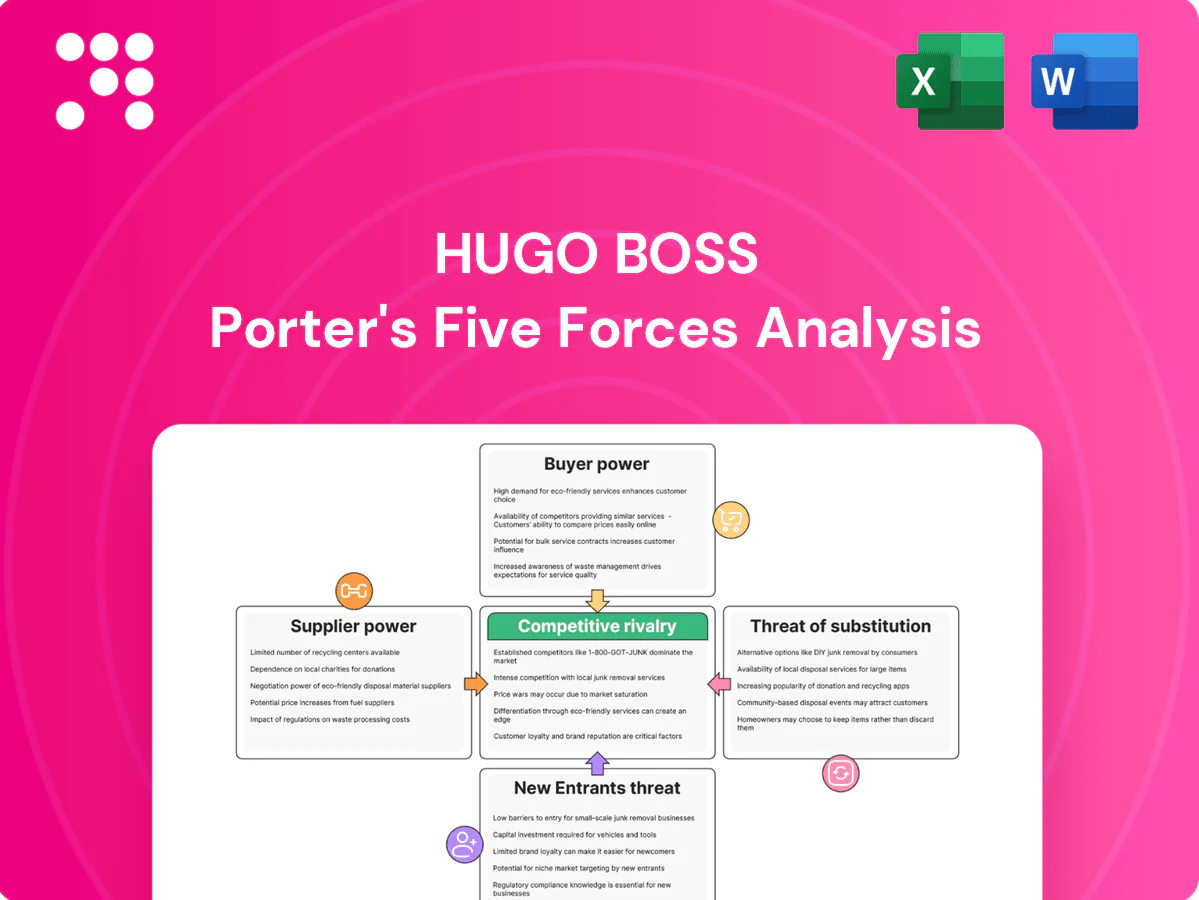

Hugo Boss navigates moderate supplier leverage, strong buyer bargaining in premium menswear, intense rivalry from luxury and fast-fashion brands, and a moderate threat from new entrants and substitutes driven by shifting consumer tastes and e-commerce. This snapshot highlights key competitive pressures shaping margins and strategic choices. Ready to move beyond the basics? Get a full strategic breakdown of Hugo Boss’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Premium materials scarcity

High-quality wool, cotton, leather and technical fabrics remain concentrated among specialized mills and tanneries, elevating supplier leverage and creating scarcity in 2024. Sustainability-certified inputs further narrowed the pool in 2024, adding price premia and longer lead times. Hugo Boss mitigates with multi-sourcing and long-term agreements but cannot fully dilute scarcity premia. This pressure raises input cost volatility and procurement risk.

Tiered manufacturing base

Production partners across Europe, North Africa and Asia give Hugo Boss sourcing flexibility but increase coordination complexity and logistics costs. Specialized tailoring and finishing vendors exert bargaining power for quality-critical garments, making switches costly due to lengthy qualification and ramp-up times. Switching suppliers is feasible but entails certification, lead-time and cost penalties. Vendor development programs aim to standardize processes and reduce supplier dependence.

Licensed category dependencies

Hugo Boss fragrances, eyewear and watches lean heavily on license partners such as Coty, Safilo and Movado, concentrating supplier power as of 2024. Licensees hold manufacturing know-how and set innovation cadence, while royalty rates in 2024 commonly range 7–12% with minimum guarantees often in the low millions, which can compress margins in downturns. Multi-year agreements and tight brand oversight stabilize long-term outcomes but limit short-term renegotiation flexibility.

Logistics and compliance pressures

Customs, ESG audits and traceability mandates raised supplier compliance costs, constraining margins as Hugo Boss (FY 2024 revenue ~€2.9bn) relies on certified vendors; energy and freight price volatility—partly passed through by suppliers—adds unpredictable cost layers. Strict social and environmental standards slow rapid supplier substitution, and though scale improves negotiating leverage, Hugo Bosss premium positioning forces uncompromised compliance, ceding bargaining room to compliant vendors.

- Compliance cost pressure: traceability + ESG audits

- Pass-through risk: energy & freight volatility

- Supplier stickiness: social/environmental standards

- Scale vs premium: bargaining constrained

Countervailing brand scale

Hugo Boss’s large, predictable volumes and global cadence—active in 100+ markets in 2024—give it preferred-partner status with key suppliers, lowering suppliers’ risk and securing price and capacity priority; vendor financing and detailed forecasting further improve commercial terms, leaving supplier bargaining power moderate, mitigated by brand scale and multi-sourcing.

- Preferred-partner status: higher order visibility

- Pricing/capacity priority: reduces supplier risk

- Vendor financing & forecasting: better terms

- Overall: supplier power moderate

Scale offsets supplier pressure: €2.9bn, 100+ markets, royalties 7–12%

Supplier power is moderate: high-concentration inputs (wool/leather) and certified suppliers push premiums and lead times, while Hugo Boss’s FY 2024 revenue ~€2.9bn and 100+ markets give scale and preferred-partner leverage. License royalties (7–12%) and compliance costs raise supplier influence, but multi-sourcing and long-term contracts mitigate risks and secure capacity.

| Metric | 2024 |

|---|---|

| Revenue | €2.9bn |

| Markets | 100+ |

| License royalties | 7–12% |

| Supplier concentration | High for premium fabrics |

What is included in the product

Concise Porter's Five Forces analysis of Hugo Boss highlighting competitive rivalry, buyer and supplier power, threats from entrants and substitutes, and strategic implications for pricing and profitability.

A clear, one-sheet Porter's Five Forces summary for Hugo Boss—perfect for quick decision-making on supplier power, brand rivalry, and retail/distribution threats.

Customers Bargaining Power

Low switching costs

Affluent consumers can readily switch among premium brands with similar aesthetics and quality, and minimal contractual lock‑in in fashion amplifies this mobility. Online marketplaces and search transparency — with luxury e‑commerce penetration around 25% in 2024 — lower information barriers and raise comparability. This keeps price sensitivity episodically high, especially for non‑hero products, pressuring margins and promotion frequency.

Wholesale leverage

Department stores, specialty retailers and pure‑play e‑commerce push markdown support, delivery windows and slotting, and their consolidation in key markets concentrates negotiating power and pricing pressure on Hugo Boss. Order cancellations and chargebacks shift inventory and margin risk upstream to the brand. Hugo Boss’s direct‑to‑consumer channel now represents around one third of sales (≈33%), partly offsetting wholesale leverage.

Price–value scrutiny

Macro slowdowns push customers toward promotions, outlets, and entry-price capsules, a dynamic Hugo Boss countered in 2024 after FY 2023 sales of about €2.8bn; frequent discounting trains buyers to wait and raises price elasticity. Clear quality cues and distinct design stories reduce haggling, while loyalty programs and personalization improve perceived value and soften customer bargaining power.

Omnichannel expectations

Buyers demand seamless availability, fast shipping and easy returns; Salesforce 2024 found 76% of shoppers expect consistent omnichannel experiences and Statista 2024 reports ~28% of apparel sales occur online, raising immediate churn risk if Hugo Boss misses SLAs. Meeting those SLAs increases fulfilment and reverse-logistics costs, squeezing margins, while superior CX and data-driven merchandising reduce defection by improving personalization and conversion.

- 76% shoppers expect omnichannel consistency (Salesforce 2024); ~28% apparel online share (Statista 2024); higher SLAs = cost pressure; superior CX/data reduces churn

Influence of tastemakers

Stylists, influencers and reviews heavily shape preference formation for premium menswear; viral trends in 2024 rerouted demand away from planned assortments within weeks, increasing collective buyer power while pressuring inventory turns.

Hugo Boss offsets this by leveraging brand ambassadors and capsule collaborations (including runway-to-retail drops), enabling rapid demand steering and premium margin protection.

Net effect on bargaining power is moderate to high due to speed and visibility of tastemaker-driven shifts.

- 2024 brand revenue focus: rapid sell-through via collaborations

- Influencer-driven spikes can reduce forecast accuracy by weeks

- Ambassador programs improve demand elasticity control

Premium fashion DTC: 33% sales, 25% e-commerce share, omnichannel risk

Customers have moderate-high bargaining power: luxury e‑commerce ~25% (2024), Hugo Boss DTC ≈33% of sales, FY2023 sales ≈€2.8bn; 76% expect omnichannel consistency (Salesforce 2024) raising SLA costs and churn risk. Retail consolidation and influencer volatility increase price sensitivity and inventory pressure, while loyalty and collaborations soften leverage.

| Metric | Value |

|---|---|

| Luxury e‑commerce | ≈25% (2024) |

| Hugo Boss DTC | ≈33% sales |

| FY2023 revenue | ≈€2.8bn |

What You See Is What You Get

Hugo Boss Porter's Five Forces Analysis

This preview shows the Hugo Boss Porter’s Five Forces analysis exactly as delivered—no placeholders or mockups. It’s the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threats of entry and substitutes. Purchase grants immediate access to this same ready-to-use file.

From Overview to Strategy Blueprint

Hugo Boss navigates moderate supplier leverage, strong buyer bargaining in premium menswear, intense rivalry from luxury and fast-fashion brands, and a moderate threat from new entrants and substitutes driven by shifting consumer tastes and e-commerce. This snapshot highlights key competitive pressures shaping margins and strategic choices. Ready to move beyond the basics? Get a full strategic breakdown of Hugo Boss’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Premium materials scarcity

High-quality wool, cotton, leather and technical fabrics remain concentrated among specialized mills and tanneries, elevating supplier leverage and creating scarcity in 2024. Sustainability-certified inputs further narrowed the pool in 2024, adding price premia and longer lead times. Hugo Boss mitigates with multi-sourcing and long-term agreements but cannot fully dilute scarcity premia. This pressure raises input cost volatility and procurement risk.

Tiered manufacturing base

Production partners across Europe, North Africa and Asia give Hugo Boss sourcing flexibility but increase coordination complexity and logistics costs. Specialized tailoring and finishing vendors exert bargaining power for quality-critical garments, making switches costly due to lengthy qualification and ramp-up times. Switching suppliers is feasible but entails certification, lead-time and cost penalties. Vendor development programs aim to standardize processes and reduce supplier dependence.

Licensed category dependencies

Hugo Boss fragrances, eyewear and watches lean heavily on license partners such as Coty, Safilo and Movado, concentrating supplier power as of 2024. Licensees hold manufacturing know-how and set innovation cadence, while royalty rates in 2024 commonly range 7–12% with minimum guarantees often in the low millions, which can compress margins in downturns. Multi-year agreements and tight brand oversight stabilize long-term outcomes but limit short-term renegotiation flexibility.

Logistics and compliance pressures

Customs, ESG audits and traceability mandates raised supplier compliance costs, constraining margins as Hugo Boss (FY 2024 revenue ~€2.9bn) relies on certified vendors; energy and freight price volatility—partly passed through by suppliers—adds unpredictable cost layers. Strict social and environmental standards slow rapid supplier substitution, and though scale improves negotiating leverage, Hugo Bosss premium positioning forces uncompromised compliance, ceding bargaining room to compliant vendors.

- Compliance cost pressure: traceability + ESG audits

- Pass-through risk: energy & freight volatility

- Supplier stickiness: social/environmental standards

- Scale vs premium: bargaining constrained

Countervailing brand scale

Hugo Boss’s large, predictable volumes and global cadence—active in 100+ markets in 2024—give it preferred-partner status with key suppliers, lowering suppliers’ risk and securing price and capacity priority; vendor financing and detailed forecasting further improve commercial terms, leaving supplier bargaining power moderate, mitigated by brand scale and multi-sourcing.

- Preferred-partner status: higher order visibility

- Pricing/capacity priority: reduces supplier risk

- Vendor financing & forecasting: better terms

- Overall: supplier power moderate

Scale offsets supplier pressure: €2.9bn, 100+ markets, royalties 7–12%

Supplier power is moderate: high-concentration inputs (wool/leather) and certified suppliers push premiums and lead times, while Hugo Boss’s FY 2024 revenue ~€2.9bn and 100+ markets give scale and preferred-partner leverage. License royalties (7–12%) and compliance costs raise supplier influence, but multi-sourcing and long-term contracts mitigate risks and secure capacity.

| Metric | 2024 |

|---|---|

| Revenue | €2.9bn |

| Markets | 100+ |

| License royalties | 7–12% |

| Supplier concentration | High for premium fabrics |

What is included in the product

Concise Porter's Five Forces analysis of Hugo Boss highlighting competitive rivalry, buyer and supplier power, threats from entrants and substitutes, and strategic implications for pricing and profitability.

A clear, one-sheet Porter's Five Forces summary for Hugo Boss—perfect for quick decision-making on supplier power, brand rivalry, and retail/distribution threats.

Customers Bargaining Power

Low switching costs

Affluent consumers can readily switch among premium brands with similar aesthetics and quality, and minimal contractual lock‑in in fashion amplifies this mobility. Online marketplaces and search transparency — with luxury e‑commerce penetration around 25% in 2024 — lower information barriers and raise comparability. This keeps price sensitivity episodically high, especially for non‑hero products, pressuring margins and promotion frequency.

Wholesale leverage

Department stores, specialty retailers and pure‑play e‑commerce push markdown support, delivery windows and slotting, and their consolidation in key markets concentrates negotiating power and pricing pressure on Hugo Boss. Order cancellations and chargebacks shift inventory and margin risk upstream to the brand. Hugo Boss’s direct‑to‑consumer channel now represents around one third of sales (≈33%), partly offsetting wholesale leverage.

Price–value scrutiny

Macro slowdowns push customers toward promotions, outlets, and entry-price capsules, a dynamic Hugo Boss countered in 2024 after FY 2023 sales of about €2.8bn; frequent discounting trains buyers to wait and raises price elasticity. Clear quality cues and distinct design stories reduce haggling, while loyalty programs and personalization improve perceived value and soften customer bargaining power.

Omnichannel expectations

Buyers demand seamless availability, fast shipping and easy returns; Salesforce 2024 found 76% of shoppers expect consistent omnichannel experiences and Statista 2024 reports ~28% of apparel sales occur online, raising immediate churn risk if Hugo Boss misses SLAs. Meeting those SLAs increases fulfilment and reverse-logistics costs, squeezing margins, while superior CX and data-driven merchandising reduce defection by improving personalization and conversion.

- 76% shoppers expect omnichannel consistency (Salesforce 2024); ~28% apparel online share (Statista 2024); higher SLAs = cost pressure; superior CX/data reduces churn

Influence of tastemakers

Stylists, influencers and reviews heavily shape preference formation for premium menswear; viral trends in 2024 rerouted demand away from planned assortments within weeks, increasing collective buyer power while pressuring inventory turns.

Hugo Boss offsets this by leveraging brand ambassadors and capsule collaborations (including runway-to-retail drops), enabling rapid demand steering and premium margin protection.

Net effect on bargaining power is moderate to high due to speed and visibility of tastemaker-driven shifts.

- 2024 brand revenue focus: rapid sell-through via collaborations

- Influencer-driven spikes can reduce forecast accuracy by weeks

- Ambassador programs improve demand elasticity control

Premium fashion DTC: 33% sales, 25% e-commerce share, omnichannel risk

Customers have moderate-high bargaining power: luxury e‑commerce ~25% (2024), Hugo Boss DTC ≈33% of sales, FY2023 sales ≈€2.8bn; 76% expect omnichannel consistency (Salesforce 2024) raising SLA costs and churn risk. Retail consolidation and influencer volatility increase price sensitivity and inventory pressure, while loyalty and collaborations soften leverage.

| Metric | Value |

|---|---|

| Luxury e‑commerce | ≈25% (2024) |

| Hugo Boss DTC | ≈33% sales |

| FY2023 revenue | ≈€2.8bn |

What You See Is What You Get

Hugo Boss Porter's Five Forces Analysis

This preview shows the Hugo Boss Porter’s Five Forces analysis exactly as delivered—no placeholders or mockups. It’s the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threats of entry and substitutes. Purchase grants immediate access to this same ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Hugo Boss navigates moderate supplier leverage, strong buyer bargaining in premium menswear, intense rivalry from luxury and fast-fashion brands, and a moderate threat from new entrants and substitutes driven by shifting consumer tastes and e-commerce. This snapshot highlights key competitive pressures shaping margins and strategic choices. Ready to move beyond the basics? Get a full strategic breakdown of Hugo Boss’s market position, competitive intensity, and external threats—all in one powerful analysis.

Suppliers Bargaining Power

Premium materials scarcity

High-quality wool, cotton, leather and technical fabrics remain concentrated among specialized mills and tanneries, elevating supplier leverage and creating scarcity in 2024. Sustainability-certified inputs further narrowed the pool in 2024, adding price premia and longer lead times. Hugo Boss mitigates with multi-sourcing and long-term agreements but cannot fully dilute scarcity premia. This pressure raises input cost volatility and procurement risk.

Tiered manufacturing base

Production partners across Europe, North Africa and Asia give Hugo Boss sourcing flexibility but increase coordination complexity and logistics costs. Specialized tailoring and finishing vendors exert bargaining power for quality-critical garments, making switches costly due to lengthy qualification and ramp-up times. Switching suppliers is feasible but entails certification, lead-time and cost penalties. Vendor development programs aim to standardize processes and reduce supplier dependence.

Licensed category dependencies

Hugo Boss fragrances, eyewear and watches lean heavily on license partners such as Coty, Safilo and Movado, concentrating supplier power as of 2024. Licensees hold manufacturing know-how and set innovation cadence, while royalty rates in 2024 commonly range 7–12% with minimum guarantees often in the low millions, which can compress margins in downturns. Multi-year agreements and tight brand oversight stabilize long-term outcomes but limit short-term renegotiation flexibility.

Logistics and compliance pressures

Customs, ESG audits and traceability mandates raised supplier compliance costs, constraining margins as Hugo Boss (FY 2024 revenue ~€2.9bn) relies on certified vendors; energy and freight price volatility—partly passed through by suppliers—adds unpredictable cost layers. Strict social and environmental standards slow rapid supplier substitution, and though scale improves negotiating leverage, Hugo Bosss premium positioning forces uncompromised compliance, ceding bargaining room to compliant vendors.

- Compliance cost pressure: traceability + ESG audits

- Pass-through risk: energy & freight volatility

- Supplier stickiness: social/environmental standards

- Scale vs premium: bargaining constrained

Countervailing brand scale

Hugo Boss’s large, predictable volumes and global cadence—active in 100+ markets in 2024—give it preferred-partner status with key suppliers, lowering suppliers’ risk and securing price and capacity priority; vendor financing and detailed forecasting further improve commercial terms, leaving supplier bargaining power moderate, mitigated by brand scale and multi-sourcing.

- Preferred-partner status: higher order visibility

- Pricing/capacity priority: reduces supplier risk

- Vendor financing & forecasting: better terms

- Overall: supplier power moderate

Scale offsets supplier pressure: €2.9bn, 100+ markets, royalties 7–12%

Supplier power is moderate: high-concentration inputs (wool/leather) and certified suppliers push premiums and lead times, while Hugo Boss’s FY 2024 revenue ~€2.9bn and 100+ markets give scale and preferred-partner leverage. License royalties (7–12%) and compliance costs raise supplier influence, but multi-sourcing and long-term contracts mitigate risks and secure capacity.

| Metric | 2024 |

|---|---|

| Revenue | €2.9bn |

| Markets | 100+ |

| License royalties | 7–12% |

| Supplier concentration | High for premium fabrics |

What is included in the product

Concise Porter's Five Forces analysis of Hugo Boss highlighting competitive rivalry, buyer and supplier power, threats from entrants and substitutes, and strategic implications for pricing and profitability.

A clear, one-sheet Porter's Five Forces summary for Hugo Boss—perfect for quick decision-making on supplier power, brand rivalry, and retail/distribution threats.

Customers Bargaining Power

Low switching costs

Affluent consumers can readily switch among premium brands with similar aesthetics and quality, and minimal contractual lock‑in in fashion amplifies this mobility. Online marketplaces and search transparency — with luxury e‑commerce penetration around 25% in 2024 — lower information barriers and raise comparability. This keeps price sensitivity episodically high, especially for non‑hero products, pressuring margins and promotion frequency.

Wholesale leverage

Department stores, specialty retailers and pure‑play e‑commerce push markdown support, delivery windows and slotting, and their consolidation in key markets concentrates negotiating power and pricing pressure on Hugo Boss. Order cancellations and chargebacks shift inventory and margin risk upstream to the brand. Hugo Boss’s direct‑to‑consumer channel now represents around one third of sales (≈33%), partly offsetting wholesale leverage.

Price–value scrutiny

Macro slowdowns push customers toward promotions, outlets, and entry-price capsules, a dynamic Hugo Boss countered in 2024 after FY 2023 sales of about €2.8bn; frequent discounting trains buyers to wait and raises price elasticity. Clear quality cues and distinct design stories reduce haggling, while loyalty programs and personalization improve perceived value and soften customer bargaining power.

Omnichannel expectations

Buyers demand seamless availability, fast shipping and easy returns; Salesforce 2024 found 76% of shoppers expect consistent omnichannel experiences and Statista 2024 reports ~28% of apparel sales occur online, raising immediate churn risk if Hugo Boss misses SLAs. Meeting those SLAs increases fulfilment and reverse-logistics costs, squeezing margins, while superior CX and data-driven merchandising reduce defection by improving personalization and conversion.

- 76% shoppers expect omnichannel consistency (Salesforce 2024); ~28% apparel online share (Statista 2024); higher SLAs = cost pressure; superior CX/data reduces churn

Influence of tastemakers

Stylists, influencers and reviews heavily shape preference formation for premium menswear; viral trends in 2024 rerouted demand away from planned assortments within weeks, increasing collective buyer power while pressuring inventory turns.

Hugo Boss offsets this by leveraging brand ambassadors and capsule collaborations (including runway-to-retail drops), enabling rapid demand steering and premium margin protection.

Net effect on bargaining power is moderate to high due to speed and visibility of tastemaker-driven shifts.

- 2024 brand revenue focus: rapid sell-through via collaborations

- Influencer-driven spikes can reduce forecast accuracy by weeks

- Ambassador programs improve demand elasticity control

Premium fashion DTC: 33% sales, 25% e-commerce share, omnichannel risk

Customers have moderate-high bargaining power: luxury e‑commerce ~25% (2024), Hugo Boss DTC ≈33% of sales, FY2023 sales ≈€2.8bn; 76% expect omnichannel consistency (Salesforce 2024) raising SLA costs and churn risk. Retail consolidation and influencer volatility increase price sensitivity and inventory pressure, while loyalty and collaborations soften leverage.

| Metric | Value |

|---|---|

| Luxury e‑commerce | ≈25% (2024) |

| Hugo Boss DTC | ≈33% sales |

| FY2023 revenue | ≈€2.8bn |

What You See Is What You Get

Hugo Boss Porter's Five Forces Analysis

This preview shows the Hugo Boss Porter’s Five Forces analysis exactly as delivered—no placeholders or mockups. It’s the full, professionally formatted document covering competitive rivalry, supplier and buyer power, threats of entry and substitutes. Purchase grants immediate access to this same ready-to-use file.