Hugo Boss PESTLE Analysis

Skip the Research. Get the Strategy.

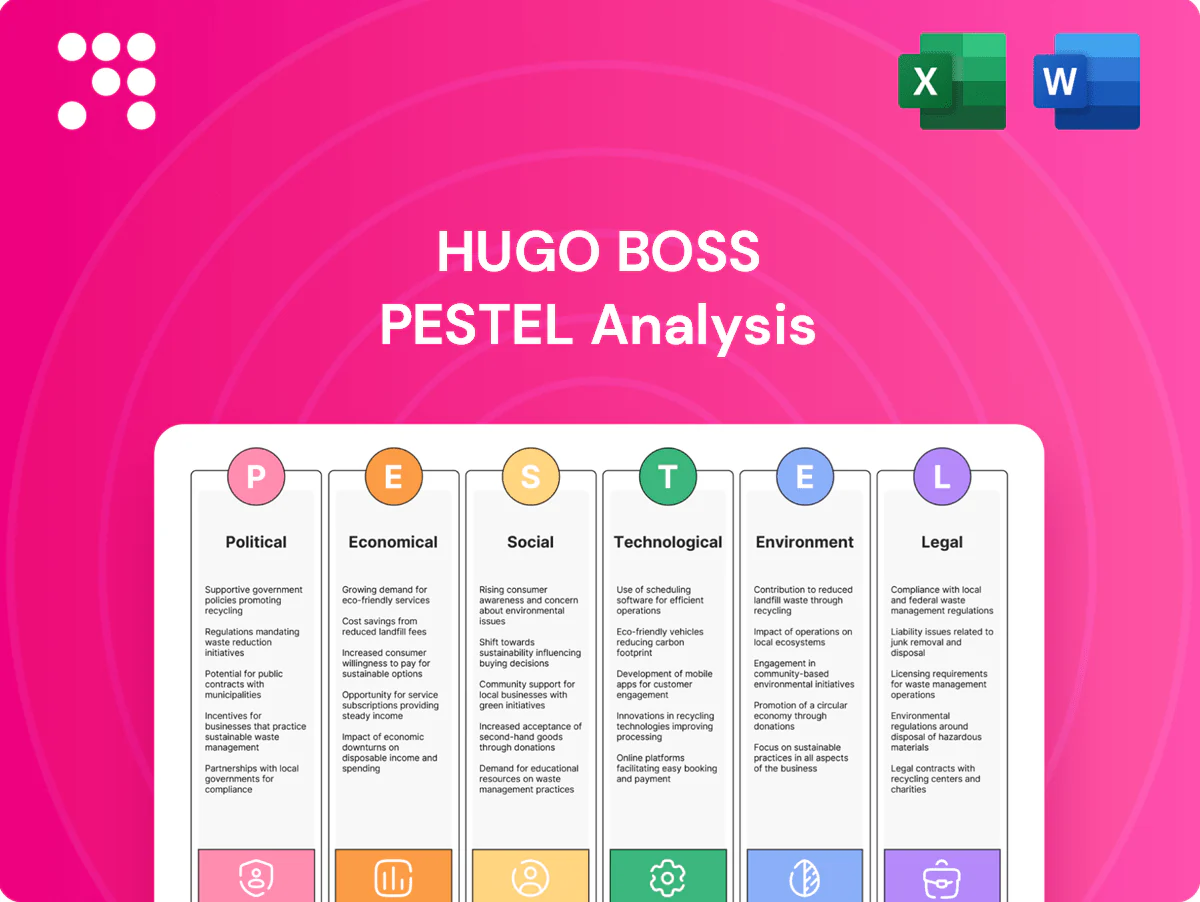

Gain strategic clarity with our PESTLE Analysis of Hugo Boss—external political, economic, social, technological, legal, and environmental forces explained to reveal risks and growth levers for the brand. Ideal for investors and strategists, this concise briefing points to actionable moves. Purchase the full, editable report for complete insights.

Political factors

Trade policies and tariffs

Global sourcing exposes HUGO BOSS to EU, US and UK tariff regimes and retaliatory duties—US Section 301 tariffs on select Chinese goods remain up to 25% and the EU‑Turkey Customs Union (since 1995) shapes Turkish costs. The EU‑Vietnam FTA (effective 2020) cuts tariffs on about 99% of goods, creating sourcing arbitrage but requiring EUR.1 and other compliance docs. Scenario planning and supplier diversification reduce shock risk.

Geopolitical instability and supply chain risk

Conflicts and sanctions disrupt material flows, logistics corridors and retail ops for Hugo Boss, as seaborne trade carries roughly 80% of global merchandise by volume (UNCTAD 2023). Rerouting air and sea freight raises lead times by weeks and boosts costs, squeezing seasonal collection margins. Regional instability also dents demand in luxury hubs: China/HK accounted for about 35% of global luxury spend (Bain 2024). Building multi-country production footprints and nearshoring buffers this volatility.

Government support and incentives

EU programmes such as Digital Europe (€7.5bn 2021–2027) and NextGenerationEU (€806.9bn recovery package) provide subsidies for retail tech and low‑impact materials that can underwrite Hugo Boss capex in digitalization and sustainability. R&D tax relief and national circularity grants (available across key markets) lower effective payback periods on pilots and new materials. Location‑specific investment incentives shape choices for DCs and flagship stores. Active monitoring of policy pipelines guides capital allocation timing and scale.

Public health and contingency policy

Pandemic-era mandates showed how store traffic can collapse quickly, pressuring Hugo Boss to shift sales online and reallocate labor; group sales were €3.18bn in 2023 while omnichannel investments expanded to protect revenue and margins. Prepared contingency playbooks and flexible staffing reduce policy-driven volatility and sustain service levels across markets.

- Omnichannel readiness

- Flexible staffing

- Contingency playbooks

Political pressure on ESG transparency

Governments increasingly mandate climate and social disclosures — EU CSRD expands reporting to roughly 50,000 companies from 2024 — forcing apparel groups like Hugo Boss to boost transparency; German LkSG (3000+ employees from 2023, 1000+ from 2024) adds supply‑chain scrutiny. High‑profile fashion names face NGO and policymaker investigations; robust reporting helps protect public contracts and supports premium positioning with values‑driven consumers.

- EU CSRD: ~50,000 companies impacted from 2024

- Germany LkSG: 3000+ employees (2023), 1000+ (2024)

- Reporting protects licenses/public contracts; strengthens brand trust

Tariffs, sanctions and China exposure squeeze margins, increase lead times

Global tariffs, sanctions and regional instability raise sourcing and logistics costs for Hugo Boss, pressuring margins and lead times; group sales €3.18bn (2023) and China/HK ~35% of luxury spend (Bain 2024) increase exposure. EU CSRD (~50,000 firms) and Germany LkSG (thresholds 3,000/1,000 employees) heighten compliance costs and reporting needs.

| Metric | Value |

|---|---|

| 2023 Sales | €3.18bn |

| China/HK luxury share | ~35% (Bain 2024) |

| EU CSRD scope | ~50,000 firms (from 2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Hugo Boss across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed sections, firm-specific sub-points and forward-looking insights to help executives, consultants and investors identify threats, opportunities and strategic responses.

A concise, visually segmented PESTLE summary of Hugo Boss that can be dropped into presentations, shared across teams, and annotated for regional specifics—streamlining external risk discussions and strategic planning.

Economic factors

Premium demand sensitivity

As a premium brand, HUGO BOSS is highly cyclical and closely tied to affluent discretionary spending, making demand sensitive to interest rates, inflation and consumer confidence. In downturns trading-down risk and softer category mix reduce average ticket sizes, while recovery phases and event-driven dressing lift sales. Price architecture and a targeted outlet strategy are used to smooth revenue volatility and protect full-price margins.

Currency fluctuations

Hugo Boss reported group sales of €3.655bn in 2023 with revenue streams split across EUR, USD and CNY, while sourcing and production costs span multiple currencies; FX volatility therefore directly pressures gross margins and reported top‑line growth. The group uses forward hedging and natural currency offsets in sourcing to stabilize earnings, and pricing updates must balance local elasticity and competitor moves to protect margins.

Wholesale vs. DTC mix

By 2024 Hugo Boss accelerated DTC expansion—own retail and e-commerce lift gross margins but increase fixed-cost and inventory leverage. Wholesale still provides geographic reach and working-capital advantages while constraining pricing and brand control. Fine-tuning channel mix by market helps balance growth and margin risk, and improved omnichannel services boost conversion rates and average order value.

Tourism and travel retail

Luxury hubs like Paris and Dubai continue to benefit from international tourism and duty-free channels as UNWTO data shows arrivals at about 88% of 2019 levels in 2024; exchange-rate swings and visa policies materially shift tourist spend, while long-haul travel recovery (IATA capacity ~90% of 2019 in 2024) boosts formalwear and gifting demand and favors localized assortments to match regional tastes.

- Tourism flows: arrivals ~88% of 2019 (2024)

- Long-haul capacity ~90% of 2019 (2024)

- Duty-free: key channel for premium sales

- Localized assortments drive conversion

Input cost inflation

Material, energy and labor cost inflation continued to pressure Hugo Bosss COGS and store opex, with European energy costs easing from 2022 peaks into 2024 but wage inflation persisting in key markets.

- Freight volatility and capacity limits disrupted seasonal deliveries despite normalized container rates in 2024

- Strategic sourcing, fabric standardization and vendor partnerships reduced input exposure

- Selective pricing and value engineering preserved perceived quality

Tariffs, sanctions and China exposure squeeze margins, increase lead times

HUGO BOSS is cyclical and sensitive to rates, inflation and consumer confidence; price architecture, outlet mix and hedging are used to protect margins. FX volatility and multi-currency sourcing directly pressure gross margins; forward hedges and natural offsets mitigate risk. DTC expansion improves gross margin but raises fixed costs and inventory leverage; tourism recovery (2024) supports premium demand.

| Metric | Value |

|---|---|

| Group sales (2023) | €3.655bn |

| Tourism arrivals (2024 vs 2019) | ~88% |

| Long-haul capacity (2024 vs 2019) | ~90% |

| Key risks | FX, wage inflation, freight volatility |

Same Document Delivered

Hugo Boss PESTLE Analysis

The preview shown here is the exact Hugo Boss PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed, with no placeholders or missing sections. After checkout you’ll instantly download this same professionally structured file.

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Hugo Boss—external political, economic, social, technological, legal, and environmental forces explained to reveal risks and growth levers for the brand. Ideal for investors and strategists, this concise briefing points to actionable moves. Purchase the full, editable report for complete insights.

Political factors

Trade policies and tariffs

Global sourcing exposes HUGO BOSS to EU, US and UK tariff regimes and retaliatory duties—US Section 301 tariffs on select Chinese goods remain up to 25% and the EU‑Turkey Customs Union (since 1995) shapes Turkish costs. The EU‑Vietnam FTA (effective 2020) cuts tariffs on about 99% of goods, creating sourcing arbitrage but requiring EUR.1 and other compliance docs. Scenario planning and supplier diversification reduce shock risk.

Geopolitical instability and supply chain risk

Conflicts and sanctions disrupt material flows, logistics corridors and retail ops for Hugo Boss, as seaborne trade carries roughly 80% of global merchandise by volume (UNCTAD 2023). Rerouting air and sea freight raises lead times by weeks and boosts costs, squeezing seasonal collection margins. Regional instability also dents demand in luxury hubs: China/HK accounted for about 35% of global luxury spend (Bain 2024). Building multi-country production footprints and nearshoring buffers this volatility.

Government support and incentives

EU programmes such as Digital Europe (€7.5bn 2021–2027) and NextGenerationEU (€806.9bn recovery package) provide subsidies for retail tech and low‑impact materials that can underwrite Hugo Boss capex in digitalization and sustainability. R&D tax relief and national circularity grants (available across key markets) lower effective payback periods on pilots and new materials. Location‑specific investment incentives shape choices for DCs and flagship stores. Active monitoring of policy pipelines guides capital allocation timing and scale.

Public health and contingency policy

Pandemic-era mandates showed how store traffic can collapse quickly, pressuring Hugo Boss to shift sales online and reallocate labor; group sales were €3.18bn in 2023 while omnichannel investments expanded to protect revenue and margins. Prepared contingency playbooks and flexible staffing reduce policy-driven volatility and sustain service levels across markets.

- Omnichannel readiness

- Flexible staffing

- Contingency playbooks

Political pressure on ESG transparency

Governments increasingly mandate climate and social disclosures — EU CSRD expands reporting to roughly 50,000 companies from 2024 — forcing apparel groups like Hugo Boss to boost transparency; German LkSG (3000+ employees from 2023, 1000+ from 2024) adds supply‑chain scrutiny. High‑profile fashion names face NGO and policymaker investigations; robust reporting helps protect public contracts and supports premium positioning with values‑driven consumers.

- EU CSRD: ~50,000 companies impacted from 2024

- Germany LkSG: 3000+ employees (2023), 1000+ (2024)

- Reporting protects licenses/public contracts; strengthens brand trust

Tariffs, sanctions and China exposure squeeze margins, increase lead times

Global tariffs, sanctions and regional instability raise sourcing and logistics costs for Hugo Boss, pressuring margins and lead times; group sales €3.18bn (2023) and China/HK ~35% of luxury spend (Bain 2024) increase exposure. EU CSRD (~50,000 firms) and Germany LkSG (thresholds 3,000/1,000 employees) heighten compliance costs and reporting needs.

| Metric | Value |

|---|---|

| 2023 Sales | €3.18bn |

| China/HK luxury share | ~35% (Bain 2024) |

| EU CSRD scope | ~50,000 firms (from 2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Hugo Boss across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed sections, firm-specific sub-points and forward-looking insights to help executives, consultants and investors identify threats, opportunities and strategic responses.

A concise, visually segmented PESTLE summary of Hugo Boss that can be dropped into presentations, shared across teams, and annotated for regional specifics—streamlining external risk discussions and strategic planning.

Economic factors

Premium demand sensitivity

As a premium brand, HUGO BOSS is highly cyclical and closely tied to affluent discretionary spending, making demand sensitive to interest rates, inflation and consumer confidence. In downturns trading-down risk and softer category mix reduce average ticket sizes, while recovery phases and event-driven dressing lift sales. Price architecture and a targeted outlet strategy are used to smooth revenue volatility and protect full-price margins.

Currency fluctuations

Hugo Boss reported group sales of €3.655bn in 2023 with revenue streams split across EUR, USD and CNY, while sourcing and production costs span multiple currencies; FX volatility therefore directly pressures gross margins and reported top‑line growth. The group uses forward hedging and natural currency offsets in sourcing to stabilize earnings, and pricing updates must balance local elasticity and competitor moves to protect margins.

Wholesale vs. DTC mix

By 2024 Hugo Boss accelerated DTC expansion—own retail and e-commerce lift gross margins but increase fixed-cost and inventory leverage. Wholesale still provides geographic reach and working-capital advantages while constraining pricing and brand control. Fine-tuning channel mix by market helps balance growth and margin risk, and improved omnichannel services boost conversion rates and average order value.

Tourism and travel retail

Luxury hubs like Paris and Dubai continue to benefit from international tourism and duty-free channels as UNWTO data shows arrivals at about 88% of 2019 levels in 2024; exchange-rate swings and visa policies materially shift tourist spend, while long-haul travel recovery (IATA capacity ~90% of 2019 in 2024) boosts formalwear and gifting demand and favors localized assortments to match regional tastes.

- Tourism flows: arrivals ~88% of 2019 (2024)

- Long-haul capacity ~90% of 2019 (2024)

- Duty-free: key channel for premium sales

- Localized assortments drive conversion

Input cost inflation

Material, energy and labor cost inflation continued to pressure Hugo Bosss COGS and store opex, with European energy costs easing from 2022 peaks into 2024 but wage inflation persisting in key markets.

- Freight volatility and capacity limits disrupted seasonal deliveries despite normalized container rates in 2024

- Strategic sourcing, fabric standardization and vendor partnerships reduced input exposure

- Selective pricing and value engineering preserved perceived quality

Tariffs, sanctions and China exposure squeeze margins, increase lead times

HUGO BOSS is cyclical and sensitive to rates, inflation and consumer confidence; price architecture, outlet mix and hedging are used to protect margins. FX volatility and multi-currency sourcing directly pressure gross margins; forward hedges and natural offsets mitigate risk. DTC expansion improves gross margin but raises fixed costs and inventory leverage; tourism recovery (2024) supports premium demand.

| Metric | Value |

|---|---|

| Group sales (2023) | €3.655bn |

| Tourism arrivals (2024 vs 2019) | ~88% |

| Long-haul capacity (2024 vs 2019) | ~90% |

| Key risks | FX, wage inflation, freight volatility |

Same Document Delivered

Hugo Boss PESTLE Analysis

The preview shown here is the exact Hugo Boss PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed, with no placeholders or missing sections. After checkout you’ll instantly download this same professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Hugo Boss—external political, economic, social, technological, legal, and environmental forces explained to reveal risks and growth levers for the brand. Ideal for investors and strategists, this concise briefing points to actionable moves. Purchase the full, editable report for complete insights.

Political factors

Trade policies and tariffs

Global sourcing exposes HUGO BOSS to EU, US and UK tariff regimes and retaliatory duties—US Section 301 tariffs on select Chinese goods remain up to 25% and the EU‑Turkey Customs Union (since 1995) shapes Turkish costs. The EU‑Vietnam FTA (effective 2020) cuts tariffs on about 99% of goods, creating sourcing arbitrage but requiring EUR.1 and other compliance docs. Scenario planning and supplier diversification reduce shock risk.

Geopolitical instability and supply chain risk

Conflicts and sanctions disrupt material flows, logistics corridors and retail ops for Hugo Boss, as seaborne trade carries roughly 80% of global merchandise by volume (UNCTAD 2023). Rerouting air and sea freight raises lead times by weeks and boosts costs, squeezing seasonal collection margins. Regional instability also dents demand in luxury hubs: China/HK accounted for about 35% of global luxury spend (Bain 2024). Building multi-country production footprints and nearshoring buffers this volatility.

Government support and incentives

EU programmes such as Digital Europe (€7.5bn 2021–2027) and NextGenerationEU (€806.9bn recovery package) provide subsidies for retail tech and low‑impact materials that can underwrite Hugo Boss capex in digitalization and sustainability. R&D tax relief and national circularity grants (available across key markets) lower effective payback periods on pilots and new materials. Location‑specific investment incentives shape choices for DCs and flagship stores. Active monitoring of policy pipelines guides capital allocation timing and scale.

Public health and contingency policy

Pandemic-era mandates showed how store traffic can collapse quickly, pressuring Hugo Boss to shift sales online and reallocate labor; group sales were €3.18bn in 2023 while omnichannel investments expanded to protect revenue and margins. Prepared contingency playbooks and flexible staffing reduce policy-driven volatility and sustain service levels across markets.

- Omnichannel readiness

- Flexible staffing

- Contingency playbooks

Political pressure on ESG transparency

Governments increasingly mandate climate and social disclosures — EU CSRD expands reporting to roughly 50,000 companies from 2024 — forcing apparel groups like Hugo Boss to boost transparency; German LkSG (3000+ employees from 2023, 1000+ from 2024) adds supply‑chain scrutiny. High‑profile fashion names face NGO and policymaker investigations; robust reporting helps protect public contracts and supports premium positioning with values‑driven consumers.

- EU CSRD: ~50,000 companies impacted from 2024

- Germany LkSG: 3000+ employees (2023), 1000+ (2024)

- Reporting protects licenses/public contracts; strengthens brand trust

Tariffs, sanctions and China exposure squeeze margins, increase lead times

Global tariffs, sanctions and regional instability raise sourcing and logistics costs for Hugo Boss, pressuring margins and lead times; group sales €3.18bn (2023) and China/HK ~35% of luxury spend (Bain 2024) increase exposure. EU CSRD (~50,000 firms) and Germany LkSG (thresholds 3,000/1,000 employees) heighten compliance costs and reporting needs.

| Metric | Value |

|---|---|

| 2023 Sales | €3.18bn |

| China/HK luxury share | ~35% (Bain 2024) |

| EU CSRD scope | ~50,000 firms (from 2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Hugo Boss across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed sections, firm-specific sub-points and forward-looking insights to help executives, consultants and investors identify threats, opportunities and strategic responses.

A concise, visually segmented PESTLE summary of Hugo Boss that can be dropped into presentations, shared across teams, and annotated for regional specifics—streamlining external risk discussions and strategic planning.

Economic factors

Premium demand sensitivity

As a premium brand, HUGO BOSS is highly cyclical and closely tied to affluent discretionary spending, making demand sensitive to interest rates, inflation and consumer confidence. In downturns trading-down risk and softer category mix reduce average ticket sizes, while recovery phases and event-driven dressing lift sales. Price architecture and a targeted outlet strategy are used to smooth revenue volatility and protect full-price margins.

Currency fluctuations

Hugo Boss reported group sales of €3.655bn in 2023 with revenue streams split across EUR, USD and CNY, while sourcing and production costs span multiple currencies; FX volatility therefore directly pressures gross margins and reported top‑line growth. The group uses forward hedging and natural currency offsets in sourcing to stabilize earnings, and pricing updates must balance local elasticity and competitor moves to protect margins.

Wholesale vs. DTC mix

By 2024 Hugo Boss accelerated DTC expansion—own retail and e-commerce lift gross margins but increase fixed-cost and inventory leverage. Wholesale still provides geographic reach and working-capital advantages while constraining pricing and brand control. Fine-tuning channel mix by market helps balance growth and margin risk, and improved omnichannel services boost conversion rates and average order value.

Tourism and travel retail

Luxury hubs like Paris and Dubai continue to benefit from international tourism and duty-free channels as UNWTO data shows arrivals at about 88% of 2019 levels in 2024; exchange-rate swings and visa policies materially shift tourist spend, while long-haul travel recovery (IATA capacity ~90% of 2019 in 2024) boosts formalwear and gifting demand and favors localized assortments to match regional tastes.

- Tourism flows: arrivals ~88% of 2019 (2024)

- Long-haul capacity ~90% of 2019 (2024)

- Duty-free: key channel for premium sales

- Localized assortments drive conversion

Input cost inflation

Material, energy and labor cost inflation continued to pressure Hugo Bosss COGS and store opex, with European energy costs easing from 2022 peaks into 2024 but wage inflation persisting in key markets.

- Freight volatility and capacity limits disrupted seasonal deliveries despite normalized container rates in 2024

- Strategic sourcing, fabric standardization and vendor partnerships reduced input exposure

- Selective pricing and value engineering preserved perceived quality

Tariffs, sanctions and China exposure squeeze margins, increase lead times

HUGO BOSS is cyclical and sensitive to rates, inflation and consumer confidence; price architecture, outlet mix and hedging are used to protect margins. FX volatility and multi-currency sourcing directly pressure gross margins; forward hedges and natural offsets mitigate risk. DTC expansion improves gross margin but raises fixed costs and inventory leverage; tourism recovery (2024) supports premium demand.

| Metric | Value |

|---|---|

| Group sales (2023) | €3.655bn |

| Tourism arrivals (2024 vs 2019) | ~88% |

| Long-haul capacity (2024 vs 2019) | ~90% |

| Key risks | FX, wage inflation, freight volatility |

Same Document Delivered

Hugo Boss PESTLE Analysis

The preview shown here is the exact Hugo Boss PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessment as displayed, with no placeholders or missing sections. After checkout you’ll instantly download this same professionally structured file.