Hulu LLC Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

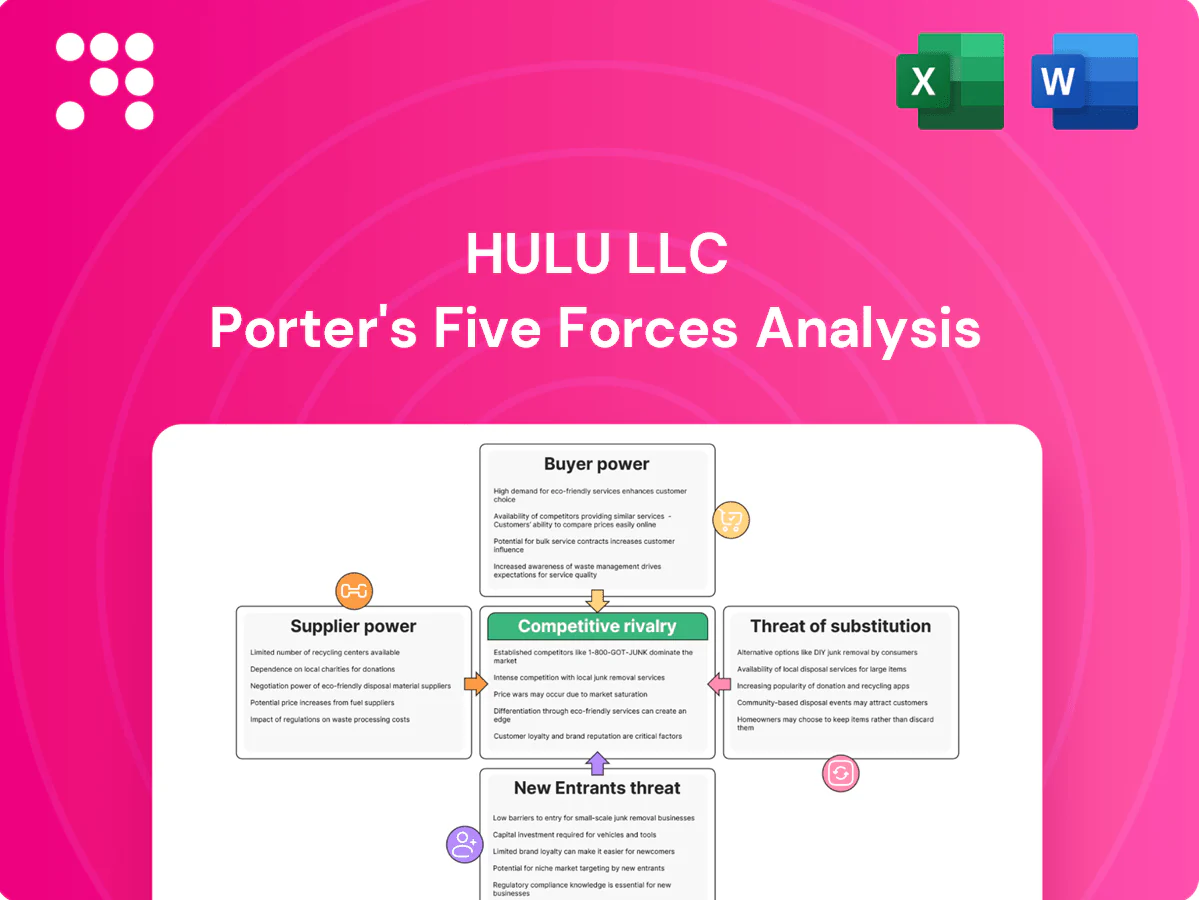

Hulu LLC faces intense rivalry in streaming, strong supplier leverage for premium content, and growing substitute threats from ad-supported and global platforms, while buyer power and regulatory shifts shape pricing and growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Major studios hold leverage

Hulu depends on a handful of networks and studios for next-day TV and big franchises, concentrating bargaining power with suppliers and limiting Hulu's sourcing flexibility. Hit franchises and next-day windows command premium licensing terms, with per-episode fees for top scripted shows often exceeding $1,000,000. Exclusive or first-window deals raise content costs and lock Hulu into higher renewals, while studio consolidation (Disney, Warner Bros. Discovery, Paramount, NBCUniversal) tightens supplier leverage.

Live TV channel costs

Carriage fees for live channels and sports networks are high and rising, with industry reports showing sports-rights inflation running roughly 8–12% annually through 2024, forcing higher per-channel fees for distributors. Programmers can and do threaten blackouts to extract favorable rates, raising short-term bargaining leverage. That inflation cascades into higher content costs that compress margins on Hulu's live tiers and force either price increases or margin erosion.

Tech and distribution gatekeepers

CDNs (Akamai, Cloudflare) and cloud providers (AWS) drive streaming delivery costs and latency; the global CDN market was roughly $24B in 2024, squeezing margins on high-bitrate video. App stores (Apple/Google) still take 15–30% in 2024, and platform placement fees or preferred‑placement deals raise CAC and reduce ARPU. Device OEMs (smart TV and set‑top vendors) control home‑screen real estate, shaping discoverability and engagement. Negotiations over revenue share and placement materially affect user acquisition and retention economics.

Talent and unions power

Guild agreements and talent deals shape Hulu originals' timelines and costs: the 2023 WGA strike lasted 148 days and the SAG-AFTRA strike 118 days, halting new production and delaying releases. Star-driven projects can demand top-tier pay—some A-list leads exceed $1 million per episode—while backend participation and residuals raise long-run expenses. These supplier dynamics increase scheduling risk and margin pressure.

- 148-day WGA strike (2023)

- 118-day SAG-AFTRA strike (2023)

- A-list pay >$1M/episode

- Backend/residuals increase lifecycle cost

Sports and event rights

Premium live sports and event rights remain scarce and highly concentrated among a few leagues and broadcasters, exemplified by the NFL securing about $113 billion in media deals through 2033, highlighting supplier dominance.

Bidding wars push up minimum guarantees and multi-year lock-ins, raising Hulu's distribution costs and exit barriers.

Blackout rules and fragmented regional rights complicate packaging and reduce Hulu's ability to offer nationwide bundled products, amplifying supplier power.

- Sparsity; High guarantees; Lock-ins; Blackouts; Concentrated leverage

Streaming platforms squeezed by studio power, rising sports rights, CDN costs, store cuts, strikes

Hulu faces concentrated supplier power: major studios/networks (Disney, WBD, Paramount, NBCU) and league rights push high guarantees and lock-ins; top scripted per-episode fees often exceed $1,000,000 and sports-rights inflation ran ~8–12% annually through 2024. CDNs/clouds and app stores (global CDN ~$24B in 2024; app store take 15–30%) raise delivery and distribution costs. Guild strikes (WGA 148d, SAG-AFTRA 118d) and A-list pay (> $1M/ep) amplify scheduling and cost risk.

| Metric | 2024/Notable |

|---|---|

| Global CDN market | $24B (2024) |

| Sports-rights inflation | 8–12% pa (through 2024) |

| NFL media deals | $113B through 2033 |

| WGA / SAG-AFTRA | 148d / 118d (2023) |

| A-list pay | > $1M per episode |

What is included in the product

Tailored Porter’s Five Forces analysis for Hulu LLC uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and intensity of rivalry; identifies disruptive streaming trends and content/licensing dynamics shaping pricing and profitability to inform strategic decisions.

A concise one-sheet Porter's Five Forces for Hulu that visualizes competitive pressure via an editable spider chart—customize force levels, swap in your data, export clean slides without macros, and integrate into dashboards or reports for fast, board-ready decision-making.

Customers Bargaining Power

Low switching costs

Consumers can subscribe and cancel Hulu month-to-month with minimal friction, undermining long-term lock-in. Multi-homing is common—US households average about 3.8 streaming subscriptions—weakening Hulu’s pricing power. Churn spikes as content cycles end, with industry monthly churn near 2.5% in 2024. Easy re-entry and low ad-supported pricing (about 7.99 USD/month) keep shoppers highly price-sensitive.

Abundant alternatives

Abundant SVOD/AVOD alternatives—Netflix (~260 million global subs in 2024) and Disney+ (~170 million in 2024), plus Peacock, Paramount+ and ad-supported entrants—give Hulu users leverage. Significant content overlap across platforms reduces differentiation and raises churn risk. Consumers routinely compare price, catalog depth and UX before committing, and time-limited promotions or bundled discounts elsewhere frequently trigger switching.

Ad tolerance vs price

Ad-supported Hulu trades lower price ($7.99/month in 2024) for increased ad load (industry ~9 minutes/hour), and users react quickly to higher frequency, driving churn or upgrades; Disney's Hulu ecosystem (~49 million subscribers in 2024) makes small shifts impactful. Advertisers' targeting demands further shape ad density, so perceived value hinges on balancing cost savings against interruption and relevance.

Bundles shape expectations

Bundles (notably the Disney+/Hulu/ESPN+ package maintained through 2024) anchor perceived value, training buyers to expect multi-service discounts and pressuring Hulu to keep standalone prices competitive.

Buyers' bundle-driven churn dynamics force Hulu to balance standalone ARPU with retention; cross-promotions reduce churn but do not eliminate customer bargaining power.

- Bundle longevity: Disney+/Hulu/ESPN+ active strategy in 2024

- Buyer expectation: multi-service discounts standard

- Impact: bundle churn constrains Hulu standalone pricing

- Mitigation: cross-promo lowers but does not remove buyer power

Quality and UX demands

Hulu faces strong customer bargaining power as viewers expect near-zero buffering, widespread 4K support and robust discovery; by 2024 Hulu served roughly 50 million subscribers so UX failures directly threaten revenue. Poor recommendation relevance lowers perceived value and increases churn; profile and parental controls boost household stickiness. UX gaps prompt rapid switching, compressing ARPU and retention.

- Subscribers: ~50M (2024)

- 4K TV penetration: >50% (2024)

- Key levers: recommendations, profiles, parental controls

US streamer: ~50M subs, ~2.5%/mo churn, $7.99 ad tier

Hulu faces strong buyer power: ~50M US subscribers (2024), easy month-to-month churn (~2.5%/mo) and common multi-homing (US households ~3.8 subs) compress pricing. Ad-supported tier at $7.99/mo and heavy competitor scale (Netflix ~260M, Disney+ ~170M in 2024) amplify switch risk. Bundles (Disney+/Hulu/ESPN+) and UX demands (4K, recommendations) further tie perceived value to price and experience.

| Metric | 2024 Value |

|---|---|

| Subscribers | ~50M |

| Monthly churn | ~2.5% |

| Avg US streaming subs/household | ~3.8 |

| Hulu ad tier price | $7.99/mo |

| Netflix global subs | ~260M |

| Disney+ subs | ~170M |

What You See Is What You Get

Hulu LLC Porter's Five Forces Analysis

This Hulu LLC Porter's Five Forces Analysis is the exact document you'll receive immediately after purchase—no surprises, no placeholders. It presents the full competitive assessment, including threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and industry rivalry, fully formatted for download. You're previewing the final version; once bought, you’ll have instant access to this ready-to-use file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hulu LLC faces intense rivalry in streaming, strong supplier leverage for premium content, and growing substitute threats from ad-supported and global platforms, while buyer power and regulatory shifts shape pricing and growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Major studios hold leverage

Hulu depends on a handful of networks and studios for next-day TV and big franchises, concentrating bargaining power with suppliers and limiting Hulu's sourcing flexibility. Hit franchises and next-day windows command premium licensing terms, with per-episode fees for top scripted shows often exceeding $1,000,000. Exclusive or first-window deals raise content costs and lock Hulu into higher renewals, while studio consolidation (Disney, Warner Bros. Discovery, Paramount, NBCUniversal) tightens supplier leverage.

Live TV channel costs

Carriage fees for live channels and sports networks are high and rising, with industry reports showing sports-rights inflation running roughly 8–12% annually through 2024, forcing higher per-channel fees for distributors. Programmers can and do threaten blackouts to extract favorable rates, raising short-term bargaining leverage. That inflation cascades into higher content costs that compress margins on Hulu's live tiers and force either price increases or margin erosion.

Tech and distribution gatekeepers

CDNs (Akamai, Cloudflare) and cloud providers (AWS) drive streaming delivery costs and latency; the global CDN market was roughly $24B in 2024, squeezing margins on high-bitrate video. App stores (Apple/Google) still take 15–30% in 2024, and platform placement fees or preferred‑placement deals raise CAC and reduce ARPU. Device OEMs (smart TV and set‑top vendors) control home‑screen real estate, shaping discoverability and engagement. Negotiations over revenue share and placement materially affect user acquisition and retention economics.

Talent and unions power

Guild agreements and talent deals shape Hulu originals' timelines and costs: the 2023 WGA strike lasted 148 days and the SAG-AFTRA strike 118 days, halting new production and delaying releases. Star-driven projects can demand top-tier pay—some A-list leads exceed $1 million per episode—while backend participation and residuals raise long-run expenses. These supplier dynamics increase scheduling risk and margin pressure.

- 148-day WGA strike (2023)

- 118-day SAG-AFTRA strike (2023)

- A-list pay >$1M/episode

- Backend/residuals increase lifecycle cost

Sports and event rights

Premium live sports and event rights remain scarce and highly concentrated among a few leagues and broadcasters, exemplified by the NFL securing about $113 billion in media deals through 2033, highlighting supplier dominance.

Bidding wars push up minimum guarantees and multi-year lock-ins, raising Hulu's distribution costs and exit barriers.

Blackout rules and fragmented regional rights complicate packaging and reduce Hulu's ability to offer nationwide bundled products, amplifying supplier power.

- Sparsity; High guarantees; Lock-ins; Blackouts; Concentrated leverage

Streaming platforms squeezed by studio power, rising sports rights, CDN costs, store cuts, strikes

Hulu faces concentrated supplier power: major studios/networks (Disney, WBD, Paramount, NBCU) and league rights push high guarantees and lock-ins; top scripted per-episode fees often exceed $1,000,000 and sports-rights inflation ran ~8–12% annually through 2024. CDNs/clouds and app stores (global CDN ~$24B in 2024; app store take 15–30%) raise delivery and distribution costs. Guild strikes (WGA 148d, SAG-AFTRA 118d) and A-list pay (> $1M/ep) amplify scheduling and cost risk.

| Metric | 2024/Notable |

|---|---|

| Global CDN market | $24B (2024) |

| Sports-rights inflation | 8–12% pa (through 2024) |

| NFL media deals | $113B through 2033 |

| WGA / SAG-AFTRA | 148d / 118d (2023) |

| A-list pay | > $1M per episode |

What is included in the product

Tailored Porter’s Five Forces analysis for Hulu LLC uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and intensity of rivalry; identifies disruptive streaming trends and content/licensing dynamics shaping pricing and profitability to inform strategic decisions.

A concise one-sheet Porter's Five Forces for Hulu that visualizes competitive pressure via an editable spider chart—customize force levels, swap in your data, export clean slides without macros, and integrate into dashboards or reports for fast, board-ready decision-making.

Customers Bargaining Power

Low switching costs

Consumers can subscribe and cancel Hulu month-to-month with minimal friction, undermining long-term lock-in. Multi-homing is common—US households average about 3.8 streaming subscriptions—weakening Hulu’s pricing power. Churn spikes as content cycles end, with industry monthly churn near 2.5% in 2024. Easy re-entry and low ad-supported pricing (about 7.99 USD/month) keep shoppers highly price-sensitive.

Abundant alternatives

Abundant SVOD/AVOD alternatives—Netflix (~260 million global subs in 2024) and Disney+ (~170 million in 2024), plus Peacock, Paramount+ and ad-supported entrants—give Hulu users leverage. Significant content overlap across platforms reduces differentiation and raises churn risk. Consumers routinely compare price, catalog depth and UX before committing, and time-limited promotions or bundled discounts elsewhere frequently trigger switching.

Ad tolerance vs price

Ad-supported Hulu trades lower price ($7.99/month in 2024) for increased ad load (industry ~9 minutes/hour), and users react quickly to higher frequency, driving churn or upgrades; Disney's Hulu ecosystem (~49 million subscribers in 2024) makes small shifts impactful. Advertisers' targeting demands further shape ad density, so perceived value hinges on balancing cost savings against interruption and relevance.

Bundles shape expectations

Bundles (notably the Disney+/Hulu/ESPN+ package maintained through 2024) anchor perceived value, training buyers to expect multi-service discounts and pressuring Hulu to keep standalone prices competitive.

Buyers' bundle-driven churn dynamics force Hulu to balance standalone ARPU with retention; cross-promotions reduce churn but do not eliminate customer bargaining power.

- Bundle longevity: Disney+/Hulu/ESPN+ active strategy in 2024

- Buyer expectation: multi-service discounts standard

- Impact: bundle churn constrains Hulu standalone pricing

- Mitigation: cross-promo lowers but does not remove buyer power

Quality and UX demands

Hulu faces strong customer bargaining power as viewers expect near-zero buffering, widespread 4K support and robust discovery; by 2024 Hulu served roughly 50 million subscribers so UX failures directly threaten revenue. Poor recommendation relevance lowers perceived value and increases churn; profile and parental controls boost household stickiness. UX gaps prompt rapid switching, compressing ARPU and retention.

- Subscribers: ~50M (2024)

- 4K TV penetration: >50% (2024)

- Key levers: recommendations, profiles, parental controls

US streamer: ~50M subs, ~2.5%/mo churn, $7.99 ad tier

Hulu faces strong buyer power: ~50M US subscribers (2024), easy month-to-month churn (~2.5%/mo) and common multi-homing (US households ~3.8 subs) compress pricing. Ad-supported tier at $7.99/mo and heavy competitor scale (Netflix ~260M, Disney+ ~170M in 2024) amplify switch risk. Bundles (Disney+/Hulu/ESPN+) and UX demands (4K, recommendations) further tie perceived value to price and experience.

| Metric | 2024 Value |

|---|---|

| Subscribers | ~50M |

| Monthly churn | ~2.5% |

| Avg US streaming subs/household | ~3.8 |

| Hulu ad tier price | $7.99/mo |

| Netflix global subs | ~260M |

| Disney+ subs | ~170M |

What You See Is What You Get

Hulu LLC Porter's Five Forces Analysis

This Hulu LLC Porter's Five Forces Analysis is the exact document you'll receive immediately after purchase—no surprises, no placeholders. It presents the full competitive assessment, including threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and industry rivalry, fully formatted for download. You're previewing the final version; once bought, you’ll have instant access to this ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Hulu LLC faces intense rivalry in streaming, strong supplier leverage for premium content, and growing substitute threats from ad-supported and global platforms, while buyer power and regulatory shifts shape pricing and growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings and strategic implications.

Suppliers Bargaining Power

Major studios hold leverage

Hulu depends on a handful of networks and studios for next-day TV and big franchises, concentrating bargaining power with suppliers and limiting Hulu's sourcing flexibility. Hit franchises and next-day windows command premium licensing terms, with per-episode fees for top scripted shows often exceeding $1,000,000. Exclusive or first-window deals raise content costs and lock Hulu into higher renewals, while studio consolidation (Disney, Warner Bros. Discovery, Paramount, NBCUniversal) tightens supplier leverage.

Live TV channel costs

Carriage fees for live channels and sports networks are high and rising, with industry reports showing sports-rights inflation running roughly 8–12% annually through 2024, forcing higher per-channel fees for distributors. Programmers can and do threaten blackouts to extract favorable rates, raising short-term bargaining leverage. That inflation cascades into higher content costs that compress margins on Hulu's live tiers and force either price increases or margin erosion.

Tech and distribution gatekeepers

CDNs (Akamai, Cloudflare) and cloud providers (AWS) drive streaming delivery costs and latency; the global CDN market was roughly $24B in 2024, squeezing margins on high-bitrate video. App stores (Apple/Google) still take 15–30% in 2024, and platform placement fees or preferred‑placement deals raise CAC and reduce ARPU. Device OEMs (smart TV and set‑top vendors) control home‑screen real estate, shaping discoverability and engagement. Negotiations over revenue share and placement materially affect user acquisition and retention economics.

Talent and unions power

Guild agreements and talent deals shape Hulu originals' timelines and costs: the 2023 WGA strike lasted 148 days and the SAG-AFTRA strike 118 days, halting new production and delaying releases. Star-driven projects can demand top-tier pay—some A-list leads exceed $1 million per episode—while backend participation and residuals raise long-run expenses. These supplier dynamics increase scheduling risk and margin pressure.

- 148-day WGA strike (2023)

- 118-day SAG-AFTRA strike (2023)

- A-list pay >$1M/episode

- Backend/residuals increase lifecycle cost

Sports and event rights

Premium live sports and event rights remain scarce and highly concentrated among a few leagues and broadcasters, exemplified by the NFL securing about $113 billion in media deals through 2033, highlighting supplier dominance.

Bidding wars push up minimum guarantees and multi-year lock-ins, raising Hulu's distribution costs and exit barriers.

Blackout rules and fragmented regional rights complicate packaging and reduce Hulu's ability to offer nationwide bundled products, amplifying supplier power.

- Sparsity; High guarantees; Lock-ins; Blackouts; Concentrated leverage

Streaming platforms squeezed by studio power, rising sports rights, CDN costs, store cuts, strikes

Hulu faces concentrated supplier power: major studios/networks (Disney, WBD, Paramount, NBCU) and league rights push high guarantees and lock-ins; top scripted per-episode fees often exceed $1,000,000 and sports-rights inflation ran ~8–12% annually through 2024. CDNs/clouds and app stores (global CDN ~$24B in 2024; app store take 15–30%) raise delivery and distribution costs. Guild strikes (WGA 148d, SAG-AFTRA 118d) and A-list pay (> $1M/ep) amplify scheduling and cost risk.

| Metric | 2024/Notable |

|---|---|

| Global CDN market | $24B (2024) |

| Sports-rights inflation | 8–12% pa (through 2024) |

| NFL media deals | $113B through 2033 |

| WGA / SAG-AFTRA | 148d / 118d (2023) |

| A-list pay | > $1M per episode |

What is included in the product

Tailored Porter’s Five Forces analysis for Hulu LLC uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and intensity of rivalry; identifies disruptive streaming trends and content/licensing dynamics shaping pricing and profitability to inform strategic decisions.

A concise one-sheet Porter's Five Forces for Hulu that visualizes competitive pressure via an editable spider chart—customize force levels, swap in your data, export clean slides without macros, and integrate into dashboards or reports for fast, board-ready decision-making.

Customers Bargaining Power

Low switching costs

Consumers can subscribe and cancel Hulu month-to-month with minimal friction, undermining long-term lock-in. Multi-homing is common—US households average about 3.8 streaming subscriptions—weakening Hulu’s pricing power. Churn spikes as content cycles end, with industry monthly churn near 2.5% in 2024. Easy re-entry and low ad-supported pricing (about 7.99 USD/month) keep shoppers highly price-sensitive.

Abundant alternatives

Abundant SVOD/AVOD alternatives—Netflix (~260 million global subs in 2024) and Disney+ (~170 million in 2024), plus Peacock, Paramount+ and ad-supported entrants—give Hulu users leverage. Significant content overlap across platforms reduces differentiation and raises churn risk. Consumers routinely compare price, catalog depth and UX before committing, and time-limited promotions or bundled discounts elsewhere frequently trigger switching.

Ad tolerance vs price

Ad-supported Hulu trades lower price ($7.99/month in 2024) for increased ad load (industry ~9 minutes/hour), and users react quickly to higher frequency, driving churn or upgrades; Disney's Hulu ecosystem (~49 million subscribers in 2024) makes small shifts impactful. Advertisers' targeting demands further shape ad density, so perceived value hinges on balancing cost savings against interruption and relevance.

Bundles shape expectations

Bundles (notably the Disney+/Hulu/ESPN+ package maintained through 2024) anchor perceived value, training buyers to expect multi-service discounts and pressuring Hulu to keep standalone prices competitive.

Buyers' bundle-driven churn dynamics force Hulu to balance standalone ARPU with retention; cross-promotions reduce churn but do not eliminate customer bargaining power.

- Bundle longevity: Disney+/Hulu/ESPN+ active strategy in 2024

- Buyer expectation: multi-service discounts standard

- Impact: bundle churn constrains Hulu standalone pricing

- Mitigation: cross-promo lowers but does not remove buyer power

Quality and UX demands

Hulu faces strong customer bargaining power as viewers expect near-zero buffering, widespread 4K support and robust discovery; by 2024 Hulu served roughly 50 million subscribers so UX failures directly threaten revenue. Poor recommendation relevance lowers perceived value and increases churn; profile and parental controls boost household stickiness. UX gaps prompt rapid switching, compressing ARPU and retention.

- Subscribers: ~50M (2024)

- 4K TV penetration: >50% (2024)

- Key levers: recommendations, profiles, parental controls

US streamer: ~50M subs, ~2.5%/mo churn, $7.99 ad tier

Hulu faces strong buyer power: ~50M US subscribers (2024), easy month-to-month churn (~2.5%/mo) and common multi-homing (US households ~3.8 subs) compress pricing. Ad-supported tier at $7.99/mo and heavy competitor scale (Netflix ~260M, Disney+ ~170M in 2024) amplify switch risk. Bundles (Disney+/Hulu/ESPN+) and UX demands (4K, recommendations) further tie perceived value to price and experience.

| Metric | 2024 Value |

|---|---|

| Subscribers | ~50M |

| Monthly churn | ~2.5% |

| Avg US streaming subs/household | ~3.8 |

| Hulu ad tier price | $7.99/mo |

| Netflix global subs | ~260M |

| Disney+ subs | ~170M |

What You See Is What You Get

Hulu LLC Porter's Five Forces Analysis

This Hulu LLC Porter's Five Forces Analysis is the exact document you'll receive immediately after purchase—no surprises, no placeholders. It presents the full competitive assessment, including threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and industry rivalry, fully formatted for download. You're previewing the final version; once bought, you’ll have instant access to this ready-to-use file.