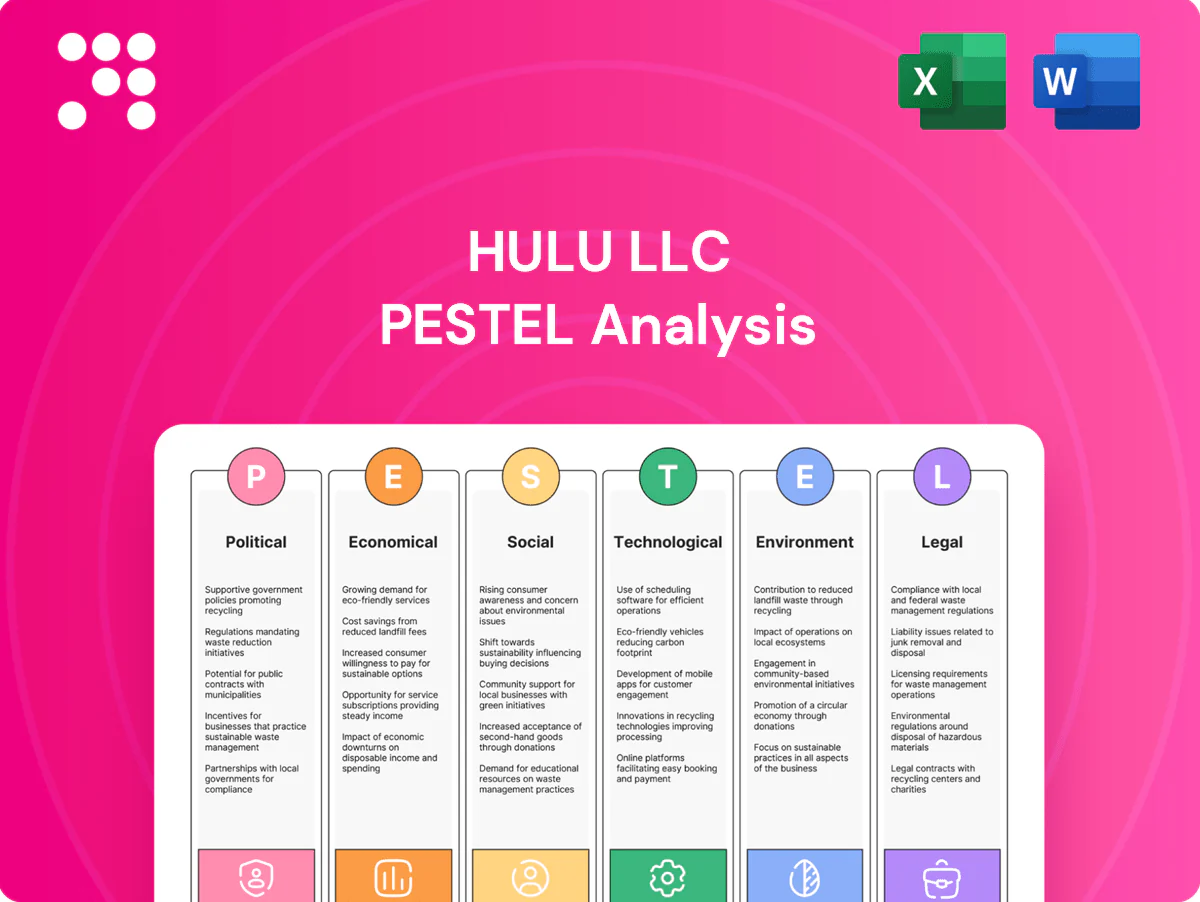

Hulu LLC PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic trends, social behaviors, technological innovation, environmental concerns, and legal pressures are reshaping Hulu LLC’s strategic landscape. This concise PESTLE highlights key risks and growth levers. Purchase the full analysis to get actionable, board-ready insights and instantly downloadable models.

Political factors

Regulatory oversight of media consolidation

Heightened antitrust scrutiny affects Hulu’s ownership and bundling choices, given Disney owns roughly 67% and Comcast 33% of Hulu. Regulators are focused on mergers and vertical integration in streaming as firms with combined scale—Hulu’s ~48 million US subscribers (2023/24)—can influence market power and consumer choice. Approval conditions often carry divestitures or behavioral remedies that shape distribution and pricing, and shifting policy could speed up or slow consolidation pathways.

Net neutrality and broadband policy

Rules on throttling and paid prioritization directly affect Hulu’s streaming QoS and carriage costs; the 2015 Open Internet Order and its 2018 repeal show regulatory reversals that reshape ISP negotiations. Reinstatement or rollback alters CDN spend and peering strategies, and with no federal net neutrality statute as of July 2025 states like California (2018) create a patchwork of obligations. Policy stability improves long-term QoS planning and subscriber retention.

Trade policy and cross-border content

Tariffs, sanctions and cultural quotas shape Hulu’s licensing and co‑production scope: the EU’s AVMSD requires platforms to ensure at least 30% European works, while Western sanctions since 2022 have restricted distribution in Russia and parts of Eastern Europe. Currency and remittance controls in markets like China constrain international rights payments, and government incentives (tax credits up to ~35% in Canada/provincial programs) encourage localized production strategies.

Broadcast and carriage politics for Live TV

Retransmission consent disputes, governed by FCC frameworks, regularly trigger blackouts that raise carriage costs for platforms like Hulu + Live TV, which reported about 4.4 million live-TV subscribers in Disney disclosures through 2024; policy debates over sports rights and local-news funding further pressure licensing fees and margins, especially during high-viewership events.

- Retransmission disputes: FCC-regulated, cause blackouts

- Hulu + Live TV: ~4.4M subscribers (2024)

- Sports/news rights: increase carriage costs

- Election cycles: amplify scrutiny on media access

Digital tax regimes and platform accountability

Governments are expanding digital service taxes in over 40 jurisdictions, which may raise Hulu's operating costs and compress ad margins; concurrently political drives for platform accountability increase obligations for content moderation and ad transparency, with the EU Digital Services Act exposing firms to fines up to 6% of global turnover and GDPR up to 4%.

- DSTs: >40 jurisdictions

- DSA fines: up to 6% global turnover

- GDPR fines: up to 4% global revenue

- Lobbying/coalitions can reduce regulatory risk

Ownership split 67%/33% reshapes US streaming; ~48M subs, Live TV 4.4M; regs raise fines 6%/4%

Antitrust scrutiny (Disney ~67%/Comcast ~33%) shapes Hulu’s ownership, bundling and consolidation options; US subscribers ~48M (2023/24) increase regulator focus. Net neutrality patchwork (no federal law, CA rules) affects CDN costs; Hulu + Live TV ~4.4M (2024) faces retransmission disputes. DSA/GDPR fines (6%/4%) and DSTs in >40 jurisdictions raise compliance and tax burdens.

| Metric | Value |

|---|---|

| Ownership | Disney 67% / Comcast 33% |

| US subs | ~48M (2023/24) |

| Live TV subs | ~4.4M (2024) |

| DSA fine | Up to 6% global turnover |

| GDPR fine | Up to 4% global revenue |

| DSTs | >40 jurisdictions |

What is included in the product

Analyzes how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Hulu LLC, with data-backed trends and region-specific regulatory context. Designed for executives and investors, the report maps threats and opportunities, offers forward-looking insights for scenario planning, and is formatted for direct use in business plans or pitch decks.

A clean, summarized Hulu LLC PESTLE analysis that’s visually segmented by PESTEL categories for quick interpretation, easily dropped into presentations or shared across teams to streamline strategic planning and align stakeholders.

Economic factors

Subscription saturation and ARPU pressure

Household streaming budgets are constrained—US households spent about $48/month on streaming in 2023—intensifying competition for wallet share against Hulu’s ~48M subscribers (2024). Price hikes (Hulu ad-supported $7.99, no-ads $17.99 in 2024) risk churn unless offset by perceived value and bundles. Ad-supported tiers and ad revenue can stabilize ARPU via hybrid monetization. Macro downturns amplify price sensitivity and downgrades.

Advertising market cyclicality

Ad spend closely tracks GDP and rate cycles—US ad budgets tightened during 2023’s slowdown and rebounded with ~2.4% GDP growth in 2024—while rising rates compressed short‑term spend. Connected TV ad revenue grew roughly 20% YoY in 2023, but scatter markets and shifting performance budgets make delivery volatile. Improved targeting and measurement drive higher yield in recoveries, and sector mix shifts (auto, retail, entertainment) cause notable quarterly swings.

Content cost inflation

Rising talent, sports and production costs—exacerbated by disruptions like the 118-day SAG-AFTRA strike in 2023—are pressuring Hulu's margins. Longer payback cycles require disciplined greenlighting and licensing to protect cash flow. Data-driven commissioning and analytics can improve hit rates and reduce waste. Co-productions and strategic windowing optimize ROI across linear, SVOD and AVOD windows.

Bundling and ecosystem synergies

Bundling with sister services (Disney+ and ESPN+) drives higher retention and lowers CAC by sharing marketing and content costs; Disney reported the bundle as a core contributor to streaming growth in 2024, supporting Hulu’s scale. Cross-promotion cuts marketing spend and raises LTV via multi-service engagement. Partner billing with telcos/device makers expands distribution but requires revenue shares that compress ARPU. Pricing architecture must avoid cannibalization while pursuing subscriber scale.

- Hulu (part of Disney bundle) — bundle-driven retention

- Cross-promo — lower CAC, higher LTV

- Partner billing — wider reach, shared economics

- Pricing trade-off — scale vs cannibalization

Exchange rates and international rights

FX swings affect Hulu's imported content costs and outbound licensing revenues; the US dollar peaked at a DXY of 114.78 in Sept 2022 and was near 103 in mid‑2024, illustrating recent volatility. Dollar strength can lower foreign production expenses while shrinking the dollar value of overseas sales. Industry hedging, multi‑currency contracts and geographically diversified rights portfolios reduce earnings volatility.

- FX volatility: DXY 114.78 (Sep 2022) → ~103 (mid‑2024)

- Impact: cheaper foreign production vs lower overseas sales receipts

- Mitigation: hedging and multi‑currency contracts

- Resilience: geographic diversification of rights

Ownership split 67%/33% reshapes US streaming; ~48M subs, Live TV 4.4M; regs raise fines 6%/4%

Household streaming spend (~$48/month in 2023) pressures Hulu’s ~48M subs (2024); pricing (ad $7.99, no‑ads $17.99 in 2024) risks churn without bundle/value. Ad revenue (CTV +20% YoY in 2023) and ~2.4% GDP growth (2024) support ad recovery; talent/production inflation and FX (DXY ~103 mid‑2024) compress margins.

| Metric | Value |

|---|---|

| Household spend | $48/mo (2023) |

| Hulu subs | ~48M (2024) |

| Prices | $7.99/$17.99 (2024) |

Preview the Actual Deliverable

Hulu LLC PESTLE Analysis

The Hulu LLC PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same structured political, economic, social, technological, legal, and environmental insights as the final file. No placeholders or surprises—download the finished report immediately after checkout.

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic trends, social behaviors, technological innovation, environmental concerns, and legal pressures are reshaping Hulu LLC’s strategic landscape. This concise PESTLE highlights key risks and growth levers. Purchase the full analysis to get actionable, board-ready insights and instantly downloadable models.

Political factors

Regulatory oversight of media consolidation

Heightened antitrust scrutiny affects Hulu’s ownership and bundling choices, given Disney owns roughly 67% and Comcast 33% of Hulu. Regulators are focused on mergers and vertical integration in streaming as firms with combined scale—Hulu’s ~48 million US subscribers (2023/24)—can influence market power and consumer choice. Approval conditions often carry divestitures or behavioral remedies that shape distribution and pricing, and shifting policy could speed up or slow consolidation pathways.

Net neutrality and broadband policy

Rules on throttling and paid prioritization directly affect Hulu’s streaming QoS and carriage costs; the 2015 Open Internet Order and its 2018 repeal show regulatory reversals that reshape ISP negotiations. Reinstatement or rollback alters CDN spend and peering strategies, and with no federal net neutrality statute as of July 2025 states like California (2018) create a patchwork of obligations. Policy stability improves long-term QoS planning and subscriber retention.

Trade policy and cross-border content

Tariffs, sanctions and cultural quotas shape Hulu’s licensing and co‑production scope: the EU’s AVMSD requires platforms to ensure at least 30% European works, while Western sanctions since 2022 have restricted distribution in Russia and parts of Eastern Europe. Currency and remittance controls in markets like China constrain international rights payments, and government incentives (tax credits up to ~35% in Canada/provincial programs) encourage localized production strategies.

Broadcast and carriage politics for Live TV

Retransmission consent disputes, governed by FCC frameworks, regularly trigger blackouts that raise carriage costs for platforms like Hulu + Live TV, which reported about 4.4 million live-TV subscribers in Disney disclosures through 2024; policy debates over sports rights and local-news funding further pressure licensing fees and margins, especially during high-viewership events.

- Retransmission disputes: FCC-regulated, cause blackouts

- Hulu + Live TV: ~4.4M subscribers (2024)

- Sports/news rights: increase carriage costs

- Election cycles: amplify scrutiny on media access

Digital tax regimes and platform accountability

Governments are expanding digital service taxes in over 40 jurisdictions, which may raise Hulu's operating costs and compress ad margins; concurrently political drives for platform accountability increase obligations for content moderation and ad transparency, with the EU Digital Services Act exposing firms to fines up to 6% of global turnover and GDPR up to 4%.

- DSTs: >40 jurisdictions

- DSA fines: up to 6% global turnover

- GDPR fines: up to 4% global revenue

- Lobbying/coalitions can reduce regulatory risk

Ownership split 67%/33% reshapes US streaming; ~48M subs, Live TV 4.4M; regs raise fines 6%/4%

Antitrust scrutiny (Disney ~67%/Comcast ~33%) shapes Hulu’s ownership, bundling and consolidation options; US subscribers ~48M (2023/24) increase regulator focus. Net neutrality patchwork (no federal law, CA rules) affects CDN costs; Hulu + Live TV ~4.4M (2024) faces retransmission disputes. DSA/GDPR fines (6%/4%) and DSTs in >40 jurisdictions raise compliance and tax burdens.

| Metric | Value |

|---|---|

| Ownership | Disney 67% / Comcast 33% |

| US subs | ~48M (2023/24) |

| Live TV subs | ~4.4M (2024) |

| DSA fine | Up to 6% global turnover |

| GDPR fine | Up to 4% global revenue |

| DSTs | >40 jurisdictions |

What is included in the product

Analyzes how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Hulu LLC, with data-backed trends and region-specific regulatory context. Designed for executives and investors, the report maps threats and opportunities, offers forward-looking insights for scenario planning, and is formatted for direct use in business plans or pitch decks.

A clean, summarized Hulu LLC PESTLE analysis that’s visually segmented by PESTEL categories for quick interpretation, easily dropped into presentations or shared across teams to streamline strategic planning and align stakeholders.

Economic factors

Subscription saturation and ARPU pressure

Household streaming budgets are constrained—US households spent about $48/month on streaming in 2023—intensifying competition for wallet share against Hulu’s ~48M subscribers (2024). Price hikes (Hulu ad-supported $7.99, no-ads $17.99 in 2024) risk churn unless offset by perceived value and bundles. Ad-supported tiers and ad revenue can stabilize ARPU via hybrid monetization. Macro downturns amplify price sensitivity and downgrades.

Advertising market cyclicality

Ad spend closely tracks GDP and rate cycles—US ad budgets tightened during 2023’s slowdown and rebounded with ~2.4% GDP growth in 2024—while rising rates compressed short‑term spend. Connected TV ad revenue grew roughly 20% YoY in 2023, but scatter markets and shifting performance budgets make delivery volatile. Improved targeting and measurement drive higher yield in recoveries, and sector mix shifts (auto, retail, entertainment) cause notable quarterly swings.

Content cost inflation

Rising talent, sports and production costs—exacerbated by disruptions like the 118-day SAG-AFTRA strike in 2023—are pressuring Hulu's margins. Longer payback cycles require disciplined greenlighting and licensing to protect cash flow. Data-driven commissioning and analytics can improve hit rates and reduce waste. Co-productions and strategic windowing optimize ROI across linear, SVOD and AVOD windows.

Bundling and ecosystem synergies

Bundling with sister services (Disney+ and ESPN+) drives higher retention and lowers CAC by sharing marketing and content costs; Disney reported the bundle as a core contributor to streaming growth in 2024, supporting Hulu’s scale. Cross-promotion cuts marketing spend and raises LTV via multi-service engagement. Partner billing with telcos/device makers expands distribution but requires revenue shares that compress ARPU. Pricing architecture must avoid cannibalization while pursuing subscriber scale.

- Hulu (part of Disney bundle) — bundle-driven retention

- Cross-promo — lower CAC, higher LTV

- Partner billing — wider reach, shared economics

- Pricing trade-off — scale vs cannibalization

Exchange rates and international rights

FX swings affect Hulu's imported content costs and outbound licensing revenues; the US dollar peaked at a DXY of 114.78 in Sept 2022 and was near 103 in mid‑2024, illustrating recent volatility. Dollar strength can lower foreign production expenses while shrinking the dollar value of overseas sales. Industry hedging, multi‑currency contracts and geographically diversified rights portfolios reduce earnings volatility.

- FX volatility: DXY 114.78 (Sep 2022) → ~103 (mid‑2024)

- Impact: cheaper foreign production vs lower overseas sales receipts

- Mitigation: hedging and multi‑currency contracts

- Resilience: geographic diversification of rights

Ownership split 67%/33% reshapes US streaming; ~48M subs, Live TV 4.4M; regs raise fines 6%/4%

Household streaming spend (~$48/month in 2023) pressures Hulu’s ~48M subs (2024); pricing (ad $7.99, no‑ads $17.99 in 2024) risks churn without bundle/value. Ad revenue (CTV +20% YoY in 2023) and ~2.4% GDP growth (2024) support ad recovery; talent/production inflation and FX (DXY ~103 mid‑2024) compress margins.

| Metric | Value |

|---|---|

| Household spend | $48/mo (2023) |

| Hulu subs | ~48M (2024) |

| Prices | $7.99/$17.99 (2024) |

Preview the Actual Deliverable

Hulu LLC PESTLE Analysis

The Hulu LLC PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same structured political, economic, social, technological, legal, and environmental insights as the final file. No placeholders or surprises—download the finished report immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock how political shifts, economic trends, social behaviors, technological innovation, environmental concerns, and legal pressures are reshaping Hulu LLC’s strategic landscape. This concise PESTLE highlights key risks and growth levers. Purchase the full analysis to get actionable, board-ready insights and instantly downloadable models.

Political factors

Regulatory oversight of media consolidation

Heightened antitrust scrutiny affects Hulu’s ownership and bundling choices, given Disney owns roughly 67% and Comcast 33% of Hulu. Regulators are focused on mergers and vertical integration in streaming as firms with combined scale—Hulu’s ~48 million US subscribers (2023/24)—can influence market power and consumer choice. Approval conditions often carry divestitures or behavioral remedies that shape distribution and pricing, and shifting policy could speed up or slow consolidation pathways.

Net neutrality and broadband policy

Rules on throttling and paid prioritization directly affect Hulu’s streaming QoS and carriage costs; the 2015 Open Internet Order and its 2018 repeal show regulatory reversals that reshape ISP negotiations. Reinstatement or rollback alters CDN spend and peering strategies, and with no federal net neutrality statute as of July 2025 states like California (2018) create a patchwork of obligations. Policy stability improves long-term QoS planning and subscriber retention.

Trade policy and cross-border content

Tariffs, sanctions and cultural quotas shape Hulu’s licensing and co‑production scope: the EU’s AVMSD requires platforms to ensure at least 30% European works, while Western sanctions since 2022 have restricted distribution in Russia and parts of Eastern Europe. Currency and remittance controls in markets like China constrain international rights payments, and government incentives (tax credits up to ~35% in Canada/provincial programs) encourage localized production strategies.

Broadcast and carriage politics for Live TV

Retransmission consent disputes, governed by FCC frameworks, regularly trigger blackouts that raise carriage costs for platforms like Hulu + Live TV, which reported about 4.4 million live-TV subscribers in Disney disclosures through 2024; policy debates over sports rights and local-news funding further pressure licensing fees and margins, especially during high-viewership events.

- Retransmission disputes: FCC-regulated, cause blackouts

- Hulu + Live TV: ~4.4M subscribers (2024)

- Sports/news rights: increase carriage costs

- Election cycles: amplify scrutiny on media access

Digital tax regimes and platform accountability

Governments are expanding digital service taxes in over 40 jurisdictions, which may raise Hulu's operating costs and compress ad margins; concurrently political drives for platform accountability increase obligations for content moderation and ad transparency, with the EU Digital Services Act exposing firms to fines up to 6% of global turnover and GDPR up to 4%.

- DSTs: >40 jurisdictions

- DSA fines: up to 6% global turnover

- GDPR fines: up to 4% global revenue

- Lobbying/coalitions can reduce regulatory risk

Ownership split 67%/33% reshapes US streaming; ~48M subs, Live TV 4.4M; regs raise fines 6%/4%

Antitrust scrutiny (Disney ~67%/Comcast ~33%) shapes Hulu’s ownership, bundling and consolidation options; US subscribers ~48M (2023/24) increase regulator focus. Net neutrality patchwork (no federal law, CA rules) affects CDN costs; Hulu + Live TV ~4.4M (2024) faces retransmission disputes. DSA/GDPR fines (6%/4%) and DSTs in >40 jurisdictions raise compliance and tax burdens.

| Metric | Value |

|---|---|

| Ownership | Disney 67% / Comcast 33% |

| US subs | ~48M (2023/24) |

| Live TV subs | ~4.4M (2024) |

| DSA fine | Up to 6% global turnover |

| GDPR fine | Up to 4% global revenue |

| DSTs | >40 jurisdictions |

What is included in the product

Analyzes how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—uniquely impact Hulu LLC, with data-backed trends and region-specific regulatory context. Designed for executives and investors, the report maps threats and opportunities, offers forward-looking insights for scenario planning, and is formatted for direct use in business plans or pitch decks.

A clean, summarized Hulu LLC PESTLE analysis that’s visually segmented by PESTEL categories for quick interpretation, easily dropped into presentations or shared across teams to streamline strategic planning and align stakeholders.

Economic factors

Subscription saturation and ARPU pressure

Household streaming budgets are constrained—US households spent about $48/month on streaming in 2023—intensifying competition for wallet share against Hulu’s ~48M subscribers (2024). Price hikes (Hulu ad-supported $7.99, no-ads $17.99 in 2024) risk churn unless offset by perceived value and bundles. Ad-supported tiers and ad revenue can stabilize ARPU via hybrid monetization. Macro downturns amplify price sensitivity and downgrades.

Advertising market cyclicality

Ad spend closely tracks GDP and rate cycles—US ad budgets tightened during 2023’s slowdown and rebounded with ~2.4% GDP growth in 2024—while rising rates compressed short‑term spend. Connected TV ad revenue grew roughly 20% YoY in 2023, but scatter markets and shifting performance budgets make delivery volatile. Improved targeting and measurement drive higher yield in recoveries, and sector mix shifts (auto, retail, entertainment) cause notable quarterly swings.

Content cost inflation

Rising talent, sports and production costs—exacerbated by disruptions like the 118-day SAG-AFTRA strike in 2023—are pressuring Hulu's margins. Longer payback cycles require disciplined greenlighting and licensing to protect cash flow. Data-driven commissioning and analytics can improve hit rates and reduce waste. Co-productions and strategic windowing optimize ROI across linear, SVOD and AVOD windows.

Bundling and ecosystem synergies

Bundling with sister services (Disney+ and ESPN+) drives higher retention and lowers CAC by sharing marketing and content costs; Disney reported the bundle as a core contributor to streaming growth in 2024, supporting Hulu’s scale. Cross-promotion cuts marketing spend and raises LTV via multi-service engagement. Partner billing with telcos/device makers expands distribution but requires revenue shares that compress ARPU. Pricing architecture must avoid cannibalization while pursuing subscriber scale.

- Hulu (part of Disney bundle) — bundle-driven retention

- Cross-promo — lower CAC, higher LTV

- Partner billing — wider reach, shared economics

- Pricing trade-off — scale vs cannibalization

Exchange rates and international rights

FX swings affect Hulu's imported content costs and outbound licensing revenues; the US dollar peaked at a DXY of 114.78 in Sept 2022 and was near 103 in mid‑2024, illustrating recent volatility. Dollar strength can lower foreign production expenses while shrinking the dollar value of overseas sales. Industry hedging, multi‑currency contracts and geographically diversified rights portfolios reduce earnings volatility.

- FX volatility: DXY 114.78 (Sep 2022) → ~103 (mid‑2024)

- Impact: cheaper foreign production vs lower overseas sales receipts

- Mitigation: hedging and multi‑currency contracts

- Resilience: geographic diversification of rights

Ownership split 67%/33% reshapes US streaming; ~48M subs, Live TV 4.4M; regs raise fines 6%/4%

Household streaming spend (~$48/month in 2023) pressures Hulu’s ~48M subs (2024); pricing (ad $7.99, no‑ads $17.99 in 2024) risks churn without bundle/value. Ad revenue (CTV +20% YoY in 2023) and ~2.4% GDP growth (2024) support ad recovery; talent/production inflation and FX (DXY ~103 mid‑2024) compress margins.

| Metric | Value |

|---|---|

| Household spend | $48/mo (2023) |

| Hulu subs | ~48M (2024) |

| Prices | $7.99/$17.99 (2024) |

Preview the Actual Deliverable

Hulu LLC PESTLE Analysis

The Hulu LLC PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It contains the same structured political, economic, social, technological, legal, and environmental insights as the final file. No placeholders or surprises—download the finished report immediately after checkout.