Humana SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Our Humana SWOT analysis distills the insurer’s competitive strengths, regulatory and reimbursement risks, and growth opportunities in Medicare Advantage and value-based care. It highlights strategic implications for investors and partners, with data-driven takeaways. Purchase the full report for the editable, investor-ready SWOT and actionable recommendations.

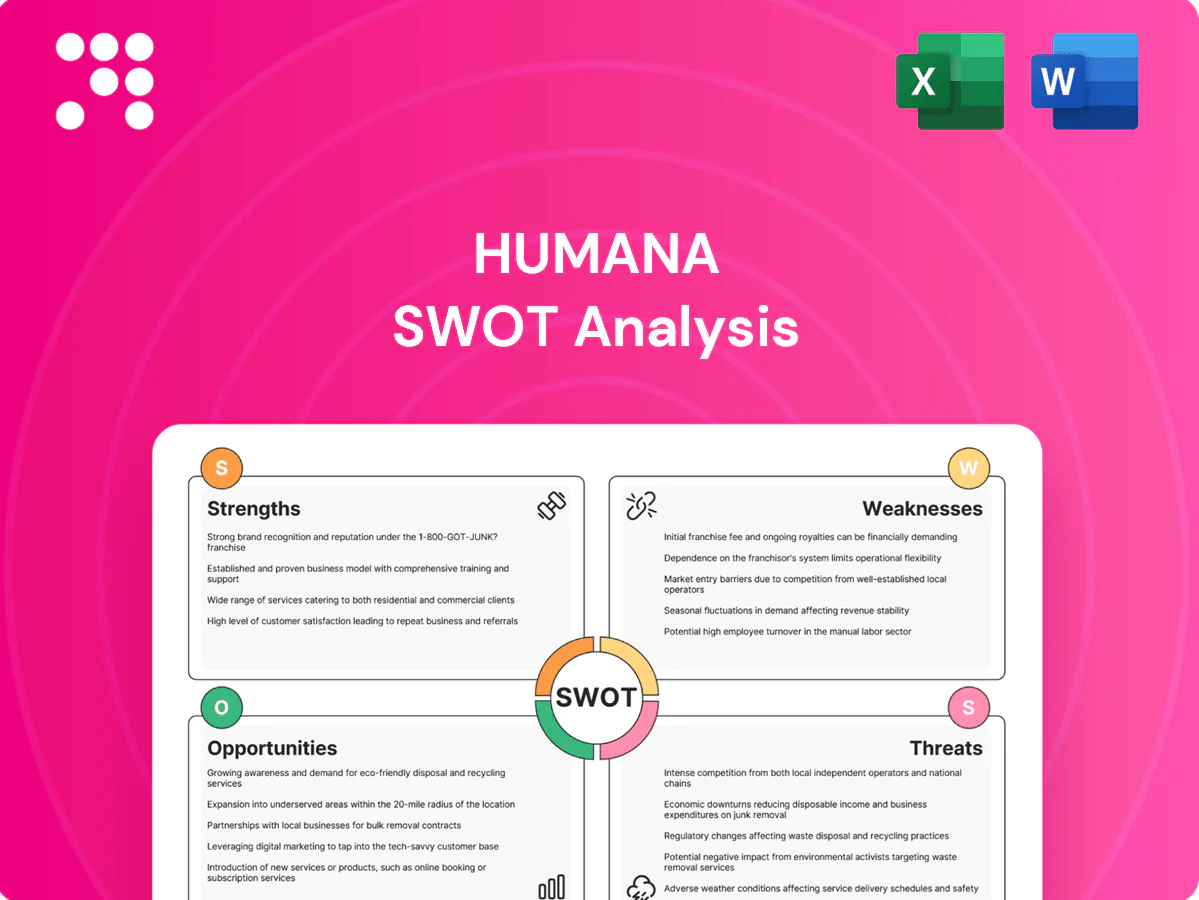

Strengths

Medicare Advantage market leadership

Humana holds a top-tier Medicare Advantage position with over 5 million MA enrollees in 2024, offering deep plan breadth across markets. Scale drives pricing leverage, richer supplemental benefits and tighter medical-cost management. Strong brand recognition among seniors aids retention and cross-sell into Part D and ancillary products. Market leadership builds a data flywheel that enhances risk scoring and targeted care management.

Integrated care and home-based delivery

Humana combines insurance with CenterWell primary care, home health and pharmacy services, serving about 6.3 million Medicare Advantage members and operating 600+ CenterWell locations as of 2024; these integrated clinical assets enable coordinated, value-based care with lower hospitalizations and contributed to a medical loss ratio near 85% in 2024, supporting sustainable margins and improved member outcomes.

Advanced analytics and risk management

Humana leverages extensive claims and clinical data to stratify risk and precisely target interventions, enabling earlier care coordination and chronic disease management. Predictive models drive utilization management and medication adherence programs, improving clinical outcomes and lowering avoidable utilization. Analytics boost STARS performance and reimbursement optimization while data-driven operations sustain continuous cost trend control.

Diverse product portfolio

Humana’s diverse product portfolio covers medical, dental, vision and supplemental benefits across individual, group and government lines, with 2024 revenue of about $86.7 billion and ~7.0 million Medicare Advantage members, spreading revenue risk and expanding addressable markets. Integrated pharmacy and specialty services deepen member relationships and drive retention, while multi-channel distribution (brokers, direct, Medicare channels) supports growth resilience.

Strong provider partnerships and value-based contracts

Humana's deep relationships with physician groups and MSOs tied to value outcomes—covering about 7.4 million Medicare Advantage and related members in 2024—drive shared-savings and capitated arrangements that improve cost predictability and margin stability. Clinical alignment enhances quality metrics and member satisfaction, and the network strategy supports scalable, repeatable operating performance.

- Value-based reach: ~7.4M MA/related members (2024)

- Payment models: shared savings and capitation improve predictability

- Outcomes: clinical alignment raises quality scores and satisfaction

- Scalability: network strategy enables repeatable operating performance

Leading Medicare Advantage: ~7.0M members, $86.7B revenue, integrated care & value-based reach

Humana holds a leading Medicare Advantage position with ~7.0M MA members (2024) and $86.7B revenue (2024), enabling pricing leverage and rich benefits. Integrated CenterWell primary care (600+ locations) plus pharmacy and home health support coordinated, value-based care and lower utilization. Value-based reach ~7.4M members and MLR near 85% in 2024 enhance cost predictability and outcomes.

| Metric | 2024 |

|---|---|

| Revenue | $86.7B |

| Medicare Advantage members | ~7.0M |

| Value-based reach | ~7.4M |

| CenterWell locations | 600+ |

| Medical Loss Ratio | ~85% |

What is included in the product

Delivers a strategic overview of Humana’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and risks shaping the future of its healthcare and insurance operations.

Provides a concise Humana SWOT matrix that highlights key strengths, weaknesses, opportunities, and threats to quickly relieve strategic decision-making pain points in healthcare operations and member services.

Weaknesses

High dependence on Medicare Advantage

Humana derives roughly 75% of 2024 consolidated revenue from Medicare Advantage and served about 5.8 million MA members in 2024, concentrating revenue and earnings in MA and increasing exposure to CMS policy and rate changes. Portfolio concentration raises volatility when benchmark rates or risk-adjustment factors shift, and Humana's commercial and Medicaid footprints remain comparatively limited. That dependency can constrain growth if MA dynamics weaken.

Exposure to medical cost trend volatility

Utilization spikes, notably inpatient and outpatient, can compress margins as post-pandemic normalization remains uneven across cohorts, with Medicare Advantage utilization still above 2019 baselines in some segments. Pharmacy and specialty drug inflation (around 9% industrywide in 2024) has pushed MLR higher. Pricing cycles often lag cost trends, creating near-term earnings risk if cost inflation persists. Humana faces pressure to rebalance rates versus accelerating medical costs.

Operational complexity from integrated model

Owning clinical assets—primary care, home health, pharmacies and care-delivery centers—raises fixed costs and execution risk as Humana balances facility investments with enrollment-driven revenue. Coordinating payor functions with primary care, home health and pharmacy needs tight governance and interoperable systems to avoid care fragmentation. Integration missteps can erode quality and member experience, while capital intensity limits flexibility in economic downturns.

Geographic concentration risks

Humana’s enrollment is concentrated in select states and in Medicare Advantage, making local regulatory shifts and regional competition able to disproportionately affect financial results and membership trends.

Disruptions to provider networks in key markets can cause outsized cost and access issues, while market-specific reputational problems have hindered growth in affected regions.

- Geographic enrollment concentration

- Medicare Advantage dependency

- Provider-network vulnerability

- Local reputational risk

Regulatory and ratings sensitivity

Regulatory and ratings sensitivity: CMS Star Ratings (scale 1–5) directly drive quality bonus payments and beneficiary choice, so volatility of even half-star shifts can materially reduce bonus revenue and plan appeal; compliance missteps risk sanctions, fines or enrollment freezes, and prior-year coding/documentation audits can trigger retroactive clawbacks; dependence on CMS approvals creates timing uncertainty for product launches and rate changes.

- Star Ratings scale 1–5 affect bonuses and enrollment

- Compliance failures → sanctions, fines, enrollment freezes

- Prior-year coding audits can cause clawbacks

- CMS approval dependence adds timing risk

MA concentration: ~75% revenue, 5.8M members; CMS risk

Humana 2024: ~75% revenue from Medicare Advantage and 5.8M MA members, concentrating exposure to CMS policy and rate shifts.

Medical utilization and pharmacy/specialty drug inflation (~9% pharmacy inflation in 2024) have raised MLRs and compressed margins.

Clinical-asset ownership and state-concentrated enrollment increase fixed-cost, network and regulatory vulnerability.

| Metric | 2024 |

|---|---|

| MA revenue share | ~75% |

| MA members | 5.8M |

| Pharmacy inflation | ~9% |

Full Version Awaits

Humana SWOT Analysis

This is a real excerpt from the complete Humana SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Purchase unlocks the entire in-depth version immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Our Humana SWOT analysis distills the insurer’s competitive strengths, regulatory and reimbursement risks, and growth opportunities in Medicare Advantage and value-based care. It highlights strategic implications for investors and partners, with data-driven takeaways. Purchase the full report for the editable, investor-ready SWOT and actionable recommendations.

Strengths

Medicare Advantage market leadership

Humana holds a top-tier Medicare Advantage position with over 5 million MA enrollees in 2024, offering deep plan breadth across markets. Scale drives pricing leverage, richer supplemental benefits and tighter medical-cost management. Strong brand recognition among seniors aids retention and cross-sell into Part D and ancillary products. Market leadership builds a data flywheel that enhances risk scoring and targeted care management.

Integrated care and home-based delivery

Humana combines insurance with CenterWell primary care, home health and pharmacy services, serving about 6.3 million Medicare Advantage members and operating 600+ CenterWell locations as of 2024; these integrated clinical assets enable coordinated, value-based care with lower hospitalizations and contributed to a medical loss ratio near 85% in 2024, supporting sustainable margins and improved member outcomes.

Advanced analytics and risk management

Humana leverages extensive claims and clinical data to stratify risk and precisely target interventions, enabling earlier care coordination and chronic disease management. Predictive models drive utilization management and medication adherence programs, improving clinical outcomes and lowering avoidable utilization. Analytics boost STARS performance and reimbursement optimization while data-driven operations sustain continuous cost trend control.

Diverse product portfolio

Humana’s diverse product portfolio covers medical, dental, vision and supplemental benefits across individual, group and government lines, with 2024 revenue of about $86.7 billion and ~7.0 million Medicare Advantage members, spreading revenue risk and expanding addressable markets. Integrated pharmacy and specialty services deepen member relationships and drive retention, while multi-channel distribution (brokers, direct, Medicare channels) supports growth resilience.

Strong provider partnerships and value-based contracts

Humana's deep relationships with physician groups and MSOs tied to value outcomes—covering about 7.4 million Medicare Advantage and related members in 2024—drive shared-savings and capitated arrangements that improve cost predictability and margin stability. Clinical alignment enhances quality metrics and member satisfaction, and the network strategy supports scalable, repeatable operating performance.

- Value-based reach: ~7.4M MA/related members (2024)

- Payment models: shared savings and capitation improve predictability

- Outcomes: clinical alignment raises quality scores and satisfaction

- Scalability: network strategy enables repeatable operating performance

Leading Medicare Advantage: ~7.0M members, $86.7B revenue, integrated care & value-based reach

Humana holds a leading Medicare Advantage position with ~7.0M MA members (2024) and $86.7B revenue (2024), enabling pricing leverage and rich benefits. Integrated CenterWell primary care (600+ locations) plus pharmacy and home health support coordinated, value-based care and lower utilization. Value-based reach ~7.4M members and MLR near 85% in 2024 enhance cost predictability and outcomes.

| Metric | 2024 |

|---|---|

| Revenue | $86.7B |

| Medicare Advantage members | ~7.0M |

| Value-based reach | ~7.4M |

| CenterWell locations | 600+ |

| Medical Loss Ratio | ~85% |

What is included in the product

Delivers a strategic overview of Humana’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and risks shaping the future of its healthcare and insurance operations.

Provides a concise Humana SWOT matrix that highlights key strengths, weaknesses, opportunities, and threats to quickly relieve strategic decision-making pain points in healthcare operations and member services.

Weaknesses

High dependence on Medicare Advantage

Humana derives roughly 75% of 2024 consolidated revenue from Medicare Advantage and served about 5.8 million MA members in 2024, concentrating revenue and earnings in MA and increasing exposure to CMS policy and rate changes. Portfolio concentration raises volatility when benchmark rates or risk-adjustment factors shift, and Humana's commercial and Medicaid footprints remain comparatively limited. That dependency can constrain growth if MA dynamics weaken.

Exposure to medical cost trend volatility

Utilization spikes, notably inpatient and outpatient, can compress margins as post-pandemic normalization remains uneven across cohorts, with Medicare Advantage utilization still above 2019 baselines in some segments. Pharmacy and specialty drug inflation (around 9% industrywide in 2024) has pushed MLR higher. Pricing cycles often lag cost trends, creating near-term earnings risk if cost inflation persists. Humana faces pressure to rebalance rates versus accelerating medical costs.

Operational complexity from integrated model

Owning clinical assets—primary care, home health, pharmacies and care-delivery centers—raises fixed costs and execution risk as Humana balances facility investments with enrollment-driven revenue. Coordinating payor functions with primary care, home health and pharmacy needs tight governance and interoperable systems to avoid care fragmentation. Integration missteps can erode quality and member experience, while capital intensity limits flexibility in economic downturns.

Geographic concentration risks

Humana’s enrollment is concentrated in select states and in Medicare Advantage, making local regulatory shifts and regional competition able to disproportionately affect financial results and membership trends.

Disruptions to provider networks in key markets can cause outsized cost and access issues, while market-specific reputational problems have hindered growth in affected regions.

- Geographic enrollment concentration

- Medicare Advantage dependency

- Provider-network vulnerability

- Local reputational risk

Regulatory and ratings sensitivity

Regulatory and ratings sensitivity: CMS Star Ratings (scale 1–5) directly drive quality bonus payments and beneficiary choice, so volatility of even half-star shifts can materially reduce bonus revenue and plan appeal; compliance missteps risk sanctions, fines or enrollment freezes, and prior-year coding/documentation audits can trigger retroactive clawbacks; dependence on CMS approvals creates timing uncertainty for product launches and rate changes.

- Star Ratings scale 1–5 affect bonuses and enrollment

- Compliance failures → sanctions, fines, enrollment freezes

- Prior-year coding audits can cause clawbacks

- CMS approval dependence adds timing risk

MA concentration: ~75% revenue, 5.8M members; CMS risk

Humana 2024: ~75% revenue from Medicare Advantage and 5.8M MA members, concentrating exposure to CMS policy and rate shifts.

Medical utilization and pharmacy/specialty drug inflation (~9% pharmacy inflation in 2024) have raised MLRs and compressed margins.

Clinical-asset ownership and state-concentrated enrollment increase fixed-cost, network and regulatory vulnerability.

| Metric | 2024 |

|---|---|

| MA revenue share | ~75% |

| MA members | 5.8M |

| Pharmacy inflation | ~9% |

Full Version Awaits

Humana SWOT Analysis

This is a real excerpt from the complete Humana SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Purchase unlocks the entire in-depth version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Our Humana SWOT analysis distills the insurer’s competitive strengths, regulatory and reimbursement risks, and growth opportunities in Medicare Advantage and value-based care. It highlights strategic implications for investors and partners, with data-driven takeaways. Purchase the full report for the editable, investor-ready SWOT and actionable recommendations.

Strengths

Medicare Advantage market leadership

Humana holds a top-tier Medicare Advantage position with over 5 million MA enrollees in 2024, offering deep plan breadth across markets. Scale drives pricing leverage, richer supplemental benefits and tighter medical-cost management. Strong brand recognition among seniors aids retention and cross-sell into Part D and ancillary products. Market leadership builds a data flywheel that enhances risk scoring and targeted care management.

Integrated care and home-based delivery

Humana combines insurance with CenterWell primary care, home health and pharmacy services, serving about 6.3 million Medicare Advantage members and operating 600+ CenterWell locations as of 2024; these integrated clinical assets enable coordinated, value-based care with lower hospitalizations and contributed to a medical loss ratio near 85% in 2024, supporting sustainable margins and improved member outcomes.

Advanced analytics and risk management

Humana leverages extensive claims and clinical data to stratify risk and precisely target interventions, enabling earlier care coordination and chronic disease management. Predictive models drive utilization management and medication adherence programs, improving clinical outcomes and lowering avoidable utilization. Analytics boost STARS performance and reimbursement optimization while data-driven operations sustain continuous cost trend control.

Diverse product portfolio

Humana’s diverse product portfolio covers medical, dental, vision and supplemental benefits across individual, group and government lines, with 2024 revenue of about $86.7 billion and ~7.0 million Medicare Advantage members, spreading revenue risk and expanding addressable markets. Integrated pharmacy and specialty services deepen member relationships and drive retention, while multi-channel distribution (brokers, direct, Medicare channels) supports growth resilience.

Strong provider partnerships and value-based contracts

Humana's deep relationships with physician groups and MSOs tied to value outcomes—covering about 7.4 million Medicare Advantage and related members in 2024—drive shared-savings and capitated arrangements that improve cost predictability and margin stability. Clinical alignment enhances quality metrics and member satisfaction, and the network strategy supports scalable, repeatable operating performance.

- Value-based reach: ~7.4M MA/related members (2024)

- Payment models: shared savings and capitation improve predictability

- Outcomes: clinical alignment raises quality scores and satisfaction

- Scalability: network strategy enables repeatable operating performance

Leading Medicare Advantage: ~7.0M members, $86.7B revenue, integrated care & value-based reach

Humana holds a leading Medicare Advantage position with ~7.0M MA members (2024) and $86.7B revenue (2024), enabling pricing leverage and rich benefits. Integrated CenterWell primary care (600+ locations) plus pharmacy and home health support coordinated, value-based care and lower utilization. Value-based reach ~7.4M members and MLR near 85% in 2024 enhance cost predictability and outcomes.

| Metric | 2024 |

|---|---|

| Revenue | $86.7B |

| Medicare Advantage members | ~7.0M |

| Value-based reach | ~7.4M |

| CenterWell locations | 600+ |

| Medical Loss Ratio | ~85% |

What is included in the product

Delivers a strategic overview of Humana’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position, growth drivers, operational gaps, and risks shaping the future of its healthcare and insurance operations.

Provides a concise Humana SWOT matrix that highlights key strengths, weaknesses, opportunities, and threats to quickly relieve strategic decision-making pain points in healthcare operations and member services.

Weaknesses

High dependence on Medicare Advantage

Humana derives roughly 75% of 2024 consolidated revenue from Medicare Advantage and served about 5.8 million MA members in 2024, concentrating revenue and earnings in MA and increasing exposure to CMS policy and rate changes. Portfolio concentration raises volatility when benchmark rates or risk-adjustment factors shift, and Humana's commercial and Medicaid footprints remain comparatively limited. That dependency can constrain growth if MA dynamics weaken.

Exposure to medical cost trend volatility

Utilization spikes, notably inpatient and outpatient, can compress margins as post-pandemic normalization remains uneven across cohorts, with Medicare Advantage utilization still above 2019 baselines in some segments. Pharmacy and specialty drug inflation (around 9% industrywide in 2024) has pushed MLR higher. Pricing cycles often lag cost trends, creating near-term earnings risk if cost inflation persists. Humana faces pressure to rebalance rates versus accelerating medical costs.

Operational complexity from integrated model

Owning clinical assets—primary care, home health, pharmacies and care-delivery centers—raises fixed costs and execution risk as Humana balances facility investments with enrollment-driven revenue. Coordinating payor functions with primary care, home health and pharmacy needs tight governance and interoperable systems to avoid care fragmentation. Integration missteps can erode quality and member experience, while capital intensity limits flexibility in economic downturns.

Geographic concentration risks

Humana’s enrollment is concentrated in select states and in Medicare Advantage, making local regulatory shifts and regional competition able to disproportionately affect financial results and membership trends.

Disruptions to provider networks in key markets can cause outsized cost and access issues, while market-specific reputational problems have hindered growth in affected regions.

- Geographic enrollment concentration

- Medicare Advantage dependency

- Provider-network vulnerability

- Local reputational risk

Regulatory and ratings sensitivity

Regulatory and ratings sensitivity: CMS Star Ratings (scale 1–5) directly drive quality bonus payments and beneficiary choice, so volatility of even half-star shifts can materially reduce bonus revenue and plan appeal; compliance missteps risk sanctions, fines or enrollment freezes, and prior-year coding/documentation audits can trigger retroactive clawbacks; dependence on CMS approvals creates timing uncertainty for product launches and rate changes.

- Star Ratings scale 1–5 affect bonuses and enrollment

- Compliance failures → sanctions, fines, enrollment freezes

- Prior-year coding audits can cause clawbacks

- CMS approval dependence adds timing risk

MA concentration: ~75% revenue, 5.8M members; CMS risk

Humana 2024: ~75% revenue from Medicare Advantage and 5.8M MA members, concentrating exposure to CMS policy and rate shifts.

Medical utilization and pharmacy/specialty drug inflation (~9% pharmacy inflation in 2024) have raised MLRs and compressed margins.

Clinical-asset ownership and state-concentrated enrollment increase fixed-cost, network and regulatory vulnerability.

| Metric | 2024 |

|---|---|

| MA revenue share | ~75% |

| MA members | 5.8M |

| Pharmacy inflation | ~9% |

Full Version Awaits

Humana SWOT Analysis

This is a real excerpt from the complete Humana SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Purchase unlocks the entire in-depth version immediately after checkout.