Hydratec Industries Porter's Five Forces Analysis

Don't Miss the Bigger Picture

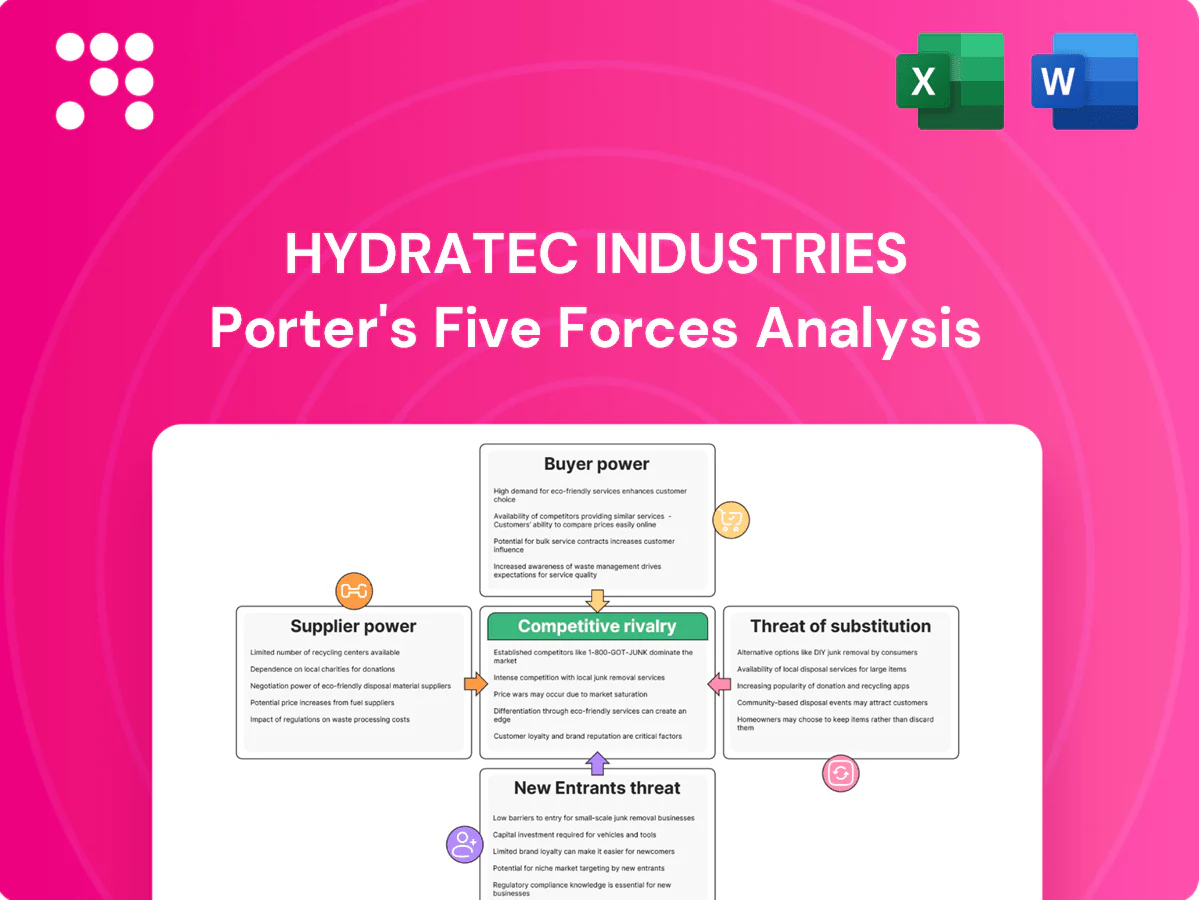

Hydratec Industries faces moderate supplier power but intense rival rivalry due to commoditized products and tight margins. Buyer bargaining is rising as customers demand integrated solutions and lower prices. Threats from substitutes and new entrants are tempered by regulatory barriers and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hydratec’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized components

Hydratec relies on niche inputs—robotics, motion controls, sensors, precision tooling—where the top five robot/mechatronics suppliers account for roughly 70% of market share, creating moderate–high supplier concentration. Limited alternative sources push switching costs and lead times often into 12–24 week ranges. Long-term contracts and dual sourcing can blunt supplier pricing power, but product redesigns add significant CAPEX and months of delay. Semiconductor/mechatronics shocks have delayed projects industry-wide, amplifying schedule risk.

Resins and materials

Resins and materials supply is volatile because engineering resin prices track petrochemical feedstocks, giving tier-1 producers pricing power in tight markets and for scarce medical-grade and food-contact grades; material qualification and regulatory hurdles make switching slow and expensive. Forward contracts commonly extend 12–24 months and recycled-content sourcing can dampen swings but cannot fully eliminate feedstock-driven volatility.

Certification and compliance

Suppliers providing FDA, EU MDR, ISO or food-safety certified parts often command premiums of roughly 15–25% in 2024, boosting supplier margins. Qualification processes and recurring audits concentrate supply to about 3–5 qualified vendors for key components. Any supplier change triggers revalidation costs (commonly around $150k–$300k) and 3–6 month delays. This materially elevates supplier bargaining power in regulated segments.

Logistics and energy

Technology roadmaps

Upstream technology cycles in 2024 shape the capabilities Hydratec can deliver, as the global industrial automation market exceeded 200 billion USD, concentrating innovation in firmware, drives and control software. Suppliers that control firmware, motor drives and ecosystems (Siemens, ABB, Rockwell among leaders) can lock integration paths and extract upgrade fees. API and protocol dependencies raise switching costs and hardware refresh cycles, increasing supplier stickiness. Co-development partnerships reduce access risk and allow Hydratec to influence supplier roadmaps.

- Market size 2024: >200B USD

- Top suppliers concentrate R&D and integration

- API/protocol lock-in increases upgrade revenue for suppliers

- Co-development secures access and roadmap influence

Supplier concentration ~70%, 12-24 wk lead times and energy costs squeeze margins

Hydratec faces moderate–high supplier power: top‑5 mechatronics suppliers ~70% share; automation market >$200B (2024). Lead times 12–24 weeks; certified parts 15–25% premiums with 3–5 qualified vendors and revalidation ~$150k–$300k. 2024 energy/freight pressure (TTF €35/MWh; EU ETS €80/t) raises pass-throughs.

| Metric | 2024 |

|---|---|

| Top‑5 share | ~70% |

| Lead times | 12–24 wks |

| TTF / EU ETS | €35/MWh / €80/t |

What is included in the product

Tailored Porter's Five Forces analysis for Hydratec Industries that uncovers key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry affecting pricing and profitability; includes strategic commentary on disruptive threats and defensive opportunities to protect market share.

A one-sheet Porter's Five Forces summary for Hydratec Industries highlighting supplier/customer power, substitutes, new entrants and rivalry—ideal for quick strategy decisions; customizable pressure levels and clean visuals make it slide-ready and easy for non-finance teams.

Customers Bargaining Power

Concentrated OEMs

Large food, automotive and healthcare OEMs often award system contracts exceeding $1M and routinely demand volume discounts (commonly 5–20%), with professional procurement teams running competitive tenders that elevate price pressure. Their scale and consolidated sourcing give them strong bargaining leverage, yet validated performance and uptime targets (typically >99% SLA) materially reduce willingness to churn among integrators.

Customization leverage

Projects are often bespoke, letting buyers demand tailored specs and commercial terms; custom engineering becomes a lever to lower price and assert IP rights. Deep integration raises switching costs through training, spares and software, strengthening buyer dependence. Lifecycle performance guarantees shift negotiations from capex to total cost of ownership, making service terms and uptime commitments central to customer bargaining power.

Service dependence

After-sales maintenance, spare parts and upgrades create platform lock-in—aftermarket services often account for 20-30% of OEM lifecycle revenue in industrial equipment (2024 industry data). Robust predictive maintenance and SLA programs, shown to cut unplanned downtime by up to 40%, can secure recurring revenue and lower buyer leverage. Weak service response raises renegotiation pressure; remote support and data access rights remain central bargaining points.

Regulatory and validation

Healthcare and food customers demand validated equipment with full traceability, narrowing acceptable suppliers and raising switching costs; requalification often runs from 50,000 to 200,000 USD and reduces mid-cycle churn. Buyers still press for compliance documentation and audit access, and in 2024 about 62% of procurement teams weight supplier sustainability (energy use, recyclability) in tender decisions.

- Narrow supplier pool due to validation/traceability

- Requalification costs 50k–200k USD lower switching

- Buyers negotiate docs and audit access

- 62% of buyers (2024) factor sustainability

Economic sensitivity

Cyclical end-markets shift buyer urgency and budgets; with IMF 2024 global growth at about 3.1% buyers tighten capex and in downturns often defer automation or demand price concessions, while tight labor markets (wage pressures up) strengthen automation ROI and blunt buyer price-push; flexible financing and outcome-based pricing reduce buyer leverage across cycles.

- Buyers defer capex in downturns

- Labor scarcity raises ROI for automation

- Flexible financing lowers purchase resistance

Predictive maintenance cuts downtime up to 40% as buyers (62%) demand sustainability

Large OEMs extract 5–20% volume discounts and run competitive tenders, but >99% SLA demands and bespoke integration raise switching costs. Aftermarket services (20–30% of lifecycle revenue) and requalification costs (50k–200k USD) lock buyers in; predictive maintenance can cut downtime up to 40%. In 2024, 62% of buyers weigh sustainability; IMF growth ~3.1% tightens capex.

| Metric | Value |

|---|---|

| Volume discounts | 5–20% |

| SLA | >99% |

| Aftermarket rev | 20–30% |

| Requalification | 50k–200k USD |

| Buyers weighting sustainability (2024) | 62% |

Same Document Delivered

Hydratec Industries Porter's Five Forces Analysis

This preview shows the exact Hydratec Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The file is fully formatted, professionally written and ready for download and use the moment you buy. You’re viewing the final deliverable; what you see is exactly what will be available to you instantly after payment.

Don't Miss the Bigger Picture

Hydratec Industries faces moderate supplier power but intense rival rivalry due to commoditized products and tight margins. Buyer bargaining is rising as customers demand integrated solutions and lower prices. Threats from substitutes and new entrants are tempered by regulatory barriers and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hydratec’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized components

Hydratec relies on niche inputs—robotics, motion controls, sensors, precision tooling—where the top five robot/mechatronics suppliers account for roughly 70% of market share, creating moderate–high supplier concentration. Limited alternative sources push switching costs and lead times often into 12–24 week ranges. Long-term contracts and dual sourcing can blunt supplier pricing power, but product redesigns add significant CAPEX and months of delay. Semiconductor/mechatronics shocks have delayed projects industry-wide, amplifying schedule risk.

Resins and materials

Resins and materials supply is volatile because engineering resin prices track petrochemical feedstocks, giving tier-1 producers pricing power in tight markets and for scarce medical-grade and food-contact grades; material qualification and regulatory hurdles make switching slow and expensive. Forward contracts commonly extend 12–24 months and recycled-content sourcing can dampen swings but cannot fully eliminate feedstock-driven volatility.

Certification and compliance

Suppliers providing FDA, EU MDR, ISO or food-safety certified parts often command premiums of roughly 15–25% in 2024, boosting supplier margins. Qualification processes and recurring audits concentrate supply to about 3–5 qualified vendors for key components. Any supplier change triggers revalidation costs (commonly around $150k–$300k) and 3–6 month delays. This materially elevates supplier bargaining power in regulated segments.

Logistics and energy

Technology roadmaps

Upstream technology cycles in 2024 shape the capabilities Hydratec can deliver, as the global industrial automation market exceeded 200 billion USD, concentrating innovation in firmware, drives and control software. Suppliers that control firmware, motor drives and ecosystems (Siemens, ABB, Rockwell among leaders) can lock integration paths and extract upgrade fees. API and protocol dependencies raise switching costs and hardware refresh cycles, increasing supplier stickiness. Co-development partnerships reduce access risk and allow Hydratec to influence supplier roadmaps.

- Market size 2024: >200B USD

- Top suppliers concentrate R&D and integration

- API/protocol lock-in increases upgrade revenue for suppliers

- Co-development secures access and roadmap influence

Supplier concentration ~70%, 12-24 wk lead times and energy costs squeeze margins

Hydratec faces moderate–high supplier power: top‑5 mechatronics suppliers ~70% share; automation market >$200B (2024). Lead times 12–24 weeks; certified parts 15–25% premiums with 3–5 qualified vendors and revalidation ~$150k–$300k. 2024 energy/freight pressure (TTF €35/MWh; EU ETS €80/t) raises pass-throughs.

| Metric | 2024 |

|---|---|

| Top‑5 share | ~70% |

| Lead times | 12–24 wks |

| TTF / EU ETS | €35/MWh / €80/t |

What is included in the product

Tailored Porter's Five Forces analysis for Hydratec Industries that uncovers key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry affecting pricing and profitability; includes strategic commentary on disruptive threats and defensive opportunities to protect market share.

A one-sheet Porter's Five Forces summary for Hydratec Industries highlighting supplier/customer power, substitutes, new entrants and rivalry—ideal for quick strategy decisions; customizable pressure levels and clean visuals make it slide-ready and easy for non-finance teams.

Customers Bargaining Power

Concentrated OEMs

Large food, automotive and healthcare OEMs often award system contracts exceeding $1M and routinely demand volume discounts (commonly 5–20%), with professional procurement teams running competitive tenders that elevate price pressure. Their scale and consolidated sourcing give them strong bargaining leverage, yet validated performance and uptime targets (typically >99% SLA) materially reduce willingness to churn among integrators.

Customization leverage

Projects are often bespoke, letting buyers demand tailored specs and commercial terms; custom engineering becomes a lever to lower price and assert IP rights. Deep integration raises switching costs through training, spares and software, strengthening buyer dependence. Lifecycle performance guarantees shift negotiations from capex to total cost of ownership, making service terms and uptime commitments central to customer bargaining power.

Service dependence

After-sales maintenance, spare parts and upgrades create platform lock-in—aftermarket services often account for 20-30% of OEM lifecycle revenue in industrial equipment (2024 industry data). Robust predictive maintenance and SLA programs, shown to cut unplanned downtime by up to 40%, can secure recurring revenue and lower buyer leverage. Weak service response raises renegotiation pressure; remote support and data access rights remain central bargaining points.

Regulatory and validation

Healthcare and food customers demand validated equipment with full traceability, narrowing acceptable suppliers and raising switching costs; requalification often runs from 50,000 to 200,000 USD and reduces mid-cycle churn. Buyers still press for compliance documentation and audit access, and in 2024 about 62% of procurement teams weight supplier sustainability (energy use, recyclability) in tender decisions.

- Narrow supplier pool due to validation/traceability

- Requalification costs 50k–200k USD lower switching

- Buyers negotiate docs and audit access

- 62% of buyers (2024) factor sustainability

Economic sensitivity

Cyclical end-markets shift buyer urgency and budgets; with IMF 2024 global growth at about 3.1% buyers tighten capex and in downturns often defer automation or demand price concessions, while tight labor markets (wage pressures up) strengthen automation ROI and blunt buyer price-push; flexible financing and outcome-based pricing reduce buyer leverage across cycles.

- Buyers defer capex in downturns

- Labor scarcity raises ROI for automation

- Flexible financing lowers purchase resistance

Predictive maintenance cuts downtime up to 40% as buyers (62%) demand sustainability

Large OEMs extract 5–20% volume discounts and run competitive tenders, but >99% SLA demands and bespoke integration raise switching costs. Aftermarket services (20–30% of lifecycle revenue) and requalification costs (50k–200k USD) lock buyers in; predictive maintenance can cut downtime up to 40%. In 2024, 62% of buyers weigh sustainability; IMF growth ~3.1% tightens capex.

| Metric | Value |

|---|---|

| Volume discounts | 5–20% |

| SLA | >99% |

| Aftermarket rev | 20–30% |

| Requalification | 50k–200k USD |

| Buyers weighting sustainability (2024) | 62% |

Same Document Delivered

Hydratec Industries Porter's Five Forces Analysis

This preview shows the exact Hydratec Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The file is fully formatted, professionally written and ready for download and use the moment you buy. You’re viewing the final deliverable; what you see is exactly what will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Hydratec Industries faces moderate supplier power but intense rival rivalry due to commoditized products and tight margins. Buyer bargaining is rising as customers demand integrated solutions and lower prices. Threats from substitutes and new entrants are tempered by regulatory barriers and scale advantages. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Hydratec’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized components

Hydratec relies on niche inputs—robotics, motion controls, sensors, precision tooling—where the top five robot/mechatronics suppliers account for roughly 70% of market share, creating moderate–high supplier concentration. Limited alternative sources push switching costs and lead times often into 12–24 week ranges. Long-term contracts and dual sourcing can blunt supplier pricing power, but product redesigns add significant CAPEX and months of delay. Semiconductor/mechatronics shocks have delayed projects industry-wide, amplifying schedule risk.

Resins and materials

Resins and materials supply is volatile because engineering resin prices track petrochemical feedstocks, giving tier-1 producers pricing power in tight markets and for scarce medical-grade and food-contact grades; material qualification and regulatory hurdles make switching slow and expensive. Forward contracts commonly extend 12–24 months and recycled-content sourcing can dampen swings but cannot fully eliminate feedstock-driven volatility.

Certification and compliance

Suppliers providing FDA, EU MDR, ISO or food-safety certified parts often command premiums of roughly 15–25% in 2024, boosting supplier margins. Qualification processes and recurring audits concentrate supply to about 3–5 qualified vendors for key components. Any supplier change triggers revalidation costs (commonly around $150k–$300k) and 3–6 month delays. This materially elevates supplier bargaining power in regulated segments.

Logistics and energy

Technology roadmaps

Upstream technology cycles in 2024 shape the capabilities Hydratec can deliver, as the global industrial automation market exceeded 200 billion USD, concentrating innovation in firmware, drives and control software. Suppliers that control firmware, motor drives and ecosystems (Siemens, ABB, Rockwell among leaders) can lock integration paths and extract upgrade fees. API and protocol dependencies raise switching costs and hardware refresh cycles, increasing supplier stickiness. Co-development partnerships reduce access risk and allow Hydratec to influence supplier roadmaps.

- Market size 2024: >200B USD

- Top suppliers concentrate R&D and integration

- API/protocol lock-in increases upgrade revenue for suppliers

- Co-development secures access and roadmap influence

Supplier concentration ~70%, 12-24 wk lead times and energy costs squeeze margins

Hydratec faces moderate–high supplier power: top‑5 mechatronics suppliers ~70% share; automation market >$200B (2024). Lead times 12–24 weeks; certified parts 15–25% premiums with 3–5 qualified vendors and revalidation ~$150k–$300k. 2024 energy/freight pressure (TTF €35/MWh; EU ETS €80/t) raises pass-throughs.

| Metric | 2024 |

|---|---|

| Top‑5 share | ~70% |

| Lead times | 12–24 wks |

| TTF / EU ETS | €35/MWh / €80/t |

What is included in the product

Tailored Porter's Five Forces analysis for Hydratec Industries that uncovers key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry affecting pricing and profitability; includes strategic commentary on disruptive threats and defensive opportunities to protect market share.

A one-sheet Porter's Five Forces summary for Hydratec Industries highlighting supplier/customer power, substitutes, new entrants and rivalry—ideal for quick strategy decisions; customizable pressure levels and clean visuals make it slide-ready and easy for non-finance teams.

Customers Bargaining Power

Concentrated OEMs

Large food, automotive and healthcare OEMs often award system contracts exceeding $1M and routinely demand volume discounts (commonly 5–20%), with professional procurement teams running competitive tenders that elevate price pressure. Their scale and consolidated sourcing give them strong bargaining leverage, yet validated performance and uptime targets (typically >99% SLA) materially reduce willingness to churn among integrators.

Customization leverage

Projects are often bespoke, letting buyers demand tailored specs and commercial terms; custom engineering becomes a lever to lower price and assert IP rights. Deep integration raises switching costs through training, spares and software, strengthening buyer dependence. Lifecycle performance guarantees shift negotiations from capex to total cost of ownership, making service terms and uptime commitments central to customer bargaining power.

Service dependence

After-sales maintenance, spare parts and upgrades create platform lock-in—aftermarket services often account for 20-30% of OEM lifecycle revenue in industrial equipment (2024 industry data). Robust predictive maintenance and SLA programs, shown to cut unplanned downtime by up to 40%, can secure recurring revenue and lower buyer leverage. Weak service response raises renegotiation pressure; remote support and data access rights remain central bargaining points.

Regulatory and validation

Healthcare and food customers demand validated equipment with full traceability, narrowing acceptable suppliers and raising switching costs; requalification often runs from 50,000 to 200,000 USD and reduces mid-cycle churn. Buyers still press for compliance documentation and audit access, and in 2024 about 62% of procurement teams weight supplier sustainability (energy use, recyclability) in tender decisions.

- Narrow supplier pool due to validation/traceability

- Requalification costs 50k–200k USD lower switching

- Buyers negotiate docs and audit access

- 62% of buyers (2024) factor sustainability

Economic sensitivity

Cyclical end-markets shift buyer urgency and budgets; with IMF 2024 global growth at about 3.1% buyers tighten capex and in downturns often defer automation or demand price concessions, while tight labor markets (wage pressures up) strengthen automation ROI and blunt buyer price-push; flexible financing and outcome-based pricing reduce buyer leverage across cycles.

- Buyers defer capex in downturns

- Labor scarcity raises ROI for automation

- Flexible financing lowers purchase resistance

Predictive maintenance cuts downtime up to 40% as buyers (62%) demand sustainability

Large OEMs extract 5–20% volume discounts and run competitive tenders, but >99% SLA demands and bespoke integration raise switching costs. Aftermarket services (20–30% of lifecycle revenue) and requalification costs (50k–200k USD) lock buyers in; predictive maintenance can cut downtime up to 40%. In 2024, 62% of buyers weigh sustainability; IMF growth ~3.1% tightens capex.

| Metric | Value |

|---|---|

| Volume discounts | 5–20% |

| SLA | >99% |

| Aftermarket rev | 20–30% |

| Requalification | 50k–200k USD |

| Buyers weighting sustainability (2024) | 62% |

Same Document Delivered

Hydratec Industries Porter's Five Forces Analysis

This preview shows the exact Hydratec Industries Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises or placeholders. The file is fully formatted, professionally written and ready for download and use the moment you buy. You’re viewing the final deliverable; what you see is exactly what will be available to you instantly after payment.