Hydrogen Group PESTLE Analysis

Skip the Research. Get the Strategy.

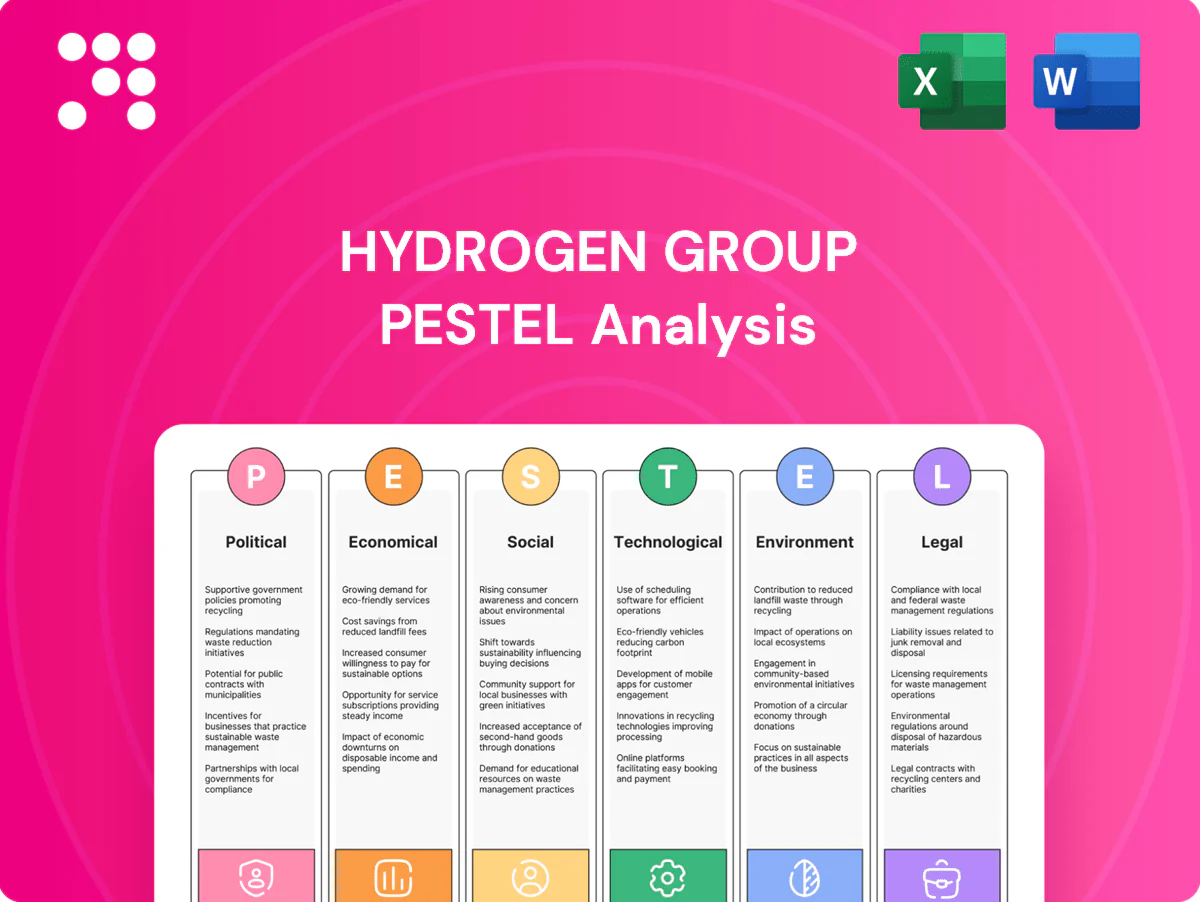

Gain strategic clarity with our PESTLE Analysis of Hydrogen Group—examining political, economic, social, technological, legal and environmental forces shaping its trajectory. Ideal for investors and strategists, it highlights regulatory risks, market opportunities and tech drivers. Buy the full report now for complete, ready-to-use insights and downloadable formats.

Political factors

Immigration and visa regimes

Work visa quotas like the US H-1B cap of 85,000 and variable processing times (USCIS premium processing 15 days, regular months) shape talent mobility; policy swings since 2020 raised denials and compliance costs. Tight regimes shrink candidate pools and delay cross-border placements, while liberal schemes (Canada Global Talent Stream 10 business days, UK skilled-worker ~3 weeks) expand niche STEM access. Hydrogen Group must monitor multi-country changes and advise clients on compliant hiring routes.

Government tech and infrastructure spend

Public digital programs and infrastructure budgets lift demand for transformation and STEM talent; global digital transformation spending reached about $3.0 trillion in 2024 (IDC), expanding government hiring for engineers and program managers. Post-election shifts frequently accelerate or pause hiring pipelines, with many governments reviewing contracts after votes. Priority areas—cybersecurity, AI, healthtech—account for the fastest hiring growth, mirroring a 2024 cybersecurity market near $220 billion (Gartner). Mapping fiscal and budget cycles helps forecast demand and bid timing.

Geopolitical stability and trade tensions

Geopolitical shocks like the Russia-Ukraine conflict (since Feb 2022) and US/EU sanctions or export controls on advanced tech (notably Oct 2022 chip rules) have disrupted hydrogen client projects and relocations, prompting pauses in hiring or reshoring and shifting role mixes; enhanced compliance can add weeks to onboarding, so scenario planning is used to protect pipeline continuity.

Skills policy and education funding

National upskilling agendas shift local supply of engineers and data talent, with the World Economic Forum estimating 50% of workers will need reskilling by 2025, increasing competition for hydrogen roles. Apprenticeships, STEM grants and reskilling programs raise candidate availability; policy cuts risk worsening shortages and driving wage inflation. Hydrogen can partner with programs to build talent pools ahead of demand.

- Reskilling need: WEF 50% by 2025

- Apprenticeships/STEM expand pipelines

- Partnerships mitigate future shortages

- Policy cuts = higher wage pressure

Diversity, equity, and inclusion mandates

Public-sector and regulated buyers increasingly embed DEI in procurement: the UK Social Value Model (updated 2023) explicitly includes workforce equality and supplier engagement, shaping shortlists, outreach and marketing for hydrogen projects. Demonstrable inclusive hiring and supplier-diversity metrics strengthen bids and pricing leverage. Failure to meet DEI criteria can bar firms from public frameworks and regulated contracts.

- DEI criteria drive shortlist decisions

- Social Value Model 2023 cited by UK buyers

- Inclusive hiring boosts bid competitiveness

- Non-compliance risks framework exclusion

Talent shift: H-1B 85,000, faster visas, $3.0trn digital

Visa caps (US H-1B 85,000; USCIS premium 15 days), faster schemes (Canada GTS 10 business days; UK skilled-worker ~3 weeks) reshape talent flows. Public digital spend ~$3.0trn (2024, IDC) and cybersecurity ~$220bn (2024, Gartner) drive demand. WEF: 50% need reskilling by 2025; UK Social Value Model 2023 embeds DEI in procurement, affecting bids.

| Indicator | 2023-2025 Data |

|---|---|

| H-1B cap | 85,000 |

| USCIS premium | 15 days |

| Canada GTS | 10 business days |

| Digital spend | $3.0trn (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental and Legal — uniquely affect the Hydrogen Group, combining current data and regional regulatory context to surface risks and opportunities. Designed for executives and investors, it delivers actionable, forward‑looking insights and scenario cues ready for business plans and strategy briefs.

A concise, visually segmented PESTLE summary of Hydrogen Group that teams can drop into presentations, modify with local notes, and share for quick alignment on external risks, market positioning, and strategic planning.

Economic factors

Hiring cycles and macro growth

Global GDP slowed to about 3% in 2024 (IMF) and falling business confidence tracked a decline in requisition volumes; downturns boosted contract/interim share by as much as 20–25% while expansions lifted permanent placements. Sector divergence is stark: tech endured the biggest cuts (headcount down ~20–30% in 2023–24), life sciences and financial services remained comparatively resilient. Early macro indicators like PMIs and weekly jobless claims guide desk rebalancing.

Wage inflation and skills premiums

Tight markets are driving wage inflation—ONS reported regular pay growth at 6.6% y/y to June 2024 while UK vacancies hovered around 1.0m—pushing up salaries and contractor rates and squeezing client budgets. Rate resistance can extend time-to-fill as contractor day rates rose roughly 8–10% in 2023–24 across tech and finance. Transparent benchmarking shortens closes. Hydrogen must update pay data by niche and region monthly.

Currency fluctuations

Multi-currency billing and candidate pay expose Hydrogen Group to FX risk across client invoicing and payroll; with global FX markets trading about $6.6 trillion per day (BIS 2022), currency moves can materially swing margins on international placements. Hedging programs and localized rate cards have cut realized volatility for many recruiters by up to mid-single digits in pilot programs. Clear FX clauses in contracts preserve profitability by passing or sharing exchange shocks with clients.

Funding cycles and deal flow

Funding cycles—VC, PE, and IPO windows—directly shape hiring in tech and biotech: PE and VC dry powder (private capital surpassed ~$2.5 trillion by mid-2024) drives scale-up hiring and C-suite mandates, while IPO windows reopen hiring sprees; funding droughts force headcount cuts and pivot to burn control.

- track fundraising milestones

- align pipeline to capital inflows

- shift hiring vs burn targets

Client procurement and payment terms

Longer DSO and tighter procurement cycles compress Hydrogen Group’s cash conversion—UK staffing DSO averaged about 50–60 days in 2024, increasing working capital pressure and funding needs.

Framework contracts drive volume but compress fees; early-pay discounts and strict credit checks shore up liquidity, while a higher MSP/RPO mix improves recurring revenue stability but can lower gross margin volatility.

- DSO: 50–60 days (UK staffing 2024)

- Frameworks: lower fees, higher volume

- Mitigants: early-pay incentives, credit checks

- MSP/RPO: boosts stability, compresses margin

Talent shift: H-1B 85,000, faster visas, $3.0trn digital

Economic slowdown (global GDP ~3% in 2024 IMF) and weaker confidence cut requisitions; tech layoffs (-20–30% 2023–24) contrast with resilient life sciences/finance. Wage inflation (UK regular pay +6.6% y/y to Jun 2024) and vacancies (~1.0m) push contractor rates +8–10%, lengthening time-to-fill and squeezing margins. DSO 50–60 days, private capital ~$2.5tn (mid‑2024), FX turnover $6.6tn/day add liquidity and FX risk.

| Metric | Value | Year/Source |

|---|---|---|

| Global GDP growth | ~3% | 2024 IMF |

| UK regular pay | +6.6% y/y | Jun 2024 ONS |

| Vacancies (UK) | ~1.0m | 2024 ONS |

| DSO (UK staffing) | 50–60 days | 2024 industry |

| Private capital | ~$2.5tn | mid‑2024 |

| FX turnover | $6.6tn/day | 2022 BIS |

Preview the Actual Deliverable

Hydrogen Group PESTLE Analysis

The Hydrogen Group PESTLE Analysis provides a clear, professional review of political, economic, social, technological, legal, and environmental factors affecting the business. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content and structure are identical to the downloadable file.

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Hydrogen Group—examining political, economic, social, technological, legal and environmental forces shaping its trajectory. Ideal for investors and strategists, it highlights regulatory risks, market opportunities and tech drivers. Buy the full report now for complete, ready-to-use insights and downloadable formats.

Political factors

Immigration and visa regimes

Work visa quotas like the US H-1B cap of 85,000 and variable processing times (USCIS premium processing 15 days, regular months) shape talent mobility; policy swings since 2020 raised denials and compliance costs. Tight regimes shrink candidate pools and delay cross-border placements, while liberal schemes (Canada Global Talent Stream 10 business days, UK skilled-worker ~3 weeks) expand niche STEM access. Hydrogen Group must monitor multi-country changes and advise clients on compliant hiring routes.

Government tech and infrastructure spend

Public digital programs and infrastructure budgets lift demand for transformation and STEM talent; global digital transformation spending reached about $3.0 trillion in 2024 (IDC), expanding government hiring for engineers and program managers. Post-election shifts frequently accelerate or pause hiring pipelines, with many governments reviewing contracts after votes. Priority areas—cybersecurity, AI, healthtech—account for the fastest hiring growth, mirroring a 2024 cybersecurity market near $220 billion (Gartner). Mapping fiscal and budget cycles helps forecast demand and bid timing.

Geopolitical stability and trade tensions

Geopolitical shocks like the Russia-Ukraine conflict (since Feb 2022) and US/EU sanctions or export controls on advanced tech (notably Oct 2022 chip rules) have disrupted hydrogen client projects and relocations, prompting pauses in hiring or reshoring and shifting role mixes; enhanced compliance can add weeks to onboarding, so scenario planning is used to protect pipeline continuity.

Skills policy and education funding

National upskilling agendas shift local supply of engineers and data talent, with the World Economic Forum estimating 50% of workers will need reskilling by 2025, increasing competition for hydrogen roles. Apprenticeships, STEM grants and reskilling programs raise candidate availability; policy cuts risk worsening shortages and driving wage inflation. Hydrogen can partner with programs to build talent pools ahead of demand.

- Reskilling need: WEF 50% by 2025

- Apprenticeships/STEM expand pipelines

- Partnerships mitigate future shortages

- Policy cuts = higher wage pressure

Diversity, equity, and inclusion mandates

Public-sector and regulated buyers increasingly embed DEI in procurement: the UK Social Value Model (updated 2023) explicitly includes workforce equality and supplier engagement, shaping shortlists, outreach and marketing for hydrogen projects. Demonstrable inclusive hiring and supplier-diversity metrics strengthen bids and pricing leverage. Failure to meet DEI criteria can bar firms from public frameworks and regulated contracts.

- DEI criteria drive shortlist decisions

- Social Value Model 2023 cited by UK buyers

- Inclusive hiring boosts bid competitiveness

- Non-compliance risks framework exclusion

Talent shift: H-1B 85,000, faster visas, $3.0trn digital

Visa caps (US H-1B 85,000; USCIS premium 15 days), faster schemes (Canada GTS 10 business days; UK skilled-worker ~3 weeks) reshape talent flows. Public digital spend ~$3.0trn (2024, IDC) and cybersecurity ~$220bn (2024, Gartner) drive demand. WEF: 50% need reskilling by 2025; UK Social Value Model 2023 embeds DEI in procurement, affecting bids.

| Indicator | 2023-2025 Data |

|---|---|

| H-1B cap | 85,000 |

| USCIS premium | 15 days |

| Canada GTS | 10 business days |

| Digital spend | $3.0trn (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental and Legal — uniquely affect the Hydrogen Group, combining current data and regional regulatory context to surface risks and opportunities. Designed for executives and investors, it delivers actionable, forward‑looking insights and scenario cues ready for business plans and strategy briefs.

A concise, visually segmented PESTLE summary of Hydrogen Group that teams can drop into presentations, modify with local notes, and share for quick alignment on external risks, market positioning, and strategic planning.

Economic factors

Hiring cycles and macro growth

Global GDP slowed to about 3% in 2024 (IMF) and falling business confidence tracked a decline in requisition volumes; downturns boosted contract/interim share by as much as 20–25% while expansions lifted permanent placements. Sector divergence is stark: tech endured the biggest cuts (headcount down ~20–30% in 2023–24), life sciences and financial services remained comparatively resilient. Early macro indicators like PMIs and weekly jobless claims guide desk rebalancing.

Wage inflation and skills premiums

Tight markets are driving wage inflation—ONS reported regular pay growth at 6.6% y/y to June 2024 while UK vacancies hovered around 1.0m—pushing up salaries and contractor rates and squeezing client budgets. Rate resistance can extend time-to-fill as contractor day rates rose roughly 8–10% in 2023–24 across tech and finance. Transparent benchmarking shortens closes. Hydrogen must update pay data by niche and region monthly.

Currency fluctuations

Multi-currency billing and candidate pay expose Hydrogen Group to FX risk across client invoicing and payroll; with global FX markets trading about $6.6 trillion per day (BIS 2022), currency moves can materially swing margins on international placements. Hedging programs and localized rate cards have cut realized volatility for many recruiters by up to mid-single digits in pilot programs. Clear FX clauses in contracts preserve profitability by passing or sharing exchange shocks with clients.

Funding cycles and deal flow

Funding cycles—VC, PE, and IPO windows—directly shape hiring in tech and biotech: PE and VC dry powder (private capital surpassed ~$2.5 trillion by mid-2024) drives scale-up hiring and C-suite mandates, while IPO windows reopen hiring sprees; funding droughts force headcount cuts and pivot to burn control.

- track fundraising milestones

- align pipeline to capital inflows

- shift hiring vs burn targets

Client procurement and payment terms

Longer DSO and tighter procurement cycles compress Hydrogen Group’s cash conversion—UK staffing DSO averaged about 50–60 days in 2024, increasing working capital pressure and funding needs.

Framework contracts drive volume but compress fees; early-pay discounts and strict credit checks shore up liquidity, while a higher MSP/RPO mix improves recurring revenue stability but can lower gross margin volatility.

- DSO: 50–60 days (UK staffing 2024)

- Frameworks: lower fees, higher volume

- Mitigants: early-pay incentives, credit checks

- MSP/RPO: boosts stability, compresses margin

Talent shift: H-1B 85,000, faster visas, $3.0trn digital

Economic slowdown (global GDP ~3% in 2024 IMF) and weaker confidence cut requisitions; tech layoffs (-20–30% 2023–24) contrast with resilient life sciences/finance. Wage inflation (UK regular pay +6.6% y/y to Jun 2024) and vacancies (~1.0m) push contractor rates +8–10%, lengthening time-to-fill and squeezing margins. DSO 50–60 days, private capital ~$2.5tn (mid‑2024), FX turnover $6.6tn/day add liquidity and FX risk.

| Metric | Value | Year/Source |

|---|---|---|

| Global GDP growth | ~3% | 2024 IMF |

| UK regular pay | +6.6% y/y | Jun 2024 ONS |

| Vacancies (UK) | ~1.0m | 2024 ONS |

| DSO (UK staffing) | 50–60 days | 2024 industry |

| Private capital | ~$2.5tn | mid‑2024 |

| FX turnover | $6.6tn/day | 2022 BIS |

Preview the Actual Deliverable

Hydrogen Group PESTLE Analysis

The Hydrogen Group PESTLE Analysis provides a clear, professional review of political, economic, social, technological, legal, and environmental factors affecting the business. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content and structure are identical to the downloadable file.

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our PESTLE Analysis of Hydrogen Group—examining political, economic, social, technological, legal and environmental forces shaping its trajectory. Ideal for investors and strategists, it highlights regulatory risks, market opportunities and tech drivers. Buy the full report now for complete, ready-to-use insights and downloadable formats.

Political factors

Immigration and visa regimes

Work visa quotas like the US H-1B cap of 85,000 and variable processing times (USCIS premium processing 15 days, regular months) shape talent mobility; policy swings since 2020 raised denials and compliance costs. Tight regimes shrink candidate pools and delay cross-border placements, while liberal schemes (Canada Global Talent Stream 10 business days, UK skilled-worker ~3 weeks) expand niche STEM access. Hydrogen Group must monitor multi-country changes and advise clients on compliant hiring routes.

Government tech and infrastructure spend

Public digital programs and infrastructure budgets lift demand for transformation and STEM talent; global digital transformation spending reached about $3.0 trillion in 2024 (IDC), expanding government hiring for engineers and program managers. Post-election shifts frequently accelerate or pause hiring pipelines, with many governments reviewing contracts after votes. Priority areas—cybersecurity, AI, healthtech—account for the fastest hiring growth, mirroring a 2024 cybersecurity market near $220 billion (Gartner). Mapping fiscal and budget cycles helps forecast demand and bid timing.

Geopolitical stability and trade tensions

Geopolitical shocks like the Russia-Ukraine conflict (since Feb 2022) and US/EU sanctions or export controls on advanced tech (notably Oct 2022 chip rules) have disrupted hydrogen client projects and relocations, prompting pauses in hiring or reshoring and shifting role mixes; enhanced compliance can add weeks to onboarding, so scenario planning is used to protect pipeline continuity.

Skills policy and education funding

National upskilling agendas shift local supply of engineers and data talent, with the World Economic Forum estimating 50% of workers will need reskilling by 2025, increasing competition for hydrogen roles. Apprenticeships, STEM grants and reskilling programs raise candidate availability; policy cuts risk worsening shortages and driving wage inflation. Hydrogen can partner with programs to build talent pools ahead of demand.

- Reskilling need: WEF 50% by 2025

- Apprenticeships/STEM expand pipelines

- Partnerships mitigate future shortages

- Policy cuts = higher wage pressure

Diversity, equity, and inclusion mandates

Public-sector and regulated buyers increasingly embed DEI in procurement: the UK Social Value Model (updated 2023) explicitly includes workforce equality and supplier engagement, shaping shortlists, outreach and marketing for hydrogen projects. Demonstrable inclusive hiring and supplier-diversity metrics strengthen bids and pricing leverage. Failure to meet DEI criteria can bar firms from public frameworks and regulated contracts.

- DEI criteria drive shortlist decisions

- Social Value Model 2023 cited by UK buyers

- Inclusive hiring boosts bid competitiveness

- Non-compliance risks framework exclusion

Talent shift: H-1B 85,000, faster visas, $3.0trn digital

Visa caps (US H-1B 85,000; USCIS premium 15 days), faster schemes (Canada GTS 10 business days; UK skilled-worker ~3 weeks) reshape talent flows. Public digital spend ~$3.0trn (2024, IDC) and cybersecurity ~$220bn (2024, Gartner) drive demand. WEF: 50% need reskilling by 2025; UK Social Value Model 2023 embeds DEI in procurement, affecting bids.

| Indicator | 2023-2025 Data |

|---|---|

| H-1B cap | 85,000 |

| USCIS premium | 15 days |

| Canada GTS | 10 business days |

| Digital spend | $3.0trn (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental and Legal — uniquely affect the Hydrogen Group, combining current data and regional regulatory context to surface risks and opportunities. Designed for executives and investors, it delivers actionable, forward‑looking insights and scenario cues ready for business plans and strategy briefs.

A concise, visually segmented PESTLE summary of Hydrogen Group that teams can drop into presentations, modify with local notes, and share for quick alignment on external risks, market positioning, and strategic planning.

Economic factors

Hiring cycles and macro growth

Global GDP slowed to about 3% in 2024 (IMF) and falling business confidence tracked a decline in requisition volumes; downturns boosted contract/interim share by as much as 20–25% while expansions lifted permanent placements. Sector divergence is stark: tech endured the biggest cuts (headcount down ~20–30% in 2023–24), life sciences and financial services remained comparatively resilient. Early macro indicators like PMIs and weekly jobless claims guide desk rebalancing.

Wage inflation and skills premiums

Tight markets are driving wage inflation—ONS reported regular pay growth at 6.6% y/y to June 2024 while UK vacancies hovered around 1.0m—pushing up salaries and contractor rates and squeezing client budgets. Rate resistance can extend time-to-fill as contractor day rates rose roughly 8–10% in 2023–24 across tech and finance. Transparent benchmarking shortens closes. Hydrogen must update pay data by niche and region monthly.

Currency fluctuations

Multi-currency billing and candidate pay expose Hydrogen Group to FX risk across client invoicing and payroll; with global FX markets trading about $6.6 trillion per day (BIS 2022), currency moves can materially swing margins on international placements. Hedging programs and localized rate cards have cut realized volatility for many recruiters by up to mid-single digits in pilot programs. Clear FX clauses in contracts preserve profitability by passing or sharing exchange shocks with clients.

Funding cycles and deal flow

Funding cycles—VC, PE, and IPO windows—directly shape hiring in tech and biotech: PE and VC dry powder (private capital surpassed ~$2.5 trillion by mid-2024) drives scale-up hiring and C-suite mandates, while IPO windows reopen hiring sprees; funding droughts force headcount cuts and pivot to burn control.

- track fundraising milestones

- align pipeline to capital inflows

- shift hiring vs burn targets

Client procurement and payment terms

Longer DSO and tighter procurement cycles compress Hydrogen Group’s cash conversion—UK staffing DSO averaged about 50–60 days in 2024, increasing working capital pressure and funding needs.

Framework contracts drive volume but compress fees; early-pay discounts and strict credit checks shore up liquidity, while a higher MSP/RPO mix improves recurring revenue stability but can lower gross margin volatility.

- DSO: 50–60 days (UK staffing 2024)

- Frameworks: lower fees, higher volume

- Mitigants: early-pay incentives, credit checks

- MSP/RPO: boosts stability, compresses margin

Talent shift: H-1B 85,000, faster visas, $3.0trn digital

Economic slowdown (global GDP ~3% in 2024 IMF) and weaker confidence cut requisitions; tech layoffs (-20–30% 2023–24) contrast with resilient life sciences/finance. Wage inflation (UK regular pay +6.6% y/y to Jun 2024) and vacancies (~1.0m) push contractor rates +8–10%, lengthening time-to-fill and squeezing margins. DSO 50–60 days, private capital ~$2.5tn (mid‑2024), FX turnover $6.6tn/day add liquidity and FX risk.

| Metric | Value | Year/Source |

|---|---|---|

| Global GDP growth | ~3% | 2024 IMF |

| UK regular pay | +6.6% y/y | Jun 2024 ONS |

| Vacancies (UK) | ~1.0m | 2024 ONS |

| DSO (UK staffing) | 50–60 days | 2024 industry |

| Private capital | ~$2.5tn | mid‑2024 |

| FX turnover | $6.6tn/day | 2022 BIS |

Preview the Actual Deliverable

Hydrogen Group PESTLE Analysis

The Hydrogen Group PESTLE Analysis provides a clear, professional review of political, economic, social, technological, legal, and environmental factors affecting the business. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content and structure are identical to the downloadable file.