Hyundai Marine & Fire PESTLE Analysis

Skip the Research. Get the Strategy.

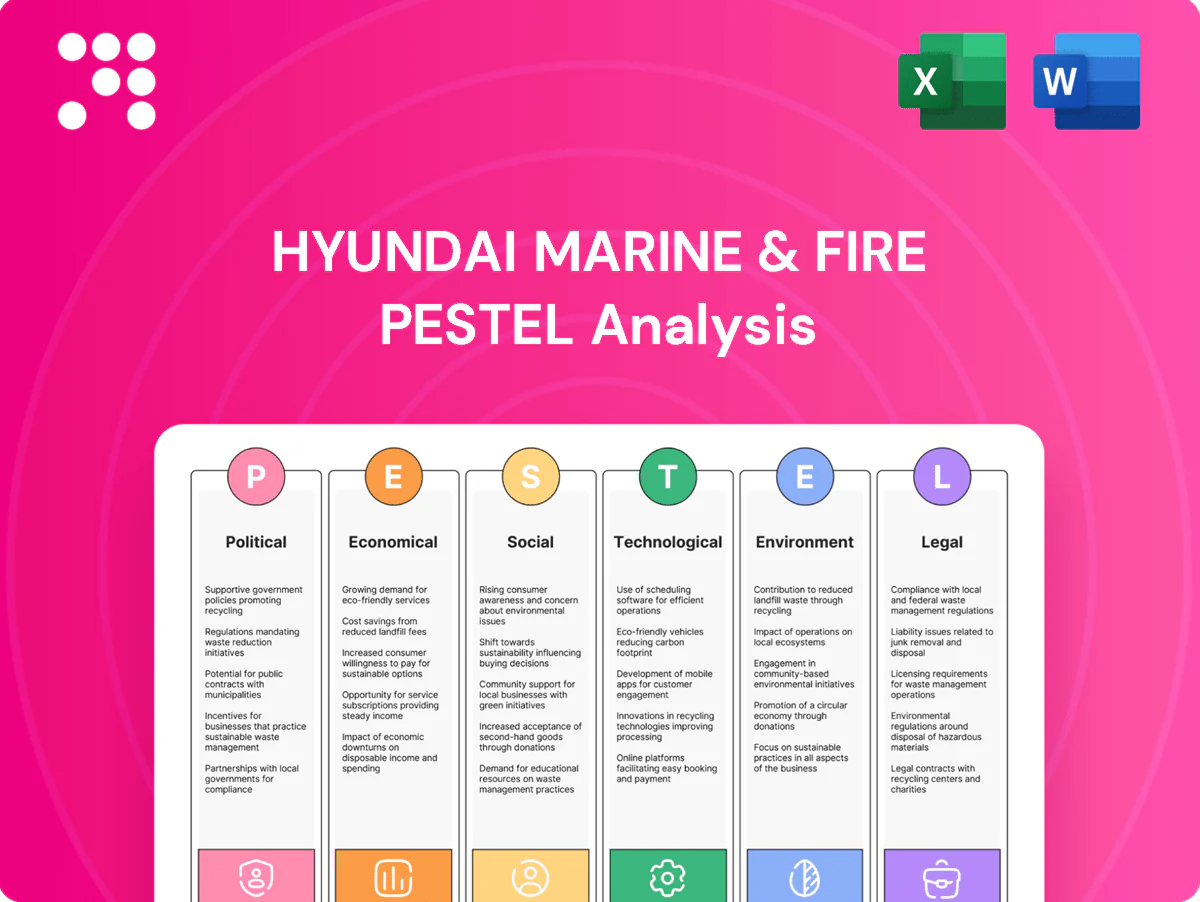

Our PESTLE Analysis of Hyundai Marine & Fire maps political, economic, social, technological, legal and environmental forces shaping the insurer’s strategy and risk profile. Packed with concise insights and real-world implications, it’s ideal for investors, advisors and strategists seeking a competitive edge. Purchase the full report to access the detailed breakdown, forecasts and ready-to-use recommendations.

Political factors

Regulatory oversight by FSC/FSS

South Korea’s Financial Services Commission and Financial Supervisory Service, established 1999 (FSS), set solvency, product and conduct rules, including a statutory risk-based capital minimum of 100% for insurers. Shifts in capital standards or reserve methodologies directly alter pricing and product mix, while close supervision raises compliance costs but underpins sector stability. Proactive engagement with regulators can shape rulemaking timelines and interpretations.

Government policy on social insurance

Public schemes such as Korea's National Health Insurance (covers over 97% of residents) and expanding pension/disaster relief programs (public social spending ~12.5% of GDP) reduce demand for some private long-term lines but leave gaps in accident, supplemental health and liability that Hyundai Marine & Fire can target. Post‑election policy shifts often reallocate subsidies, so insurers must realign product mix and pricing to evolving public‑private risk sharing.

Geopolitical tensions on the Korean Peninsula

Periodic North Korea risks elevate catastrophe, political-risk and supply-chain exposures for corporate clients, underlined by South Korea’s defense spending of about $50.6 billion in 2023 (SIPRI). Heightened tensions push reinsurers to demand larger capital buffers and higher premiums, increasing costs for Hyundai Marine & Fire while specialty-cover demand may grow but underwriting risk rises. Scenario planning and stress tests are critical for portfolio resilience.

Industrial policy and trade relations

Industrial policy and FTAs shape Hyundai Marine & Fire’s exposure: South Korea’s export orientation (roughly $700bn goods exports in 2024) drives demand for marine, cargo and trade-credit lines, while trade disputes or sanctions shift routes and increase claim frequency. Government support for EVs, semiconductors and shipbuilding (Korean yards held ~40% of global orderbook in 2024) reallocates commercial risk pools. Aligning underwriting capacity to favored sectors can unlock premium growth with targeted risk controls.

- FTA exposure: export-led premium opportunities

- Sanctions/trade disputes: higher route disruption claims

- Sector support: EVs/semiconductors/shipbuilding concentrate risk

- Strategy: capacity alignment + targeted controls = growth

Public disaster preparedness and subsidies

National disaster frameworks and mitigation funding shape catastrophe exposure and claims volatility; Swiss Re estimated insured natural catastrophe losses at about USD 120 billion in 2023. Government incentives for safety upgrades lower loss ratios over time—UNDRR finds each USD 1 invested in disaster risk reduction can save about USD 4 in future losses. Post-disaster aid can depress short-term insurance uptake while boosting reconstruction cover demand; partnerships on resiliency programs reduce tail risk and enhance Hyundai Marine & Fire’s brand.

- Policy environment: mitigation funding influences claims volatility

- Incentives: safety upgrades cut loss ratios (UNDRR 4:1 benefit)

- Post-disaster aid: alters insurance demand and penetration

- Partnerships: lower tail risk, improve reputation

100% RBC, >97% health cover and $700bn exports shape Korea insurers

Regulatory capital rules (statutory risk‑based minimum 100%) and active FSS/FSC supervision raise compliance costs but stabilize the market. Korea’s National Health Insurance covers >97% of residents, and public social spending ~12.5% of GDP reduces some private demand. North Korea tensions (S. Korea defense spending $50.6bn in 2023) lift reinsurance costs; export volume ~$700bn (2024) sustains marine/cargo demand.

| Metric | Value |

|---|---|

| RBC minimum | 100% |

| National Health coverage | >97% |

| Exports (goods) | $700bn (2024) |

| Defense spend | $50.6bn (2023) |

| Insured nat cat losses | $120bn (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Hyundai Marine & Fire, with data-driven trends, region-specific regulatory context and forward-looking insights to help executives, consultants and investors identify threats, opportunities and actionable strategies.

A clean, summarized PESTLE of Hyundai Marine & Fire for easy reference in meetings, visually segmented by category, editable for regional or business-line notes, and concise enough to drop into presentations or share across teams for quick alignment on external risks and market positioning.

Economic factors

Interest rate cycle and investment returns

Non-life insurers like Hyundai Marine & Fire depend on float investment income; with the Fed funds rate at 5.25–5.50% and global 10‑yr yields near 4% in mid‑2025, recent hikes have boosted fixed‑income returns while cuts would compress earnings. Duration matching between assets and liabilities is critical for long‑term motor and casualty lines. Macroeconomic volatility has shifted allocations toward equities and alternatives, and investment results directly shape pricing discipline and growth appetite.

GDP growth and industrial output

Corporate insurance demand for Hyundai Marine & Fire closely follows activity in manufacturing, exports and services, and global GDP growth slowed to 3.0% in 2024 (IMF), tempering premium momentum. Strong capex cycles historically raise property, engineering and liability premiums; conversely slowdowns compress renewal rates and elevate corporate credit risk. Hyundai Marine's diversified book across marine, non-life and specialty lines helps buffer this cyclicality.

Inflation and claims severity

Rising medical, auto parts and construction costs — with industry estimates showing auto parts up ~10% and construction materials ~8% in 2023–24 — push loss severity across Hyundai Marine & Fire’s auto and property lines. Pricing and reinsurance must adjust (2024 reinsurance renewals saw low-single-digit to mid‑teens rate moves) or margins erode. Claims inflation often trails headline CPI by 1–3pts, requiring rigorous trend analytics, and policy terms and deductibles are being recalibrated to preserve profitability.

Employment and consumer spending

Employment trends and household income drive demand for Hyundai Marine & Fires long-term and auto policies: South Koreas unemployment remains low at around 3%, supporting premium persistency and cross-sell potential, while income strain raises lapse rates and fraud risk during downturns; flexible payment plans and targeted retention programs reduce churn.

- employment: ~3% unemployment

- impact: higher persistency, cross-sell

- risk: higher lapses/fraud in stress

- mitigation: flexible payments, retention

KRW exchange rate volatility

KRW exchange-rate swings (roughly 1,300–1,400 KRW/USD in 2024–mid‑2025) materially affect reinsurance premiums, overseas investments and USD/EUR‑denominated claims; a 5–10% won depreciation raises imported parts and repair costs, increasing auto claims inflation. Hedging policies and currency‑matched assets can reduce earnings volatility, and pricing must embed explicit FX sensitivities.

- Impact: reinsurance/claims FX exposure

- Driver: imported parts cost up with weaker won

- Mitigation: hedging and FX‑matched assets

- Recommendation: pricing to include FX stress (5–10% scenarios)

100% RBC, >97% health cover and $700bn exports shape Korea insurers

Higher global yields (US 10y ~4% mid‑2025; Fed funds 5.25–5.50%) bolstered Hyundai Marine & Fire’s investment income but cuts would compress margins; 2024 global GDP ~3.0% (IMF) slowed premium growth. KRW ~1,300–1,400/USD raises imported parts costs, adding 5–10% to claims inflation; domestic unemployment ~3% supports persistency.

| Metric | Value | Impact |

|---|---|---|

| Fed funds / US10y | 5.25–5.50% / ~4% | Investment income sensitivity |

| Global GDP 2024 | ~3.0% | Premium growth pressure |

| KRW/USD | 1,300–1,400 | Claims/import cost +5–10% |

Same Document Delivered

Hyundai Marine & Fire PESTLE Analysis

The preview shown here is the exact Hyundai Marine & Fire PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete Political, Economic, Social, Technological, Legal and Environmental assessment as displayed, with no placeholders or teasers. After checkout you’ll be able to download this same final file instantly.

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Hyundai Marine & Fire maps political, economic, social, technological, legal and environmental forces shaping the insurer’s strategy and risk profile. Packed with concise insights and real-world implications, it’s ideal for investors, advisors and strategists seeking a competitive edge. Purchase the full report to access the detailed breakdown, forecasts and ready-to-use recommendations.

Political factors

Regulatory oversight by FSC/FSS

South Korea’s Financial Services Commission and Financial Supervisory Service, established 1999 (FSS), set solvency, product and conduct rules, including a statutory risk-based capital minimum of 100% for insurers. Shifts in capital standards or reserve methodologies directly alter pricing and product mix, while close supervision raises compliance costs but underpins sector stability. Proactive engagement with regulators can shape rulemaking timelines and interpretations.

Government policy on social insurance

Public schemes such as Korea's National Health Insurance (covers over 97% of residents) and expanding pension/disaster relief programs (public social spending ~12.5% of GDP) reduce demand for some private long-term lines but leave gaps in accident, supplemental health and liability that Hyundai Marine & Fire can target. Post‑election policy shifts often reallocate subsidies, so insurers must realign product mix and pricing to evolving public‑private risk sharing.

Geopolitical tensions on the Korean Peninsula

Periodic North Korea risks elevate catastrophe, political-risk and supply-chain exposures for corporate clients, underlined by South Korea’s defense spending of about $50.6 billion in 2023 (SIPRI). Heightened tensions push reinsurers to demand larger capital buffers and higher premiums, increasing costs for Hyundai Marine & Fire while specialty-cover demand may grow but underwriting risk rises. Scenario planning and stress tests are critical for portfolio resilience.

Industrial policy and trade relations

Industrial policy and FTAs shape Hyundai Marine & Fire’s exposure: South Korea’s export orientation (roughly $700bn goods exports in 2024) drives demand for marine, cargo and trade-credit lines, while trade disputes or sanctions shift routes and increase claim frequency. Government support for EVs, semiconductors and shipbuilding (Korean yards held ~40% of global orderbook in 2024) reallocates commercial risk pools. Aligning underwriting capacity to favored sectors can unlock premium growth with targeted risk controls.

- FTA exposure: export-led premium opportunities

- Sanctions/trade disputes: higher route disruption claims

- Sector support: EVs/semiconductors/shipbuilding concentrate risk

- Strategy: capacity alignment + targeted controls = growth

Public disaster preparedness and subsidies

National disaster frameworks and mitigation funding shape catastrophe exposure and claims volatility; Swiss Re estimated insured natural catastrophe losses at about USD 120 billion in 2023. Government incentives for safety upgrades lower loss ratios over time—UNDRR finds each USD 1 invested in disaster risk reduction can save about USD 4 in future losses. Post-disaster aid can depress short-term insurance uptake while boosting reconstruction cover demand; partnerships on resiliency programs reduce tail risk and enhance Hyundai Marine & Fire’s brand.

- Policy environment: mitigation funding influences claims volatility

- Incentives: safety upgrades cut loss ratios (UNDRR 4:1 benefit)

- Post-disaster aid: alters insurance demand and penetration

- Partnerships: lower tail risk, improve reputation

100% RBC, >97% health cover and $700bn exports shape Korea insurers

Regulatory capital rules (statutory risk‑based minimum 100%) and active FSS/FSC supervision raise compliance costs but stabilize the market. Korea’s National Health Insurance covers >97% of residents, and public social spending ~12.5% of GDP reduces some private demand. North Korea tensions (S. Korea defense spending $50.6bn in 2023) lift reinsurance costs; export volume ~$700bn (2024) sustains marine/cargo demand.

| Metric | Value |

|---|---|

| RBC minimum | 100% |

| National Health coverage | >97% |

| Exports (goods) | $700bn (2024) |

| Defense spend | $50.6bn (2023) |

| Insured nat cat losses | $120bn (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Hyundai Marine & Fire, with data-driven trends, region-specific regulatory context and forward-looking insights to help executives, consultants and investors identify threats, opportunities and actionable strategies.

A clean, summarized PESTLE of Hyundai Marine & Fire for easy reference in meetings, visually segmented by category, editable for regional or business-line notes, and concise enough to drop into presentations or share across teams for quick alignment on external risks and market positioning.

Economic factors

Interest rate cycle and investment returns

Non-life insurers like Hyundai Marine & Fire depend on float investment income; with the Fed funds rate at 5.25–5.50% and global 10‑yr yields near 4% in mid‑2025, recent hikes have boosted fixed‑income returns while cuts would compress earnings. Duration matching between assets and liabilities is critical for long‑term motor and casualty lines. Macroeconomic volatility has shifted allocations toward equities and alternatives, and investment results directly shape pricing discipline and growth appetite.

GDP growth and industrial output

Corporate insurance demand for Hyundai Marine & Fire closely follows activity in manufacturing, exports and services, and global GDP growth slowed to 3.0% in 2024 (IMF), tempering premium momentum. Strong capex cycles historically raise property, engineering and liability premiums; conversely slowdowns compress renewal rates and elevate corporate credit risk. Hyundai Marine's diversified book across marine, non-life and specialty lines helps buffer this cyclicality.

Inflation and claims severity

Rising medical, auto parts and construction costs — with industry estimates showing auto parts up ~10% and construction materials ~8% in 2023–24 — push loss severity across Hyundai Marine & Fire’s auto and property lines. Pricing and reinsurance must adjust (2024 reinsurance renewals saw low-single-digit to mid‑teens rate moves) or margins erode. Claims inflation often trails headline CPI by 1–3pts, requiring rigorous trend analytics, and policy terms and deductibles are being recalibrated to preserve profitability.

Employment and consumer spending

Employment trends and household income drive demand for Hyundai Marine & Fires long-term and auto policies: South Koreas unemployment remains low at around 3%, supporting premium persistency and cross-sell potential, while income strain raises lapse rates and fraud risk during downturns; flexible payment plans and targeted retention programs reduce churn.

- employment: ~3% unemployment

- impact: higher persistency, cross-sell

- risk: higher lapses/fraud in stress

- mitigation: flexible payments, retention

KRW exchange rate volatility

KRW exchange-rate swings (roughly 1,300–1,400 KRW/USD in 2024–mid‑2025) materially affect reinsurance premiums, overseas investments and USD/EUR‑denominated claims; a 5–10% won depreciation raises imported parts and repair costs, increasing auto claims inflation. Hedging policies and currency‑matched assets can reduce earnings volatility, and pricing must embed explicit FX sensitivities.

- Impact: reinsurance/claims FX exposure

- Driver: imported parts cost up with weaker won

- Mitigation: hedging and FX‑matched assets

- Recommendation: pricing to include FX stress (5–10% scenarios)

100% RBC, >97% health cover and $700bn exports shape Korea insurers

Higher global yields (US 10y ~4% mid‑2025; Fed funds 5.25–5.50%) bolstered Hyundai Marine & Fire’s investment income but cuts would compress margins; 2024 global GDP ~3.0% (IMF) slowed premium growth. KRW ~1,300–1,400/USD raises imported parts costs, adding 5–10% to claims inflation; domestic unemployment ~3% supports persistency.

| Metric | Value | Impact |

|---|---|---|

| Fed funds / US10y | 5.25–5.50% / ~4% | Investment income sensitivity |

| Global GDP 2024 | ~3.0% | Premium growth pressure |

| KRW/USD | 1,300–1,400 | Claims/import cost +5–10% |

Same Document Delivered

Hyundai Marine & Fire PESTLE Analysis

The preview shown here is the exact Hyundai Marine & Fire PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete Political, Economic, Social, Technological, Legal and Environmental assessment as displayed, with no placeholders or teasers. After checkout you’ll be able to download this same final file instantly.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Hyundai Marine & Fire maps political, economic, social, technological, legal and environmental forces shaping the insurer’s strategy and risk profile. Packed with concise insights and real-world implications, it’s ideal for investors, advisors and strategists seeking a competitive edge. Purchase the full report to access the detailed breakdown, forecasts and ready-to-use recommendations.

Political factors

Regulatory oversight by FSC/FSS

South Korea’s Financial Services Commission and Financial Supervisory Service, established 1999 (FSS), set solvency, product and conduct rules, including a statutory risk-based capital minimum of 100% for insurers. Shifts in capital standards or reserve methodologies directly alter pricing and product mix, while close supervision raises compliance costs but underpins sector stability. Proactive engagement with regulators can shape rulemaking timelines and interpretations.

Government policy on social insurance

Public schemes such as Korea's National Health Insurance (covers over 97% of residents) and expanding pension/disaster relief programs (public social spending ~12.5% of GDP) reduce demand for some private long-term lines but leave gaps in accident, supplemental health and liability that Hyundai Marine & Fire can target. Post‑election policy shifts often reallocate subsidies, so insurers must realign product mix and pricing to evolving public‑private risk sharing.

Geopolitical tensions on the Korean Peninsula

Periodic North Korea risks elevate catastrophe, political-risk and supply-chain exposures for corporate clients, underlined by South Korea’s defense spending of about $50.6 billion in 2023 (SIPRI). Heightened tensions push reinsurers to demand larger capital buffers and higher premiums, increasing costs for Hyundai Marine & Fire while specialty-cover demand may grow but underwriting risk rises. Scenario planning and stress tests are critical for portfolio resilience.

Industrial policy and trade relations

Industrial policy and FTAs shape Hyundai Marine & Fire’s exposure: South Korea’s export orientation (roughly $700bn goods exports in 2024) drives demand for marine, cargo and trade-credit lines, while trade disputes or sanctions shift routes and increase claim frequency. Government support for EVs, semiconductors and shipbuilding (Korean yards held ~40% of global orderbook in 2024) reallocates commercial risk pools. Aligning underwriting capacity to favored sectors can unlock premium growth with targeted risk controls.

- FTA exposure: export-led premium opportunities

- Sanctions/trade disputes: higher route disruption claims

- Sector support: EVs/semiconductors/shipbuilding concentrate risk

- Strategy: capacity alignment + targeted controls = growth

Public disaster preparedness and subsidies

National disaster frameworks and mitigation funding shape catastrophe exposure and claims volatility; Swiss Re estimated insured natural catastrophe losses at about USD 120 billion in 2023. Government incentives for safety upgrades lower loss ratios over time—UNDRR finds each USD 1 invested in disaster risk reduction can save about USD 4 in future losses. Post-disaster aid can depress short-term insurance uptake while boosting reconstruction cover demand; partnerships on resiliency programs reduce tail risk and enhance Hyundai Marine & Fire’s brand.

- Policy environment: mitigation funding influences claims volatility

- Incentives: safety upgrades cut loss ratios (UNDRR 4:1 benefit)

- Post-disaster aid: alters insurance demand and penetration

- Partnerships: lower tail risk, improve reputation

100% RBC, >97% health cover and $700bn exports shape Korea insurers

Regulatory capital rules (statutory risk‑based minimum 100%) and active FSS/FSC supervision raise compliance costs but stabilize the market. Korea’s National Health Insurance covers >97% of residents, and public social spending ~12.5% of GDP reduces some private demand. North Korea tensions (S. Korea defense spending $50.6bn in 2023) lift reinsurance costs; export volume ~$700bn (2024) sustains marine/cargo demand.

| Metric | Value |

|---|---|

| RBC minimum | 100% |

| National Health coverage | >97% |

| Exports (goods) | $700bn (2024) |

| Defense spend | $50.6bn (2023) |

| Insured nat cat losses | $120bn (2023) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Hyundai Marine & Fire, with data-driven trends, region-specific regulatory context and forward-looking insights to help executives, consultants and investors identify threats, opportunities and actionable strategies.

A clean, summarized PESTLE of Hyundai Marine & Fire for easy reference in meetings, visually segmented by category, editable for regional or business-line notes, and concise enough to drop into presentations or share across teams for quick alignment on external risks and market positioning.

Economic factors

Interest rate cycle and investment returns

Non-life insurers like Hyundai Marine & Fire depend on float investment income; with the Fed funds rate at 5.25–5.50% and global 10‑yr yields near 4% in mid‑2025, recent hikes have boosted fixed‑income returns while cuts would compress earnings. Duration matching between assets and liabilities is critical for long‑term motor and casualty lines. Macroeconomic volatility has shifted allocations toward equities and alternatives, and investment results directly shape pricing discipline and growth appetite.

GDP growth and industrial output

Corporate insurance demand for Hyundai Marine & Fire closely follows activity in manufacturing, exports and services, and global GDP growth slowed to 3.0% in 2024 (IMF), tempering premium momentum. Strong capex cycles historically raise property, engineering and liability premiums; conversely slowdowns compress renewal rates and elevate corporate credit risk. Hyundai Marine's diversified book across marine, non-life and specialty lines helps buffer this cyclicality.

Inflation and claims severity

Rising medical, auto parts and construction costs — with industry estimates showing auto parts up ~10% and construction materials ~8% in 2023–24 — push loss severity across Hyundai Marine & Fire’s auto and property lines. Pricing and reinsurance must adjust (2024 reinsurance renewals saw low-single-digit to mid‑teens rate moves) or margins erode. Claims inflation often trails headline CPI by 1–3pts, requiring rigorous trend analytics, and policy terms and deductibles are being recalibrated to preserve profitability.

Employment and consumer spending

Employment trends and household income drive demand for Hyundai Marine & Fires long-term and auto policies: South Koreas unemployment remains low at around 3%, supporting premium persistency and cross-sell potential, while income strain raises lapse rates and fraud risk during downturns; flexible payment plans and targeted retention programs reduce churn.

- employment: ~3% unemployment

- impact: higher persistency, cross-sell

- risk: higher lapses/fraud in stress

- mitigation: flexible payments, retention

KRW exchange rate volatility

KRW exchange-rate swings (roughly 1,300–1,400 KRW/USD in 2024–mid‑2025) materially affect reinsurance premiums, overseas investments and USD/EUR‑denominated claims; a 5–10% won depreciation raises imported parts and repair costs, increasing auto claims inflation. Hedging policies and currency‑matched assets can reduce earnings volatility, and pricing must embed explicit FX sensitivities.

- Impact: reinsurance/claims FX exposure

- Driver: imported parts cost up with weaker won

- Mitigation: hedging and FX‑matched assets

- Recommendation: pricing to include FX stress (5–10% scenarios)

100% RBC, >97% health cover and $700bn exports shape Korea insurers

Higher global yields (US 10y ~4% mid‑2025; Fed funds 5.25–5.50%) bolstered Hyundai Marine & Fire’s investment income but cuts would compress margins; 2024 global GDP ~3.0% (IMF) slowed premium growth. KRW ~1,300–1,400/USD raises imported parts costs, adding 5–10% to claims inflation; domestic unemployment ~3% supports persistency.

| Metric | Value | Impact |

|---|---|---|

| Fed funds / US10y | 5.25–5.50% / ~4% | Investment income sensitivity |

| Global GDP 2024 | ~3.0% | Premium growth pressure |

| KRW/USD | 1,300–1,400 | Claims/import cost +5–10% |

Same Document Delivered

Hyundai Marine & Fire PESTLE Analysis

The preview shown here is the exact Hyundai Marine & Fire PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the complete Political, Economic, Social, Technological, Legal and Environmental assessment as displayed, with no placeholders or teasers. After checkout you’ll be able to download this same final file instantly.