Hyundai Motor PESTLE Analysis

Your Competitive Advantage Starts with This Report

Our PESTLE analysis reveals how regulatory shifts, supply-chain dynamics, economic cycles and rapid tech innovation are reshaping Hyundai Motor’s strategic landscape. You’ll get concise insights into risks and growth levers across markets and mobility trends. Ideal for investors and strategists seeking actionable intelligence. Purchase the full PESTLE to access the complete, ready-to-use report.

Political factors

EV incentives and industrial policy

US IRA credits up to $7,500, EU purchase bonuses of several thousand euros, Korea’s direct EV subsidies and tax breaks, and India’s FAME/PLI schemes materially steer EV affordability and Hyundai’s model mix. Local-content rules and income caps can re-rank eligible Hyundai models, so localization and compliant sourcing protect incentive access and margins. Monitoring planned phase-outs and election cycles is critical for pricing and capacity planning.

Trade tariffs and geopolitical tensions

Tariff regimes on vehicles, batteries and components directly affect Hyundai’s landed costs and pricing as US EV rules (IRA) tie subsidies to domestic content and a $7,500 tax credit, while the EU’s 2023 provisional anti-subsidy duties on Chinese EVs reached up to 38.1%. US–China tensions and EU trade probes force export-strategy shifts. Hyundai’s diversified footprint across Korea, US, Europe, India and ASEAN hedges risk. Proactive lobbying and rerouting suppliers sustain competitiveness.

Local manufacturing and content mandates

Policies like Buy America and the EU battery passport force Hyundai to site plants and source locally to qualify for up to $7,500 IRA EV tax credits; battery-component thresholds (roughly 50%) and critical-mineral rules (starting ~40%) are driving changes. Hyundai’s ~$7.4bn U.S. EV/battery investment and partnerships with SK On and miners aim to deepen cell, cathode and electronics regional supply. Non-compliance risks losing incentives and causing volume shortfalls.

Infrastructure funding priorities

Political stability and policy continuity

Election outcomes and coalition shifts can reverse or reinforce auto emissions targets, affecting Hyundai’s regional product and investment decisions; markets with stable policy — e.g., EU Fit for 55 (55% GHG cut by 2030) and EU 2035 zero-emission new car mandate — enable long-cycle capex.

Volatile regimes raise risk premiums and delay fleet electrification commitments, so scenario planning aligns Hyundai’s product cadence with policy durability.

- policy: EU Fit for 55 — 55% by 2030

- mandate: EU 2035 zero-emission cars

- risk: electoral volatility increases delay/default risk

Global incentives, tariffs reshape automaker EV mix; US $7,500, EU 38.1%

Global incentives (US IRA $7,500; EU purchase bonuses; Korea/India subsidies) and tariffs (EU anti-subsidy duties up to 38.1%) materially reshape Hyundai’s model mix, localization and sourcing. US $7.4bn Hyundai U.S. EV/battery investment and public charging funding (US 7.5B; China >2.4M chargers 2023) drive siting and rollout timing. Election cycles and phase-outs raise planning risk.

| Item | Value |

|---|---|

| US EV tax credit | $7,500 |

| Hyundai U.S. EV investment | $7.4bn |

| US charger funding | $7.5B |

| China public chargers (2023) | >2.4M |

| EU anti-subsidy duty | up to 38.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect Hyundai Motor across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights; designed for executives and investors to identify opportunities, risks and strategic actions tailored to the global auto market.

A concise, visually segmented PESTLE summary for Hyundai Motor that relieves the pain of complex external-risk analysis by fitting directly into slides, strategy packs, or client reports, while remaining editable for region- or business-specific notes to speed alignment across teams.

Economic factors

Interest rates and consumer financing

Higher interest rates (US new‑vehicle loan APR averaged about 7–9% in 2024) elevate monthly payments, squeezing affordability and prompting down‑trading from premium models to entry EVs and SUVs. Even modest rate cuts have historically revived volume quickly, benefiting mass‑market EVs and compact SUVs. Hyundai’s captive finance arm cushions rate swings with targeted promotions and flexible terms. Strong credit risk management remains essential during slowdowns.

Currency volatility (KRW, USD, EUR, CNY)

Exchange-rate swings alter export competitiveness and margins; USD/KRW ranged c.1,250–1,400 in 2023–2024 while EUR/USD sat around 1.05–1.10 and CNY/USD near 7.1–7.3, shifting Hyundai’s realized prices in key markets. Natural hedging via regional production in the US, Czech Republic, India and China and localized sourcing reduces translation and transaction exposure. Financial hedging using forwards and options stabilizes cash flows but raises financing costs. Pricing agility and optioned features enable Hyundai to pass through or absorb FX shocks.

Commodity and battery material costs

Lithium, nickel, cobalt, graphite and steel prices materially drive Hyundai’s EV BOM and margins; battery pack average fell to about 132 USD/kWh in 2023 (BNEF), but raw-material volatility still pressures profitability. Long-term offtakes and growing recycling capacity reduce exposure to spot swings. Shift to LFP — >50% of Chinese EV batteries in 2024 (SNE Research) — brings cost stability and broad segment coverage, while cost pass-through hinges on Hyundai’s brand power and competitive intensity.

Global supply chain resilience

Port congestion and Red Sea disruptions since late 2023 have forced rerouting and higher insurance costs, while semiconductor cycles continue to cause intermittent output swings for Hyundai; dual-sourcing and regional inventory buffers have improved production continuity. Platform commonality reduces complexity and safety stock needs, and digital visibility shortens response times to shocks.

- Port congestion: higher dwell times

- Red Sea: rerouting/escorts since 2023

- Semiconductors: cyclical supply impacts

- Mitigation: dual-sourcing, regional buffers

- Efficiency: platform commonality, digital visibility

Demand cycles and market mix

Demand growth in India and ASEAN supports volume—IMF 2024 GDP: India ~6.8%, ASEAN-5 ~4.5%—while mature markets are replacement-led; fleet and rideshare channels smooth sales volatility but squeeze margins. EV adoption varies sharply (China NEV ~60% of new sales 2024, EU ~25%, India <5%), so Hyundai’s ICE/HEV/EV/FCEV mix hedges cyclical risk.

- India/ASEAN growth: +6.8% / +4.5% (IMF 2024)

- Replacement vs volume: mature vs emerging

- Fleet/rideshare: volatility down, margins down

- EV mix: China 60%, EU 25%, India <5% (2024)

- Portfolio balance mitigates cycles

Global incentives, tariffs reshape automaker EV mix; US $7,500, EU 38.1%

Higher US new‑vehicle loan APR ~7–9% (2024) squeezes affordability; Hyundai Finance eases via targeted promos. USD/KRW ~1,250–1,400 (2023–24) shifts margins; regional plants provide natural hedge. Battery pack ~$132/kWh (2023) and China LFP >50% (2024) lower EV BOM volatility; India GDP ~6.8% (2024) underpins volume growth.

| Metric | Value | Impact |

|---|---|---|

| US loan APR | 7–9% | Affordability |

| USD/KRW | 1,250–1,400 | Margins |

| Battery cost | $132/kWh | EV BOM |

| India GDP | ~6.8% | Demand |

What You See Is What You Get

Hyundai Motor PESTLE Analysis

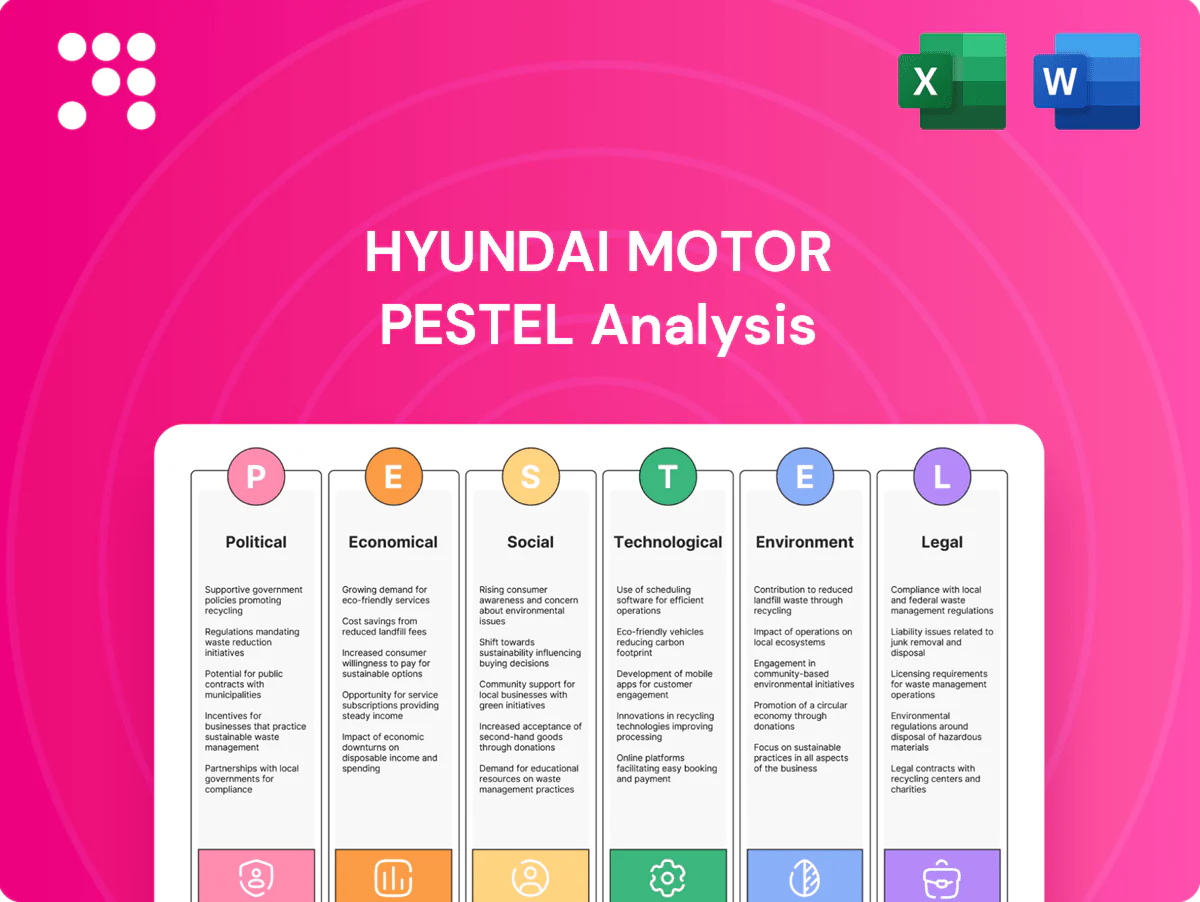

The preview shown here is the exact Hyundai Motor PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It includes comprehensive Political, Economic, Social, Technological, Legal, and Environmental evaluations as displayed. No placeholders or teasers—what you see is the final downloadable file. Purchase delivers this same complete document instantly.

Your Competitive Advantage Starts with This Report

Our PESTLE analysis reveals how regulatory shifts, supply-chain dynamics, economic cycles and rapid tech innovation are reshaping Hyundai Motor’s strategic landscape. You’ll get concise insights into risks and growth levers across markets and mobility trends. Ideal for investors and strategists seeking actionable intelligence. Purchase the full PESTLE to access the complete, ready-to-use report.

Political factors

EV incentives and industrial policy

US IRA credits up to $7,500, EU purchase bonuses of several thousand euros, Korea’s direct EV subsidies and tax breaks, and India’s FAME/PLI schemes materially steer EV affordability and Hyundai’s model mix. Local-content rules and income caps can re-rank eligible Hyundai models, so localization and compliant sourcing protect incentive access and margins. Monitoring planned phase-outs and election cycles is critical for pricing and capacity planning.

Trade tariffs and geopolitical tensions

Tariff regimes on vehicles, batteries and components directly affect Hyundai’s landed costs and pricing as US EV rules (IRA) tie subsidies to domestic content and a $7,500 tax credit, while the EU’s 2023 provisional anti-subsidy duties on Chinese EVs reached up to 38.1%. US–China tensions and EU trade probes force export-strategy shifts. Hyundai’s diversified footprint across Korea, US, Europe, India and ASEAN hedges risk. Proactive lobbying and rerouting suppliers sustain competitiveness.

Local manufacturing and content mandates

Policies like Buy America and the EU battery passport force Hyundai to site plants and source locally to qualify for up to $7,500 IRA EV tax credits; battery-component thresholds (roughly 50%) and critical-mineral rules (starting ~40%) are driving changes. Hyundai’s ~$7.4bn U.S. EV/battery investment and partnerships with SK On and miners aim to deepen cell, cathode and electronics regional supply. Non-compliance risks losing incentives and causing volume shortfalls.

Infrastructure funding priorities

Political stability and policy continuity

Election outcomes and coalition shifts can reverse or reinforce auto emissions targets, affecting Hyundai’s regional product and investment decisions; markets with stable policy — e.g., EU Fit for 55 (55% GHG cut by 2030) and EU 2035 zero-emission new car mandate — enable long-cycle capex.

Volatile regimes raise risk premiums and delay fleet electrification commitments, so scenario planning aligns Hyundai’s product cadence with policy durability.

- policy: EU Fit for 55 — 55% by 2030

- mandate: EU 2035 zero-emission cars

- risk: electoral volatility increases delay/default risk

Global incentives, tariffs reshape automaker EV mix; US $7,500, EU 38.1%

Global incentives (US IRA $7,500; EU purchase bonuses; Korea/India subsidies) and tariffs (EU anti-subsidy duties up to 38.1%) materially reshape Hyundai’s model mix, localization and sourcing. US $7.4bn Hyundai U.S. EV/battery investment and public charging funding (US 7.5B; China >2.4M chargers 2023) drive siting and rollout timing. Election cycles and phase-outs raise planning risk.

| Item | Value |

|---|---|

| US EV tax credit | $7,500 |

| Hyundai U.S. EV investment | $7.4bn |

| US charger funding | $7.5B |

| China public chargers (2023) | >2.4M |

| EU anti-subsidy duty | up to 38.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect Hyundai Motor across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights; designed for executives and investors to identify opportunities, risks and strategic actions tailored to the global auto market.

A concise, visually segmented PESTLE summary for Hyundai Motor that relieves the pain of complex external-risk analysis by fitting directly into slides, strategy packs, or client reports, while remaining editable for region- or business-specific notes to speed alignment across teams.

Economic factors

Interest rates and consumer financing

Higher interest rates (US new‑vehicle loan APR averaged about 7–9% in 2024) elevate monthly payments, squeezing affordability and prompting down‑trading from premium models to entry EVs and SUVs. Even modest rate cuts have historically revived volume quickly, benefiting mass‑market EVs and compact SUVs. Hyundai’s captive finance arm cushions rate swings with targeted promotions and flexible terms. Strong credit risk management remains essential during slowdowns.

Currency volatility (KRW, USD, EUR, CNY)

Exchange-rate swings alter export competitiveness and margins; USD/KRW ranged c.1,250–1,400 in 2023–2024 while EUR/USD sat around 1.05–1.10 and CNY/USD near 7.1–7.3, shifting Hyundai’s realized prices in key markets. Natural hedging via regional production in the US, Czech Republic, India and China and localized sourcing reduces translation and transaction exposure. Financial hedging using forwards and options stabilizes cash flows but raises financing costs. Pricing agility and optioned features enable Hyundai to pass through or absorb FX shocks.

Commodity and battery material costs

Lithium, nickel, cobalt, graphite and steel prices materially drive Hyundai’s EV BOM and margins; battery pack average fell to about 132 USD/kWh in 2023 (BNEF), but raw-material volatility still pressures profitability. Long-term offtakes and growing recycling capacity reduce exposure to spot swings. Shift to LFP — >50% of Chinese EV batteries in 2024 (SNE Research) — brings cost stability and broad segment coverage, while cost pass-through hinges on Hyundai’s brand power and competitive intensity.

Global supply chain resilience

Port congestion and Red Sea disruptions since late 2023 have forced rerouting and higher insurance costs, while semiconductor cycles continue to cause intermittent output swings for Hyundai; dual-sourcing and regional inventory buffers have improved production continuity. Platform commonality reduces complexity and safety stock needs, and digital visibility shortens response times to shocks.

- Port congestion: higher dwell times

- Red Sea: rerouting/escorts since 2023

- Semiconductors: cyclical supply impacts

- Mitigation: dual-sourcing, regional buffers

- Efficiency: platform commonality, digital visibility

Demand cycles and market mix

Demand growth in India and ASEAN supports volume—IMF 2024 GDP: India ~6.8%, ASEAN-5 ~4.5%—while mature markets are replacement-led; fleet and rideshare channels smooth sales volatility but squeeze margins. EV adoption varies sharply (China NEV ~60% of new sales 2024, EU ~25%, India <5%), so Hyundai’s ICE/HEV/EV/FCEV mix hedges cyclical risk.

- India/ASEAN growth: +6.8% / +4.5% (IMF 2024)

- Replacement vs volume: mature vs emerging

- Fleet/rideshare: volatility down, margins down

- EV mix: China 60%, EU 25%, India <5% (2024)

- Portfolio balance mitigates cycles

Global incentives, tariffs reshape automaker EV mix; US $7,500, EU 38.1%

Higher US new‑vehicle loan APR ~7–9% (2024) squeezes affordability; Hyundai Finance eases via targeted promos. USD/KRW ~1,250–1,400 (2023–24) shifts margins; regional plants provide natural hedge. Battery pack ~$132/kWh (2023) and China LFP >50% (2024) lower EV BOM volatility; India GDP ~6.8% (2024) underpins volume growth.

| Metric | Value | Impact |

|---|---|---|

| US loan APR | 7–9% | Affordability |

| USD/KRW | 1,250–1,400 | Margins |

| Battery cost | $132/kWh | EV BOM |

| India GDP | ~6.8% | Demand |

What You See Is What You Get

Hyundai Motor PESTLE Analysis

The preview shown here is the exact Hyundai Motor PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It includes comprehensive Political, Economic, Social, Technological, Legal, and Environmental evaluations as displayed. No placeholders or teasers—what you see is the final downloadable file. Purchase delivers this same complete document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Our PESTLE analysis reveals how regulatory shifts, supply-chain dynamics, economic cycles and rapid tech innovation are reshaping Hyundai Motor’s strategic landscape. You’ll get concise insights into risks and growth levers across markets and mobility trends. Ideal for investors and strategists seeking actionable intelligence. Purchase the full PESTLE to access the complete, ready-to-use report.

Political factors

EV incentives and industrial policy

US IRA credits up to $7,500, EU purchase bonuses of several thousand euros, Korea’s direct EV subsidies and tax breaks, and India’s FAME/PLI schemes materially steer EV affordability and Hyundai’s model mix. Local-content rules and income caps can re-rank eligible Hyundai models, so localization and compliant sourcing protect incentive access and margins. Monitoring planned phase-outs and election cycles is critical for pricing and capacity planning.

Trade tariffs and geopolitical tensions

Tariff regimes on vehicles, batteries and components directly affect Hyundai’s landed costs and pricing as US EV rules (IRA) tie subsidies to domestic content and a $7,500 tax credit, while the EU’s 2023 provisional anti-subsidy duties on Chinese EVs reached up to 38.1%. US–China tensions and EU trade probes force export-strategy shifts. Hyundai’s diversified footprint across Korea, US, Europe, India and ASEAN hedges risk. Proactive lobbying and rerouting suppliers sustain competitiveness.

Local manufacturing and content mandates

Policies like Buy America and the EU battery passport force Hyundai to site plants and source locally to qualify for up to $7,500 IRA EV tax credits; battery-component thresholds (roughly 50%) and critical-mineral rules (starting ~40%) are driving changes. Hyundai’s ~$7.4bn U.S. EV/battery investment and partnerships with SK On and miners aim to deepen cell, cathode and electronics regional supply. Non-compliance risks losing incentives and causing volume shortfalls.

Infrastructure funding priorities

Political stability and policy continuity

Election outcomes and coalition shifts can reverse or reinforce auto emissions targets, affecting Hyundai’s regional product and investment decisions; markets with stable policy — e.g., EU Fit for 55 (55% GHG cut by 2030) and EU 2035 zero-emission new car mandate — enable long-cycle capex.

Volatile regimes raise risk premiums and delay fleet electrification commitments, so scenario planning aligns Hyundai’s product cadence with policy durability.

- policy: EU Fit for 55 — 55% by 2030

- mandate: EU 2035 zero-emission cars

- risk: electoral volatility increases delay/default risk

Global incentives, tariffs reshape automaker EV mix; US $7,500, EU 38.1%

Global incentives (US IRA $7,500; EU purchase bonuses; Korea/India subsidies) and tariffs (EU anti-subsidy duties up to 38.1%) materially reshape Hyundai’s model mix, localization and sourcing. US $7.4bn Hyundai U.S. EV/battery investment and public charging funding (US 7.5B; China >2.4M chargers 2023) drive siting and rollout timing. Election cycles and phase-outs raise planning risk.

| Item | Value |

|---|---|

| US EV tax credit | $7,500 |

| Hyundai U.S. EV investment | $7.4bn |

| US charger funding | $7.5B |

| China public chargers (2023) | >2.4M |

| EU anti-subsidy duty | up to 38.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect Hyundai Motor across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights; designed for executives and investors to identify opportunities, risks and strategic actions tailored to the global auto market.

A concise, visually segmented PESTLE summary for Hyundai Motor that relieves the pain of complex external-risk analysis by fitting directly into slides, strategy packs, or client reports, while remaining editable for region- or business-specific notes to speed alignment across teams.

Economic factors

Interest rates and consumer financing

Higher interest rates (US new‑vehicle loan APR averaged about 7–9% in 2024) elevate monthly payments, squeezing affordability and prompting down‑trading from premium models to entry EVs and SUVs. Even modest rate cuts have historically revived volume quickly, benefiting mass‑market EVs and compact SUVs. Hyundai’s captive finance arm cushions rate swings with targeted promotions and flexible terms. Strong credit risk management remains essential during slowdowns.

Currency volatility (KRW, USD, EUR, CNY)

Exchange-rate swings alter export competitiveness and margins; USD/KRW ranged c.1,250–1,400 in 2023–2024 while EUR/USD sat around 1.05–1.10 and CNY/USD near 7.1–7.3, shifting Hyundai’s realized prices in key markets. Natural hedging via regional production in the US, Czech Republic, India and China and localized sourcing reduces translation and transaction exposure. Financial hedging using forwards and options stabilizes cash flows but raises financing costs. Pricing agility and optioned features enable Hyundai to pass through or absorb FX shocks.

Commodity and battery material costs

Lithium, nickel, cobalt, graphite and steel prices materially drive Hyundai’s EV BOM and margins; battery pack average fell to about 132 USD/kWh in 2023 (BNEF), but raw-material volatility still pressures profitability. Long-term offtakes and growing recycling capacity reduce exposure to spot swings. Shift to LFP — >50% of Chinese EV batteries in 2024 (SNE Research) — brings cost stability and broad segment coverage, while cost pass-through hinges on Hyundai’s brand power and competitive intensity.

Global supply chain resilience

Port congestion and Red Sea disruptions since late 2023 have forced rerouting and higher insurance costs, while semiconductor cycles continue to cause intermittent output swings for Hyundai; dual-sourcing and regional inventory buffers have improved production continuity. Platform commonality reduces complexity and safety stock needs, and digital visibility shortens response times to shocks.

- Port congestion: higher dwell times

- Red Sea: rerouting/escorts since 2023

- Semiconductors: cyclical supply impacts

- Mitigation: dual-sourcing, regional buffers

- Efficiency: platform commonality, digital visibility

Demand cycles and market mix

Demand growth in India and ASEAN supports volume—IMF 2024 GDP: India ~6.8%, ASEAN-5 ~4.5%—while mature markets are replacement-led; fleet and rideshare channels smooth sales volatility but squeeze margins. EV adoption varies sharply (China NEV ~60% of new sales 2024, EU ~25%, India <5%), so Hyundai’s ICE/HEV/EV/FCEV mix hedges cyclical risk.

- India/ASEAN growth: +6.8% / +4.5% (IMF 2024)

- Replacement vs volume: mature vs emerging

- Fleet/rideshare: volatility down, margins down

- EV mix: China 60%, EU 25%, India <5% (2024)

- Portfolio balance mitigates cycles

Global incentives, tariffs reshape automaker EV mix; US $7,500, EU 38.1%

Higher US new‑vehicle loan APR ~7–9% (2024) squeezes affordability; Hyundai Finance eases via targeted promos. USD/KRW ~1,250–1,400 (2023–24) shifts margins; regional plants provide natural hedge. Battery pack ~$132/kWh (2023) and China LFP >50% (2024) lower EV BOM volatility; India GDP ~6.8% (2024) underpins volume growth.

| Metric | Value | Impact |

|---|---|---|

| US loan APR | 7–9% | Affordability |

| USD/KRW | 1,250–1,400 | Margins |

| Battery cost | $132/kWh | EV BOM |

| India GDP | ~6.8% | Demand |

What You See Is What You Get

Hyundai Motor PESTLE Analysis

The preview shown here is the exact Hyundai Motor PESTLE analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It includes comprehensive Political, Economic, Social, Technological, Legal, and Environmental evaluations as displayed. No placeholders or teasers—what you see is the final downloadable file. Purchase delivers this same complete document instantly.