International Airlines Business Model Canvas

Explore a Global Airline Business Model Canvas: customer segments, revenue & costs

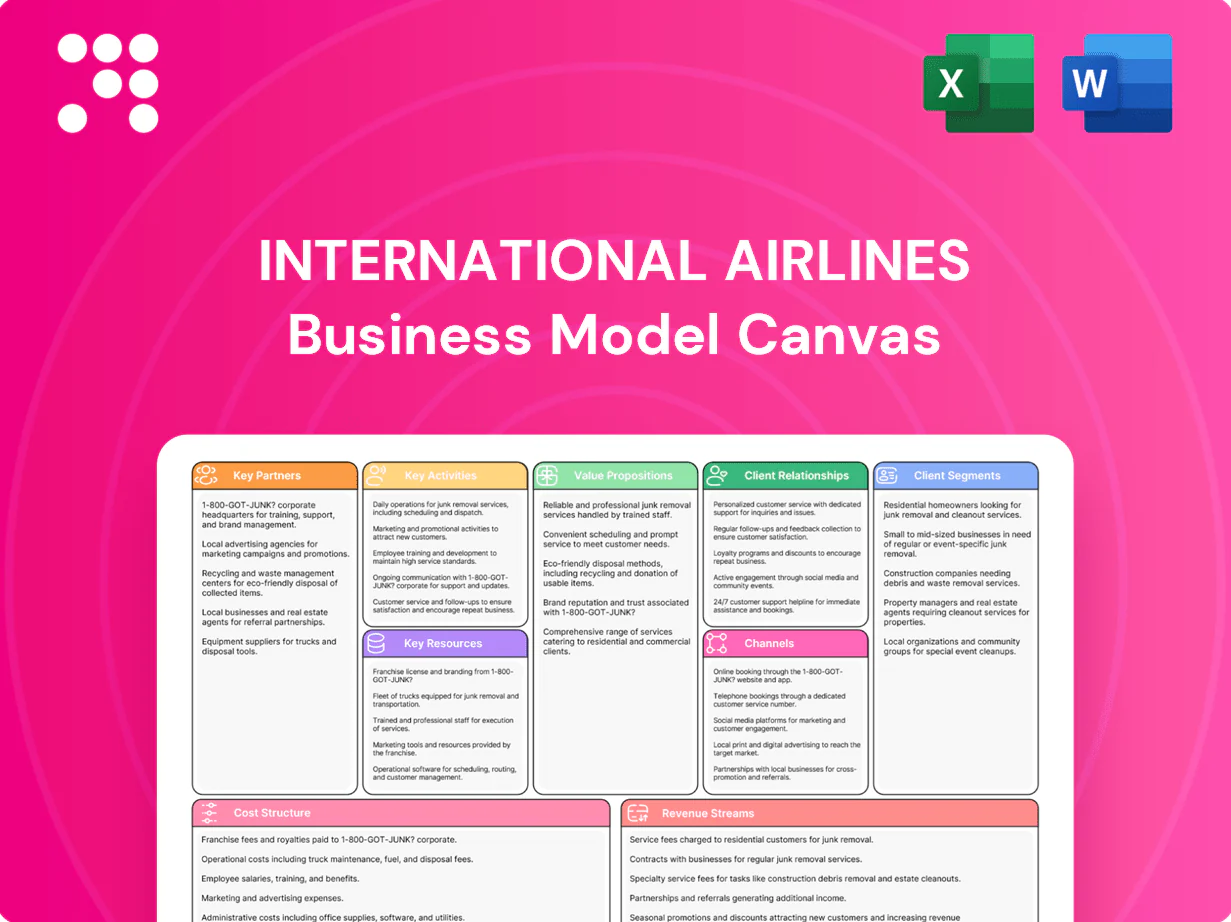

Explore International Airlines’ Business Model Canvas to see how it connects customer segments, value propositions, revenue streams and cost structure. This concise snapshot reveals key partnerships and operational levers. Ideal for investors, consultants, and strategists seeking actionable insights. Purchase the full Word/Excel canvas for a section-by-section breakdown.

Partnerships

Aircraft and engine manufacturers

Partnerships with Airbus, Boeing and engine OEMs such as Rolls-Royce and GE secure fleet availability, performance and OEM support; multi-year purchase agreements for hundreds of aircraft lower unit costs and enable fleet commonality and training synergies. OEM maintenance programs and mid-life upgrades sustain reliability and fuel efficiency, while joint R&D in 2024 accelerated SAF-readiness and next-gen cabin innovations.

Alliances, codeshare, and interline partners

IAG airlines leverage oneworld and bilateral codeshares to extend network reach, tapping oneworld’s network of over 1,000 destinations in more than 170 territories (2024) to offer seamless itineraries and reciprocal frequent‑flyer benefits that boost appeal to global travelers. Shared lounges and coordinated schedules improve connectivity and transfer times, while partners smooth seasonal demand swings and help optimize aircraft utilization across the group.

Airports, ground handlers, and catering providers

Hubs such as LHR, MAD, DUB, and BCN require deep coordination for slots and turnarounds; LHR is subject to a 480,000 annual slot cap, forcing precise scheduling and partner alignment.

Ground handling and catering partners drive punctuality and service consistency, and joint process improvements reduce delays and operational costs.

Premium lounge partners enhance customer experience and support ancillary revenue through upsell and retention opportunities.

Distribution partners: GDS, OTAs, and TMCs

Distribution partners—GDS, OTAs and TMCs—expand market reach across leisure and corporate segments, with OTAs handling about half of online bookings and corporate travel typically contributing 10–20% of airline revenue; corporate negotiated rates and growing NDC connectivity (adopted by hundreds of carriers by 2024) give airlines tighter offer control. Data-sharing with partners refines merchandising and ancillaries, while co-marketing drives incremental bookings and higher yield.

- GDS/OTAs/TMCs: market reach

- Corporate rates + NDC: offer control

- Data-sharing: better ancillaries

- Co-marketing: incremental bookings

Fuel, SAF suppliers, and financial partners

Strategic fuel hedgers and SAF producers support cost stability and decarbonization, with SAF supply still nascent at roughly 0.3% of global jet fuel demand in 2024, so multi-year offtakes secure future volumes and pricing. Banks, lessors, and ECAs provide liquidity and leases—lessors control about 50% of the global commercial fleet—while risk partners manage FX, interest rate, and commodity exposures to protect margins.

- SAF 2024 share ≈0.3%

- Lessors ≈50% of fleet

- Multi-year SAF offtakes lock supply

- Risk partners hedge FX, rates, commodities

Partnerships secure fleet, fuel and network access, boosting yields and ancillaries

Key partnerships secure fleet, cost and fuel stability (OEMs, lessors, banks), expand network and yield (oneworld, codeshares, GDS/OTAs, NDC) and improve operations and experience (ground handlers, caterers, lounges, SAF offtakes, hedgers). Coordination at constrained hubs (LHR slots) and data-sharing with distribution partners drives higher ancillaries and utilization.

| Partner | Role | 2024 metric |

|---|---|---|

| oneworld | Network | 1,000+ destinations, 170 territories |

| SAF suppliers | Decarbonize | ≈0.3% jet fuel |

| Lessors | Fleet finance | ≈50% global fleet |

| LHR | Hub constraint | 480,000 slot cap |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to international airlines, covering all 9 BMC blocks with detailed customer segments, channels, value propositions, revenue streams, cost structure, key activities, partners and regulatory considerations. Ideal for presentations, investor discussions and strategic decision-making, it includes competitive advantages and a linked SWOT to validate business plans using real-world operational insights.

High-level view of an international airline’s business model with editable cells to streamline route planning, fleet utilization and revenue streams—saves hours reconciling disparate data. Great for quick boardroom reviews, comparing carriers side-by-side, and adapting strategy during regulatory or market shocks.

Activities

Network and schedule optimization

IAG plans routes across 80+ long-haul and 200+ short-haul destinations to maximize connectivity and yields, leveraging hubs at London Heathrow, Madrid and Barcelona. Rigorous slot management and hub banking at Heathrow and Madrid smooth transfer flows and protect peak-hour connectivity. Seasonal and event-driven capacity shifts (summer peaks, major events) adjust frequencies and gauge to capture demand spikes. Ongoing competitive monitoring informs frequency and aircraft-gauge decisions.

Flight operations and safety management

Daily flight operations prioritize on-time performance (OTP targets often above 80%) and strict regulatory compliance; airlines coordinate crewing, ATC slots and maintenance to meet schedules. Safety management systems, including IATA IOSA (over 400 airlines enrolled), and recurrent training underpin reliability. Dedicated irregular-ops teams focus on rapid recovery to limit customer disruption. Continuous improvement programs target 1–3% annual fuel-efficiency gains and shorter turnarounds (30–90 minutes).

Revenue management and pricing

Dynamic pricing allocates seats across fare classes to maximize load factor and yield, supporting a global passenger load factor around 80.6% in 2023. Ancillary bundling—bag fees, seat selection and bundles—now contributes a double-digit share of airline revenues and boosted margins industrywide. Corporate contracting and group sales, with business travel near 80% of 2019 levels in 2023, balance the mix. Data science underpins demand forecasting and rapid competitive response.

Fleet and MRO lifecycle management

- Fleet size 2024 ~26,000 jets

- Leased share ~40%

- Cabin refresh 5–10 yr

- MRO market focus on engine/airframe reliability

Loyalty, digital, and customer experience

Avios powers cross-brand loyalty engagement and monetization, with the Avios currency serving customers across airlines, hotels and retail (30m+ members reported by 2024). Apps, websites and NDC enable personalized offers and self-service, driving higher ancillary conversion and mobile bookings. Service design elevates premium cabins and lounges, while continuous feedback loops improve disruption handling and net promoter scores.

- Avios: 30m+ members (2024)

- NDC & apps: increased personalized offers & self-service

- Service design: premium cabin/lounge uplift

- Feedback loops: faster disruption recovery, higher satisfaction

280+ routes;80.6% LF

IAG plans 280+ routes via LHR, MAD, BCN with slot banking and seasonal capacity shifts. OTP targets >80% backed by IOSA, recovery teams and 1–3% annual fuel-eff gains. Dynamic pricing and ancillaries (double-digit revenue share) support ~80.6% load factor (2023); fleet ~26,000 jets (2024), leased ~40%.

| Metric | Value |

|---|---|

| Load factor | 80.6% (2023) |

| Global fleet | ~26,000 (2024) |

| Leased share | ~40% |

| Avios members | 30m+ (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact International Airlines Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it contains the same content, structure, and formatting shown here. Upon completing your order you’ll instantly download the full file, ready to edit, present, and apply in Word and Excel formats. No surprises—what you see is what you get.

Explore a Global Airline Business Model Canvas: customer segments, revenue & costs

Explore International Airlines’ Business Model Canvas to see how it connects customer segments, value propositions, revenue streams and cost structure. This concise snapshot reveals key partnerships and operational levers. Ideal for investors, consultants, and strategists seeking actionable insights. Purchase the full Word/Excel canvas for a section-by-section breakdown.

Partnerships

Aircraft and engine manufacturers

Partnerships with Airbus, Boeing and engine OEMs such as Rolls-Royce and GE secure fleet availability, performance and OEM support; multi-year purchase agreements for hundreds of aircraft lower unit costs and enable fleet commonality and training synergies. OEM maintenance programs and mid-life upgrades sustain reliability and fuel efficiency, while joint R&D in 2024 accelerated SAF-readiness and next-gen cabin innovations.

Alliances, codeshare, and interline partners

IAG airlines leverage oneworld and bilateral codeshares to extend network reach, tapping oneworld’s network of over 1,000 destinations in more than 170 territories (2024) to offer seamless itineraries and reciprocal frequent‑flyer benefits that boost appeal to global travelers. Shared lounges and coordinated schedules improve connectivity and transfer times, while partners smooth seasonal demand swings and help optimize aircraft utilization across the group.

Airports, ground handlers, and catering providers

Hubs such as LHR, MAD, DUB, and BCN require deep coordination for slots and turnarounds; LHR is subject to a 480,000 annual slot cap, forcing precise scheduling and partner alignment.

Ground handling and catering partners drive punctuality and service consistency, and joint process improvements reduce delays and operational costs.

Premium lounge partners enhance customer experience and support ancillary revenue through upsell and retention opportunities.

Distribution partners: GDS, OTAs, and TMCs

Distribution partners—GDS, OTAs and TMCs—expand market reach across leisure and corporate segments, with OTAs handling about half of online bookings and corporate travel typically contributing 10–20% of airline revenue; corporate negotiated rates and growing NDC connectivity (adopted by hundreds of carriers by 2024) give airlines tighter offer control. Data-sharing with partners refines merchandising and ancillaries, while co-marketing drives incremental bookings and higher yield.

- GDS/OTAs/TMCs: market reach

- Corporate rates + NDC: offer control

- Data-sharing: better ancillaries

- Co-marketing: incremental bookings

Fuel, SAF suppliers, and financial partners

Strategic fuel hedgers and SAF producers support cost stability and decarbonization, with SAF supply still nascent at roughly 0.3% of global jet fuel demand in 2024, so multi-year offtakes secure future volumes and pricing. Banks, lessors, and ECAs provide liquidity and leases—lessors control about 50% of the global commercial fleet—while risk partners manage FX, interest rate, and commodity exposures to protect margins.

- SAF 2024 share ≈0.3%

- Lessors ≈50% of fleet

- Multi-year SAF offtakes lock supply

- Risk partners hedge FX, rates, commodities

Partnerships secure fleet, fuel and network access, boosting yields and ancillaries

Key partnerships secure fleet, cost and fuel stability (OEMs, lessors, banks), expand network and yield (oneworld, codeshares, GDS/OTAs, NDC) and improve operations and experience (ground handlers, caterers, lounges, SAF offtakes, hedgers). Coordination at constrained hubs (LHR slots) and data-sharing with distribution partners drives higher ancillaries and utilization.

| Partner | Role | 2024 metric |

|---|---|---|

| oneworld | Network | 1,000+ destinations, 170 territories |

| SAF suppliers | Decarbonize | ≈0.3% jet fuel |

| Lessors | Fleet finance | ≈50% global fleet |

| LHR | Hub constraint | 480,000 slot cap |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to international airlines, covering all 9 BMC blocks with detailed customer segments, channels, value propositions, revenue streams, cost structure, key activities, partners and regulatory considerations. Ideal for presentations, investor discussions and strategic decision-making, it includes competitive advantages and a linked SWOT to validate business plans using real-world operational insights.

High-level view of an international airline’s business model with editable cells to streamline route planning, fleet utilization and revenue streams—saves hours reconciling disparate data. Great for quick boardroom reviews, comparing carriers side-by-side, and adapting strategy during regulatory or market shocks.

Activities

Network and schedule optimization

IAG plans routes across 80+ long-haul and 200+ short-haul destinations to maximize connectivity and yields, leveraging hubs at London Heathrow, Madrid and Barcelona. Rigorous slot management and hub banking at Heathrow and Madrid smooth transfer flows and protect peak-hour connectivity. Seasonal and event-driven capacity shifts (summer peaks, major events) adjust frequencies and gauge to capture demand spikes. Ongoing competitive monitoring informs frequency and aircraft-gauge decisions.

Flight operations and safety management

Daily flight operations prioritize on-time performance (OTP targets often above 80%) and strict regulatory compliance; airlines coordinate crewing, ATC slots and maintenance to meet schedules. Safety management systems, including IATA IOSA (over 400 airlines enrolled), and recurrent training underpin reliability. Dedicated irregular-ops teams focus on rapid recovery to limit customer disruption. Continuous improvement programs target 1–3% annual fuel-efficiency gains and shorter turnarounds (30–90 minutes).

Revenue management and pricing

Dynamic pricing allocates seats across fare classes to maximize load factor and yield, supporting a global passenger load factor around 80.6% in 2023. Ancillary bundling—bag fees, seat selection and bundles—now contributes a double-digit share of airline revenues and boosted margins industrywide. Corporate contracting and group sales, with business travel near 80% of 2019 levels in 2023, balance the mix. Data science underpins demand forecasting and rapid competitive response.

Fleet and MRO lifecycle management

- Fleet size 2024 ~26,000 jets

- Leased share ~40%

- Cabin refresh 5–10 yr

- MRO market focus on engine/airframe reliability

Loyalty, digital, and customer experience

Avios powers cross-brand loyalty engagement and monetization, with the Avios currency serving customers across airlines, hotels and retail (30m+ members reported by 2024). Apps, websites and NDC enable personalized offers and self-service, driving higher ancillary conversion and mobile bookings. Service design elevates premium cabins and lounges, while continuous feedback loops improve disruption handling and net promoter scores.

- Avios: 30m+ members (2024)

- NDC & apps: increased personalized offers & self-service

- Service design: premium cabin/lounge uplift

- Feedback loops: faster disruption recovery, higher satisfaction

280+ routes;80.6% LF

IAG plans 280+ routes via LHR, MAD, BCN with slot banking and seasonal capacity shifts. OTP targets >80% backed by IOSA, recovery teams and 1–3% annual fuel-eff gains. Dynamic pricing and ancillaries (double-digit revenue share) support ~80.6% load factor (2023); fleet ~26,000 jets (2024), leased ~40%.

| Metric | Value |

|---|---|

| Load factor | 80.6% (2023) |

| Global fleet | ~26,000 (2024) |

| Leased share | ~40% |

| Avios members | 30m+ (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact International Airlines Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it contains the same content, structure, and formatting shown here. Upon completing your order you’ll instantly download the full file, ready to edit, present, and apply in Word and Excel formats. No surprises—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Explore a Global Airline Business Model Canvas: customer segments, revenue & costs

Explore International Airlines’ Business Model Canvas to see how it connects customer segments, value propositions, revenue streams and cost structure. This concise snapshot reveals key partnerships and operational levers. Ideal for investors, consultants, and strategists seeking actionable insights. Purchase the full Word/Excel canvas for a section-by-section breakdown.

Partnerships

Aircraft and engine manufacturers

Partnerships with Airbus, Boeing and engine OEMs such as Rolls-Royce and GE secure fleet availability, performance and OEM support; multi-year purchase agreements for hundreds of aircraft lower unit costs and enable fleet commonality and training synergies. OEM maintenance programs and mid-life upgrades sustain reliability and fuel efficiency, while joint R&D in 2024 accelerated SAF-readiness and next-gen cabin innovations.

Alliances, codeshare, and interline partners

IAG airlines leverage oneworld and bilateral codeshares to extend network reach, tapping oneworld’s network of over 1,000 destinations in more than 170 territories (2024) to offer seamless itineraries and reciprocal frequent‑flyer benefits that boost appeal to global travelers. Shared lounges and coordinated schedules improve connectivity and transfer times, while partners smooth seasonal demand swings and help optimize aircraft utilization across the group.

Airports, ground handlers, and catering providers

Hubs such as LHR, MAD, DUB, and BCN require deep coordination for slots and turnarounds; LHR is subject to a 480,000 annual slot cap, forcing precise scheduling and partner alignment.

Ground handling and catering partners drive punctuality and service consistency, and joint process improvements reduce delays and operational costs.

Premium lounge partners enhance customer experience and support ancillary revenue through upsell and retention opportunities.

Distribution partners: GDS, OTAs, and TMCs

Distribution partners—GDS, OTAs and TMCs—expand market reach across leisure and corporate segments, with OTAs handling about half of online bookings and corporate travel typically contributing 10–20% of airline revenue; corporate negotiated rates and growing NDC connectivity (adopted by hundreds of carriers by 2024) give airlines tighter offer control. Data-sharing with partners refines merchandising and ancillaries, while co-marketing drives incremental bookings and higher yield.

- GDS/OTAs/TMCs: market reach

- Corporate rates + NDC: offer control

- Data-sharing: better ancillaries

- Co-marketing: incremental bookings

Fuel, SAF suppliers, and financial partners

Strategic fuel hedgers and SAF producers support cost stability and decarbonization, with SAF supply still nascent at roughly 0.3% of global jet fuel demand in 2024, so multi-year offtakes secure future volumes and pricing. Banks, lessors, and ECAs provide liquidity and leases—lessors control about 50% of the global commercial fleet—while risk partners manage FX, interest rate, and commodity exposures to protect margins.

- SAF 2024 share ≈0.3%

- Lessors ≈50% of fleet

- Multi-year SAF offtakes lock supply

- Risk partners hedge FX, rates, commodities

Partnerships secure fleet, fuel and network access, boosting yields and ancillaries

Key partnerships secure fleet, cost and fuel stability (OEMs, lessors, banks), expand network and yield (oneworld, codeshares, GDS/OTAs, NDC) and improve operations and experience (ground handlers, caterers, lounges, SAF offtakes, hedgers). Coordination at constrained hubs (LHR slots) and data-sharing with distribution partners drives higher ancillaries and utilization.

| Partner | Role | 2024 metric |

|---|---|---|

| oneworld | Network | 1,000+ destinations, 170 territories |

| SAF suppliers | Decarbonize | ≈0.3% jet fuel |

| Lessors | Fleet finance | ≈50% global fleet |

| LHR | Hub constraint | 480,000 slot cap |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to international airlines, covering all 9 BMC blocks with detailed customer segments, channels, value propositions, revenue streams, cost structure, key activities, partners and regulatory considerations. Ideal for presentations, investor discussions and strategic decision-making, it includes competitive advantages and a linked SWOT to validate business plans using real-world operational insights.

High-level view of an international airline’s business model with editable cells to streamline route planning, fleet utilization and revenue streams—saves hours reconciling disparate data. Great for quick boardroom reviews, comparing carriers side-by-side, and adapting strategy during regulatory or market shocks.

Activities

Network and schedule optimization

IAG plans routes across 80+ long-haul and 200+ short-haul destinations to maximize connectivity and yields, leveraging hubs at London Heathrow, Madrid and Barcelona. Rigorous slot management and hub banking at Heathrow and Madrid smooth transfer flows and protect peak-hour connectivity. Seasonal and event-driven capacity shifts (summer peaks, major events) adjust frequencies and gauge to capture demand spikes. Ongoing competitive monitoring informs frequency and aircraft-gauge decisions.

Flight operations and safety management

Daily flight operations prioritize on-time performance (OTP targets often above 80%) and strict regulatory compliance; airlines coordinate crewing, ATC slots and maintenance to meet schedules. Safety management systems, including IATA IOSA (over 400 airlines enrolled), and recurrent training underpin reliability. Dedicated irregular-ops teams focus on rapid recovery to limit customer disruption. Continuous improvement programs target 1–3% annual fuel-efficiency gains and shorter turnarounds (30–90 minutes).

Revenue management and pricing

Dynamic pricing allocates seats across fare classes to maximize load factor and yield, supporting a global passenger load factor around 80.6% in 2023. Ancillary bundling—bag fees, seat selection and bundles—now contributes a double-digit share of airline revenues and boosted margins industrywide. Corporate contracting and group sales, with business travel near 80% of 2019 levels in 2023, balance the mix. Data science underpins demand forecasting and rapid competitive response.

Fleet and MRO lifecycle management

- Fleet size 2024 ~26,000 jets

- Leased share ~40%

- Cabin refresh 5–10 yr

- MRO market focus on engine/airframe reliability

Loyalty, digital, and customer experience

Avios powers cross-brand loyalty engagement and monetization, with the Avios currency serving customers across airlines, hotels and retail (30m+ members reported by 2024). Apps, websites and NDC enable personalized offers and self-service, driving higher ancillary conversion and mobile bookings. Service design elevates premium cabins and lounges, while continuous feedback loops improve disruption handling and net promoter scores.

- Avios: 30m+ members (2024)

- NDC & apps: increased personalized offers & self-service

- Service design: premium cabin/lounge uplift

- Feedback loops: faster disruption recovery, higher satisfaction

280+ routes;80.6% LF

IAG plans 280+ routes via LHR, MAD, BCN with slot banking and seasonal capacity shifts. OTP targets >80% backed by IOSA, recovery teams and 1–3% annual fuel-eff gains. Dynamic pricing and ancillaries (double-digit revenue share) support ~80.6% load factor (2023); fleet ~26,000 jets (2024), leased ~40%.

| Metric | Value |

|---|---|

| Load factor | 80.6% (2023) |

| Global fleet | ~26,000 (2024) |

| Leased share | ~40% |

| Avios members | 30m+ (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact International Airlines Business Model Canvas you’ll receive after purchase—not a mockup or sample—and it contains the same content, structure, and formatting shown here. Upon completing your order you’ll instantly download the full file, ready to edit, present, and apply in Word and Excel formats. No surprises—what you see is what you get.