Iberdrola Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

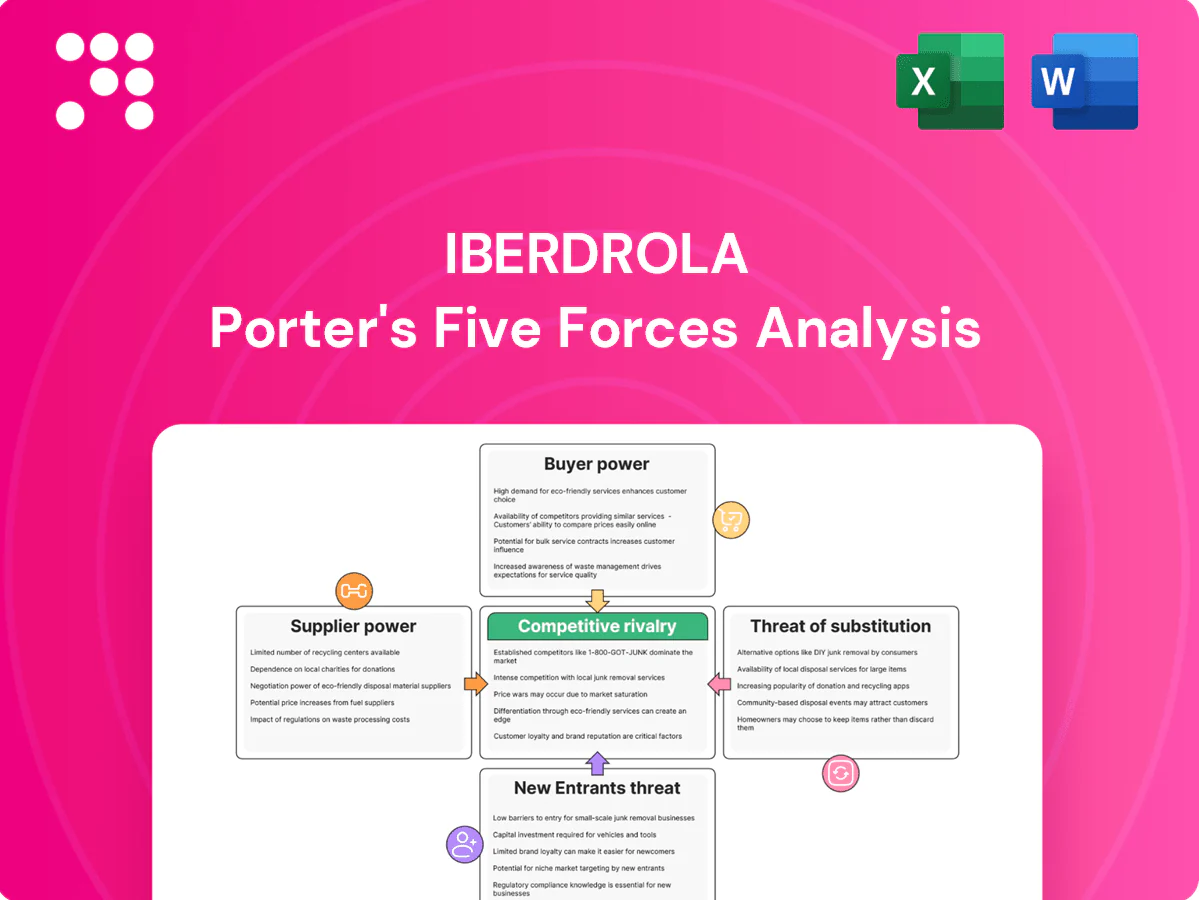

Iberdrola faces robust competitive pressures from incumbents and regulatory shifts, while supplier and buyer dynamics are tempered by long-term contracts and renewable scale advantages; substitutes and entry threats hinge on tech costs and policy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Iberdrola’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated turbine and inverter vendors

Global wind turbine, grid inverter and HV equipment markets are highly concentrated—top five OEMs supply roughly 70% of capacity (2023–24), raising switching costs and delivery risk. Iberdrola mitigates via multi-sourcing and long-term framework agreements. Technology lock-in and certification requirements preserve supplier leverage. Supply-chain tightness has pushed turbine lead times to about 12–24 months and pressured capex upward in 2023–24.

Critical raw materials and components

Power electronics, transformers and cables depend on copper, steel, semiconductors and rare earths, with China still supplying over 80% of rare earth processing, concentrating upstream risk. Commodity volatility and limited refining capacity squeeze margins as input prices and lead times spike. Iberdrola uses hedging and scale procurement to soften cost shocks and reported significant centralized procurement in 2024 to manage exposure. Pass-through of higher costs remains uneven between regulated and merchant activities.

Grid equipment and EPC capacity constraints

Large network expansions face scarce EPC contractors and specialized crews, with contractor backlogs reported at 12–18 months in 2024, elevating supplier bargaining power through scheduling and price pressure. Iberdrola’s repeat volumes and standardized designs have secured better terms and reduced unit costs, but localized labor shortages and tight regulatory deadlines can still shift leverage to suppliers.

Fuel and balancing services

- Suppliers: situational power during gas-backed dispatch

- Hubs/interconnects: diversification reduces single-supplier risk

- Iberdrola: growing storage/hydro lowers exposure over time

- Peaks: cost spikes limit negotiation room

Digital platforms and OEM software

SCADA, asset analytics and OEM firmware create proprietary ecosystems that centralize control and limit interoperability. In 2024 Iberdrola reported active negotiation of data rights and adoption of open standards to reduce lock-in, but licensing, cybersecurity compliance and data-access clauses still enable supplier leverage. Upgrades and warranties often remain tied to OEM service bundles, sustaining supplier influence.

- Proprietary SCADA ecosystems

- Data-access & licensing clauses

- Iberdrola pushes open standards (2024)

- OEM upgrades/warranties = sustained influence

High supplier power, long turbine lead times and rare-earth risk push procurement pressures

Supplier power is high in turbines, inverters and HV gear (top‑5 ≈70% market share; turbine lead times 12–24 months in 2023–24), raising switching costs and capex. Upstream concentration (China >80% rare‑earth processing) and commodity volatility pushed procurement risk and margins in 2023–24. Iberdrola mitigates via multi‑sourcing, long‑term frameworks, centralized procurement and growing storage/hydro.

| Category | Metric (2023–24) | Impact |

|---|---|---|

| Wind OEMs | Top‑5 ≈70% share; lead times 12–24m | High |

| Rare earths | China >80% processing | High |

| EPC/labour | Backlogs 12–18m (2024) | Medium |

What is included in the product

Evaluates supplier and buyer power, threat of new entrants and substitutes, and competitive rivalry for Iberdrola, highlighting regulatory pressure, scale advantages, and the renewable-energy transition shaping profitability and market positioning. Includes strategic implications for pricing, investment prioritization, and defenses against emerging disruptive entrants.

A concise one-sheet Porter’s Five Forces for Iberdrola that maps supplier, buyer, entrant, substitute, and rivalry pressures—ready to drop into decks; customizable force levels and radar visuals make strategic decisions fast, clear, and accessible to non-experts.

Customers Bargaining Power

Regulated customers with tariff oversight

Network users pay regulated tariffs set by authorities, so direct buyer bargaining power is limited; regulators oversee tariffs for millions of customers and completed the 2023–2024 tariff reviews that shape charges in 2024. Regulators prioritize affordability and reliability, indirectly pressuring returns and linking allowed revenues to quality metrics (SAIDI/SAIFI). Iberdrola’s operational efficiency and service quality therefore influence the revenue the regulator permits, so customer leverage is mediated through the regulatory process in 2024.

Liberalized retail customers

Households and SMEs in liberalized retail markets can switch suppliers, raising price sensitivity and bargaining leverage. Transparent comparison tools and dynamic tariffs increase churn risk, pressuring margins. Iberdrola emphasizes green branding, bundled offers and loyalty programs to reduce attrition, while varying switching frictions by country generally keep buyer power at a moderate level.

Large industrial and corporate PPAs

Large industrial and corporate buyers negotiate bespoke PPAs and flexibility terms, using volume and creditworthiness to secure lower prices and longer tenors; global corporate PPA deals reached 29.4 GW in 2023 (BNEF). Iberdrola leverages a multi‑GW pipeline and diversified geographies to balance offtake and counterparty risk, but intense competition for marquee clients forces price and contractual concessions.

Distributed energy prosumers

Rooftop solar, storage and smart devices enable prosumers to self-supply, shrinking demand for traditional retail supply and driving higher expectations for rates and services; as self-consumption rises Iberdrola counters with aggregation, virtual power plants and behind-the-meter offers to reduce churn. These solutions increase buyer negotiating power by shifting value from commodity supply to flexibility and services, forcing Iberdrola to compete on tariffs, DER integration and platform features.

- Trend: prosumers shift value to flexibility and services

- Iberdrola response: aggregation, VPPs, behind-the-meter

- Impact: lower churn but stronger customer bargaining power

Public sector and municipalities

Tenders for public-sector supply and renewables are formal and heavily price-driven, while ESG criteria and local-content rules impose non-price demands; Iberdrola’s scale and credibility—targeting 60 GW of renewables by 2025—strengthen bid success, yet competitive auctions institutionalize significant buyer leverage.

- Price-focused tenders

- ESG and local-content constraints

- Iberdrola scale: 60 GW target by 2025

- Auctions increase customer bargaining power

Tariff caps limit bargaining; PPAs 29.4 GW and DERs raise buyer leverage

Regulated tariffs set by authorities (2023–24 tariff reviews) cap direct customer bargaining power and tie allowed revenues to reliability metrics. Retail switching raises household/SME price sensitivity and churn risk. Corporate buyers secured 29.4 GW of global PPAs in 2023, forcing contractual concessions. Prosumers and DERs increase leverage, met by Iberdrola aggregation and VPP offers.

| Metric | Value | Impact |

|---|---|---|

| Tariff reviews | 2023–24 | Limits direct bargaining |

| Corporate PPAs | 29.4 GW (2023) | Higher buyer leverage |

| Renewables scale | 60 GW target (2025) | Stronger auction competitiveness |

What You See Is What You Get

Iberdrola Porter's Five Forces Analysis

This Iberdrola Porter's Five Forces Analysis is the full, professionally prepared report you see in the preview, covering competitive rivalry, supplier and buyer power, threats of entry and substitutes with actionable insights. The previewed file is identical to the one delivered instantly after purchase—no placeholders, no samples. It’s formatted and ready to download and use immediately for strategic or investment decisions.

A Must-Have Tool for Decision-Makers

Iberdrola faces robust competitive pressures from incumbents and regulatory shifts, while supplier and buyer dynamics are tempered by long-term contracts and renewable scale advantages; substitutes and entry threats hinge on tech costs and policy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Iberdrola’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated turbine and inverter vendors

Global wind turbine, grid inverter and HV equipment markets are highly concentrated—top five OEMs supply roughly 70% of capacity (2023–24), raising switching costs and delivery risk. Iberdrola mitigates via multi-sourcing and long-term framework agreements. Technology lock-in and certification requirements preserve supplier leverage. Supply-chain tightness has pushed turbine lead times to about 12–24 months and pressured capex upward in 2023–24.

Critical raw materials and components

Power electronics, transformers and cables depend on copper, steel, semiconductors and rare earths, with China still supplying over 80% of rare earth processing, concentrating upstream risk. Commodity volatility and limited refining capacity squeeze margins as input prices and lead times spike. Iberdrola uses hedging and scale procurement to soften cost shocks and reported significant centralized procurement in 2024 to manage exposure. Pass-through of higher costs remains uneven between regulated and merchant activities.

Grid equipment and EPC capacity constraints

Large network expansions face scarce EPC contractors and specialized crews, with contractor backlogs reported at 12–18 months in 2024, elevating supplier bargaining power through scheduling and price pressure. Iberdrola’s repeat volumes and standardized designs have secured better terms and reduced unit costs, but localized labor shortages and tight regulatory deadlines can still shift leverage to suppliers.

Fuel and balancing services

- Suppliers: situational power during gas-backed dispatch

- Hubs/interconnects: diversification reduces single-supplier risk

- Iberdrola: growing storage/hydro lowers exposure over time

- Peaks: cost spikes limit negotiation room

Digital platforms and OEM software

SCADA, asset analytics and OEM firmware create proprietary ecosystems that centralize control and limit interoperability. In 2024 Iberdrola reported active negotiation of data rights and adoption of open standards to reduce lock-in, but licensing, cybersecurity compliance and data-access clauses still enable supplier leverage. Upgrades and warranties often remain tied to OEM service bundles, sustaining supplier influence.

- Proprietary SCADA ecosystems

- Data-access & licensing clauses

- Iberdrola pushes open standards (2024)

- OEM upgrades/warranties = sustained influence

High supplier power, long turbine lead times and rare-earth risk push procurement pressures

Supplier power is high in turbines, inverters and HV gear (top‑5 ≈70% market share; turbine lead times 12–24 months in 2023–24), raising switching costs and capex. Upstream concentration (China >80% rare‑earth processing) and commodity volatility pushed procurement risk and margins in 2023–24. Iberdrola mitigates via multi‑sourcing, long‑term frameworks, centralized procurement and growing storage/hydro.

| Category | Metric (2023–24) | Impact |

|---|---|---|

| Wind OEMs | Top‑5 ≈70% share; lead times 12–24m | High |

| Rare earths | China >80% processing | High |

| EPC/labour | Backlogs 12–18m (2024) | Medium |

What is included in the product

Evaluates supplier and buyer power, threat of new entrants and substitutes, and competitive rivalry for Iberdrola, highlighting regulatory pressure, scale advantages, and the renewable-energy transition shaping profitability and market positioning. Includes strategic implications for pricing, investment prioritization, and defenses against emerging disruptive entrants.

A concise one-sheet Porter’s Five Forces for Iberdrola that maps supplier, buyer, entrant, substitute, and rivalry pressures—ready to drop into decks; customizable force levels and radar visuals make strategic decisions fast, clear, and accessible to non-experts.

Customers Bargaining Power

Regulated customers with tariff oversight

Network users pay regulated tariffs set by authorities, so direct buyer bargaining power is limited; regulators oversee tariffs for millions of customers and completed the 2023–2024 tariff reviews that shape charges in 2024. Regulators prioritize affordability and reliability, indirectly pressuring returns and linking allowed revenues to quality metrics (SAIDI/SAIFI). Iberdrola’s operational efficiency and service quality therefore influence the revenue the regulator permits, so customer leverage is mediated through the regulatory process in 2024.

Liberalized retail customers

Households and SMEs in liberalized retail markets can switch suppliers, raising price sensitivity and bargaining leverage. Transparent comparison tools and dynamic tariffs increase churn risk, pressuring margins. Iberdrola emphasizes green branding, bundled offers and loyalty programs to reduce attrition, while varying switching frictions by country generally keep buyer power at a moderate level.

Large industrial and corporate PPAs

Large industrial and corporate buyers negotiate bespoke PPAs and flexibility terms, using volume and creditworthiness to secure lower prices and longer tenors; global corporate PPA deals reached 29.4 GW in 2023 (BNEF). Iberdrola leverages a multi‑GW pipeline and diversified geographies to balance offtake and counterparty risk, but intense competition for marquee clients forces price and contractual concessions.

Distributed energy prosumers

Rooftop solar, storage and smart devices enable prosumers to self-supply, shrinking demand for traditional retail supply and driving higher expectations for rates and services; as self-consumption rises Iberdrola counters with aggregation, virtual power plants and behind-the-meter offers to reduce churn. These solutions increase buyer negotiating power by shifting value from commodity supply to flexibility and services, forcing Iberdrola to compete on tariffs, DER integration and platform features.

- Trend: prosumers shift value to flexibility and services

- Iberdrola response: aggregation, VPPs, behind-the-meter

- Impact: lower churn but stronger customer bargaining power

Public sector and municipalities

Tenders for public-sector supply and renewables are formal and heavily price-driven, while ESG criteria and local-content rules impose non-price demands; Iberdrola’s scale and credibility—targeting 60 GW of renewables by 2025—strengthen bid success, yet competitive auctions institutionalize significant buyer leverage.

- Price-focused tenders

- ESG and local-content constraints

- Iberdrola scale: 60 GW target by 2025

- Auctions increase customer bargaining power

Tariff caps limit bargaining; PPAs 29.4 GW and DERs raise buyer leverage

Regulated tariffs set by authorities (2023–24 tariff reviews) cap direct customer bargaining power and tie allowed revenues to reliability metrics. Retail switching raises household/SME price sensitivity and churn risk. Corporate buyers secured 29.4 GW of global PPAs in 2023, forcing contractual concessions. Prosumers and DERs increase leverage, met by Iberdrola aggregation and VPP offers.

| Metric | Value | Impact |

|---|---|---|

| Tariff reviews | 2023–24 | Limits direct bargaining |

| Corporate PPAs | 29.4 GW (2023) | Higher buyer leverage |

| Renewables scale | 60 GW target (2025) | Stronger auction competitiveness |

What You See Is What You Get

Iberdrola Porter's Five Forces Analysis

This Iberdrola Porter's Five Forces Analysis is the full, professionally prepared report you see in the preview, covering competitive rivalry, supplier and buyer power, threats of entry and substitutes with actionable insights. The previewed file is identical to the one delivered instantly after purchase—no placeholders, no samples. It’s formatted and ready to download and use immediately for strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Iberdrola faces robust competitive pressures from incumbents and regulatory shifts, while supplier and buyer dynamics are tempered by long-term contracts and renewable scale advantages; substitutes and entry threats hinge on tech costs and policy. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Iberdrola’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated turbine and inverter vendors

Global wind turbine, grid inverter and HV equipment markets are highly concentrated—top five OEMs supply roughly 70% of capacity (2023–24), raising switching costs and delivery risk. Iberdrola mitigates via multi-sourcing and long-term framework agreements. Technology lock-in and certification requirements preserve supplier leverage. Supply-chain tightness has pushed turbine lead times to about 12–24 months and pressured capex upward in 2023–24.

Critical raw materials and components

Power electronics, transformers and cables depend on copper, steel, semiconductors and rare earths, with China still supplying over 80% of rare earth processing, concentrating upstream risk. Commodity volatility and limited refining capacity squeeze margins as input prices and lead times spike. Iberdrola uses hedging and scale procurement to soften cost shocks and reported significant centralized procurement in 2024 to manage exposure. Pass-through of higher costs remains uneven between regulated and merchant activities.

Grid equipment and EPC capacity constraints

Large network expansions face scarce EPC contractors and specialized crews, with contractor backlogs reported at 12–18 months in 2024, elevating supplier bargaining power through scheduling and price pressure. Iberdrola’s repeat volumes and standardized designs have secured better terms and reduced unit costs, but localized labor shortages and tight regulatory deadlines can still shift leverage to suppliers.

Fuel and balancing services

- Suppliers: situational power during gas-backed dispatch

- Hubs/interconnects: diversification reduces single-supplier risk

- Iberdrola: growing storage/hydro lowers exposure over time

- Peaks: cost spikes limit negotiation room

Digital platforms and OEM software

SCADA, asset analytics and OEM firmware create proprietary ecosystems that centralize control and limit interoperability. In 2024 Iberdrola reported active negotiation of data rights and adoption of open standards to reduce lock-in, but licensing, cybersecurity compliance and data-access clauses still enable supplier leverage. Upgrades and warranties often remain tied to OEM service bundles, sustaining supplier influence.

- Proprietary SCADA ecosystems

- Data-access & licensing clauses

- Iberdrola pushes open standards (2024)

- OEM upgrades/warranties = sustained influence

High supplier power, long turbine lead times and rare-earth risk push procurement pressures

Supplier power is high in turbines, inverters and HV gear (top‑5 ≈70% market share; turbine lead times 12–24 months in 2023–24), raising switching costs and capex. Upstream concentration (China >80% rare‑earth processing) and commodity volatility pushed procurement risk and margins in 2023–24. Iberdrola mitigates via multi‑sourcing, long‑term frameworks, centralized procurement and growing storage/hydro.

| Category | Metric (2023–24) | Impact |

|---|---|---|

| Wind OEMs | Top‑5 ≈70% share; lead times 12–24m | High |

| Rare earths | China >80% processing | High |

| EPC/labour | Backlogs 12–18m (2024) | Medium |

What is included in the product

Evaluates supplier and buyer power, threat of new entrants and substitutes, and competitive rivalry for Iberdrola, highlighting regulatory pressure, scale advantages, and the renewable-energy transition shaping profitability and market positioning. Includes strategic implications for pricing, investment prioritization, and defenses against emerging disruptive entrants.

A concise one-sheet Porter’s Five Forces for Iberdrola that maps supplier, buyer, entrant, substitute, and rivalry pressures—ready to drop into decks; customizable force levels and radar visuals make strategic decisions fast, clear, and accessible to non-experts.

Customers Bargaining Power

Regulated customers with tariff oversight

Network users pay regulated tariffs set by authorities, so direct buyer bargaining power is limited; regulators oversee tariffs for millions of customers and completed the 2023–2024 tariff reviews that shape charges in 2024. Regulators prioritize affordability and reliability, indirectly pressuring returns and linking allowed revenues to quality metrics (SAIDI/SAIFI). Iberdrola’s operational efficiency and service quality therefore influence the revenue the regulator permits, so customer leverage is mediated through the regulatory process in 2024.

Liberalized retail customers

Households and SMEs in liberalized retail markets can switch suppliers, raising price sensitivity and bargaining leverage. Transparent comparison tools and dynamic tariffs increase churn risk, pressuring margins. Iberdrola emphasizes green branding, bundled offers and loyalty programs to reduce attrition, while varying switching frictions by country generally keep buyer power at a moderate level.

Large industrial and corporate PPAs

Large industrial and corporate buyers negotiate bespoke PPAs and flexibility terms, using volume and creditworthiness to secure lower prices and longer tenors; global corporate PPA deals reached 29.4 GW in 2023 (BNEF). Iberdrola leverages a multi‑GW pipeline and diversified geographies to balance offtake and counterparty risk, but intense competition for marquee clients forces price and contractual concessions.

Distributed energy prosumers

Rooftop solar, storage and smart devices enable prosumers to self-supply, shrinking demand for traditional retail supply and driving higher expectations for rates and services; as self-consumption rises Iberdrola counters with aggregation, virtual power plants and behind-the-meter offers to reduce churn. These solutions increase buyer negotiating power by shifting value from commodity supply to flexibility and services, forcing Iberdrola to compete on tariffs, DER integration and platform features.

- Trend: prosumers shift value to flexibility and services

- Iberdrola response: aggregation, VPPs, behind-the-meter

- Impact: lower churn but stronger customer bargaining power

Public sector and municipalities

Tenders for public-sector supply and renewables are formal and heavily price-driven, while ESG criteria and local-content rules impose non-price demands; Iberdrola’s scale and credibility—targeting 60 GW of renewables by 2025—strengthen bid success, yet competitive auctions institutionalize significant buyer leverage.

- Price-focused tenders

- ESG and local-content constraints

- Iberdrola scale: 60 GW target by 2025

- Auctions increase customer bargaining power

Tariff caps limit bargaining; PPAs 29.4 GW and DERs raise buyer leverage

Regulated tariffs set by authorities (2023–24 tariff reviews) cap direct customer bargaining power and tie allowed revenues to reliability metrics. Retail switching raises household/SME price sensitivity and churn risk. Corporate buyers secured 29.4 GW of global PPAs in 2023, forcing contractual concessions. Prosumers and DERs increase leverage, met by Iberdrola aggregation and VPP offers.

| Metric | Value | Impact |

|---|---|---|

| Tariff reviews | 2023–24 | Limits direct bargaining |

| Corporate PPAs | 29.4 GW (2023) | Higher buyer leverage |

| Renewables scale | 60 GW target (2025) | Stronger auction competitiveness |

What You See Is What You Get

Iberdrola Porter's Five Forces Analysis

This Iberdrola Porter's Five Forces Analysis is the full, professionally prepared report you see in the preview, covering competitive rivalry, supplier and buyer power, threats of entry and substitutes with actionable insights. The previewed file is identical to the one delivered instantly after purchase—no placeholders, no samples. It’s formatted and ready to download and use immediately for strategic or investment decisions.