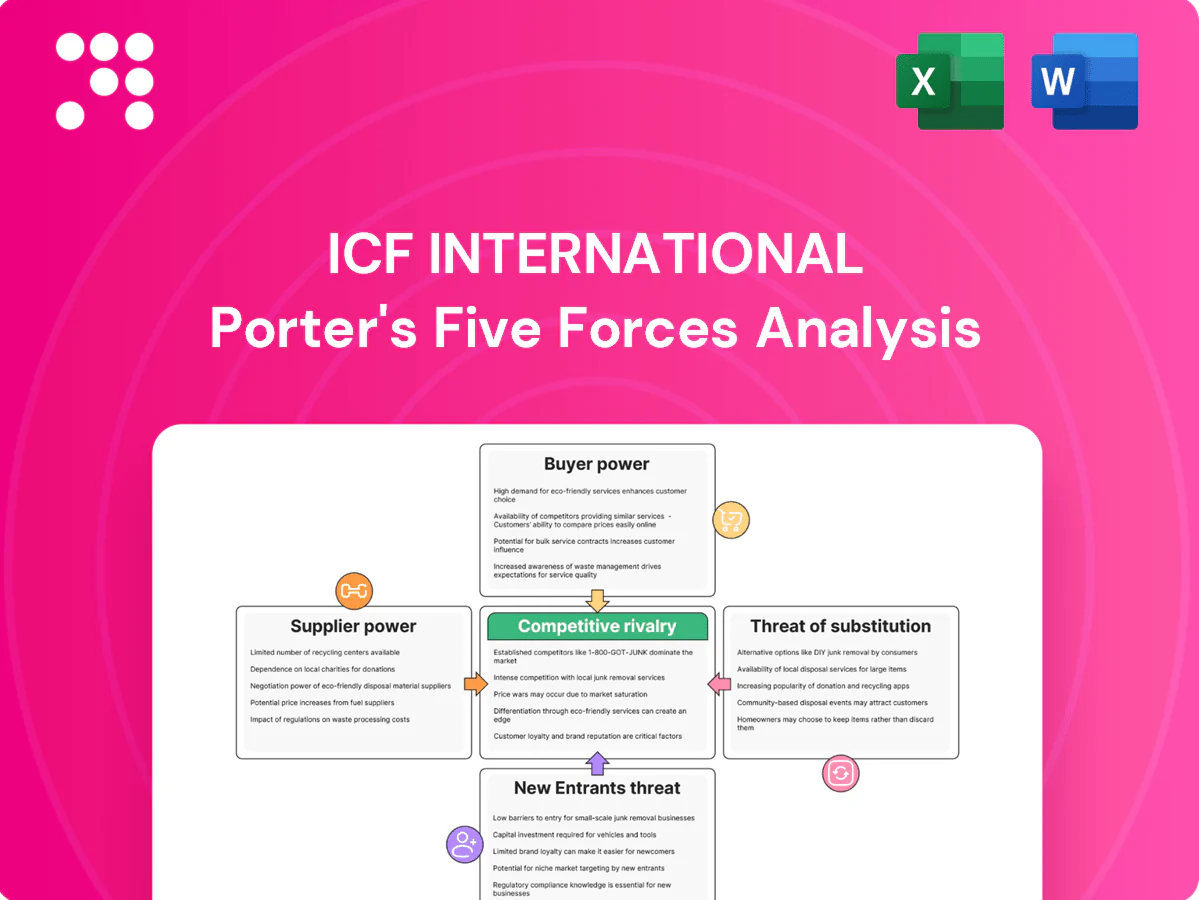

ICF International Porter's Five Forces Analysis

Don't Miss the Bigger Picture

ICF International faces nuanced competitive pressures—from client consolidation raising buyer power to specialized suppliers shaping cost dynamics; substitutes and regulatory shifts further complicate growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ICF International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized talent scarcity

ICF relies on scarce consultants, data scientists and domain experts, driving wage inflation and higher switching costs as global cybersecurity workforce shortfall reached about 3.4 million in 2024 (ISC2). Tight markets for AI/ML and cloud architects give boutique firms and individuals leverage, raising retention and recruiting costs versus industry median tech pay (information security analysts ~103,590 USD). Retention, training and long-term contracts mitigate but cannot eliminate turnover risk, and multi-year projects amplify disruption from key-person loss.

Hyperscaler and SaaS dependence

ICF depends on hyperscalers and enterprise SaaS (AWS 32%, Azure 22%, Google Cloud 10% market share in 2024 per Canalys), concentrating supplier pricing tiers and roadmap control. Volume commitments and certification demands create term lock‑ins and switching costs. Multi‑cloud and open‑source adoption mitigate some leverage. Public sector security and FedRAMP/IL compliance reduce substitution options.

Data and content providers

Access to proprietary datasets, emissions inventories, health data tools and geospatial content is critical to ICF’s services; the global geospatial analytics market was about $70 billion in 2024, underpinning supplier leverage. Licensing fees and usage caps—often exceeding $100,000 annually for specialized datasets—and data sovereignty rules across many jurisdictions elevate supplier influence. Negotiated enterprise licenses mitigate costs but key datasets remain price-inelastic, and loss or degradation of data quality can materially impair project delivery for a firm with ~$1.7B revenue (FY2023).

Subcontractors and niche boutiques

On complex federal and energy programs ICF routinely leans on subcontractors and niche boutiques for specialized capabilities and surge capacity; preferred status and strong past performance give some subs leverage to negotiate higher rates and broader scopes, while prime-contractor obligations limit ICF’s ability to replace them once work is underway. Structured master service agreements mitigate but do not eliminate this supplier risk.

- Supplier leverage: preferred status raises bargaining power

- Switching costs: prime responsibilities constrain midstream changes

- Risk mitigation: MSAs reduce but do not remove exposure

Regulatory compliance tools

Specialized regulatory compliance, cybersecurity, and accreditation services (FedRAMP, CMMC v2.0, ISO) are required to serve government clients, and as of 2024 FedRAMP listed over 600 authorized cloud services, concentrating capability among few vendors and increasing supplier leverage on price and schedules. Limited qualified providers and certification bottlenecks can delay bids or ATOs; building in-house capability reduces dependency but is time- and cost-intensive.

- High dependence on certified vendors

- FedRAMP: >600 authorized services (2024)

- Certification bottlenecks raise schedule risk

- In-house build lowers exposure but increases CAPEX/OPEX

Supplier squeeze: 3.4M cyber gap; concentrated cloud, datasets >$100k

ICF faces strong supplier leverage from scarce cybersecurity/AI talent (global shortfall ~3.4M in 2024) and concentrated cloud providers (AWS 32%, Azure 22%, Google 10% in 2024), raising costs and switching barriers; data/licensing fees (specialized datasets often >$100k/yr) and certified vendors (FedRAMP >600 services) further limit bargaining power.

| Factor | 2024 data |

|---|---|

| Cyber workforce gap | 3.4M |

| Cloud share | AWS 32% / Azure 22% / GCP 10% |

| Dataset fees | >$100k/yr |

| FedRAMP | >600 services |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to ICF International, assessing competitive rivalry, supplier and buyer power, entry barriers, and substitutes to pinpoint strategic risks and opportunities.

A concise ICF International Porter's Five Forces snapshot—instantly reveals competitive pressures, removes analysis bottlenecks, and feeds clean visuals into decks for faster, confident strategic decisions.

Customers Bargaining Power

Concentrated government buyers

Large federal and state agencies exert outsized bargaining power in the >$700B annual federal contracting market (2023), using procurement rules and long cycles to demand lower rates. IDIQ and GWAC vehicles compress margins and raise audit scrutiny across bids. Option-year renewals, often tied to specific performance metrics, force disciplined pricing and service KPIs. Budget cycles and continuing resolutions create timing leverage for buyers.

Professionalized procurement

Professionalized procurement drives down fees and tightens terms as buyers use rigorous RFPs with best-value tradeoffs and past-performance scoring to rank firms. Benchmarking across vendors standardizes rate cards while unbundling of scopes invites competition for discrete tasks. Framework agreements increasingly cap margins and enforce SLAs with financial penalties, shaping ICF’s bid strategies in 2024.

Switching among integrators

Many clients can switch among top consultancies and systems integrators for commoditized services, eroding pricing power in digital modernization and PMO work; the global IT services market was about $1.4 trillion in 2024, intensifying competition for fee-sensitive projects. Proprietary IP, outcomes-based contracts, and embedded teams increase client stickiness and raise switching costs. A strong delivery reputation and past performance reduce churn risk and defend margins.

Outcome and KPI focus

Clients increasingly tie payment to milestones, throughput, and measurable outcomes, shifting performance risk onto ICF and narrowing pricing buffers; clear baselining and agile delivery practices are critical to protect margins.

Differentiated domain expertise lets ICF command value-based fees, offsetting outcome-risk and supporting higher realization rates when metrics are predefined and auditable.

- Outcome-linked payments: increases provider risk

- Clear baselining: protects scope and margins

- Agile delivery: mitigates throughput variability

- Domain specialization: enables value-based pricing

Commercial diversification

Commercial diversification into energy, utilities and health payers reduces client concentration but exposes ICF to procurement teams focused on vendor consolidation; customers commonly negotiate 3- to 5-year master services agreements trading 5–15% volume discounts for revenue visibility. Cross-selling of advisory and implementation services helps offset pricing pressure while competitive pilots are widely used before scale-up.

- vendor consolidation: skilled procurement

- typical contract length: 3–5 years

- volume discounts: ~5–15%

- mitigant: cross-selling; pilots precede scale

Federal buyers squeeze margins in $700B+; MSAs cut 5–15%

Large federal/state buyers drive pricing in the >$700B federal contracting market (2023), using IDIQ/GWAC vehicles and rigorous RFPs to compress margins and demand SLAs. Clients can switch among consultancies for commoditized services, securing 5–15% volume discounts on 3–5 year MSAs; outcome-linked payments shift performance risk to providers.

| Metric | Value | Impact |

|---|---|---|

| Federal market (2023) | $700B+ | High buyer power |

| Contract length | 3–5 yrs | Negotiation leverage |

| Volume discounts | 5–15% | Margin pressure |

Preview Before You Purchase

ICF International Porter's Five Forces Analysis

This preview displays the exact ICF International Porter's Five Forces Analysis you'll receive after purchase—fully formatted and citation-backed. No placeholders or samples; the file available for instant download is identical to this view. It's the final, ready-to-use analysis for your reports and strategic planning.

Don't Miss the Bigger Picture

ICF International faces nuanced competitive pressures—from client consolidation raising buyer power to specialized suppliers shaping cost dynamics; substitutes and regulatory shifts further complicate growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ICF International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized talent scarcity

ICF relies on scarce consultants, data scientists and domain experts, driving wage inflation and higher switching costs as global cybersecurity workforce shortfall reached about 3.4 million in 2024 (ISC2). Tight markets for AI/ML and cloud architects give boutique firms and individuals leverage, raising retention and recruiting costs versus industry median tech pay (information security analysts ~103,590 USD). Retention, training and long-term contracts mitigate but cannot eliminate turnover risk, and multi-year projects amplify disruption from key-person loss.

Hyperscaler and SaaS dependence

ICF depends on hyperscalers and enterprise SaaS (AWS 32%, Azure 22%, Google Cloud 10% market share in 2024 per Canalys), concentrating supplier pricing tiers and roadmap control. Volume commitments and certification demands create term lock‑ins and switching costs. Multi‑cloud and open‑source adoption mitigate some leverage. Public sector security and FedRAMP/IL compliance reduce substitution options.

Data and content providers

Access to proprietary datasets, emissions inventories, health data tools and geospatial content is critical to ICF’s services; the global geospatial analytics market was about $70 billion in 2024, underpinning supplier leverage. Licensing fees and usage caps—often exceeding $100,000 annually for specialized datasets—and data sovereignty rules across many jurisdictions elevate supplier influence. Negotiated enterprise licenses mitigate costs but key datasets remain price-inelastic, and loss or degradation of data quality can materially impair project delivery for a firm with ~$1.7B revenue (FY2023).

Subcontractors and niche boutiques

On complex federal and energy programs ICF routinely leans on subcontractors and niche boutiques for specialized capabilities and surge capacity; preferred status and strong past performance give some subs leverage to negotiate higher rates and broader scopes, while prime-contractor obligations limit ICF’s ability to replace them once work is underway. Structured master service agreements mitigate but do not eliminate this supplier risk.

- Supplier leverage: preferred status raises bargaining power

- Switching costs: prime responsibilities constrain midstream changes

- Risk mitigation: MSAs reduce but do not remove exposure

Regulatory compliance tools

Specialized regulatory compliance, cybersecurity, and accreditation services (FedRAMP, CMMC v2.0, ISO) are required to serve government clients, and as of 2024 FedRAMP listed over 600 authorized cloud services, concentrating capability among few vendors and increasing supplier leverage on price and schedules. Limited qualified providers and certification bottlenecks can delay bids or ATOs; building in-house capability reduces dependency but is time- and cost-intensive.

- High dependence on certified vendors

- FedRAMP: >600 authorized services (2024)

- Certification bottlenecks raise schedule risk

- In-house build lowers exposure but increases CAPEX/OPEX

Supplier squeeze: 3.4M cyber gap; concentrated cloud, datasets >$100k

ICF faces strong supplier leverage from scarce cybersecurity/AI talent (global shortfall ~3.4M in 2024) and concentrated cloud providers (AWS 32%, Azure 22%, Google 10% in 2024), raising costs and switching barriers; data/licensing fees (specialized datasets often >$100k/yr) and certified vendors (FedRAMP >600 services) further limit bargaining power.

| Factor | 2024 data |

|---|---|

| Cyber workforce gap | 3.4M |

| Cloud share | AWS 32% / Azure 22% / GCP 10% |

| Dataset fees | >$100k/yr |

| FedRAMP | >600 services |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to ICF International, assessing competitive rivalry, supplier and buyer power, entry barriers, and substitutes to pinpoint strategic risks and opportunities.

A concise ICF International Porter's Five Forces snapshot—instantly reveals competitive pressures, removes analysis bottlenecks, and feeds clean visuals into decks for faster, confident strategic decisions.

Customers Bargaining Power

Concentrated government buyers

Large federal and state agencies exert outsized bargaining power in the >$700B annual federal contracting market (2023), using procurement rules and long cycles to demand lower rates. IDIQ and GWAC vehicles compress margins and raise audit scrutiny across bids. Option-year renewals, often tied to specific performance metrics, force disciplined pricing and service KPIs. Budget cycles and continuing resolutions create timing leverage for buyers.

Professionalized procurement

Professionalized procurement drives down fees and tightens terms as buyers use rigorous RFPs with best-value tradeoffs and past-performance scoring to rank firms. Benchmarking across vendors standardizes rate cards while unbundling of scopes invites competition for discrete tasks. Framework agreements increasingly cap margins and enforce SLAs with financial penalties, shaping ICF’s bid strategies in 2024.

Switching among integrators

Many clients can switch among top consultancies and systems integrators for commoditized services, eroding pricing power in digital modernization and PMO work; the global IT services market was about $1.4 trillion in 2024, intensifying competition for fee-sensitive projects. Proprietary IP, outcomes-based contracts, and embedded teams increase client stickiness and raise switching costs. A strong delivery reputation and past performance reduce churn risk and defend margins.

Outcome and KPI focus

Clients increasingly tie payment to milestones, throughput, and measurable outcomes, shifting performance risk onto ICF and narrowing pricing buffers; clear baselining and agile delivery practices are critical to protect margins.

Differentiated domain expertise lets ICF command value-based fees, offsetting outcome-risk and supporting higher realization rates when metrics are predefined and auditable.

- Outcome-linked payments: increases provider risk

- Clear baselining: protects scope and margins

- Agile delivery: mitigates throughput variability

- Domain specialization: enables value-based pricing

Commercial diversification

Commercial diversification into energy, utilities and health payers reduces client concentration but exposes ICF to procurement teams focused on vendor consolidation; customers commonly negotiate 3- to 5-year master services agreements trading 5–15% volume discounts for revenue visibility. Cross-selling of advisory and implementation services helps offset pricing pressure while competitive pilots are widely used before scale-up.

- vendor consolidation: skilled procurement

- typical contract length: 3–5 years

- volume discounts: ~5–15%

- mitigant: cross-selling; pilots precede scale

Federal buyers squeeze margins in $700B+; MSAs cut 5–15%

Large federal/state buyers drive pricing in the >$700B federal contracting market (2023), using IDIQ/GWAC vehicles and rigorous RFPs to compress margins and demand SLAs. Clients can switch among consultancies for commoditized services, securing 5–15% volume discounts on 3–5 year MSAs; outcome-linked payments shift performance risk to providers.

| Metric | Value | Impact |

|---|---|---|

| Federal market (2023) | $700B+ | High buyer power |

| Contract length | 3–5 yrs | Negotiation leverage |

| Volume discounts | 5–15% | Margin pressure |

Preview Before You Purchase

ICF International Porter's Five Forces Analysis

This preview displays the exact ICF International Porter's Five Forces Analysis you'll receive after purchase—fully formatted and citation-backed. No placeholders or samples; the file available for instant download is identical to this view. It's the final, ready-to-use analysis for your reports and strategic planning.

Description

Don't Miss the Bigger Picture

ICF International faces nuanced competitive pressures—from client consolidation raising buyer power to specialized suppliers shaping cost dynamics; substitutes and regulatory shifts further complicate growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ICF International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized talent scarcity

ICF relies on scarce consultants, data scientists and domain experts, driving wage inflation and higher switching costs as global cybersecurity workforce shortfall reached about 3.4 million in 2024 (ISC2). Tight markets for AI/ML and cloud architects give boutique firms and individuals leverage, raising retention and recruiting costs versus industry median tech pay (information security analysts ~103,590 USD). Retention, training and long-term contracts mitigate but cannot eliminate turnover risk, and multi-year projects amplify disruption from key-person loss.

Hyperscaler and SaaS dependence

ICF depends on hyperscalers and enterprise SaaS (AWS 32%, Azure 22%, Google Cloud 10% market share in 2024 per Canalys), concentrating supplier pricing tiers and roadmap control. Volume commitments and certification demands create term lock‑ins and switching costs. Multi‑cloud and open‑source adoption mitigate some leverage. Public sector security and FedRAMP/IL compliance reduce substitution options.

Data and content providers

Access to proprietary datasets, emissions inventories, health data tools and geospatial content is critical to ICF’s services; the global geospatial analytics market was about $70 billion in 2024, underpinning supplier leverage. Licensing fees and usage caps—often exceeding $100,000 annually for specialized datasets—and data sovereignty rules across many jurisdictions elevate supplier influence. Negotiated enterprise licenses mitigate costs but key datasets remain price-inelastic, and loss or degradation of data quality can materially impair project delivery for a firm with ~$1.7B revenue (FY2023).

Subcontractors and niche boutiques

On complex federal and energy programs ICF routinely leans on subcontractors and niche boutiques for specialized capabilities and surge capacity; preferred status and strong past performance give some subs leverage to negotiate higher rates and broader scopes, while prime-contractor obligations limit ICF’s ability to replace them once work is underway. Structured master service agreements mitigate but do not eliminate this supplier risk.

- Supplier leverage: preferred status raises bargaining power

- Switching costs: prime responsibilities constrain midstream changes

- Risk mitigation: MSAs reduce but do not remove exposure

Regulatory compliance tools

Specialized regulatory compliance, cybersecurity, and accreditation services (FedRAMP, CMMC v2.0, ISO) are required to serve government clients, and as of 2024 FedRAMP listed over 600 authorized cloud services, concentrating capability among few vendors and increasing supplier leverage on price and schedules. Limited qualified providers and certification bottlenecks can delay bids or ATOs; building in-house capability reduces dependency but is time- and cost-intensive.

- High dependence on certified vendors

- FedRAMP: >600 authorized services (2024)

- Certification bottlenecks raise schedule risk

- In-house build lowers exposure but increases CAPEX/OPEX

Supplier squeeze: 3.4M cyber gap; concentrated cloud, datasets >$100k

ICF faces strong supplier leverage from scarce cybersecurity/AI talent (global shortfall ~3.4M in 2024) and concentrated cloud providers (AWS 32%, Azure 22%, Google 10% in 2024), raising costs and switching barriers; data/licensing fees (specialized datasets often >$100k/yr) and certified vendors (FedRAMP >600 services) further limit bargaining power.

| Factor | 2024 data |

|---|---|

| Cyber workforce gap | 3.4M |

| Cloud share | AWS 32% / Azure 22% / GCP 10% |

| Dataset fees | >$100k/yr |

| FedRAMP | >600 services |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to ICF International, assessing competitive rivalry, supplier and buyer power, entry barriers, and substitutes to pinpoint strategic risks and opportunities.

A concise ICF International Porter's Five Forces snapshot—instantly reveals competitive pressures, removes analysis bottlenecks, and feeds clean visuals into decks for faster, confident strategic decisions.

Customers Bargaining Power

Concentrated government buyers

Large federal and state agencies exert outsized bargaining power in the >$700B annual federal contracting market (2023), using procurement rules and long cycles to demand lower rates. IDIQ and GWAC vehicles compress margins and raise audit scrutiny across bids. Option-year renewals, often tied to specific performance metrics, force disciplined pricing and service KPIs. Budget cycles and continuing resolutions create timing leverage for buyers.

Professionalized procurement

Professionalized procurement drives down fees and tightens terms as buyers use rigorous RFPs with best-value tradeoffs and past-performance scoring to rank firms. Benchmarking across vendors standardizes rate cards while unbundling of scopes invites competition for discrete tasks. Framework agreements increasingly cap margins and enforce SLAs with financial penalties, shaping ICF’s bid strategies in 2024.

Switching among integrators

Many clients can switch among top consultancies and systems integrators for commoditized services, eroding pricing power in digital modernization and PMO work; the global IT services market was about $1.4 trillion in 2024, intensifying competition for fee-sensitive projects. Proprietary IP, outcomes-based contracts, and embedded teams increase client stickiness and raise switching costs. A strong delivery reputation and past performance reduce churn risk and defend margins.

Outcome and KPI focus

Clients increasingly tie payment to milestones, throughput, and measurable outcomes, shifting performance risk onto ICF and narrowing pricing buffers; clear baselining and agile delivery practices are critical to protect margins.

Differentiated domain expertise lets ICF command value-based fees, offsetting outcome-risk and supporting higher realization rates when metrics are predefined and auditable.

- Outcome-linked payments: increases provider risk

- Clear baselining: protects scope and margins

- Agile delivery: mitigates throughput variability

- Domain specialization: enables value-based pricing

Commercial diversification

Commercial diversification into energy, utilities and health payers reduces client concentration but exposes ICF to procurement teams focused on vendor consolidation; customers commonly negotiate 3- to 5-year master services agreements trading 5–15% volume discounts for revenue visibility. Cross-selling of advisory and implementation services helps offset pricing pressure while competitive pilots are widely used before scale-up.

- vendor consolidation: skilled procurement

- typical contract length: 3–5 years

- volume discounts: ~5–15%

- mitigant: cross-selling; pilots precede scale

Federal buyers squeeze margins in $700B+; MSAs cut 5–15%

Large federal/state buyers drive pricing in the >$700B federal contracting market (2023), using IDIQ/GWAC vehicles and rigorous RFPs to compress margins and demand SLAs. Clients can switch among consultancies for commoditized services, securing 5–15% volume discounts on 3–5 year MSAs; outcome-linked payments shift performance risk to providers.

| Metric | Value | Impact |

|---|---|---|

| Federal market (2023) | $700B+ | High buyer power |

| Contract length | 3–5 yrs | Negotiation leverage |

| Volume discounts | 5–15% | Margin pressure |

Preview Before You Purchase

ICF International Porter's Five Forces Analysis

This preview displays the exact ICF International Porter's Five Forces Analysis you'll receive after purchase—fully formatted and citation-backed. No placeholders or samples; the file available for instant download is identical to this view. It's the final, ready-to-use analysis for your reports and strategic planning.