ICICI Lombard General Insurance PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock competitive advantage with our PESTLE Analysis of ICICI Lombard General Insurance—concise, actionable, and built for decision-makers. Discover how political, economic, social, technological, legal, and environmental forces shape the firm's strategy and risk profile. Purchase the full report to access deep-dive insights and ready-to-use recommendations.

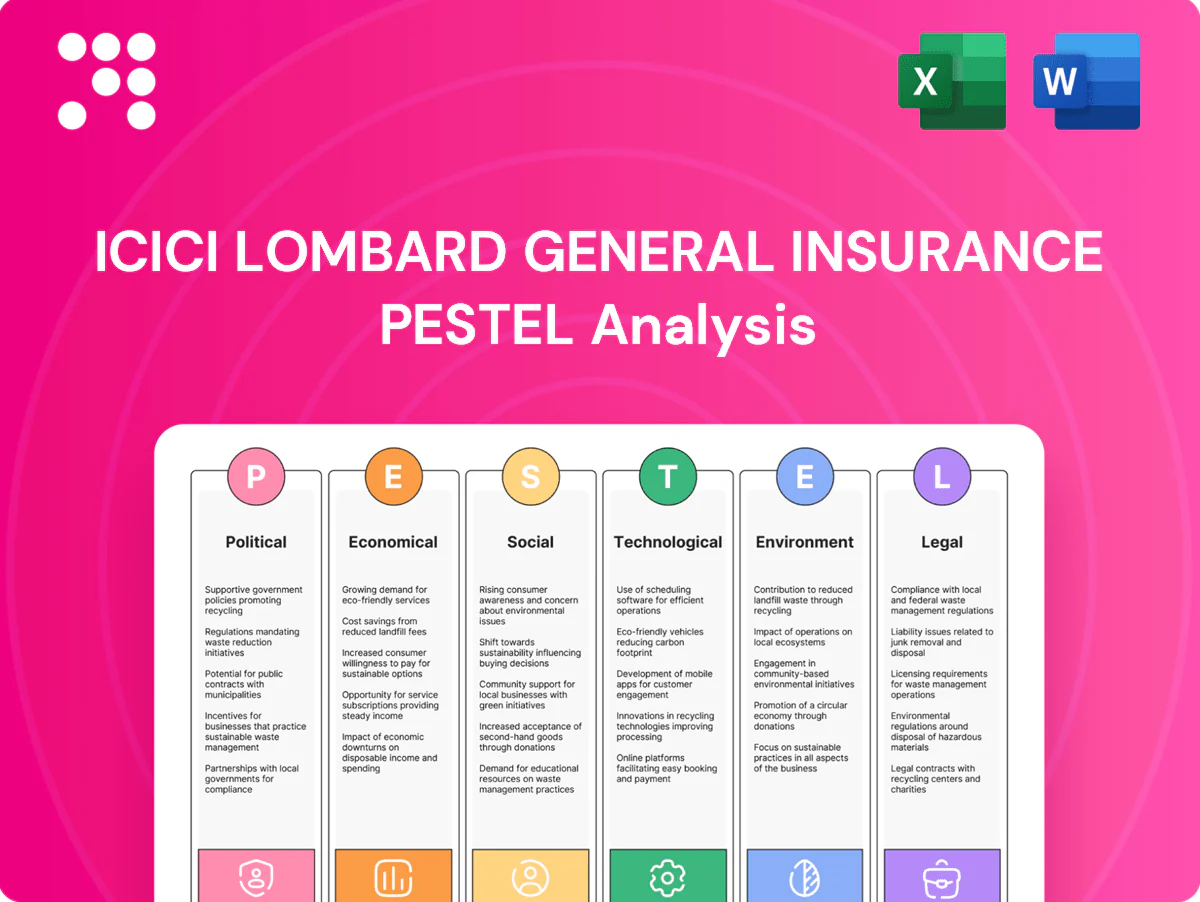

Political factors

IRDAI policy direction

IRDAI policy direction shapes ICICI Lombard product design, solvency norms (minimum solvency ratio 1.5) and pricing flexibility; pro-competition measures like use & file and the regulatory sandbox (introduced 2019) speed launches but demand tight governance; frequent circulars force agile compliance and IT updates; alignment with IRDAI roadmaps steers growth focus toward health and micro-insurance.

Government insurance schemes

Participation in government programs such as Ayushman Bharat, which aims to cover about 500 million beneficiaries, can boost ICICI Lombard’s scale and brand but often brings lower margins and altered case mix and claim patterns. Tender dynamics and reimbursement timelines strain working capital, while coordination with public hospitals and TPAs is operationally intensive in a sector where public health spending is ~1.3% of GDP.

Motor and road safety policy

Mandatory third-party motor insurance under the Motor Vehicles Act drives penetration and enlarges premium pools as enforcement improves, with India recording about 151,113 road fatalities in 2021 (NCRB), underpinning demand for cover. Scrappage policy introduced in 2021, higher traffic fines and safety initiatives lower claim frequency but can raise average claim severity. Electrification incentives (FAME era) shift risk profiles and repair costs upward due to battery damage and specialist parts, while policy stability aids pricing and reserving.

Public-sector competition and privatization

Policy stance toward PSU insurers reshapes market-share and pricing discipline; IRDAI reported gross direct premium at INR 2.13 lakh crore in FY24, with ICICI Lombard GWP ~INR 29,000 crore, so PSU recapitalization or consolidation can materially change competitive intensity. Government distribution tie-ups (post offices, welfare schemes) give PSUs access advantages, while political priorities often push product focus toward financial inclusion over pure profitability.

Geopolitical and fiscal priorities

Budgetary shifts such as the 2024 Union Budget's elevated capital expenditure of ₹11.1 lakh crore and increased health outlays drive demand for commercial and retail covers, while the 2024 general election reshuffled subsidy and compliance priorities. Trade and geopolitical tensions tightened reinsurance capacity post-2022–24 catastrophe losses, pushing reinsurer pricing up (~15% in 2024). Macroeconomic anchors—inflation and rate policy—keep premium growth volatile.

- ₹11.1 lakh crore capex raises commercial insurance demand

- 2024 election altered subsidy/compliance regimes

- Reinsurance pricing up ~15% (2024)

- Inflation/rate policy anchor premium volatility

IRDAI squeeze: solvency 1.5, Ayushman 500m, reins +15%

Political factors: IRDAI rules (minimum solvency ratio 1.5) and sandbox speed product launches; government schemes (Ayushman Bharat ~500 million) expand scale but compress margins; mandatory third-party cover and 151,113 road deaths (2021) sustain demand; 2024 capex ₹11.1 lakh crore and ~15% reinsurance price rise (2024) tighten pricing and capital.

| Indicator | Value |

|---|---|

| IRDAI solvency | 1.5 |

| IR gross direct premium FY24 | ₹2.13 lakh crore |

| ICICI Lombard GWP FY24 | ~₹29,000 crore |

| Ayushman Bharat reach | ~500m |

| Reinsurance price change (2024) | +15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ICICI Lombard General Insurance across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section uses current market and regulatory data to identify risks, opportunities and forward-looking insights for executives, investors and strategists.

A compact, visually segmented PESTLE summary for ICICI Lombard that highlights external risks and opportunities, easily dropped into presentations, shared across teams, and annotated for local/regional context—streamlining planning, compliance discussions and strategic decision-making.

Economic factors

GDP growth and insurance penetration

Economic expansion—India growing around 7% annually into 2024–25—boosts insurable assets and discretionary spend, while non-life insurance penetration remains low (under 1% of GDP), offering runway for ICICI Lombard; SME formation (SMEs contribute roughly 30% of GDP and employ over 100 million) lifts commercial lines demand, but macro downturns increase lapse risk and customer price sensitivity, making growth cyclical and income-dependent.

Inflation and medical cost trend

Healthcare inflation has been running materially above headline CPI — roughly 9–10% vs CPI around 5–6% in recent 2023–24 data — pressuring ICICI Lombard health loss ratios and forcing repricing cycles. Rising provider tariffs and pharmaceutical costs require frequent product redesign and rate resets. Motor spare-parts and repair costs up ~6–8% boost claim severity. Reserving assumptions must embed persistence of these trends.

Interest rates and investment income

Insurers like ICICI Lombard depend on investment returns to offset underwriting cycles; with RBI policy rate at 6.5% and 10-year G-sec near 7.2% (mid-2025) yield curve shifts materially change book yields, duration strategy and solvency metrics. Higher rates boost investment income but mark-to-market drags asset valuations. Strong asset-liability management is therefore vital for solvency (regulatory minimum 150%) and long-tail motor/health liabilities.

Auto sales and credit cycles

New vehicle sales and rising financing penetration remain primary drivers of motor premium growth for ICICI Lombard, with higher loan origination increasing policy tie-ins via bancassurance.

Credit quality affects bancassurance throughput and premium collections, while cycles in construction, logistics and manufacturing shape demand for commercial lines and fleet cover.

Supply-chain shocks disrupt parts availability, raising repair costs and loss ratios, pressuring underwriting and pricing.

- motor growth: linked to new vehicle sales and finance penetration

- credit risk: impacts bancassurance sales and collections

- sector cycles: construction/logistics/manufacturing drive commercial premiums

- supply shocks: increase parts costs and claim severity

Reinsurance pricing and capacity

Global catastrophe-driven treaty terms tightened after consecutive loss years, with Aon reporting average reinsurance rate increases of 20–45% at 2023–24 renewals, pushing higher cession costs and elevated retention levels for property and specialty lines.

Exchange rate moves matter: USD/INR traded near 83 in mid-2025, raising offshore reinsurance expenses for ICICI Lombard and increasing INR-denominated cost volatility.

Careful panel selection and diversification of reinsurers remain key to mitigate capacity swings and protect solvency metrics.

- Aon 2024: reinsurance rates +20–45%

- USD/INR ~83 (mid-2025)

- Higher cession costs → increased retentions

- Panel diversification reduces volatility

IRDAI squeeze: solvency 1.5, Ayushman 500m, reins +15%

India GDP ~7% (2024–25) and sub‑1% non‑life penetration create growth runway; SMEs (~30% of GDP; 100m+ employed) lift commercial demand but macro shocks raise lapses. Healthcare inflation ~9–10% vs CPI 5–6% (2023–24) and motor repair inflation 6–8% increase loss severity. RBI policy rate ~6.5% and 10y G‑sec ~7.2% (mid‑2025) improve investment yield but raise MTM volatility; reinsurance rates +20–45% (Aon 2024) and USD/INR ~83 raise cession costs.

| Metric | Value |

|---|---|

| GDP growth | ~7% (2024–25) |

| Non‑life penetration | <1% of GDP |

| SME share/employment | ~30% GDP; 100m+ employed |

| Healthcare inflation | 9–10% (2023–24) |

| RBI policy / 10y G‑sec | 6.5% / ~7.2% (mid‑2025) |

| Reinsurance rate change | +20–45% (Aon 2024) |

| USD/INR | ~83 (mid‑2025) |

What You See Is What You Get

ICICI Lombard General Insurance PESTLE Analysis

The ICICI Lombard General Insurance PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal, and environmental factors shaping the insurer’s strategy and risks. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It’s comprehensive, actionable, and downloadable immediately upon payment.

Skip the Research. Get the Strategy.

Unlock competitive advantage with our PESTLE Analysis of ICICI Lombard General Insurance—concise, actionable, and built for decision-makers. Discover how political, economic, social, technological, legal, and environmental forces shape the firm's strategy and risk profile. Purchase the full report to access deep-dive insights and ready-to-use recommendations.

Political factors

IRDAI policy direction

IRDAI policy direction shapes ICICI Lombard product design, solvency norms (minimum solvency ratio 1.5) and pricing flexibility; pro-competition measures like use & file and the regulatory sandbox (introduced 2019) speed launches but demand tight governance; frequent circulars force agile compliance and IT updates; alignment with IRDAI roadmaps steers growth focus toward health and micro-insurance.

Government insurance schemes

Participation in government programs such as Ayushman Bharat, which aims to cover about 500 million beneficiaries, can boost ICICI Lombard’s scale and brand but often brings lower margins and altered case mix and claim patterns. Tender dynamics and reimbursement timelines strain working capital, while coordination with public hospitals and TPAs is operationally intensive in a sector where public health spending is ~1.3% of GDP.

Motor and road safety policy

Mandatory third-party motor insurance under the Motor Vehicles Act drives penetration and enlarges premium pools as enforcement improves, with India recording about 151,113 road fatalities in 2021 (NCRB), underpinning demand for cover. Scrappage policy introduced in 2021, higher traffic fines and safety initiatives lower claim frequency but can raise average claim severity. Electrification incentives (FAME era) shift risk profiles and repair costs upward due to battery damage and specialist parts, while policy stability aids pricing and reserving.

Public-sector competition and privatization

Policy stance toward PSU insurers reshapes market-share and pricing discipline; IRDAI reported gross direct premium at INR 2.13 lakh crore in FY24, with ICICI Lombard GWP ~INR 29,000 crore, so PSU recapitalization or consolidation can materially change competitive intensity. Government distribution tie-ups (post offices, welfare schemes) give PSUs access advantages, while political priorities often push product focus toward financial inclusion over pure profitability.

Geopolitical and fiscal priorities

Budgetary shifts such as the 2024 Union Budget's elevated capital expenditure of ₹11.1 lakh crore and increased health outlays drive demand for commercial and retail covers, while the 2024 general election reshuffled subsidy and compliance priorities. Trade and geopolitical tensions tightened reinsurance capacity post-2022–24 catastrophe losses, pushing reinsurer pricing up (~15% in 2024). Macroeconomic anchors—inflation and rate policy—keep premium growth volatile.

- ₹11.1 lakh crore capex raises commercial insurance demand

- 2024 election altered subsidy/compliance regimes

- Reinsurance pricing up ~15% (2024)

- Inflation/rate policy anchor premium volatility

IRDAI squeeze: solvency 1.5, Ayushman 500m, reins +15%

Political factors: IRDAI rules (minimum solvency ratio 1.5) and sandbox speed product launches; government schemes (Ayushman Bharat ~500 million) expand scale but compress margins; mandatory third-party cover and 151,113 road deaths (2021) sustain demand; 2024 capex ₹11.1 lakh crore and ~15% reinsurance price rise (2024) tighten pricing and capital.

| Indicator | Value |

|---|---|

| IRDAI solvency | 1.5 |

| IR gross direct premium FY24 | ₹2.13 lakh crore |

| ICICI Lombard GWP FY24 | ~₹29,000 crore |

| Ayushman Bharat reach | ~500m |

| Reinsurance price change (2024) | +15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ICICI Lombard General Insurance across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section uses current market and regulatory data to identify risks, opportunities and forward-looking insights for executives, investors and strategists.

A compact, visually segmented PESTLE summary for ICICI Lombard that highlights external risks and opportunities, easily dropped into presentations, shared across teams, and annotated for local/regional context—streamlining planning, compliance discussions and strategic decision-making.

Economic factors

GDP growth and insurance penetration

Economic expansion—India growing around 7% annually into 2024–25—boosts insurable assets and discretionary spend, while non-life insurance penetration remains low (under 1% of GDP), offering runway for ICICI Lombard; SME formation (SMEs contribute roughly 30% of GDP and employ over 100 million) lifts commercial lines demand, but macro downturns increase lapse risk and customer price sensitivity, making growth cyclical and income-dependent.

Inflation and medical cost trend

Healthcare inflation has been running materially above headline CPI — roughly 9–10% vs CPI around 5–6% in recent 2023–24 data — pressuring ICICI Lombard health loss ratios and forcing repricing cycles. Rising provider tariffs and pharmaceutical costs require frequent product redesign and rate resets. Motor spare-parts and repair costs up ~6–8% boost claim severity. Reserving assumptions must embed persistence of these trends.

Interest rates and investment income

Insurers like ICICI Lombard depend on investment returns to offset underwriting cycles; with RBI policy rate at 6.5% and 10-year G-sec near 7.2% (mid-2025) yield curve shifts materially change book yields, duration strategy and solvency metrics. Higher rates boost investment income but mark-to-market drags asset valuations. Strong asset-liability management is therefore vital for solvency (regulatory minimum 150%) and long-tail motor/health liabilities.

Auto sales and credit cycles

New vehicle sales and rising financing penetration remain primary drivers of motor premium growth for ICICI Lombard, with higher loan origination increasing policy tie-ins via bancassurance.

Credit quality affects bancassurance throughput and premium collections, while cycles in construction, logistics and manufacturing shape demand for commercial lines and fleet cover.

Supply-chain shocks disrupt parts availability, raising repair costs and loss ratios, pressuring underwriting and pricing.

- motor growth: linked to new vehicle sales and finance penetration

- credit risk: impacts bancassurance sales and collections

- sector cycles: construction/logistics/manufacturing drive commercial premiums

- supply shocks: increase parts costs and claim severity

Reinsurance pricing and capacity

Global catastrophe-driven treaty terms tightened after consecutive loss years, with Aon reporting average reinsurance rate increases of 20–45% at 2023–24 renewals, pushing higher cession costs and elevated retention levels for property and specialty lines.

Exchange rate moves matter: USD/INR traded near 83 in mid-2025, raising offshore reinsurance expenses for ICICI Lombard and increasing INR-denominated cost volatility.

Careful panel selection and diversification of reinsurers remain key to mitigate capacity swings and protect solvency metrics.

- Aon 2024: reinsurance rates +20–45%

- USD/INR ~83 (mid-2025)

- Higher cession costs → increased retentions

- Panel diversification reduces volatility

IRDAI squeeze: solvency 1.5, Ayushman 500m, reins +15%

India GDP ~7% (2024–25) and sub‑1% non‑life penetration create growth runway; SMEs (~30% of GDP; 100m+ employed) lift commercial demand but macro shocks raise lapses. Healthcare inflation ~9–10% vs CPI 5–6% (2023–24) and motor repair inflation 6–8% increase loss severity. RBI policy rate ~6.5% and 10y G‑sec ~7.2% (mid‑2025) improve investment yield but raise MTM volatility; reinsurance rates +20–45% (Aon 2024) and USD/INR ~83 raise cession costs.

| Metric | Value |

|---|---|

| GDP growth | ~7% (2024–25) |

| Non‑life penetration | <1% of GDP |

| SME share/employment | ~30% GDP; 100m+ employed |

| Healthcare inflation | 9–10% (2023–24) |

| RBI policy / 10y G‑sec | 6.5% / ~7.2% (mid‑2025) |

| Reinsurance rate change | +20–45% (Aon 2024) |

| USD/INR | ~83 (mid‑2025) |

What You See Is What You Get

ICICI Lombard General Insurance PESTLE Analysis

The ICICI Lombard General Insurance PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal, and environmental factors shaping the insurer’s strategy and risks. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It’s comprehensive, actionable, and downloadable immediately upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Unlock competitive advantage with our PESTLE Analysis of ICICI Lombard General Insurance—concise, actionable, and built for decision-makers. Discover how political, economic, social, technological, legal, and environmental forces shape the firm's strategy and risk profile. Purchase the full report to access deep-dive insights and ready-to-use recommendations.

Political factors

IRDAI policy direction

IRDAI policy direction shapes ICICI Lombard product design, solvency norms (minimum solvency ratio 1.5) and pricing flexibility; pro-competition measures like use & file and the regulatory sandbox (introduced 2019) speed launches but demand tight governance; frequent circulars force agile compliance and IT updates; alignment with IRDAI roadmaps steers growth focus toward health and micro-insurance.

Government insurance schemes

Participation in government programs such as Ayushman Bharat, which aims to cover about 500 million beneficiaries, can boost ICICI Lombard’s scale and brand but often brings lower margins and altered case mix and claim patterns. Tender dynamics and reimbursement timelines strain working capital, while coordination with public hospitals and TPAs is operationally intensive in a sector where public health spending is ~1.3% of GDP.

Motor and road safety policy

Mandatory third-party motor insurance under the Motor Vehicles Act drives penetration and enlarges premium pools as enforcement improves, with India recording about 151,113 road fatalities in 2021 (NCRB), underpinning demand for cover. Scrappage policy introduced in 2021, higher traffic fines and safety initiatives lower claim frequency but can raise average claim severity. Electrification incentives (FAME era) shift risk profiles and repair costs upward due to battery damage and specialist parts, while policy stability aids pricing and reserving.

Public-sector competition and privatization

Policy stance toward PSU insurers reshapes market-share and pricing discipline; IRDAI reported gross direct premium at INR 2.13 lakh crore in FY24, with ICICI Lombard GWP ~INR 29,000 crore, so PSU recapitalization or consolidation can materially change competitive intensity. Government distribution tie-ups (post offices, welfare schemes) give PSUs access advantages, while political priorities often push product focus toward financial inclusion over pure profitability.

Geopolitical and fiscal priorities

Budgetary shifts such as the 2024 Union Budget's elevated capital expenditure of ₹11.1 lakh crore and increased health outlays drive demand for commercial and retail covers, while the 2024 general election reshuffled subsidy and compliance priorities. Trade and geopolitical tensions tightened reinsurance capacity post-2022–24 catastrophe losses, pushing reinsurer pricing up (~15% in 2024). Macroeconomic anchors—inflation and rate policy—keep premium growth volatile.

- ₹11.1 lakh crore capex raises commercial insurance demand

- 2024 election altered subsidy/compliance regimes

- Reinsurance pricing up ~15% (2024)

- Inflation/rate policy anchor premium volatility

IRDAI squeeze: solvency 1.5, Ayushman 500m, reins +15%

Political factors: IRDAI rules (minimum solvency ratio 1.5) and sandbox speed product launches; government schemes (Ayushman Bharat ~500 million) expand scale but compress margins; mandatory third-party cover and 151,113 road deaths (2021) sustain demand; 2024 capex ₹11.1 lakh crore and ~15% reinsurance price rise (2024) tighten pricing and capital.

| Indicator | Value |

|---|---|

| IRDAI solvency | 1.5 |

| IR gross direct premium FY24 | ₹2.13 lakh crore |

| ICICI Lombard GWP FY24 | ~₹29,000 crore |

| Ayushman Bharat reach | ~500m |

| Reinsurance price change (2024) | +15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect ICICI Lombard General Insurance across Political, Economic, Social, Technological, Environmental and Legal dimensions; each section uses current market and regulatory data to identify risks, opportunities and forward-looking insights for executives, investors and strategists.

A compact, visually segmented PESTLE summary for ICICI Lombard that highlights external risks and opportunities, easily dropped into presentations, shared across teams, and annotated for local/regional context—streamlining planning, compliance discussions and strategic decision-making.

Economic factors

GDP growth and insurance penetration

Economic expansion—India growing around 7% annually into 2024–25—boosts insurable assets and discretionary spend, while non-life insurance penetration remains low (under 1% of GDP), offering runway for ICICI Lombard; SME formation (SMEs contribute roughly 30% of GDP and employ over 100 million) lifts commercial lines demand, but macro downturns increase lapse risk and customer price sensitivity, making growth cyclical and income-dependent.

Inflation and medical cost trend

Healthcare inflation has been running materially above headline CPI — roughly 9–10% vs CPI around 5–6% in recent 2023–24 data — pressuring ICICI Lombard health loss ratios and forcing repricing cycles. Rising provider tariffs and pharmaceutical costs require frequent product redesign and rate resets. Motor spare-parts and repair costs up ~6–8% boost claim severity. Reserving assumptions must embed persistence of these trends.

Interest rates and investment income

Insurers like ICICI Lombard depend on investment returns to offset underwriting cycles; with RBI policy rate at 6.5% and 10-year G-sec near 7.2% (mid-2025) yield curve shifts materially change book yields, duration strategy and solvency metrics. Higher rates boost investment income but mark-to-market drags asset valuations. Strong asset-liability management is therefore vital for solvency (regulatory minimum 150%) and long-tail motor/health liabilities.

Auto sales and credit cycles

New vehicle sales and rising financing penetration remain primary drivers of motor premium growth for ICICI Lombard, with higher loan origination increasing policy tie-ins via bancassurance.

Credit quality affects bancassurance throughput and premium collections, while cycles in construction, logistics and manufacturing shape demand for commercial lines and fleet cover.

Supply-chain shocks disrupt parts availability, raising repair costs and loss ratios, pressuring underwriting and pricing.

- motor growth: linked to new vehicle sales and finance penetration

- credit risk: impacts bancassurance sales and collections

- sector cycles: construction/logistics/manufacturing drive commercial premiums

- supply shocks: increase parts costs and claim severity

Reinsurance pricing and capacity

Global catastrophe-driven treaty terms tightened after consecutive loss years, with Aon reporting average reinsurance rate increases of 20–45% at 2023–24 renewals, pushing higher cession costs and elevated retention levels for property and specialty lines.

Exchange rate moves matter: USD/INR traded near 83 in mid-2025, raising offshore reinsurance expenses for ICICI Lombard and increasing INR-denominated cost volatility.

Careful panel selection and diversification of reinsurers remain key to mitigate capacity swings and protect solvency metrics.

- Aon 2024: reinsurance rates +20–45%

- USD/INR ~83 (mid-2025)

- Higher cession costs → increased retentions

- Panel diversification reduces volatility

IRDAI squeeze: solvency 1.5, Ayushman 500m, reins +15%

India GDP ~7% (2024–25) and sub‑1% non‑life penetration create growth runway; SMEs (~30% of GDP; 100m+ employed) lift commercial demand but macro shocks raise lapses. Healthcare inflation ~9–10% vs CPI 5–6% (2023–24) and motor repair inflation 6–8% increase loss severity. RBI policy rate ~6.5% and 10y G‑sec ~7.2% (mid‑2025) improve investment yield but raise MTM volatility; reinsurance rates +20–45% (Aon 2024) and USD/INR ~83 raise cession costs.

| Metric | Value |

|---|---|

| GDP growth | ~7% (2024–25) |

| Non‑life penetration | <1% of GDP |

| SME share/employment | ~30% GDP; 100m+ employed |

| Healthcare inflation | 9–10% (2023–24) |

| RBI policy / 10y G‑sec | 6.5% / ~7.2% (mid‑2025) |

| Reinsurance rate change | +20–45% (Aon 2024) |

| USD/INR | ~83 (mid‑2025) |

What You See Is What You Get

ICICI Lombard General Insurance PESTLE Analysis

The ICICI Lombard General Insurance PESTLE Analysis provides a concise assessment of political, economic, social, technological, legal, and environmental factors shaping the insurer’s strategy and risks. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It’s comprehensive, actionable, and downloadable immediately upon payment.