ICZ AS Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

ICZ AS faces moderate supplier influence, niche buyer dynamics, and niche-specific substitute risks that shape its competitive positioning; pockets of regulatory and technological pressure suggest strategic focus areas. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis to get actionable, consultant-grade insights and the data you need to guide investment or strategy decisions.

Suppliers Bargaining Power

Reliance on hyperscalers

ICZ’s dependence on IaaS/PaaS leaves hyperscalers with pricing leverage; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 33%, 22% and 11% of the market (Canalys 2024), enabling contract terms, volume commitments and egress fees that can lock architectures. Multi-cloud designs and framework agreements reduce exposure, but specialist services (AI/ML, cloud-native security) remain hard to substitute, sustaining supplier power; Google offers committed-use discounts up to ~57%.

Specialized software vendors

Core stacks (databases, middleware, EHR modules, identity) are concentrated, with the top 3 enterprise DB/infra vendors accounting for over 50% of market share, and certification requirements common. License models and audits drive recurring cost pressure — enterprise licenses and audit penalties can add double-digit percent to project TCO. Long integration cycles increase switching costs and time-to-value. Bundling across projects and reference status materially improves negotiation leverage.

Scarce skilled talent

Senior developers, solution architects and security specialists act as critical suppliers for ICZ AS, and tight CEE labor markets push wage demands and attrition risk higher, with Korn Ferry projecting an 85 million global talent shortfall by 2030 as context for sustained pressure.

Project timelines for e-government and healthcare implementations depend on retaining these domain experts, where single departures can delay deliveries by months.

Strategic sourcing, internal academies and nearshoring are practical levers to rebalance supplier power and contain cost and schedule volatility.

Data and interoperability providers

Access to registries, payment rails and healthcare interfaces is often controlled by authorities or vendors (eg NHS Digital APIs and FHIR mandates in 2024), and API terms, SLAs and certification gates directly shape delivery schedules and penalties. Vendor-specific connectors entrench dependencies and raise switching costs, while reusable adapters reduce lock-in severity.

- Authority-controlled APIs: NHS Digital, payer gateways

- Standard: HL7 FHIR (2024 widespread)

- Risk: vendor connector lock-in

- Mitigation: reusable adapters

Cybersecurity and compliance tools

Sector work mandates certified security products and audit tooling for government and healthcare, and limited approved-vendor lists increase supplier leverage; regulatory updates in 2024 drive frequent upgrade cycles on supplier timelines, while framework contracts (typically 3–5 years) and alternative approved products partially constrain that power.

- Certified tooling required

- Limited approved vendors

- 2024: regulatory-driven upgrades

- Framework contracts 3–5 years

CEE techs hit by hyperscaler pricing, cloud lock-in and 85m talent gap

ICZ faces strong supplier power: hyperscalers (AWS 33%, Azure 22%, GCP 11% Canalys 2024) set pricing, egress fees and committed-use discounts (GCP up to ~57%), while top-3 enterprise infra vendors hold >50% share and enterprise licensing/audits add recurring TCO. CEE tech talent shortages and Korn Ferry’s 85m 2030 gap raise wage/attrition risk, and authority-controlled APIs/FHIR (widespread 2024) increase vendor lock-in.

| Item | 2024/Stat |

|---|---|

| Hyperscaler share | AWS 33% / Azure 22% / GCP 11% (Canalys 2024) |

| GCP discount | Committed-use up to ~57% |

| Top-3 infra | >50% market share |

| Talent gap | Korn Ferry 85m by 2030 |

| Standards/APIs | HL7 FHIR widespread 2024 |

| Frameworks | 3–5 year contracts |

What is included in the product

Tailored Porter's Five Forces analysis for ICZ AS that uncovers competitive drivers, buyer and supplier power, substitution risks and entry barriers, highlighting disruptive threats and strategic levers affecting its pricing, margins and market position.

A concise one-sheet Porter's Five Forces for ICZ AS—instantly visualizes competitive pressure with a radar chart, easy to copy into decks and tweak with your own data or scenarios for rapid decision-making.

Customers Bargaining Power

Public sector procurement leverage

Public buyers run competitive tenders with strict price weighting—price often accounts for 60% or more of award criteria—pressuring ICZ AS margins. EU public procurement remains large (around €2.3 trillion market value in recent years), and framework agreements aggregate demand, squeezing suppliers through long-term discounted rates. Transparency and challenge rights frequently delay awards and increase bid risk, while complex IT and systems scopes still allow ICZ AS to pursue value-based differentiation and higher-margin solutions.

Enterprise buyers with options

Banks and large healthcare providers benchmark integrators regionally and, as of 2024, increasingly multisource or split lots to drive competition and lower bids. Strong vendor management programs extract deeper discounts and compress margins for integrators. ICZ can offset price pressure by offering outcome SLAs (eg, 99.9% uptime, measured KPIs) and proprietary domain IP that ties value to outcomes rather than price.

High switching costs in mission systems

Critical e-government and hospital systems have deep process and data ties, creating high switching costs that deter migration; healthcare IT market scale — about $185 billion in 2024 — underscores the heavy investment embedded in mission systems. Migration risk, retraining, and compliance testing (often taking 6–18 months) raise barriers to change, yet buyers still press for 5–15% price concessions at renewal. Referenceable performance and documented continuity reduce churn threats and strengthen vendor negotiating power.

Demand for interoperability and open standards

Buyers mandate open APIs and standards-compliant solutions to avoid lock-in, broadening their supplier pool and increasing bargaining power; the global API management market was estimated at about USD 6.3B in 2024, underscoring demand. Compliance imposes extra engineering effort for ICZ, but showcasing reusable integration assets and reference connectors can reclaim value and support higher-margin services.

- avoids lock-in

- broadens suppliers

- requires extra engineering

- reuse assets reclaim value

Budget cycles and payment terms

Public budgets and capex approvals in 2024 commonly add 3–6 months to procurement timelines, favoring milestone payments; extended payment terms shift working capital burdens onto vendors and compress vendor margins. Buyers increasingly insert delay penalties (often 0.5–1.5% per week) and demand phased delivery or modular scopes to balance cash flow and project risk.

- Capex delays: 3–6 months

- Working capital shift: higher receivables

- Penalties: 0.5–1.5%/week

- Mitigation: phased delivery/modular scopes

EU tenders, API mandates and capex delays force 5–15% renewal cuts

Public tenders (EU procurement ~€2.3T) and bank/healthcare benchmarking drive aggressive price weighting, compressing ICZ AS margins. High switching costs in e-gov and healthcare (healthcare IT market ~$185B in 2024) limit churn but buyers still demand 5–15% renewals discounts. Open-API mandates (API mgmt ~$6.3B in 2024), capex delays (3–6 months) and penalties (0.5–1.5%/week) increase buyer leverage.

| Metric | 2024 Value |

|---|---|

| EU public procurement | €2.3T |

| Healthcare IT market | $185B |

| API management | $6.3B |

| Capex delays | 3–6 months |

| Renewal discount pressure | 5–15% |

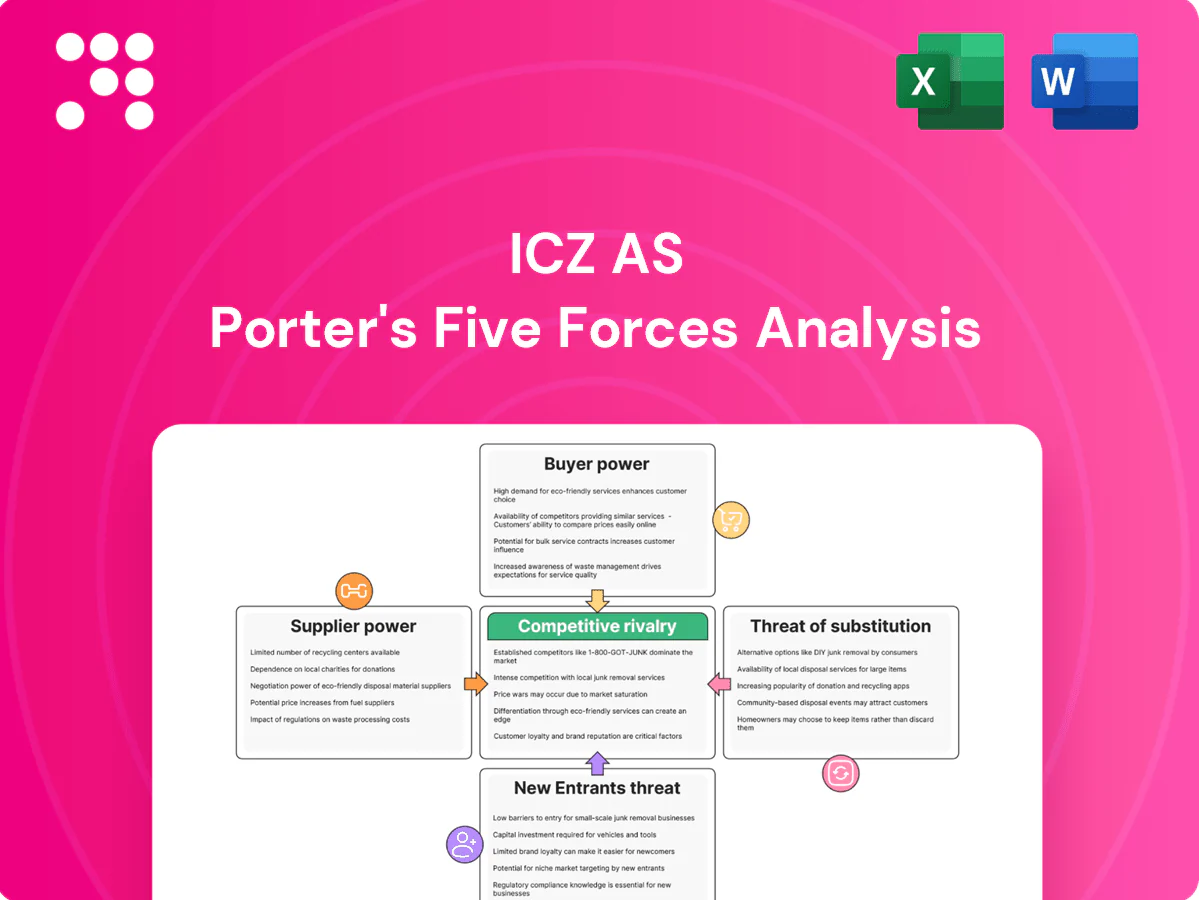

What You See Is What You Get

ICZ AS Porter's Five Forces Analysis

This preview shows the exact ICZ AS Porter's Five Forces analysis you'll receive after purchase—fully formatted, professional, and ready to use. It is the complete deliverable, not a sample or placeholder, and will be available for immediate download upon payment. Use it as-is for decision-making, presentations, or further research.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

ICZ AS faces moderate supplier influence, niche buyer dynamics, and niche-specific substitute risks that shape its competitive positioning; pockets of regulatory and technological pressure suggest strategic focus areas. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis to get actionable, consultant-grade insights and the data you need to guide investment or strategy decisions.

Suppliers Bargaining Power

Reliance on hyperscalers

ICZ’s dependence on IaaS/PaaS leaves hyperscalers with pricing leverage; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 33%, 22% and 11% of the market (Canalys 2024), enabling contract terms, volume commitments and egress fees that can lock architectures. Multi-cloud designs and framework agreements reduce exposure, but specialist services (AI/ML, cloud-native security) remain hard to substitute, sustaining supplier power; Google offers committed-use discounts up to ~57%.

Specialized software vendors

Core stacks (databases, middleware, EHR modules, identity) are concentrated, with the top 3 enterprise DB/infra vendors accounting for over 50% of market share, and certification requirements common. License models and audits drive recurring cost pressure — enterprise licenses and audit penalties can add double-digit percent to project TCO. Long integration cycles increase switching costs and time-to-value. Bundling across projects and reference status materially improves negotiation leverage.

Scarce skilled talent

Senior developers, solution architects and security specialists act as critical suppliers for ICZ AS, and tight CEE labor markets push wage demands and attrition risk higher, with Korn Ferry projecting an 85 million global talent shortfall by 2030 as context for sustained pressure.

Project timelines for e-government and healthcare implementations depend on retaining these domain experts, where single departures can delay deliveries by months.

Strategic sourcing, internal academies and nearshoring are practical levers to rebalance supplier power and contain cost and schedule volatility.

Data and interoperability providers

Access to registries, payment rails and healthcare interfaces is often controlled by authorities or vendors (eg NHS Digital APIs and FHIR mandates in 2024), and API terms, SLAs and certification gates directly shape delivery schedules and penalties. Vendor-specific connectors entrench dependencies and raise switching costs, while reusable adapters reduce lock-in severity.

- Authority-controlled APIs: NHS Digital, payer gateways

- Standard: HL7 FHIR (2024 widespread)

- Risk: vendor connector lock-in

- Mitigation: reusable adapters

Cybersecurity and compliance tools

Sector work mandates certified security products and audit tooling for government and healthcare, and limited approved-vendor lists increase supplier leverage; regulatory updates in 2024 drive frequent upgrade cycles on supplier timelines, while framework contracts (typically 3–5 years) and alternative approved products partially constrain that power.

- Certified tooling required

- Limited approved vendors

- 2024: regulatory-driven upgrades

- Framework contracts 3–5 years

CEE techs hit by hyperscaler pricing, cloud lock-in and 85m talent gap

ICZ faces strong supplier power: hyperscalers (AWS 33%, Azure 22%, GCP 11% Canalys 2024) set pricing, egress fees and committed-use discounts (GCP up to ~57%), while top-3 enterprise infra vendors hold >50% share and enterprise licensing/audits add recurring TCO. CEE tech talent shortages and Korn Ferry’s 85m 2030 gap raise wage/attrition risk, and authority-controlled APIs/FHIR (widespread 2024) increase vendor lock-in.

| Item | 2024/Stat |

|---|---|

| Hyperscaler share | AWS 33% / Azure 22% / GCP 11% (Canalys 2024) |

| GCP discount | Committed-use up to ~57% |

| Top-3 infra | >50% market share |

| Talent gap | Korn Ferry 85m by 2030 |

| Standards/APIs | HL7 FHIR widespread 2024 |

| Frameworks | 3–5 year contracts |

What is included in the product

Tailored Porter's Five Forces analysis for ICZ AS that uncovers competitive drivers, buyer and supplier power, substitution risks and entry barriers, highlighting disruptive threats and strategic levers affecting its pricing, margins and market position.

A concise one-sheet Porter's Five Forces for ICZ AS—instantly visualizes competitive pressure with a radar chart, easy to copy into decks and tweak with your own data or scenarios for rapid decision-making.

Customers Bargaining Power

Public sector procurement leverage

Public buyers run competitive tenders with strict price weighting—price often accounts for 60% or more of award criteria—pressuring ICZ AS margins. EU public procurement remains large (around €2.3 trillion market value in recent years), and framework agreements aggregate demand, squeezing suppliers through long-term discounted rates. Transparency and challenge rights frequently delay awards and increase bid risk, while complex IT and systems scopes still allow ICZ AS to pursue value-based differentiation and higher-margin solutions.

Enterprise buyers with options

Banks and large healthcare providers benchmark integrators regionally and, as of 2024, increasingly multisource or split lots to drive competition and lower bids. Strong vendor management programs extract deeper discounts and compress margins for integrators. ICZ can offset price pressure by offering outcome SLAs (eg, 99.9% uptime, measured KPIs) and proprietary domain IP that ties value to outcomes rather than price.

High switching costs in mission systems

Critical e-government and hospital systems have deep process and data ties, creating high switching costs that deter migration; healthcare IT market scale — about $185 billion in 2024 — underscores the heavy investment embedded in mission systems. Migration risk, retraining, and compliance testing (often taking 6–18 months) raise barriers to change, yet buyers still press for 5–15% price concessions at renewal. Referenceable performance and documented continuity reduce churn threats and strengthen vendor negotiating power.

Demand for interoperability and open standards

Buyers mandate open APIs and standards-compliant solutions to avoid lock-in, broadening their supplier pool and increasing bargaining power; the global API management market was estimated at about USD 6.3B in 2024, underscoring demand. Compliance imposes extra engineering effort for ICZ, but showcasing reusable integration assets and reference connectors can reclaim value and support higher-margin services.

- avoids lock-in

- broadens suppliers

- requires extra engineering

- reuse assets reclaim value

Budget cycles and payment terms

Public budgets and capex approvals in 2024 commonly add 3–6 months to procurement timelines, favoring milestone payments; extended payment terms shift working capital burdens onto vendors and compress vendor margins. Buyers increasingly insert delay penalties (often 0.5–1.5% per week) and demand phased delivery or modular scopes to balance cash flow and project risk.

- Capex delays: 3–6 months

- Working capital shift: higher receivables

- Penalties: 0.5–1.5%/week

- Mitigation: phased delivery/modular scopes

EU tenders, API mandates and capex delays force 5–15% renewal cuts

Public tenders (EU procurement ~€2.3T) and bank/healthcare benchmarking drive aggressive price weighting, compressing ICZ AS margins. High switching costs in e-gov and healthcare (healthcare IT market ~$185B in 2024) limit churn but buyers still demand 5–15% renewals discounts. Open-API mandates (API mgmt ~$6.3B in 2024), capex delays (3–6 months) and penalties (0.5–1.5%/week) increase buyer leverage.

| Metric | 2024 Value |

|---|---|

| EU public procurement | €2.3T |

| Healthcare IT market | $185B |

| API management | $6.3B |

| Capex delays | 3–6 months |

| Renewal discount pressure | 5–15% |

What You See Is What You Get

ICZ AS Porter's Five Forces Analysis

This preview shows the exact ICZ AS Porter's Five Forces analysis you'll receive after purchase—fully formatted, professional, and ready to use. It is the complete deliverable, not a sample or placeholder, and will be available for immediate download upon payment. Use it as-is for decision-making, presentations, or further research.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

ICZ AS faces moderate supplier influence, niche buyer dynamics, and niche-specific substitute risks that shape its competitive positioning; pockets of regulatory and technological pressure suggest strategic focus areas. This snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter’s Five Forces Analysis to get actionable, consultant-grade insights and the data you need to guide investment or strategy decisions.

Suppliers Bargaining Power

Reliance on hyperscalers

ICZ’s dependence on IaaS/PaaS leaves hyperscalers with pricing leverage; in 2024 AWS, Microsoft Azure and Google Cloud held roughly 33%, 22% and 11% of the market (Canalys 2024), enabling contract terms, volume commitments and egress fees that can lock architectures. Multi-cloud designs and framework agreements reduce exposure, but specialist services (AI/ML, cloud-native security) remain hard to substitute, sustaining supplier power; Google offers committed-use discounts up to ~57%.

Specialized software vendors

Core stacks (databases, middleware, EHR modules, identity) are concentrated, with the top 3 enterprise DB/infra vendors accounting for over 50% of market share, and certification requirements common. License models and audits drive recurring cost pressure — enterprise licenses and audit penalties can add double-digit percent to project TCO. Long integration cycles increase switching costs and time-to-value. Bundling across projects and reference status materially improves negotiation leverage.

Scarce skilled talent

Senior developers, solution architects and security specialists act as critical suppliers for ICZ AS, and tight CEE labor markets push wage demands and attrition risk higher, with Korn Ferry projecting an 85 million global talent shortfall by 2030 as context for sustained pressure.

Project timelines for e-government and healthcare implementations depend on retaining these domain experts, where single departures can delay deliveries by months.

Strategic sourcing, internal academies and nearshoring are practical levers to rebalance supplier power and contain cost and schedule volatility.

Data and interoperability providers

Access to registries, payment rails and healthcare interfaces is often controlled by authorities or vendors (eg NHS Digital APIs and FHIR mandates in 2024), and API terms, SLAs and certification gates directly shape delivery schedules and penalties. Vendor-specific connectors entrench dependencies and raise switching costs, while reusable adapters reduce lock-in severity.

- Authority-controlled APIs: NHS Digital, payer gateways

- Standard: HL7 FHIR (2024 widespread)

- Risk: vendor connector lock-in

- Mitigation: reusable adapters

Cybersecurity and compliance tools

Sector work mandates certified security products and audit tooling for government and healthcare, and limited approved-vendor lists increase supplier leverage; regulatory updates in 2024 drive frequent upgrade cycles on supplier timelines, while framework contracts (typically 3–5 years) and alternative approved products partially constrain that power.

- Certified tooling required

- Limited approved vendors

- 2024: regulatory-driven upgrades

- Framework contracts 3–5 years

CEE techs hit by hyperscaler pricing, cloud lock-in and 85m talent gap

ICZ faces strong supplier power: hyperscalers (AWS 33%, Azure 22%, GCP 11% Canalys 2024) set pricing, egress fees and committed-use discounts (GCP up to ~57%), while top-3 enterprise infra vendors hold >50% share and enterprise licensing/audits add recurring TCO. CEE tech talent shortages and Korn Ferry’s 85m 2030 gap raise wage/attrition risk, and authority-controlled APIs/FHIR (widespread 2024) increase vendor lock-in.

| Item | 2024/Stat |

|---|---|

| Hyperscaler share | AWS 33% / Azure 22% / GCP 11% (Canalys 2024) |

| GCP discount | Committed-use up to ~57% |

| Top-3 infra | >50% market share |

| Talent gap | Korn Ferry 85m by 2030 |

| Standards/APIs | HL7 FHIR widespread 2024 |

| Frameworks | 3–5 year contracts |

What is included in the product

Tailored Porter's Five Forces analysis for ICZ AS that uncovers competitive drivers, buyer and supplier power, substitution risks and entry barriers, highlighting disruptive threats and strategic levers affecting its pricing, margins and market position.

A concise one-sheet Porter's Five Forces for ICZ AS—instantly visualizes competitive pressure with a radar chart, easy to copy into decks and tweak with your own data or scenarios for rapid decision-making.

Customers Bargaining Power

Public sector procurement leverage

Public buyers run competitive tenders with strict price weighting—price often accounts for 60% or more of award criteria—pressuring ICZ AS margins. EU public procurement remains large (around €2.3 trillion market value in recent years), and framework agreements aggregate demand, squeezing suppliers through long-term discounted rates. Transparency and challenge rights frequently delay awards and increase bid risk, while complex IT and systems scopes still allow ICZ AS to pursue value-based differentiation and higher-margin solutions.

Enterprise buyers with options

Banks and large healthcare providers benchmark integrators regionally and, as of 2024, increasingly multisource or split lots to drive competition and lower bids. Strong vendor management programs extract deeper discounts and compress margins for integrators. ICZ can offset price pressure by offering outcome SLAs (eg, 99.9% uptime, measured KPIs) and proprietary domain IP that ties value to outcomes rather than price.

High switching costs in mission systems

Critical e-government and hospital systems have deep process and data ties, creating high switching costs that deter migration; healthcare IT market scale — about $185 billion in 2024 — underscores the heavy investment embedded in mission systems. Migration risk, retraining, and compliance testing (often taking 6–18 months) raise barriers to change, yet buyers still press for 5–15% price concessions at renewal. Referenceable performance and documented continuity reduce churn threats and strengthen vendor negotiating power.

Demand for interoperability and open standards

Buyers mandate open APIs and standards-compliant solutions to avoid lock-in, broadening their supplier pool and increasing bargaining power; the global API management market was estimated at about USD 6.3B in 2024, underscoring demand. Compliance imposes extra engineering effort for ICZ, but showcasing reusable integration assets and reference connectors can reclaim value and support higher-margin services.

- avoids lock-in

- broadens suppliers

- requires extra engineering

- reuse assets reclaim value

Budget cycles and payment terms

Public budgets and capex approvals in 2024 commonly add 3–6 months to procurement timelines, favoring milestone payments; extended payment terms shift working capital burdens onto vendors and compress vendor margins. Buyers increasingly insert delay penalties (often 0.5–1.5% per week) and demand phased delivery or modular scopes to balance cash flow and project risk.

- Capex delays: 3–6 months

- Working capital shift: higher receivables

- Penalties: 0.5–1.5%/week

- Mitigation: phased delivery/modular scopes

EU tenders, API mandates and capex delays force 5–15% renewal cuts

Public tenders (EU procurement ~€2.3T) and bank/healthcare benchmarking drive aggressive price weighting, compressing ICZ AS margins. High switching costs in e-gov and healthcare (healthcare IT market ~$185B in 2024) limit churn but buyers still demand 5–15% renewals discounts. Open-API mandates (API mgmt ~$6.3B in 2024), capex delays (3–6 months) and penalties (0.5–1.5%/week) increase buyer leverage.

| Metric | 2024 Value |

|---|---|

| EU public procurement | €2.3T |

| Healthcare IT market | $185B |

| API management | $6.3B |

| Capex delays | 3–6 months |

| Renewal discount pressure | 5–15% |

What You See Is What You Get

ICZ AS Porter's Five Forces Analysis

This preview shows the exact ICZ AS Porter's Five Forces analysis you'll receive after purchase—fully formatted, professional, and ready to use. It is the complete deliverable, not a sample or placeholder, and will be available for immediate download upon payment. Use it as-is for decision-making, presentations, or further research.